Copyright 2026 First Samuel Limited

Read the previous Investment Matters here:

Before parsing the RBA’s decision to increase interest rates, we thought it useful to briefly comment on an optimistic view of Australia’s future.

Macquarie Bank’s CEO, Shemara Wikramanayake, opened its famous annual investment conference with confidence in markets and the future. What made her address more important this year was the theme that other presenters then built upon- a redefinition of Australia’s quality and future.

Australia as an investment destination is often reduced to banks, housing and iron ore, but the strategic picture is broader. The country has energy, land, minerals, infrastructure, rule of law, proximity to Asia and relatively low government debt. In a world paying more attention to supply chains, power availability, data centres and critical minerals, those advantages matter.

It is a theme we have hoped to capture in our portfolio for many years.

When we speak of the diversity of a basket of metals, minerals and mining services, Shemara suggest Australia held the “periodic table” in its hands. A reference to the table of all elements you may have learnt about in secondary school.

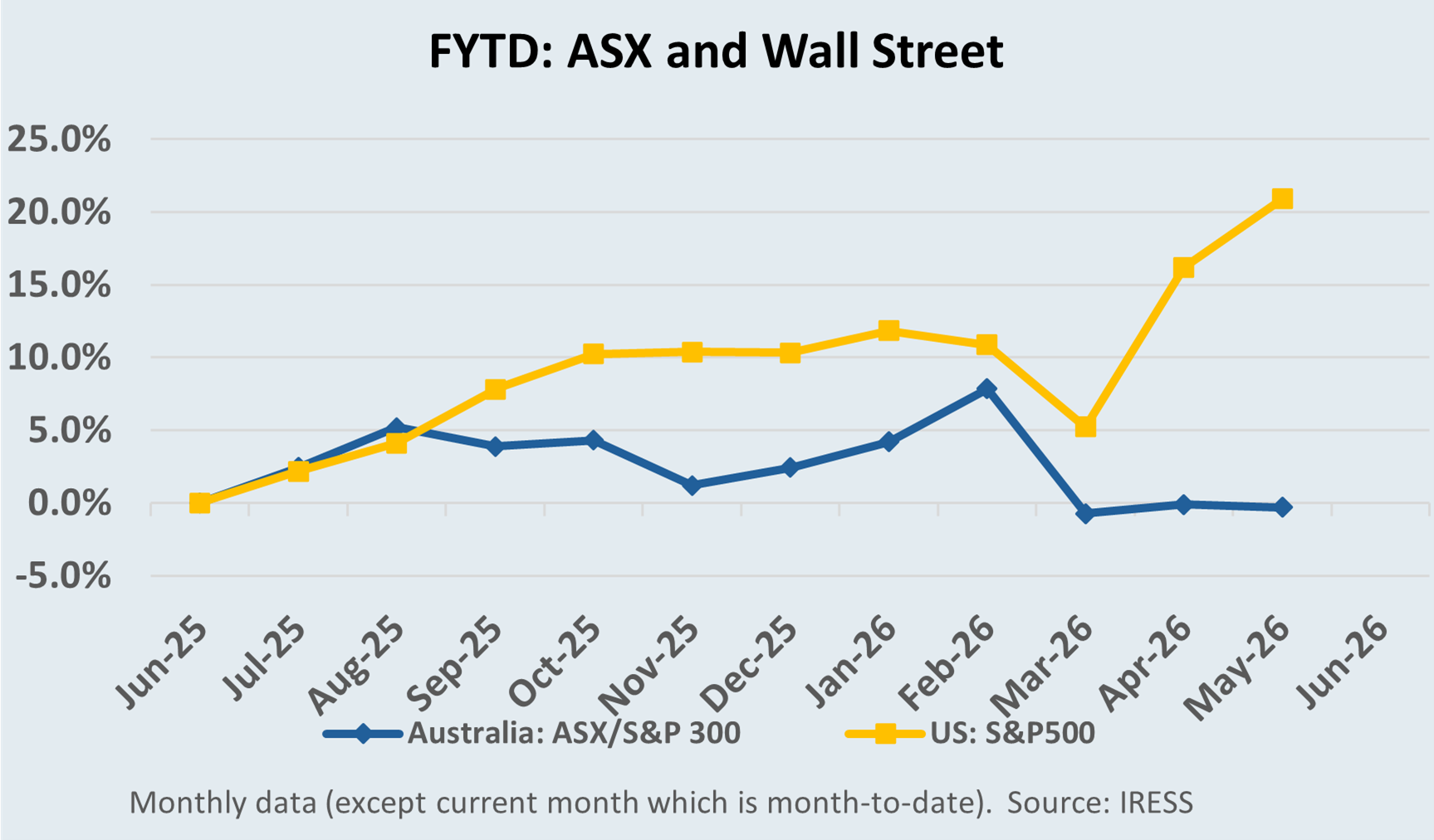

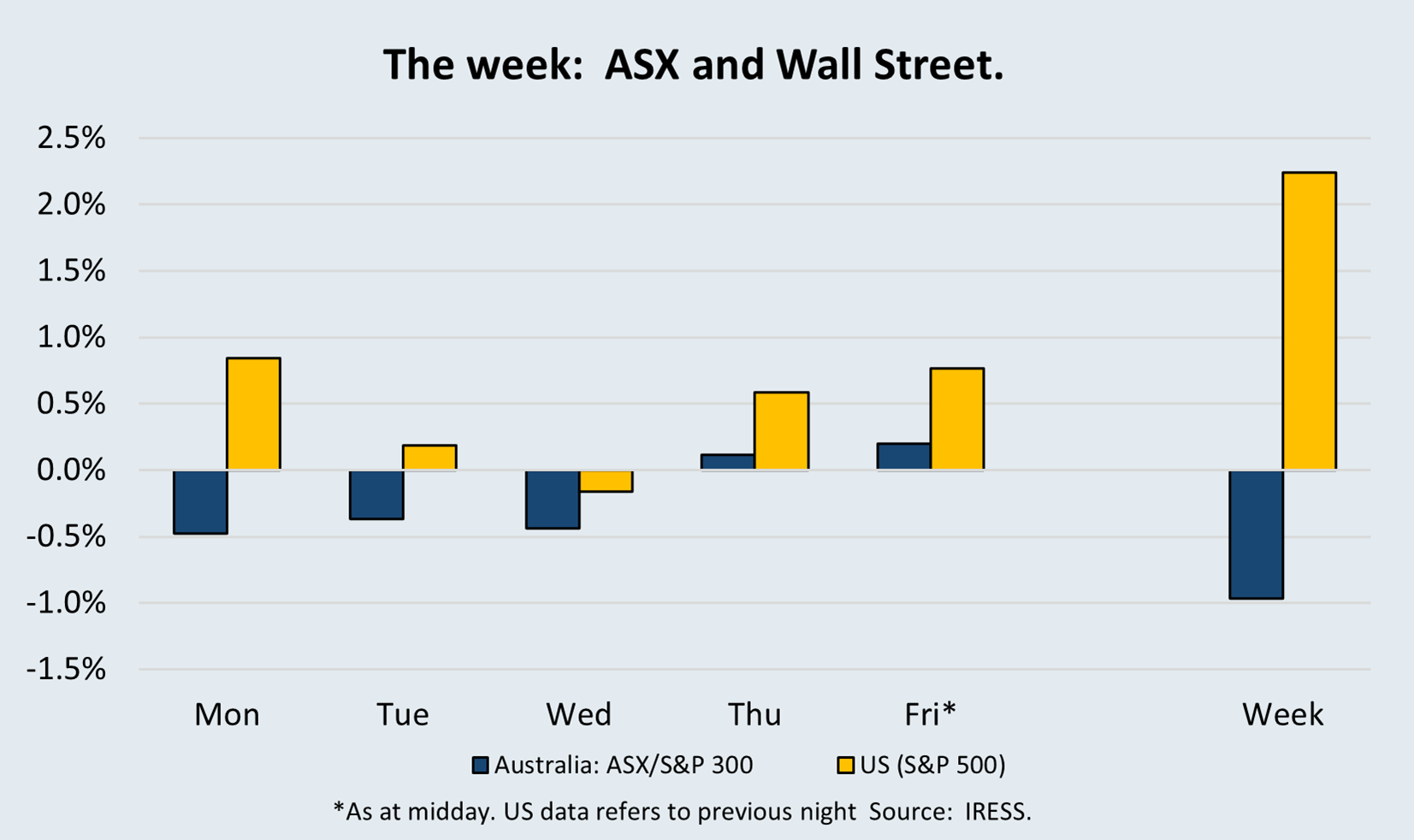

The Market

The Budget

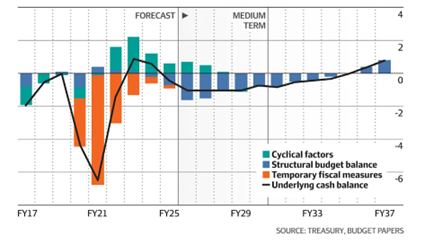

Treasurer Jim Chalmers has handed down what many observers are calling the most structurally significant budget in a generation — one that deliberately tilts the tax system away from asset wealth and toward wage earners. For retirees and those approaching retirement, there is a great deal to digest.

The headline changes are hard to miss. Negative gearing on existing investment properties is abolished, effective from budget night. The 50% capital gains tax discount — introduced by John Howard back in 1999 — is being wound back, reverting to an inflation-based model. Pre-1985 assets, long fully exempt from CGT, are now being brought into the net. And discretionary trusts face a new 30% minimum tax rate on distributions, regardless of the recipient’s marginal rate. Together, these measures are expected to raise more than $7 billion a year by the end of the forward estimates period.

Whilst the increase in taxation isn’t enough to solve structural deficits (see below), which will require much more political capital in future years, there does appear to be a deliberate delay in passing on the benefits of change to presumably younger Australians. Perhaps next year.

Figure #1: Structural budget balance (% of GDP)

The political logic is straightforward. Prime Minister Albanese has framed growing intergenerational inequity — particularly around housing — as a genuine threat to social cohesion. This budget is designed to shift property ownership toward younger Australians. If successful, this is a big positive for the future trajectory of equity earnings.

For those already fully retired and no longer running active investment structures, the direct impact of these changes may be limited. But if you or members of your family hold investment properties, discretionary trusts, or older pre-CGT assets still on the books, it is well worth a close conversation with your adviser about the practical implications — particularly around the timing of any asset sales and the crystallisation of capital gains.

2026 Federal budget: a quick review

Reviews of federal budgets carry a great deal of political baggage. They are often as much about expectations as what is delivered, and too often they struggle to rise above the partisan. That is not the task here. As CIO, the more useful test is to measure the Budget against the objectives that matter for portfolio outcomes: productivity, inflation, interest rates, earnings, capital allocation, housing, energy security and long-term fiscal sustainability.

The question is not whether the Budget was politically clever. The question is whether it improved the economic settings that drive investment returns.

Bold?

The first issue is whether Australia received the bold reform budget it needed. The answer is probably yes, if reform is backed up in future years and sustained under potential pressure. The Budget appears more reform-minded than many recent budgets, particularly in areas such as tax, housing, productivity and spending control. But the higher test is whether it was bold in absolute terms, rather than merely bold compared with Australia’s recent low-reform baseline. A fair reading may be that this was politically significant and directionally useful, but still not a complete reform program. It was bold enough to matter, but not bold enough to settle the question.

Interest rates

The second issue is the impact on interest rates and RBA deliberations. The Budget does not obviously force the RBA to tighten policy further, but nor does it make the RBA’s job materially easier. In an economy still dealing with inflation pressure, tight capacity and sensitive household balance sheets, fiscal policy matters because it can either lean against demand or leave monetary policy doing most of the work. From a portfolio perspective, this is critical. Rates flow directly into equity multiples, bond yields, housing, bank credit quality, infrastructure valuations and consumer spending. The Budget did not throw petrol on the inflation fire, but it did not remove the RBA’s matches either.

Quality of spending

The third issue is the quality of spending. This is not a simple argument for smaller government. Australia has underinvested in important areas, and poor capital allocation across the economy means the government will continue to play a large role. But if the government is going to be large, the spending needs to be wise. In a perfect world, the Budget would have done more to reduce excess spending, lower pressure on aggregate demand, and restructure major programs. But we are realists, and this was a Labor government not facing significant fiscal or political pressure, so wholesale spending cuts would have been a miracle!

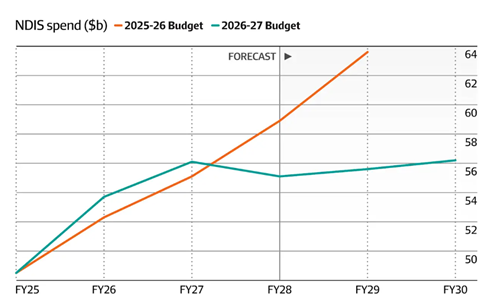

Within this context, the NDIS was the most pressing example. While broader spending discipline remains incomplete, material progress on the NDIS blowout would be a meaningful and necessary step. The question was not whether the government would be large. It already is. In this case, we are thankful for limited progress. And make no mistake, NDIS spending was risking equity valuations given its impact on interest rates and productivity.

Figure #2- A revised NDIS projection appears more sustainable

Source: Australian Treasury Budget Papers

Health

The fourth issue is health expenditure and the way the healthcare industry is funded. With several portfolio companies exposed to healthcare, we would have liked to see more work on structural fee and rebate reform. Instead, the emphasis appears to have been on stronger compliance and enforcement. That is important because the integrity of the system matters, but it does not solve the deeper question of how healthcare providers across the full scope of services are funded on a sustainable basis. Compliance can protect the system, but it cannot substitute for a funding model that allows the system to invest in capacity, technology, service quality and long-term efficiency.

Housing

The fifth issue is housing incentives and capital allocation. In our view, economic policy is as much about creating or changing expectations and incentives as it is about the direct impacts of taxes and charges. Australia’s weak productivity in 2026 is partly due to poor investment and asset allocation. This didn’t happen in isolation; Australia built an incentive structure that rewarded unproductive housing investment. Those incentives became self-fulfilling. Returns to housing investment grew, more people wanted to participate, and capital continued to be drawn into housing rather than more productive uses. Negative gearing was not just a tax setting. Over time, it became a national capital-allocation signal.

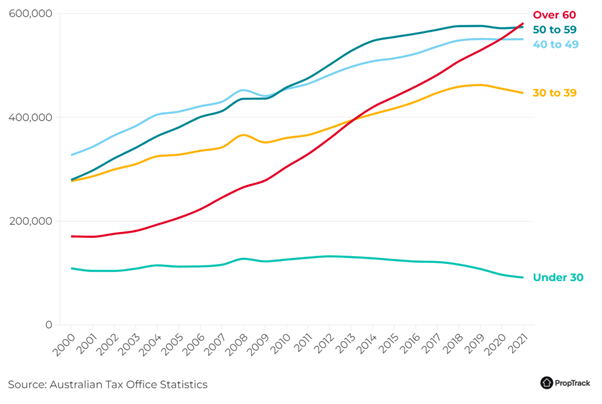

Figure #3 – Number of Australian landlords by age

We suspect that in five years’ time, the subtle changes to housing incentives may prove exceptionally important. The removal of negative gearing for new purchases of established dwellings should give young families a better opportunity to buy existing homes, safe from investor competition. At the same time, leaving negative gearing available for new dwellings should increase demand for new construction. That is exactly the kind of policy distinction Australia has often failed to make: discouraging unproductive bidding for existing assets while still encouraging the creation of new supply. The point is not simply fairness. It is whether the tax system can redirect capital from speculation toward formation.

New business investment

The sixth issue of relevance to our portfolios is whether the new settings can promote new business investment. More critically, in my mind, the question is whether they create stronger incentives for future generations to build new businesses. We were excited by the changes announced because they appear to shift the reward structure away from passive asset accumulation and toward enterprise, risk-taking and productive work. For a young person today, the best use of skill should not be leveraging into expensive property to reduce a tax burden. It should be building something new with time, effort, talent and capital.

Tax return reform

The final issue may prove critical in future years, even though it sits in the weeds of how we consider income from different sources. Anyone who completes their own tax return, or watches an accountant complete it, will recognise the structure of the income tax declaration: different boxes for different types of income and different categories of expenses. In a simple world, we would add up income, subtract deductions and determine a net amount. This Budget appears to build new flexibility into those calculations. Net rental income may still be reported in the right box, but rental losses will no longer be used to reduce other income. Similarly, the Working Australians Tax Offset for employees and sole traders will only be available to offset employee or sole-trader income. What we are seeing is tax policy increasingly differentiating among types of income, thereby changing the incentives attached to each.

CGT

Capital gains tax reform also fits under this broader umbrella of removing distortions. The principle is simple: people should not pay tax merely because prices rose with inflation. If an asset keeps pace with inflation, that is not a real gain. The individual already paid tax on the earnings used to purchase the asset. But after the gains rise above inflation, the earnings are taxed similarly to other forms of income, with special treatment for superannuation. These changes can be seen together as an attempt to remove distortions that have shaped Australian investment behaviour for decades. Australia will bear the cost of those distortions for a long time, but the country may now be beginning to escape them.

One final point worth keeping in mind: political observers note that this is almost certainly the only budget in this electoral cycle where Labor will take genuine policy risks. With the next election just over a year away by next budget, caution will return. The reforms you see here are, likely, as bold as this government gets. If you have questions about how any of these changes apply to your situation, please don’t hesitate to reach out.

The Banking Sector facing the inevitable

Rates, Real Estate, Credit quality. Expensive.

As regular readers would be aware, in our opinion, Australian bank stocks have defied gravity; commanding valuations that assume a world of perpetual credit growth, benign arrears, and an ever-inflating housing market. That world is changing — and the share prices are finally starting to say so.

The premium attached to the major banks has been sustained by two forces. The first is a persistent misconception that operating conditions remain broadly supportive. Investors have anchored to the remarkable resilience Australian banks showed through the rate-hiking cycle, mistaking a lagged deterioration for a soft landing. The second is structural: Australia’s large industry superannuation funds, swimming in compulsory contributions, have recycled billions into the domestic equity market’s most liquid names. The big four banks — convenient, familiar, dividend-paying — have absorbed much of that flow, providing a bid that had little to do with fundamental value.

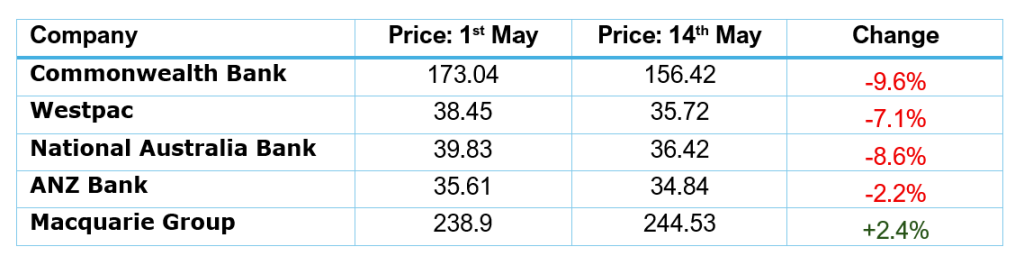

But the foundations are shifting. The federal budget introduces material changes to negative gearing and capital gains tax treatment that directly erode the after-tax appeal of leveraged property investment — the engine behind roughly 40 per cent of mortgage flow and 56 per cent of new lending into the major banks.

The implications ripple across three dimensions: mortgage growth is likely to slow as investor activity cools; net interest margins face modest but structural pressure as the book tilts from higher-yielding investor loans toward owner-occupier and first home buyer flow; and while asset quality appears broadly manageable, unemployment forecasts have deteriorated and broader risk appetite is softening. CBA and Westpac — most exposed given their heavy tilt toward investor mortgage lending — post results and the Budget the market gave its views clearly.

Figure #4 – Banking sector – price impacts of updates and Federal Budget

Our positioning is appropriate for the current environment. Underweight the large banks, and underweight consumer-facing sectors appear suitable, as fuel-driven inflation and weakening credit growth take hold. Despite the fall, the price of each of the Big Four still doesn’t reflect rising provisions, slowing mortgage growth and policy adjustments.

Company Updates

While broad equity indices are not showing significant volatility, stock-level movements at times have been remarkable. Markets, now, don’t seem capable of anything other than trading the obvious. For example, many company updates released mention the impact of the war in the Middle East. This is no surprise to anyone, let alone professional investors, and yet the price moves in response to these updates are often dramatic. While interesting to observe, we remain on the sidelines until prices move outside our valuation targets.

The impact, however, from updates can be significant with outsized moves in positions such as Healius (negative), Block XYZ (positive), Life360 (mixed) and Bapcor (negative).

We have presented the updates from Metcash, CSL and Inghams in more detail.

SGH: physical assets, embedded value and capital discipline

Portfolio company update

SGH, formerly Seven Group, was one of the more useful updates from an existing portfolio investment. The company spoke directly to continued strength in infrastructure and development demand, with Boral’s quarry and asphalt positions remaining central to why we own the stock.

Boral and Ravenhall: value becoming explicit

The newly announced Dexus partnership at Ravenhall is a clear example. The project involves Boral’s 630-hectare Ravenhall site in Melbourne, with Boral and Dexus each holding 50% of the proposed logistics precinct. Dexus has described the site as expected to become the largest institutionally held logistics precinct in Australasia, subject to rezoning and business-plan approvals. Media reports have described the long-term end value at around $10 billion.[1]

The Dexus transaction was a core option within our SGH investment case. It is an example of how the market often fails to recognise future embedded value until that value becomes explicit. SGH’s ownership of Boral has always included more than concrete, quarrying and asphalt earnings. It also includes land, logistics optionality, and the ability to apply capital discipline to assets that were not necessarily being properly valued by the market.

SGH’s bid with Steel Dynamics for BlueScope: privileged assets earning too little

BlueScope is also relevant to both our SGH and BlueScope positions. We support the current SGH/Steel Dynamics proposal and share SGH’s view of the transaction’s value to SGH’s portfolio. SGH and Steel Dynamics have submitted a revised proposal for BlueScope, with SGH proposing to retain BlueScope’s Australia and rest-of-world operations while Steel Dynamics would take the North American operations.[2]

Ryan Stokes’ explanation of why the Australian steel assets make sense inside SGH was clear and compelling. The current ROIC of circa 5% is too low for these privileged assets. SGH would follow its well-worn path to deliver higher ROIC through a mix of discipline, operational focus and capital savvy. We look forward to it as SGH shareholders.

Metcash Trading Update

Metcash’s trading update showed solid underlying revenue growth across the business when tobacco is excluded, which we regard as the relevant performance measure. Group revenue rose 3.8% excluding tobacco, with encouraging contributions from each major segment. Food revenue increased 5.4% ex-tobacco, including 2.6% growth in supermarkets and a strong 14.0% increase in Foodservice & Convenience. Liquor was also positive, with revenue up 1.0%, supported by 6.4% growth in on-premises wholesale sales. Hardware & Tools continued to recover, with revenue up 4.3%, including 6.7% growth in Total Tools and 3.7% in Hardware.

Figure #5: The many brands of Metcash

Source: Company website

Metcash guided to FY26 underlying EBIT of $501–505 million and underlying NPAT of $268–270 million, with good cash flow and debt towards the lower end of its target leverage range. Craig Woolford viewed the update as showing slightly stronger second-half sales trends and better margin outcomes in Food and Liquor, but with a more mixed result in Hardware. Hardware sales growth was stronger, but margins fell sharply, leading him to reduce FY27 and FY28 EPS forecasts by 7% and 8%, respectively, while cutting FY26 by only 1%. His target price was lowered from $4.05 to $3.80, but he retained a Buy recommendation. The key risks are the size of any Hardware margin recovery and the rising likelihood of more supermarket retail store ownership. The market responded positively, with MTS rising roughly 8.4% for the week.

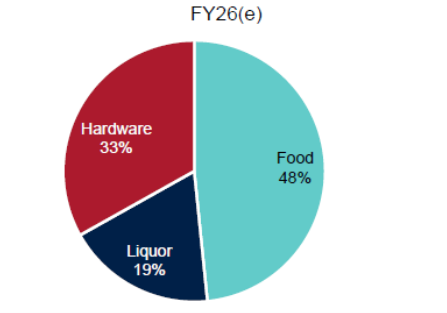

As a reminder, Metcash’s operating business can be broken down into three broad segments. Although Food represents almost half of the company’s earnings, both liquor and hardware remain important in the long run.

Figure #6: Share of earnings by segment – Metcash

Source: MST Marquee

Inghams: extracting more value from a valuable asset

Our team attended Inghams’ investor day in person in Sydney and had the opportunity to catch up with CEO Edward Alexander and senior management. The day reinforced our confidence in the value of the underlying asset. This is a scaled poultry supply chain across Australia and New Zealand, with strong positions in fresh poultry, retail, frozen and value-enhanced products. Inghams is not a marginal supplier; it is a core part of the protein supply chain for supermarkets, QSR and food service customers.

The trading update was pleasing. FY26 EBITDA guidance of $180–200m pre AASB 16 was maintained despite the Middle East-related fuel and input cost shock. The company has quantified the diesel/fuel impact at $7–10 million in FY26. Excluding that war-related pressure, the underlying trading trend appears better than the headline suggests. Volumes and net selling prices are growing only around 1%, so the earnings improvement is not driven by a strong top line. It is coming from better execution.

The operating challenge is significant. Inghams is moving millions of birds through a short-life system. Product has a shelf life of roughly 18 days and needs to reach shelves with 8–10 days remaining. Management says it is achieving this around 98% of the time. That highlights the real strategy: improving value per bird. A bird processed at the right size, in the right plant, at the right time, for the right customer, is worth more than the same bird pushed through a fragmented system.

Figure #7: Coordination of the supply chain is critical to increase value per bird

Source: Company announcement

There are tangible examples. Inghams processes around 8,000 tonnes of chicken meat per week, with roughly 15% going into ingredients. Instead of just selling whole birds to the wholesale market, around 20–25% of this volume is value-enhanced, including hot roast, and Inghams has a higher market share in value-added than in birds produced. It is also the leader in the frozen segment, where it leverages its strong brand. We would argue

Automation, tray packing, fully cooked capability and advanced ingredients all support the same objective: better yield, lower waste, improved mix and higher value extraction. The opportunity is to lift the value per bird. That means better planning, better bird sizing, higher plant utilisation, lower waste, stronger labour efficiency, better shelf-life outcomes, improved customer mix and more disciplined capital allocation. Initiatives in automation, fully cooked capability, tray packing, frozen and advanced ingredients all support this direction.

The key issue remains execution. Operational consistency, capital productivity and competitive intensity have historically held returns back. But if Inghams can sustain the recent earnings improvement and deliver its $60–80m savings program, the long-term value in the asset base should become more visible.

We are encouraged by the strategy. The challenge is timing. A three-year transformation may be reasonable for systems, capital and contracts, but the operating evidence should appear much sooner. The market was as pleased with the update as we were with the stock rising from $1.70 to Wednesday’s close of $1.93, up about 13.5%.

The market response was encouraging. Inghams’ share price rose strongly through the week following the investor day and trading update, moving from around $1.70 on Friday to about $1.93 by Wednesday. That suggests investors looked past the near-term Middle East-related fuel impact and focused instead on the maintained FY26 guidance, the improving Australian earnings run-rate, and a clearer strategy to lift value per bird.

CSL Update

CSL: still a wait-and-see reset

CSL’s update was not well-received by the market. It was treated as another downgrade and a loss-of-confidence event, not as a clean reset.

The update was the Interim CEO 90 Day Review under Gordon Naylor. CSL cut FY26 guidance to around US$15.2bn revenue and US$3.1bn NPATA, excluding restructuring and impairment costs. The main revenue headwinds were around US$300m from US immunoglobulin channel inventory normalisation, US$200m from lower China albumin market value, and US$150m from the Middle East conflict, HEMGENIX and iron competition. CSL also flagged an additional ~US$5bn of non-cash pre-tax impairments across FY26 and FY27, mainly related to CSL Vifor intangibles and under-utilised PPE.

The market reaction was brutal. CSL fell around 16% on the announcement day to about $100.75, traded below $100 intraday, and was down more than 20% across the week. The stock is now at decade-low levels and has fallen heavily in 2026.

This outcome is consistent with the conclusion of our recent CSL report. We argued that CSL’s old premium valuation rested on too much faith in perpetual growth, scientific productivity and management judgment. Those assumptions have been challenged. Innovation has been weaker than hoped, Vifor was a poor acquisition, governance now matters more, and Seqirus deserves a lower multiple than Behring. The market was right to withdraw some of CSL’s old premiums.

But the update does not prove that Behring is broken. The core plasma franchise still has attractive demand characteristics, durable immunoglobulin demand and a global plasma collection moat. The issue is that CSL has over-earned trust, over-invested in parts of the business and under-delivered on execution. The market is no longer willing to capitalise long-dated growth promises without evidence.

Our positioning remains wait-and-see. We are underweight in CSL, and there is no rush to add aggressively. There is still no permanent new CEO, and we are not especially enthusiastic about Gordon Naylor as the person to rebuild market confidence. But we also do not want to remain too underweight forever in a large, high-quality healthcare asset if the reset eventually leads to better decisions.

There is also no permanent new CEO yet. Gordon Naylor is the interim CEO, and we are not especially enthusiastic about Naylor as the person to rebuild market confidence. The next permanent leadership appointment matters.

So our stance remains unchanged. CSL looks less like a broken growth story and more like a high-quality business in a credibility reset. But it is still wait-and-see. We are likely to add over the course of FY26, but there is no hurry. Remaining too underweight in a large, high-quality healthcare asset carries risk, but the company still needs to earn back trust before it deserves a materially larger position.

The information in this article is of a general nature and does not take into consideration your personal objectives, financial situation or needs. Before acting on any of this information, you should consider whether it is appropriate for your personal circumstances and seek personal financial advice.