Copyright 2026 First Samuel Limited

Read the previous Investment Matters here:

Before parsing the RBA’s decision to increase interest rates, we thought it useful to briefly comment on an optimistic view of Australia’s future.

Macquarie Bank’s CEO, Shemara Wikramanayake, opened its famous annual investment conference with confidence in markets and the future. What made her address more important this year was the theme that other presenters then built upon- a redefinition of Australia’s quality and future.

Australia as an investment destination is often reduced to banks, housing and iron ore, but the strategic picture is broader. The country has energy, land, minerals, infrastructure, rule of law, proximity to Asia and relatively low government debt. In a world paying more attention to supply chains, power availability, data centres and critical minerals, those advantages matter.

It is a theme we have hoped to capture in our portfolio for many years.

When we speak of the diversity of a basket of metals, minerals and mining services, Shemara suggest Australia held the “periodic table” in its hands. A reference to the table of all elements you may have learnt about in secondary school.

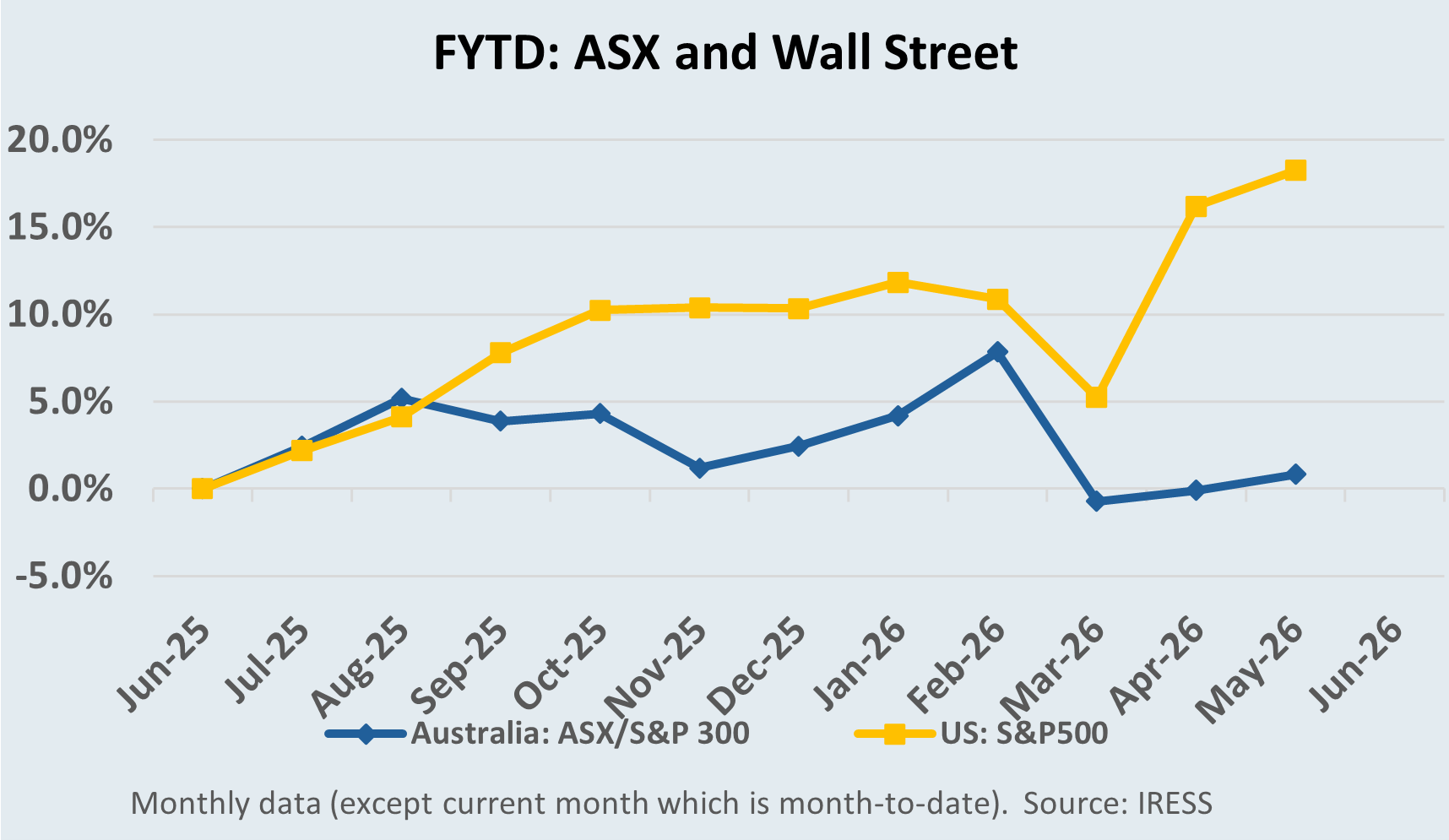

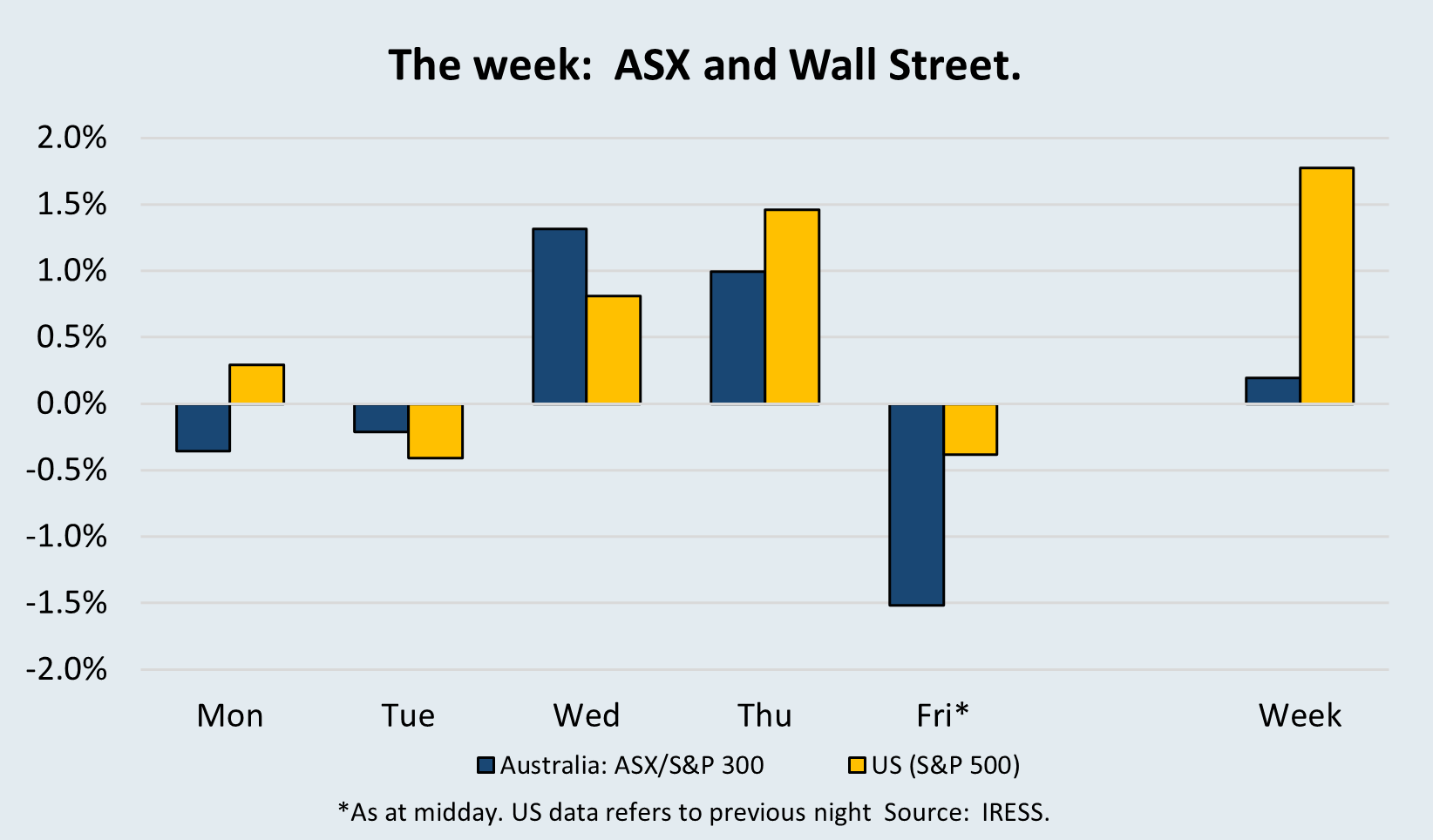

The Market

Australia looking better than expected, but not in obvious places

She suggests the periodic table is becoming a more useful way to think about Australia than the old quarry-and-bank shorthand. Australia’s resource endowment, energy capacity, institutional stability and balance-sheet flexibility all become more important in a world where supply chains are being rebuilt, and power availability increasingly shapes industrial and technology investment.

The conference did not remove the macro uncertainty. The duration of the war remains the key global variable, and the RBA still has to balance improving inflation signals against housing pressure, migration and the risk of easier financial conditions. But the company meetings were a useful reminder that equity investing is not just macro forecasting.

Australia has assets the world increasingly needs: energy, minerals, land, infrastructure, institutions and balance-sheet flexibility. The better companies are using technology, capital discipline and privileged assets to improve returns. Others, like Endeavour, may not be investments for us, but still provide valuable signals about the consumer and the economy. That is why conferences like this matter. They help connect the macro story to what companies are actually seeing, doing and changing.

The RBA’s uncomfortable problem

Fragile consumer, hard inflation data

It was useful to hear from Chief Economist Ric Deverell early in the week, and then listen to company CEOs spend the next few days talking about the fragility of the domestic consumer. That followed recent updates from Woolworths and Coles, which also pointed to a cautious consumer backdrop. Put simply, households are not happy, and the outlook should remain cautious.

Nevertheless, the RBA Monetary Policy Board raised the cash rate to 4.35% as widely anticipated. The Board vote was split 8-1. Governor Bullock noted in the press conference that the Board now assesses the cash rate as being “a bit restrictive”. Despite assuming the conflict is resolved soon and fuel prices decline, the Board assessed that “the risks remain tilted to the upside”.

The problem for the RBA is that it is not responding to feelings. It is responding to hard data, and that data is still clear and problematic. Inflation remains too high. Non-tradable inflation, which is domestically generated and harder to dismiss as imported price pressure, remains too high. The RBA also has to consider the possibility that wages rise faster than previously expected if higher oil prices feed into broader inflation expectations and wage demands.

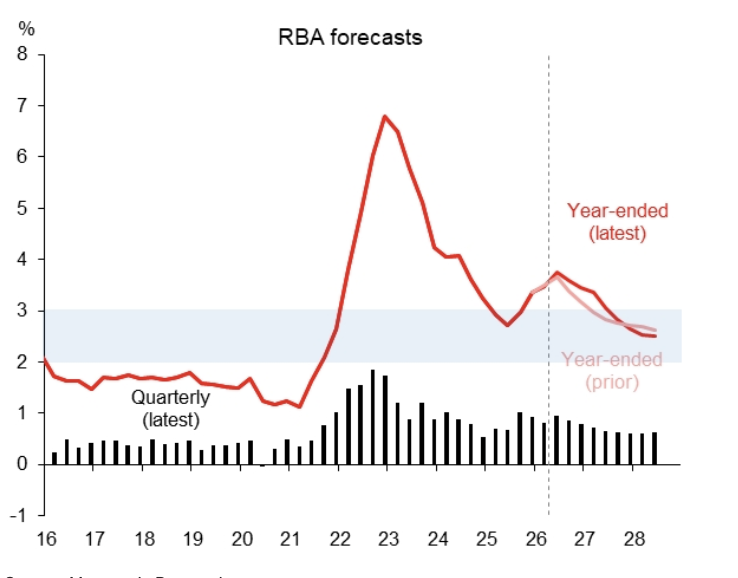

We can see the concerns the RBA has expressed in its updated CPI forecasts shown below, which it expects to remain outside the target range for longer than it expected last year. This is despite also forecasting ongoing rises in the RBA cash rate.

Figure #1: Australia Trimmed Mean CPI Inflation: The RBA revised their underlying inflation forecasts higher on the view that firms are likely to pass on at least some of the increase in costs of fuel and other commodities

Source: Macquarie Research

The economy is strong in some places, weak in others.

This creates an awkward split. The part of the economy most exposed to interest rates is already under pressure. Middle-class households, mortgage-belt suburbs and upwardly mobile families are carrying the weight of higher rates, higher insurance, higher energy prices and higher grocery bills. That is showing up in company commentary. It is visible in supermarkets, hotels, liquor stores, discretionary retail, and housing-related activity.

But the overall economy is being supported by forces that mortgage rates only partly influence, or do not influence at all.

Business credit and investment remain healthy because companies know they cannot stand still. The threats and opportunities from new technology, resources, the energy transition, data, automation, and supply chain change all require capital. That is good for Australia. A productivity problem ultimately requires business investment, and business investment often requires higher credit.

Government spending is also strong. Some of it is required to catch up on infrastructure development after record immigration. Some is required for the health needs of older Australians, and the education needs of younger Australians. Increasingly, some is required to smooth the harsher edges of modern life: inflation, higher energy prices, housing stress and cost-of-living pressure.

The economy is also being supported by older Australians, who have generally benefited from stronger asset values, higher deposit rates and lower direct mortgage exposure. Their spending patterns differ from those of younger, mortgage-holding households, making the household sector less uniform than it once appeared.

Finally, Australia continues to benefit from strong terms of trade. We are still selling the materials we produce at relatively high prices compared with the cost of many imports we purchase. That national income support matters, even when individual households feel stretched.

The cash-rate channel is powerful, but uneven

The RBA’s bluntest tool is still the cash rate, and its most powerful direct transmission mechanism remains the mortgage rate. That is where the policy bite is immediate and painful. The difficulty is that many other supports for the economy are much less sensitive to domestic interest rates. The RBA cannot set fiscal policy. It cannot directly slow population-driven demand for infrastructure, health, education and government services.

For business investment, domestic interest rates matter, but they are often a marginal consideration when companies are responding to technological change, resource opportunities, supply chain risk, and the need to improve productivity.

For households with savings, limited debt and high passive income, higher rates can even have the opposite effect, lifting interest income and increasing their capacity — and sometimes their need — to support adult children and their families.

Where the pain lands

That leaves the greatest impact of higher rates on the part of the economy already under stress: mortgaged households and discretionary consumer spending. This is exactly what companies are now describing. The middle-class suburbs, the mortgage belt, and the upwardly mobile households that once drove much of the discretionary demand are now being squeezed by higher mortgage payments, insurance costs, energy costs, and grocery bills.

Our concern is that the RBA has sought feedback from companies as part of its standard liaison program, and firms are unequivocally concerned – expectations for demand growth over the next 12 months are as weak as leading into COVID. This will not stop firms from putting up prices. Australia has true competition in a few markets and oligopolies in most. But the liaison program may have prompted a pause. Firms have genuinely provided relevant

Figure #2- Indeed, firms in the RBA liaison program have lowered their domestic growth expectations dramatically, in line with the sharp fall in business confidence seen in other surveys

Source: RBA, Macquarie Research

There is also a second-round housing effect. The optimism that followed expectations of recent rate cuts has now reversed. House prices are already under pressure, and affordability was already close to record-stretched levels before the latest shock. With the war sitting in the background, the sensible portfolio response is caution rather than assuming the consumer can simply absorb another round of pressure.

Portfolio implication

This caution is already reflected in the portfolio. We have limited exposure to Australian banks and limited exposure to the domestic discretionary economy. Recent banking updates have already shown credit risks and expected losses beginning to tick higher, and that was before the medium-term effects of the war were fully visible.

For us, the conclusion is straightforward: the RBA may be right to respond to the inflation data, but the4 policy’s transmission is uneven. It lands hardest on the parts of the economy where the stress is already most obvious.

Macquarie Investment Conference

Macquarie: More than stock presentations

A conference as a ground-up check on portfolios, companies and the economy

This week we attended the Macquarie Australia Conference, which gave us the opportunity to listen to a selection of more than 100 companies, economists and market speakers.

Conferences like this are useful for three different reasons.

- Portfolio companies: revisiting investments we already own

The first is the chance to revisit investments we already own, particularly when management teams offer valuable perspectives on broader global trends and domestic outcomes. This was the case with SGH, formerly Seven Group, and Worley. In both cases, the company presentations were useful not just because of what they said about the businesses themselves, but because of what they revealed about infrastructure demand, energy, industrial activity, technology and capital allocation.

- Companies we do not own: testing old theses

The second category is companies we do not own, or industries where we have previously had a cautious or negative view. These meetings are useful because they test existing theses. They help us understand whether the problems are getting worse, whether management teams are responding intelligently, and whether recent share price weakness is creating genuine opportunity or simply reflecting a business model under pressure.

- Economic linkages: businesses that tell us something wider

The third category is smaller but often highly valuable: companies whose comments are closely linked to other parts of the economy. Endeavour Group and Gem Life are examples. We may not need to own these businesses to learn from them. Their comments on consumers, housing, pubs, retirement living, development activity and local communities can provide useful signals about the wider economy.

Taken together, the conference was a reminder that company meetings are not just about individual stocks. They are a way of checking the temperature of the economy from the ground up. This year, the dominant themes were the duration of the war, the RBA’s difficult balancing act, Australia’s strategic advantages, and the extent to which well-managed companies are using technology, capital discipline and privileged assets to improve returns.

War duration, fuel and material costs

A short shock versus a longer disruption

The risk from the war is not only the first move in oil prices or the immediate market reaction. The larger risk is duration. If higher fuel, freight, and material costs persist, they will be passed through to company margins, project costs, household budgets, and wage expectations. Recent comments from major company CEOs sit squarely in that frame: activity may still be broadly constructive, but higher fuel and material costs are another pressure point for family budgets.

This is a difficult combination for the RBA. A fragile consumer is already evident in company commentary, while a longer war could keep inflationary pressures alive through diesel, transport, materials, insurance, and construction costs. Even if the conflict ends, some of these costs may not reverse quickly. Companies can absorb them for a time, but not indefinitely. They are eventually passed on to customers, taken through lower margins, or reflected in delayed projects and softer demand.

A short shock can be priced and moved through. A longer disruption changes behaviour. Companies hold more inventory, customers trade down, infrastructure projects become more expensive, households become more cautious and central banks have less room to ease

Analysis presented by Macquarie Economist Ric Deverell provided an interesting backdrop to the energy price risk posed by an extended conflict.

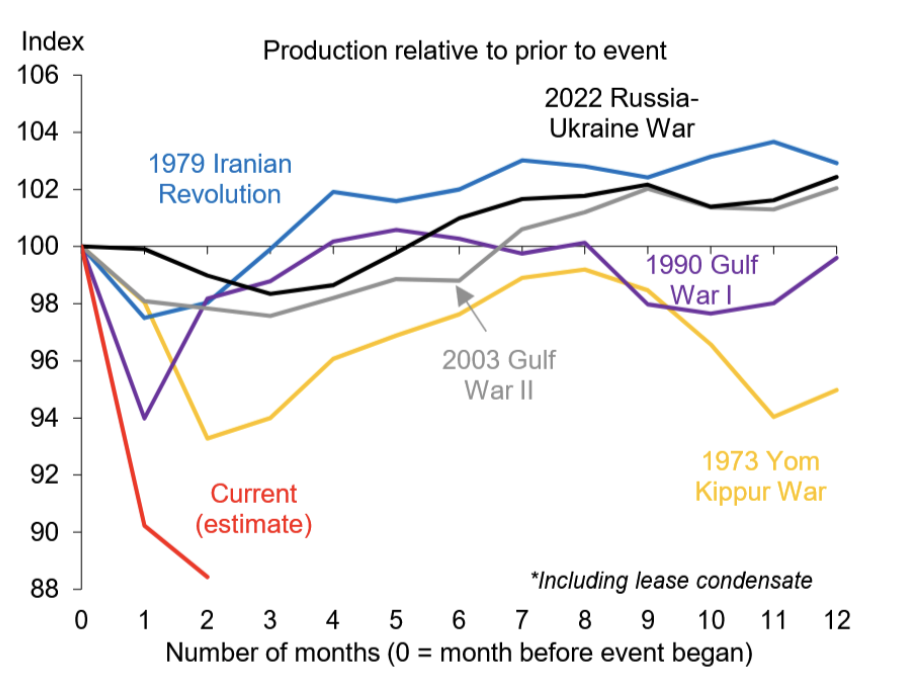

The first chart below shows the extent of the production loss in the current war. Approximately 12 million barrels of crude production per day have been lost (the index falling from 100 to 88). Yet the price impact on Brent Crude has been much more muted than some expected and significantly less than in previous episodes.

Figure #3: Global crude oil production impacts from various historical conflicts

Source: Macquarie Research

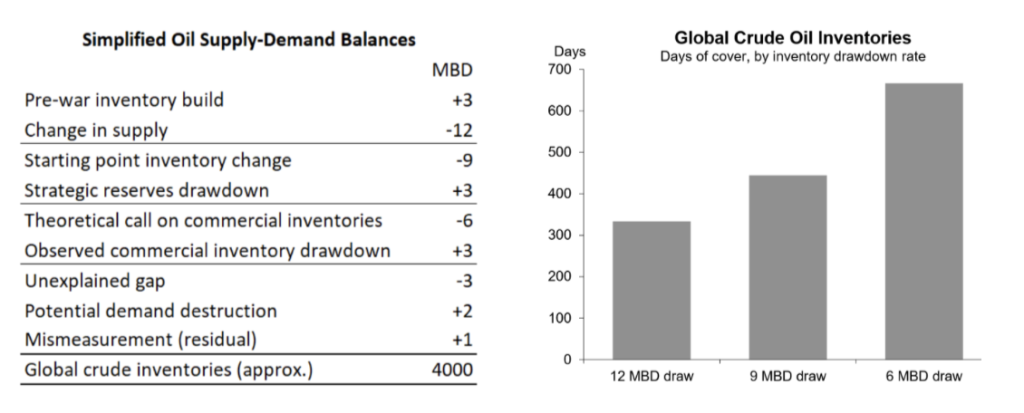

.So what has happened to mute the price impact?

The following table and chart show that the solution has been closely linked to pre-war inventory build, strategic reserves drawdown, and demand destruction. In recent Investment Matters, we have already discussed the economy’s lower energy intensity compared to the 1970’s and early 2000’s. The combination of planning, especially by China and the US, early impacts of EV’s and changes to the energy grid have allowed the price impact to be muted.

But even the best-prepared countries (which do not include Australia, despite being an energy exporter) have only limited reserves (300+ days), with a 12 million-barrel-per-day draw.

Figure #4: Global crude oil production impacts from various historical conflicts

Source: Macquarie Research

Company presentations in more detail

The final section of this week’s Investment Matters highlights what we learnt from three of the presentations.

- Seven Group Holdings, SGH

- Endeavour Group, EDV

- Seek Limited, SEK

SGH: physical assets, embedded value and capital discipline

Portfolio company update

SGH, formerly Seven Group, was one of the more useful updates from an existing portfolio investment. The company spoke directly to continued strength in infrastructure and development demand, with Boral’s quarry and asphalt positions remaining central to why we own the stock.

Boral and Ravenhall: value becoming explicit

The newly announced Dexus partnership at Ravenhall is a clear example. The project involves Boral’s 630-hectare Ravenhall site in Melbourne, with Boral and Dexus each holding 50% of the proposed logistics precinct. Dexus has described the site as expected to become the largest institutionally held logistics precinct in Australasia, subject to rezoning and business-plan approvals. Media reports have described the long-term end value at around $10 billion.[1]

The Dexus transaction was a core option within our SGH investment case. It is an example of how the market often fails to recognise future embedded value until that value becomes explicit. SGH’s ownership of Boral has always included more than concrete, quarrying and asphalt earnings. It also includes land, logistics optionality, and the ability to apply capital discipline to assets that were not necessarily being properly valued by the market.

SGH’s bid with Steel Dynamics for BlueScope: privileged assets earning too little

BlueScope is also relevant to both our SGH and BlueScope positions. We support the current SGH/Steel Dynamics proposal and share SGH’s view of the transaction’s value to SGH’s portfolio. SGH and Steel Dynamics have submitted a revised proposal for BlueScope, with SGH proposing to retain BlueScope’s Australia and rest-of-world operations while Steel Dynamics would take the North American operations.[2]

Ryan Stokes’ explanation of why the Australian steel assets make sense inside SGH was clear and compelling. The current ROIC of circa 5% is too low for these privileged assets. SGH would follow its well-worn path to deliver higher ROIC through a mix of discipline, operational focus and capital savvy. We look forward to it as SGH shareholders.

WesTrac and Caterpillar: technology inside the machine

Your author will admit to spending part of the conference happily geeking out over discussions concerning big yellow toys. But beneath the machinery, the theatre was a serious investment. Caterpillar’s technology is becoming more embedded in how equipment is operated, monitored, and improved. This is relevant to SGH through WesTrac, but also to our broader thinking about technology and AI across equipment-heavy businesses such as Cleanaway and Emeco.

Figure #5: Caterpillar’s next generation of equipment is increasingly technology-enabled, with GPS, sensors and onboard systems helping improve accuracy, safety and productivity.

Caterpillar’s next generation of equipment is increasingly technology-enabled, with GPS, sensors and onboard systems helping improve accuracy, safety and productivity.

Cat Grade with 3D is a good example. The system uses GPS to automatically adjust blade lift and tilt movements, helping operators reach design specifications faster while reducing rework, labour and material costs. The factory-installed Cat Grade with 3D Ready option includes the hardware required for the 3D system, including onboard sensors, GNSS antennas and receivers, and a 10-inch touchscreen display.[3]

The useful point is not that machines are suddenly replacing skilled operators. It is that the machine is increasingly becoming an intelligent co-worker: improving accuracy, reducing waste, shortening training curves and making work safer. For SGH, this supports the quality of WesTrac’s position as the local Caterpillar dealer, with future value increasingly tied to technology, service, training, parts and customer productivity rather than equipment sales alone.

The pace of this development is impressive, and it also helps frame how we think about technology and AI across a wider range of portfolio investments, including Cleanaway and Emeco, where equipment utilisation, labour efficiency, safety, route optimisation, maintenance and customer productivity all matter.

Endeavour: not for us, but worth listening to

Why would we not own it in its current form

There are many reasons we would not own Endeavour Group in its current form. The hotel business includes real assets but also exposes the portfolio to electronic gaming machines, which are socially problematic and increasingly difficult to reconcile with long-term portfolio ownership. The liquor and hotel formats are also facing a more difficult consumer backdrop than they have for many years. A weakened middle class, higher interest rates, cost-of-living pressure and more selective discretionary spending are all weighing on the parts of the economy that Endeavour depends on. Large-format liquor retail and suburban hotels may still have scale advantages, but scale alone is less powerful when customers are trading down, visiting less often, or only spending around major occasions.

Why was it still useful

That does not make Endeavour irrelevant to us. In fact, it makes the company a more useful economic indicator. Its comments on Dan Murphy’s, suburban hotels, value-seeking behaviour, celebrations, local communities and property strategy provide a direct read on the Australian consumer. Endeavour may not be a business we want to own, but it is a business worth listening to.

Hotels: asset value, capital need and social complexity

The pubs were once an aside but are now a major asset and a major question. There appears to be underinvestment in some physical hotels, particularly those competing for local community relevance. The opportunity is a rebuild around what works and what does not; the risk is that hotels require capital, judgement and discipline at the same time as the consumer is under pressure.

Liquor retail: value and occasions

Dan Murphy’s appears to be trading better than parts of the hotel network, but the broader liquor customer is still becoming more value conscious. Customers are more focused on cheaper favourite brands, inventory availability around major occasions such as Easter and Anzac Day, and simple price credibility. That makes price, range, local execution and cost position more important than fashionable retail language.

Strategy: Beware of old retail thinking

The risk is that Endeavour still reaches for concepts that sound better than they operate: omni-channel, cross-sell, loyalty leverage and private label. Some of these may have a role, but none is a substitute for value, execution and capital discipline. There is no easy answer based on 2000s retail thinking.

SEEK: unique data, large opportunity, and the management question

Seek has been a disappointing portfolio position, selling off amid concerns about AI, rising interest rates, and unemployment.

We also listened to Grant Wright, Group Executive AI, at the Macquarie Conference. That helped frame the real AI question for companies such as SEEK. The opportunity is not simply access to large language models. Increasingly, everyone has access to powerful off-the-shelf tools. The advantage comes from applying those tools to proprietary data, workflows and real-world decisions that competitors cannot easily observe.

We are convinced that many existing software solutions will be disintermediate and replaced by new AI tools, but not all face the same risks. But even well-placed companies may not be able to embrace the opportunities presented; after all, Seek.com.au emerged from the opportunities Fairfax Media missed.

That is why SEEK remains one of the more interesting high-risk, high-return portfolio positions. AI is most powerful when applied to high-quality data, and two-sided markets provide the opportunity to observe real-world decisions. SEEK can see employers, candidates, job advertisements, applications, search behaviour, pricing, conversion, hiring outcomes and where the process breaks down. These are signals from decisions made by real people and companies.

The opportunity is larger than making job advertising slightly more efficient. Recruitment is full of noise. Employers do not need 1,000 AI-generated applications. They need five candidates who are ready to talk, or 50 candidates who are high-fit, verified and plausibly interested. Candidates need confidence that the employer is real, the role exists, and the process is not a black hole. SEEK should be able to build trust infrastructure into the platform: identity verification, portable credentials, references, qualification checks and better matching. This is especially important if AI agents make it easy for candidates to apply for jobs at an industrial scale. SEEK’s role should be to reduce noise, not amplify it.

Grant Wright explained the scope of these opportunities well.

If SEEK can do this, the addressable market becomes more interesting. The company starts to replicate parts of the role historically played by recruiters and employment agents. A recruiter does not create value by producing a pile of resumes. The value is in knowing who is real, who is suitable, who is likely to move, and who is ready for a conversation. If SEEK can provide that at scale, pricing can then move away from the value of an advertisement and towards the probability of placement. Same-day matching, screening and workflow tools could move SEEK closer to the economics of recruitment rather than classifieds.

But it also can’t continue to waste money on existing work practices. So, the first and most important signpost for us is cost. SEEK has historically looked like an organisation with too much cost for the quality of its market position. The operating margin is not high enough for a company with strong brands, network effects, data advantages and a digital marketplace model. We were disappointed by the cost growth forecasts, particularly because this should be one of the business’s best-placed to use technology to reduce complexity and improve operating leverage.

The alternative is not to starve the business of investment. A lower-cost, higher-investment version of SEEK should be possible: removing duplicated costs, simplifying the structure, reducing internal process drag, and using AI to improve productivity, while still investing aggressively in product, data, trust, verification, and matching. The issue is not whether SEEK should invest. It is whether enough of the current cost base is building future advantage. Cost discipline should create more room for the right investment, not less.

The second signpost is product development. SEEK needs to show that it can turn its data advantage into practical products customers value: better matching, screening, verification, workflow and employer productivity. The prize is fewer poor applications, faster candidate discovery, higher trust and better hiring outcomes.

The third signpost is flexibility. SEEK needs to manage the interplay between softer hiring demand, product release and pricing. Yield growth has been relatively easy to manage, and there is good evidence that SEEK can still price the core product. But yield growth is the easier part of the story. The more valuable pricing opportunity is linked to probability to place.

This brings us back to the management question. Is this the team that can convert the opportunity? If we were sure, SEEK would already be a larger position in the portfolio. The company has the ingredients: brand, scale, a two-sided marketplace, unique decision data, pricing power and a clear role for AI in improving trust and reducing noise. But the opportunity is not automatic. In a period of structural change, investors need more than long-term company men “looking forward with confidence”. We need evidence that the organisation understands the scale of the opportunity and the need to change costs, products, and pricing simultaneously.

For us, the question is whether SEEK can lower unnecessary costs, increase investment in the right product areas, and turn its two-sided data advantage into better matching, verification, pricing and placement outcomes.

The information in this article is of a general nature and does not take into consideration your personal objectives, financial situation or needs. Before acting on any of this information, you should consider whether it is appropriate for your personal circumstances and seek personal financial advice.