Copyright 2026 First Samuel Limited

Read the previous Investment Matters here:

In this week’s Investment Matters, confident that the many twists of Iran, the Australian political malaise, and prognostication on interest rates can wait another week, if not longer, we return to the discussion of stocks.

We felt it was useful to revisit CSL Limited, a great Australian company with a valuable global franchise that has underperformed as a stock in recent years.

Once the largest company on the ASX when its share price was above $300, it remains an important component of the ASX300. For the past year, we have owned a position, but at a smaller weight than the index. The update on CSL that follows has been curated to suit a variety of readers’ appetites.

The punchline leads us off. A relatively short discussion, “snapshot” if you like of how the stock price got to today’s levels, along with an assessment of the value of the underlying business, follows.

Feel free to stop at this point.

For those with additional stamina, we have presented a much more detailed explanation of how we reached our conclusions. The remainder of the piece outlines

- What CSL actually is

- Why the stock de-rated

- Behring: the franchise that still matters most

- Innovation: where credibility broke

- Vifor: a poor acquisition, not just a difficult one

- Seqirus: valuable, but lower quality

- Governance, leadership and the future use of cash

And finally, we have a glossary to explain the plethora of scientific and product names.

The Market

Punchline: a high-quality business in a credibility reset

Thesis in brief

• CSL is a high-quality Behring (essentially, its plasma business)-led company in a credibility reset: the premium multiple has broken, but the core franchise has not. The opportunity is open for investors to own the core business with upside leverage to improved returns from capital allocation.

At a glance

- First Samuel holds CSL in clients’ Australian shares sub-portfolios

- Its share price has fallen considerably since we purchased

- The premium multiple that CSL long maintained broke because the market lost faith in innovation, capital allocation and governance

- The de-rating looks broadly justified for the non-core assets, but less so for Behring

- The opportunity now is not heroic science; it is stronger management of CSL’s existing earning power and the promise of better future decisions

CSL is a large, visible, and benchmark stock. We first purchased CSL in July 2025 at approximately $246 share. Prior to the onset of the Iran War, but after a poorly received 1H26 set of financial results, which included a profit downgrade and the surprise departure of its CEO, its share price had fallen by about 40%.

All of the ground made since 2017 has reversed.

Figure #1: CSL daily share price since 2017

Source: TradingEconomics

The snapshot shows there is valuation support for additional buying at these levels, but there is no rush to be fully invested (a position likely more than 4% of the sub-portfolio)

CSL is a long-term opportunity, but three near-term issues mean there is no urgency. US immunoglobulin prices are under pressure from oversupply, though underlying demand remains sound. Chinese albumin sales are soft, with no clear recovery in sight. And rising energy costs are adding modest headwinds to margins.

None of these changes the medium-term case, but together they are likely to weigh on earnings in the short term — a sustained recovery will probably require these conditions to improve, alongside the appointment of a permanent CEO.

Snapshot: where are we and how did we get here

At a glance

- The share price fell because investors lost faith in CSL’s new drug pipeline, its spending decisions, and in the short-term management and its board.

- The opportunity is not about betting on new drugs. It is about owning a strong business at a fair price, with the potential for better decisions ahead.

CSL is no longer being asked to live up to the market’s old fantasy of a flawless compounder. That matters. For years, CSL as a stock carried a premium that rested not only on a high-quality plasma franchise, but on a more ambitious assumption: that quality would extend indefinitely into innovation, reinvestment and strategic judgment.

That was always a generous reading of the business. It implied not just durable demand, but near-permanent excellence in capital deployment and scientific productivity.

That confidence has broken. Innovation has disappointed. Vifor (a global specialty pharmaceutical company in the treatment areas of iron deficiency, dialysis, nephrology & rare disease) was, in our view, a poor acquisition. Governance now matters in a way it did not when the share price was rising. Leadership change has sharpened the sense that CSL is in transition rather than in command.

The market typically hates this combination. It can forgive a slow quarter. It is far less forgiving when confidence in management judgment starts to slip.

Even so, the de-rating looks too broad. The market has valid reasons to apply a lower multiple to CSL’s non-core businesses and to reduce the old innovation premium. But it may now be over-applying that discount to CSL Behring, where the key value drivers remain intact: durable immunoglobulin demand, hard-to-replicate plasma collection infrastructure, and strong earning power from an installed product base that still has pricing authority.

That is the nub of the opportunity. CSL today looks more like a quality-plus-optionality investment and less like a classic premium compounder.

That quality sits in Behring – the blood plasma business. The optionality sits in what a chastened CSL might do with future cash flows. If the company becomes more humble, more focused and more disciplined, the next phase of value creation may not require heroic scientific wins. It may simply require fewer bad decisions.

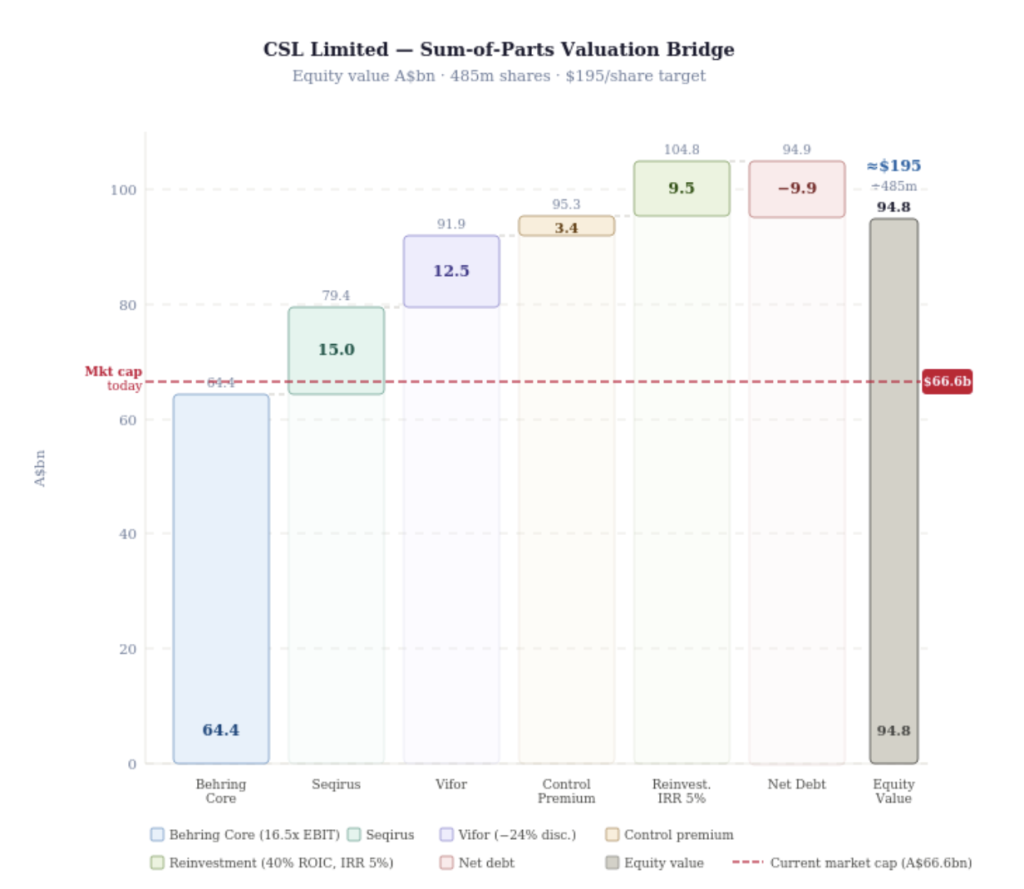

Our long-run valuation has broadly sat around the low-$230s since 2019. That valuation has come down by around $35 over the past 12 months. At $230, our valuation sat $70 below the market for a number of years because it was never heavily dependent on Vifor and the Behring franchise still does most of the real economic work.

Figure #2: First Samuel CSL valuation – Sum of Parts

Figure 2: Sum-of-parts valuation bridge – CSL Limited. Equity value A$bn. Source: internal analysis.

Today, with the stock price down far more than our estimate of intrinsic value, a large part of the move appears to be driven by sentiment and multiple compression rather than a collapse in core earnings’ power. The market does not need to agree on the stock’s full value for it to be attractive. It only needs some confidence that future cash will be invested more sensibly than it was in the Vifor period.

The bridge to our valuation below shows the not-too-heroic assumptions required to reach $195 per share (currently $137). Behring at 16.5x EBIT, Seqirus (influenza vaccines) sold or demerged as an IPO at $15b, Vifor at 24% discount to purchase price, a takeover premium of 5% and a return on reinvested cash flows (research and development) of $9.5b.

At the time of our purchase, CSL accounted for almost 4.5% of the ASX300 index. Its share price had fallen 15% during the previous 12 months. On a risk-adjusted basis, it represented a reasonable opportunity to reduce tracking error (the difference from the index).

With hindsight, we could have waited longer. The position size meant we have seen a portfolio impact slightly lower than the index impact – stronger relative performance, but that is cold comfort against an absolute loss.

Additional Material: What CSL actually is

CSL operates three businesses with very different economic profiles.

CSL Behring — the plasma and specialty biologics division — collects donated blood plasma, processes it and turns it into medicines for immunology, bleeding disorders, hereditary angioedema and critical care.

Seqirus makes influenza vaccines.

Vifor sells iron-deficiency and kidney-disease therapies.

In FY25, group revenue was US$15.6 billion: Behring US$11.2bn (72%), Seqirus US$2.17bn and Vifor US$2.23bn. Within Behring, immunoglobulin products alone generated US$6.1bn. Behring drives the value. Seqirus and Vifor affect the multiple and the investment narrative, but the core franchise sits entirely in Behring.

Source: CSL presentation materials

Why the stock de-rated

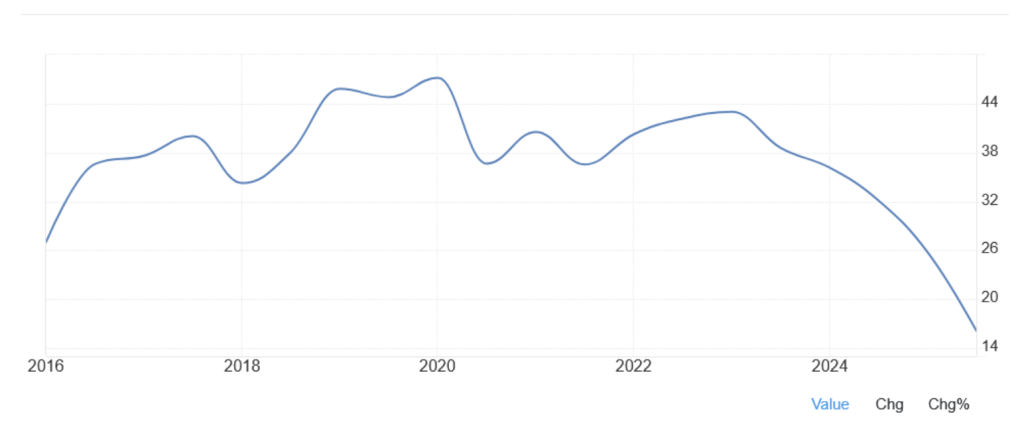

The share-price fall — from a peak above A$300 to around A$130 today — reflects four compounding factors, not a single event.

The first is that the premium rating had become too ambitious. The market priced CSL not merely as a strong healthcare company but as a near-flawless capital compounder. That distinction matters: high quality can still disappoint when the bar is set that high.

The second is that innovation disappointed at the wrong moment. At a premium multiple, cash generation alone is not enough — the company must keep replenishing the future. CSL has had genuine successes, including garadacimab (Andembry) — but the broader pattern has disappointed.

The Phase III AEGIS-II trial for CSL112 failed in 2024, removing one of the most visible pipeline hopes. Other programs have been delayed or narrowed. A premium multiple can absorb normal attrition; it struggles when failures suggest the pipeline was never as deep as assumed.

The third is capital allocation. Without a large franked dividend stream, CSL’s valuation depends heavily on management reinvesting cash wisely. For years, that trust was central to the investment case. The Vifor acquisition broke it. Once investors doubt the next dollar will be well spent, the premium multiple falls quickly.

The fourth is governance. The board appears too close to the old success story. The second strike on the remuneration report in 2025 was a signal that shareholder patience is no longer unlimited.

The final point [is this a fifth compounding factor is a separate item?] is that the market hates mixed messages – especially in the short-term. In one direction, it sees a powerful core plasma franchise. In the other, it sees vaccine uncertainty, an acquisition that diluted quality, restructuring charges, impairments, leadership turnover and a thinner-than-expected innovation ledger. When markets cannot neatly separate the strong core from the noisy edges, they tend to value the whole enterprise more harshly than the core alone deserves.

Figure 3 shows this clearly. In 2022 at ~A$300, investors paid ~40x earnings. Today at ~A$137, with EPS actually higher than in 2022, the multiple is ~16x. Earnings have held up. The confidence paid for has not.

Figure #3: Price-to-earnings (historical P/E) CSL since 2017

Source: TradingEconomics

What broke the premium multiple?

• weaker scientific productivity

• poor capital allocation through Vifor

• a governance discount

• lower-quality non-core assets

Behring: Plasma the franchise that still matters most

CSL has made mistakes. The key question is whether those mistakes have damaged the Behring franchise. They have not — not in any way the share price chart would suggest. Behring’s three structural strengths remain intact: durable demand, a hard-to-replicate collection network, and established earnings power from products already in clinical use.

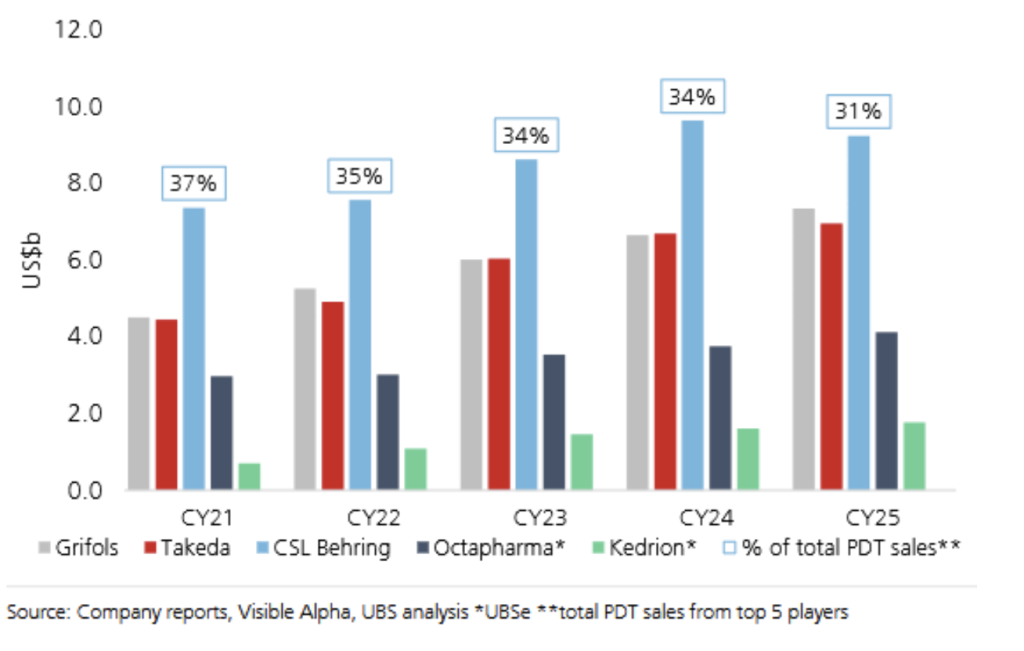

Immunoglobulin is a clinically necessary therapy with no substitutes. The market grows at a steady mid-to-high single-digit rate across multiple geographies and conditions, with benign competitive dynamics. Five or six players highlighted in the graphic below supply the global market. FY25 global Ig revenue of US$6.1bn demonstrates the scale.

Next is the collection. Plasma is a real-world product. It is physical, regulated, operationally intense, and deeply path-dependent.

CSL Plasma operates one of the world’s largest and most sophisticated plasma collection networks, which is a strategic asset. Collection infrastructure, donor relationships, logistics, fractionation capability, manufacturing reliability and regulatory know-how all reinforce one another. Unlike in Australia, where unpaid Red Cross donors play a big role, the US and other markets have a paid collection infrastructure. Your author recalls visiting the poorest places in the US to see the concentration of plasma collection centres, such as the one shown in the picture below.

The moat around the CSL competitive position is the system. We put a lot of weight on collection and fractionation, getting the maximum out of a litre of blood. The system is expensive to build, difficult to scale and very hard to replicate quickly.

This is also why yield matters. Management has highlighted programs that could reduce plasma collection needs by around 20% over time. Every improvement in yield means more saleable products from the same underlying plasma base. That reduces collection intensity, improves resilience and strengthens the economics of the installed network.

CSL has, however, lost market share in recent years — a genuine execution failing that contributed to the de-rating and the CEO change (see Figure 4).

Figure 4: Plasma-derived therapy sales US$bn – 2021–2025 (UBS Research)

Margins and margin pressure have also played a key role. The market once assumed that margins would simply march back to the old highs as if the post-COVID distortion had been temporary. That was too simple.

On the other hand, there is no evidence that Behring has become structurally mediocre. The more accurate view is that margins remain structurally strong, even if they are less likely to revisit the market’s old heroic assumptions. Over time, Behring’s economics should still be supported by mix, yield, scale, contracting discipline, and the simple fact that immunoglobulin is a hard market to enter and serve well.

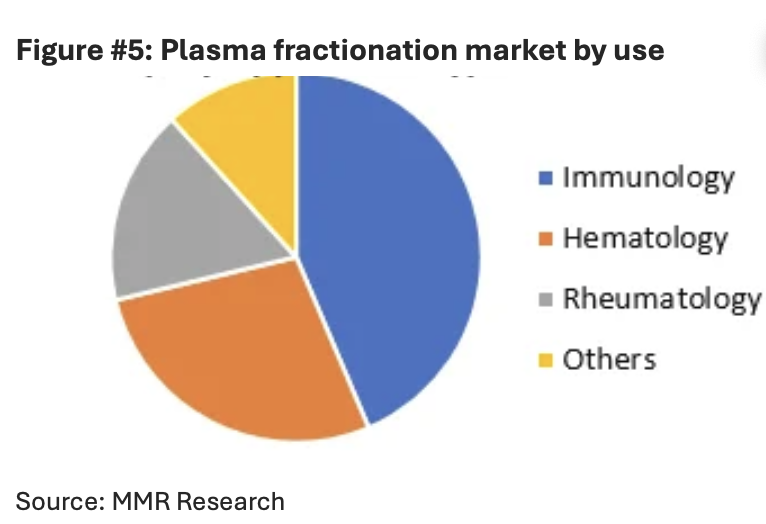

The chart below shows market share in the US$32.96bn global fractionation market split into different uses.

The market is right to discount Vifor and Seqirus. It is wrong to apply the same discount to Behring. Behring does not need to be perfect — it only needs to remain what it is: a scarce, durable franchise with pricing support and long-lived demand.

Innovation: where credibility broke

The problem is not that individual programs have failed — failure is normal in drug development. The problem is the cumulative pattern: a decade of R&D investment (US$1.4bn in FY2025 alone) has not supported the level of scientific productivity once priced into the stock. We have held this view since 2019. Today, little future value, which is not clearly outlined in products near approval, is ascribed to the stock.

Unlike building a new supermarket (Woolworths) or expanding a rubbish tip (Cleanaway) where the investment broadly replicates the past, CSL must invent its own future. It starts with a wealth of knowledge and strong relationships, but it is still science. Should it generate a return higher or lower than its cost of capital? Returning more than the cost of capital adds to valuation; returning less reduces value, and pure failure rapidly reduces value. Recent outcomes have not been favourable.

The largest single setback was CSL112. In February 2024, the Phase III AEGIS-II trial failed to meet its primary efficacy endpoint of reducing the risk of major adverse cardiovascular events at 90 days, and CSL said there were no plans for a near-term regulatory filing. That mattered because CSL112 had been one of the more visible later-stage efforts to extend the story beyond the plasma base. .

The supporting cast did not help.

At the October 2024 R&D briefing, CSL disclosed that the HIZENTRA study response rate was within the expected range, but that the placebo group showed an unexpectedly high response rate. That is not the same thing as a toxic failure, but in market terms it still reads as friction: another example of a program that does not straightforwardly convert scientific effort into clean commercial momentum.

More recently, the first-half 2026 numbers included a US$430 million impairment on the group’s self-amplifying mRNA platform, which management attributed to declining COVID disease burden and more onerous US regulatory requirements. Again, one can write a charitable version of this. The technology is evolving, markets change, and regulators move. But the harsher and, in our view, fairer conclusion is that the cupboard has looked thinner than the old premium multiple allowed for.

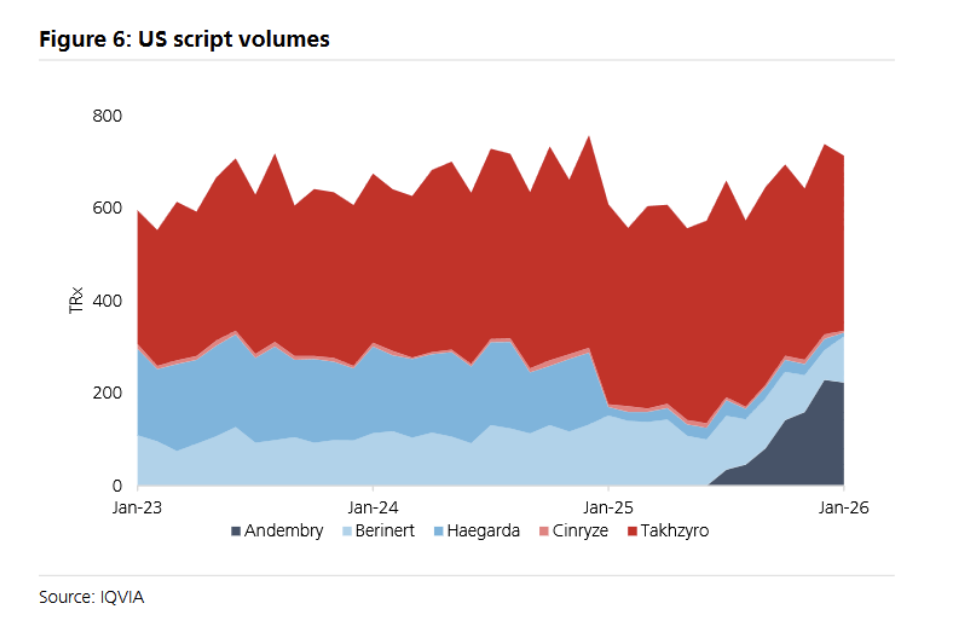

There are genuine bright spots. Andembry, the anti-FXIIa HAE product garadacimab, received approvals across six major markets in FY25 and uptake has accelerated (see figure #6, below). Building on wins like this could support a re-rating over time.

As an investor in biotechnology for almost two decades, the role of CSL and its innovation programs within Australia and globally shouldn’t be understated. The market assumed CSL was good at investing in future biotech. Decades later, the platform hasn’t delivered outside of a relatively limited scope of expertise.

That is why the issue is scientific productivity, not mere bad luck. The company has spent heavily on R&D and continues to do so. In FY2025, CSL invested US$1.4 billion in R&D. Yet the shape of the visible pipeline today feels narrower, more dependent on line extensions and commercial execution, and less obviously capable of commanding the premium once attached to the group.

Vifor: a poor acquisition, not just a difficult one

We view Vifor as fundamentally a poor acquisition.

That is a stronger statement than saying the deal was merely too expensive or badly timed. It means the acquisition damaged the overall investment case and contributed to the stock’s re-rating.

Vifor was expensive. CSL acquired Swiss pharmaceutical company Vifor Pharma for A$16.4bn in 2021, paying a 60% premium for its stock. It increased exposure to markets with less certain long-term demand, added complexity to a group that did not need more moving parts, and undermined confidence in capital allocation at precisely the time investors were relying on management’s judgment to justify the premium multiple.

The strategic issue sits in the end-markets. Plasma and immunoglobulins are not easy businesses, but their demand outlook is relatively legible. Kidney care is different. It is clinically important, commercially meaningful and still capable of growth. But it is also much more exposed to changes in disease management, reimbursement, treatment pathways and broader cardiometabolic medicine. CSL bought into that complexity at a moment when the story was already becoming harder to underwrite.

The emergence of GLP-1 therapies sharpens the point. The exact science did not need to be perfectly known for management to exercise greater caution. By the time the market had fully started to absorb the broader renal implications of the obesity and diabetes drug wave, the logic of paying-up for kidney-related demand growth looked less secure. The FLOW data showed semaglutide (Ozempic) reducing clinically important kidney outcomes, and the FDA subsequently approved Ozempic to reduce the risk of worsening kidney disease and cardiovascular death in adults with type 2 diabetes and chronic kidney disease.

Today, Lilly’s Retatrutide has moved deeper into late-stage development as part of a new generation of cardiometabolic medicines. The point is not that these drugs eliminate kidney disease tomorrow. It is that they obscure the long-run demand assumptions for parts of the nephrology market. In our view, CSL should have been more alive to that risk.

Seqirus: valuable, but lower quality

Seqirus is not a bad business — it is a lower-quality one, and that distinction matters for how the group is valued. Flu vaccines are more seasonal, more policy-sensitive and more volatile than plasma products. By FY26, CSL guided to a mid-teens revenue decline for Seqirus — worse than its own prior guidance — reflecting a sharp post-COVID fall in US vaccination rates. A demerger makes strategic sense: not because Seqirus is secretly worth a fortune on its own, but because separating it would allow investors to value Behring more cleanly.

The point is that it should no longer interfere with how investors think about Behring. If CSL wants to be valued more cleanly, then separating the lower-quality vaccine exposure is a rational move.

Governance, leadership and the future use of cash

Governance is discussed here because it has become a valuation issue, not merely an organisational one. The question is whether CSL’s governance structure is still well-suited to the company it has become. In our view, the answer is sufficiently uncertain to justify a governance discount. Our view is that the board appears too close to the old CSL success story, with too much weight placed on continuity and not enough visible evidence of strategic renewal.

Leadership change intensified that concern. Paul McKenzie retired as CEO in February 2026, and Gordon Naylor stepped in as interim CEO. The appointment of a 33-year CSL veteran, moving directly from the CSL Board to the position of CEO, symbolises the governance concerns the market has raised. The market knows that and prices accordingly.

Value creation depends on successful reinvestment and disciplined execution. Simply executing better may appear important today, and it is the type of issue boards can obsess over. But the value proposition for CSL is future cash flows and their use.

Governance matters, especially because of cash

CSL remains a strong cash generator. Future value depends heavily on what management and the board choose to do with that cash. There is no large franked distribution stream; it doesn’t pay much Australian tax, so CSL cannot anchor the shareholder experience in the same way as other large Australian companies can.

When governance is trusted, and reinvestment is assumed to be well managed, that is a feature. When governance is questioned, it becomes a discount.

The irony is that the loss of trust may improve the future. Humility can be productive. A company that has been punished for overreach often becomes more disciplined than one that is still being cheered on by the market. That possibility is central to the current opportunity. CSL may now be better placed to create value simply by being more focused, less acquisitive and more realistic about where it does and does not have an edge.

That points to what the new CSL should become: a tighter, more focused Behring-led healthcare company, owning a small number of strong franchises and applying a much tougher hurdle rate to anything outside the core. If the company cannot evolve into that, then it should move further in the direction of simplification.

Conclusion

CSL is no longer the stock the market once imagined. That is not necessarily bad news.

The old premium valuation rested on too much faith in perpetual growth, scientific productivity and management judgment. Those assumptions have been challenged. Innovation has been weaker than hoped. Vifor was a poor acquisition. Governance now deserves to matter. Seqirus deserves a lower multiple than Behring. The market has been right to withdraw some of the old premiums.

But the market may now be making a second error by applying too much of that punishment to the core business. Behring remains a strong franchise, with durable immunoglobulin demand, a global plasma collection moat and an earning base that does not require fantasy to justify it. If that is right, then the stock no longer needs perfection to work. It only needs restraint, focus and better future use of cash.

That is why CSL now looks less like a broken growth story and more like a high-quality business in a credibility reset. The reset may be creating the most interesting entry point the stock has offered in years.

We are likely to add to the position over FY26, although we believe there is no rush.

Glossary

Key terms, drug names, conditions and abbreviations used in this report.

DRUG AND PRODUCT NAMES

Privigen — CSL Behring’s main intravenous immunoglobulin (IVIG) product. Administered by infusion in hospital or clinic, used to treat primary immune deficiency disorders and certain autoimmune conditions. One of the largest single revenue lines in the group.

Hizentra — CSL Behring’s subcutaneous immunoglobulin (SCIG) product — administered under the skin, so patients can self-infuse at home rather than attending a clinic. Faster-growing than IVIG, reflecting a broad shift towards home-based therapy.

Andembry (garadacimab) — A once-monthly preventive treatment for hereditary angioedema (HAE) developed by CSL Behring. It blocks a protein called factor XIIa (FXIIa) that triggers HAE attacks. Approved in Australia, Japan, Europe, the UK, Switzerland and the US in FY25.

Clazakizumab — An experimental drug in development at CSL Behring for cardiovascular complications in end-stage kidney disease, currently in Phase III clinical trials. CSL has also licensed broader rights outside this specific indication to Eli Lilly.

CSL112 — A drug candidate designed to rapidly reverse cholesterol deposits in arteries and reduce the risk of a second heart attack. The large Phase III trial (AEGIS-II) failed in February 2024, and CSL shelved development plans — the most significant pipeline setback in recent years.

Filspari (sparsentan) — A treatment for IgA nephropathy, a chronic kidney disease in which immune deposits damage the kidney’s filtering units. Part of the Vifor portfolio. Approved in the US and growing in Europe.

Tavneos (avacopan) — A treatment for ANCA vasculitis, a rare autoimmune disease causing severe inflammation of blood vessels, particularly affecting the kidneys. Part of the Vifor portfolio.

Velphoro (sucroferric oxyhydroxide) — An iron-based medication that controls phosphate levels in dialysis patients. High phosphate is a serious complication of kidney failure. Part of the Vifor portfolio.

Ozempic / semaglutide — A weekly injectable drug made by Novo Nordisk, originally for type 2 diabetes and now widely used for weight loss. Clinical trial data (the FLOW trial) showed it significantly reduces kidney disease progression, which has implications for long-run demand for some Vifor products.

Retatrutide — An experimental drug in development at Eli Lilly for obesity, diabetes and related conditions — part of the next generation of GLP-1-based medicines. Mentioned as a further potential headwind for kidney disease treatment demand.

MEDICAL CONDITIONS

Immunoglobulin (Ig) — Proteins (antibodies) produced by the immune system to fight infection. CSL collects donated blood plasma, extracts and purifies these proteins, and administers them to patients whose immune systems cannot produce adequate quantities themselves. Delivered either intravenously (IVIG) or subcutaneously (SCIG).

IVIG (intravenous immunoglobulin) — Immunoglobulin delivered directly into a vein, typically in a clinic or hospital. Used to treat primary immune deficiency, autoimmune nerve disorders, and various inflammatory conditions.

SCIG (subcutaneous immunoglobulin) — Immunoglobulin delivered under the skin, usually self-administered by the patient at home. A faster-growing segment than IVIG as it offers patients more independence.

HAE (hereditary angioedema) — A rare genetic condition causing sudden, severe and potentially life-threatening swelling attacks in the skin, gastrointestinal tract and airways. Andembry (garadacimab) is approved to prevent these attacks.

Haemophilia — Inherited conditions in which blood does not clot normally due to missing or defective clotting proteins. CSL Behring manufactures replacement clotting factor products for haemophilia patients.

Albumin — A protein in blood plasma that maintains fluid balance and transports substances around the body. CSL’s albumin products are used in surgery, trauma, liver disease and intensive care. A significant revenue contributor, particularly in China.

SID (secondary immune deficiency) — A condition where the immune system is weakened by another illness or its treatment — for example, cancer chemotherapy or certain medications. A growing segment of immunoglobulin therapy demand as more SID patients are identified.

CIDP (chronic inflammatory demyelinating polyneuropathy) — A progressive autoimmune condition damaging the protective myelin sheath around nerve fibres, causing limb weakness and impaired sensation. Immunoglobulin therapy is a standard treatment. Also relevant to competitive dynamics around anti-FcRn drugs.

MG (myasthenia gravis) — An autoimmune disease causing muscle weakness by blocking signals between nerves and muscles. Immunoglobulin therapy is used in acute management and is relevant to anti-FcRn competition.

IgA nephropathy — A chronic kidney disease in which IgA antibody deposits build up in the kidney’s filtering units, gradually impairing function. Filspari (sparsentan) is approved for this condition.

ANCA vasculitis — A rare but serious autoimmune disease causing inflammation of small blood vessels, often affecting the kidneys and lungs. Tavneos (avacopan) is approved for this condition.

SCIENCE AND PIPELINE TERMS

GLP-1 (glucagon-like peptide-1) therapies — A class of drugs that mimic a hormone regulating blood sugar and appetite, originally developed for type 2 diabetes and now widely used for weight loss. Ozempic (semaglutide) is the best-known example. Their proven kidney benefits have raised questions about future demand for some Vifor products.

Anti-FcRn therapies — A newer class of drugs that reduce levels of abnormal immunoglobulins in the blood. Being used or trialled in conditions such as CIDP and myasthenia gravis, they represent an emerging form of competition to standard immunoglobulin therapy in some indications.

mRNA (messenger RNA) platform — A technology that instructs cells to produce a specific protein, triggering an immune response. Best known from COVID-19 vaccines. CSL invested in a self-amplifying version; it took a US$430 million write-down on this platform in early 2026 following reduced COVID demand and US regulatory challenges.

Fractionation — The industrial process of separating donated blood plasma into its individual components — immunoglobulins, albumin, clotting factors and others. CSL’s fractionation facilities are central to its competitive position: expensive to build, heavily regulated, and a significant barrier to new entrants.

FXIIa (factor XIIa) — A blood protein involved in triggering HAE attacks. Andembry (garadacimab) works by inhibiting this factor, preventing the chain of events that leads to swelling episodes.

AEGIS-II — The large Phase III clinical trial for CSL112, testing whether the drug could reduce major cardiovascular events in the 90 days after an initial heart attack. It enrolled over 17,000 patients and its failure in early 2024 was a major setback for CSL’s drug pipeline.

TDAPA (Transitional Drug Add-on Payment Adjustment) — A US Medicare reimbursement policy providing supplementary payments to dialysis providers for newly approved drugs for a limited period. Some Vifor products have benefited from TDAPA inclusion, but this support is temporary.

Nomogram collections — A more precise, data-driven method of determining how much plasma to collect from each donor, based on their weight and other measurements. The shift to nomogram collections is expected to improve yield — the usable product extracted per donation — over time.

The information in this article is of a general nature and does not take into consideration your personal objectives, financial situation or needs. Before acting on any of this information, you should consider whether it is appropriate for your personal circumstances and seek personal financial advice.