An IPO with more than $75bn of meaning to markets

Copyright 2026 First Samuel Limited

This week Craig takes a deep, deep dive into SpaceX and, at $75bn, the largest ever IPO1:

- A dramatic challenge for markets

- The role of ETFs, passive investment and limited ‘free float’

- The limits of SpaceX as a conglomerate

- Where will SpaceX’s IPO proceeds go?

- Valuing strategic momentum

- Markets’ capacity to absorb

- SpaceX’s IPO as a litmus test

Note, SpaceX will not be in the S&P Dow Jones indices for at least 12 months, and only then if it is profitable. However, it will be in the MSCI (the global shares’ benchmark), FTSE Russell and Nasdaq indices after 15 days.

1 The deal is the largest Initial Public Offering, almost three times larger than the previous – Saudi Aramco at $29bn, but not the largest capital raising. That honour went to Alphabet (i.e. Google), which raised $85bn last week.

Read the previous Investment Matters here:

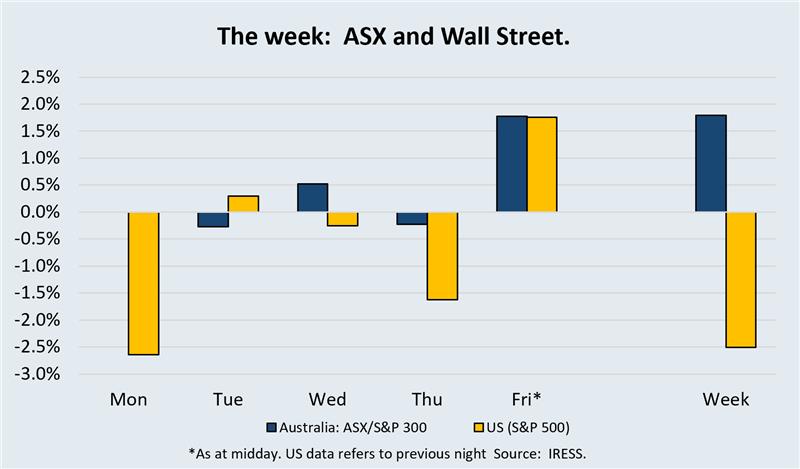

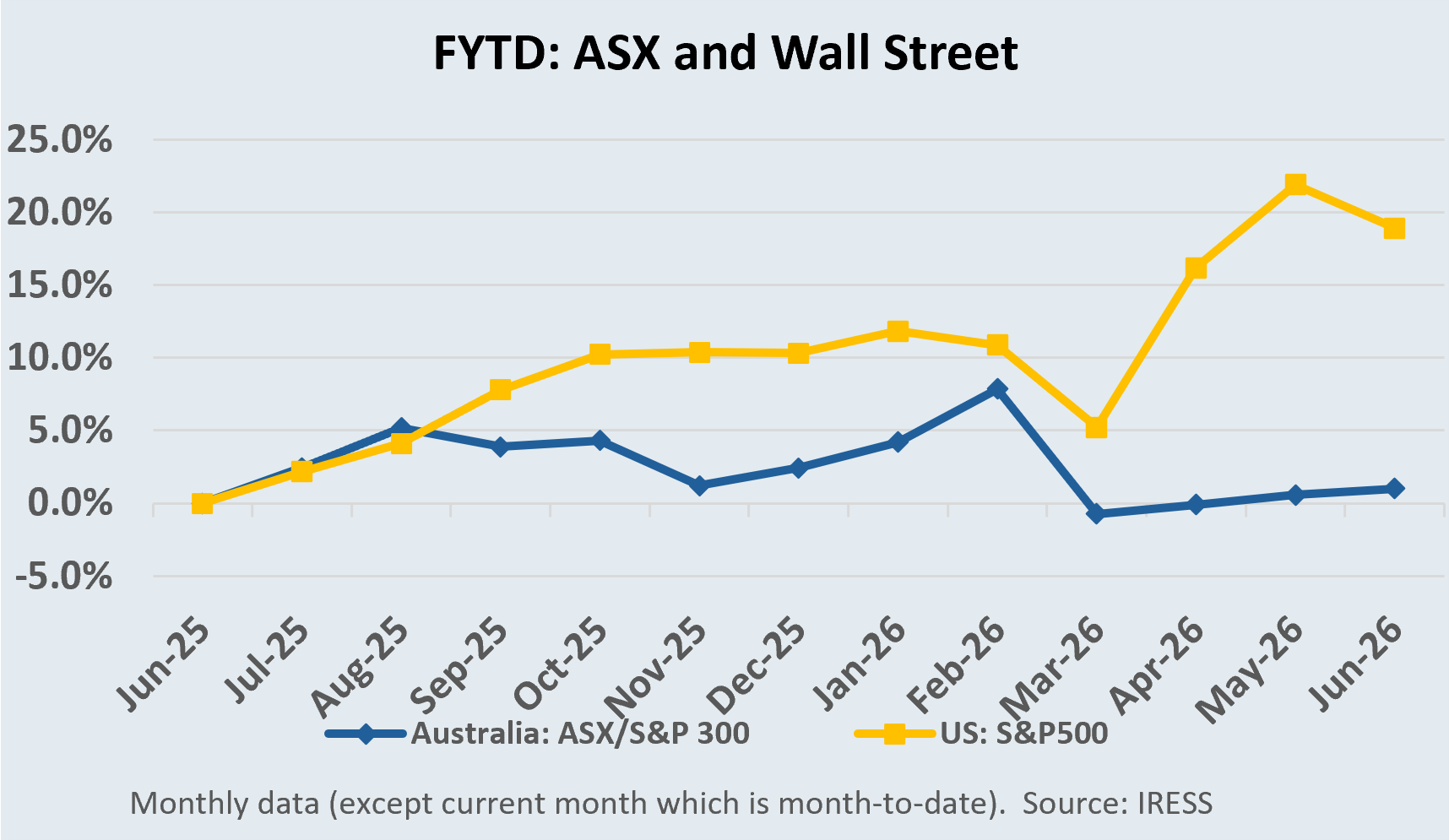

The market

An IPO with more than $75bn of meaning to markets

On Saturday morning, Australia time, SpaceX will trade on US markets. Depending on how successfully it trades, the company will be the most expensive company ever IPO’d (Initial Public Offering). Whilst only a small amount of the company will be sold in the IPO, the $75bn raised to buy the stock will be the largest on record.

SpaceX is a vertically integrated space infrastructure company founded by Elon Musk. Its original business was launching, designing, manufacturing and operating reusable rockets to carry satellites, cargo and people into orbit. Falcon 9 remains the workhorse, and reusability has given SpaceX a major cost and cadence advantage in global launch markets.

The listed SpaceX conglomerate also owns Starlink, the telecommunications company and XAi, which includes the X (formerly Twitter) platform and Grok, the AI application. The success of the IPO is not only critical to Elon Musk’s wealth, but it will also provide context for myriad other questions about the market, the current economic cycle, and the nature of economic development going forward.

Figure#1: What is SpaceX?

Source: SpaceX IPO Prospectus

What are the issues raised by the SpaceX IPO, and how do they affect markets?

There are seven important issues raised by the SpaceX IPO.

- The importance of narrative and storytelling versus valuation and price.

It is a great story, but it is being sold for a very high price, $1.7trn. SpaceX, as an idea, sells itself, with a broad scope of future-oriented narratives, plans, and themes. But the extreme valuation not only requires that its existing plans be delivered with high likelihood but also requires future unaccounted-for development to succeed.

We will discuss the SpaceX valuation in the context of our market views in a later section.

- Narrative and storytelling: SpaceX is being sold as more than a company. It is space, satellites, defence, AI infrastructure, communications, founder genius and American industrial strategy in one package.

- Cold hard value: SpaceX posted a $4.94bn loss in 2025 despite revenue rising to $18.67bn. A $1.7trn valuation for a company losing $5bn with only $18bn of revenue, that does not make it uninvestable, but it makes clear what the market is being asked to do: price a strategic future, not current earnings.

- Regulatory problems: As an investor who appreciates more details rather than less, and forecasts with veracity rather than buzzwords, it is interesting to reflect on changes in global regulations around IPOs. Fundamentally, markets have moved more towards buyer-beware, giving companies far greater freedom in what they may say about their futures.

We appreciated the quote in a recent New York Times op-ed noting the continued weakening of traditional restraints, which eventually granted executives a wide berth for “speculative optimism,” said Amit Seru, a finance professor at the Stanford Graduate School of Business. “Combine that with a culture increasingly comfortable with long-duration technology bets, and the equilibrium naturally shifts toward more aggressive storytelling.”

- Artificial demand.

The size of the float and the global interest in the IPO highlight the role of passive investment and Exchange Traded Funds (ETFs) in modern markets.

- Generally, for a company to be included in a market index (and therefore, generally, purchasable by an ETF), it needs to trade for several months, to be profitable, and to have a high percentage of the company available to purchase.

- SpaceX fails all these tests – it lists this week, it loses money, and more than 90% of the company will be retained by Elon Musk and existing owners (referred to as limited free float).

- In a perfect world, this company wouldn’t be included in market indices nor purchased by an ETF. So imagine the scenario when up to 40% of the market in the US, which is owned by passive index investors, is instead forced within a short period (less than 1 month) to need to scramble to purchase stock in SpaceX that they are not otherwise allocated, generating abnormal market signals and excess demand in the short-term.

- The index issue is uncomfortable. Nasdaq has bent its rules to quickly accommodate SpaceX, reducing the seasoning period and weakening the old free-float discipline that should normally protect index investors from scarcity-driven pricing. Not only that, but they have also pretended, for the purposes of its index, that the free float is 3x larger than it is.

These actions create a visible buyer with a timetable. In the first month, demand will not be purely fundamental: IPO allocations, hedge-fund pre-positioning, Nasdaq-100 buying, ETF flows, derivative hedging and a large greenshoe will all interact with a very small tradeable float.

Note that SpaceX will not be included in S&P Dow Jones indices until both 12 months have lapsed and it is profitable. Technically speaking, this will make only a modest difference to demand because of much larger Nasdaq and MSCI indexed-based demand.

- For our clients with an International Securities sub-portfolio, this is less of an issue. Despite MSCI, which operates a broad international ETF (VGS/VGAD) that also uses an early-inclusion framework, not being SpaceX-specific and its weights being free-float-adjusted, the direct benchmark risk should be modest.

- But even a small MSCI weight can generate meaningful dollar demand across global portfolios. The result is a listing in which early price discovery may be overwhelmed by mechanical flows, scarcity, and index implementation rather than by a clean assessment of value.

Figure #2: Explaining index-driven demand

Source: FT Research

- Conglomerate issue.

Forty years after markets decided conglomerates destroy value, imagine the irony of SpaceX as an extraordinarily large, diverse, and ultimately expensive conglomerate leading markets’ imagination. Especially considering the concerns regarding conglomerates are all there…

- Visibility in conglomerates is limited. SpaceX has provided at best scant details of its business.

- Inefficient Capital Allocation: Often conglomerates subsidise underperforming subsidiaries using profits from successful ones, rather than allowing capital to flow to the highest-yielding opportunities. At SpaceX, not only are Starlink profits used in the rocket business, but the entire company is investing new capital in XAi despite its limited existing business model.

- Lack of Synergy is another conglomerate concern – but in the case of SpaceX, this is less of an issue.

Which leaves the big questions. Will the imprimatur of Elon Musk reverse market wisdom? Are governance concerns and Tesla’s patchy track record relevant? Regarding governance, SpaceX is asking public shareholders to fund a company in which Elon Musk retains dominant control. That may be acceptable if investors believe he is the asset. It is much less comfortable if they believe the public market is being used mainly as a liquidity and funding mechanism while control remains private in substance.

For passive and retail investors following the hype, there may be demand in the short run, but eventually underlying institutional demand is likely to settle at a different equilibrium price.

- As a litmus test for AI demand.

The SpaceX IPO in an important litmus test for future trillion-dollar IPOs, including OpenAI (ChatGPT) and Anthropic (owner of Claude AI). Not only is the performance of the SpaceX IPO an indication of expected demand for other listings, but experienced market participants are wary of the challenge provided by historical precedents.

Those with long memories understand that market excesses often generate the conditions in which such IPOs are engineered – and that they can be a precursor to future weakness. In the context of stretched valuations, this may provide the most significant impact in the medium term.

- As an indicator of the size of investment required in AI.

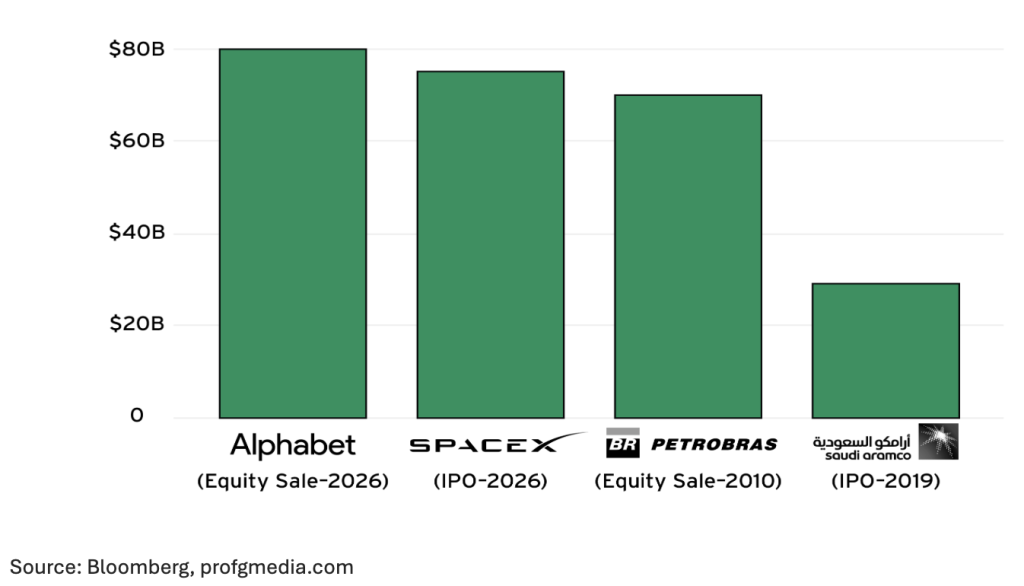

Ultimately, IPOs and equity raisings alike are about how companies plan to spend their money and where the proceeds of the IPOs are funnelled. We have noted that the SpaceX IPO is the largest ever, despite the small percentage raised. But there are also equity raises undertaken for existing companies, and one announced on 1 June 2026 for Google (Alphabet) broke all records at almost $80bn.

It relates directly to the SpaceX IPO insofar as the purpose of Google’s equity raise was also to fund predominantly AI-related capex. The chart below shows that, in combination with Google, the SpaceX IPO dwarfs the size of other equity raises, including Saudi Aramco (oil) in 2019 and the sale of Petrobras (Brazilian oil) in 2010.

Figure #3: Largest equity sales and IPOs

- Valuing strategic momentum and government support.

Stepping back, SpaceX, as a non-government company, is playing a role that governments once assumed. SpaceX is not a pure-play launch company. It is launch, Starlink, military communications, sovereign infrastructure and perhaps future space-based compute. SpaceX is partly a geopolitical tool in space and in ground communications through Starlink, and in the battle for AI supremacy through Grok and other AI models with China and the rest of the world.

That makes it strategically important in a way most listed companies are not. This is a new form of an old problem – does bundling several national-capability assets create a premium, or does it make the company harder to govern, regulate and value?

- Is there capacity to absorb these IPOs when future revenues are uncertain?

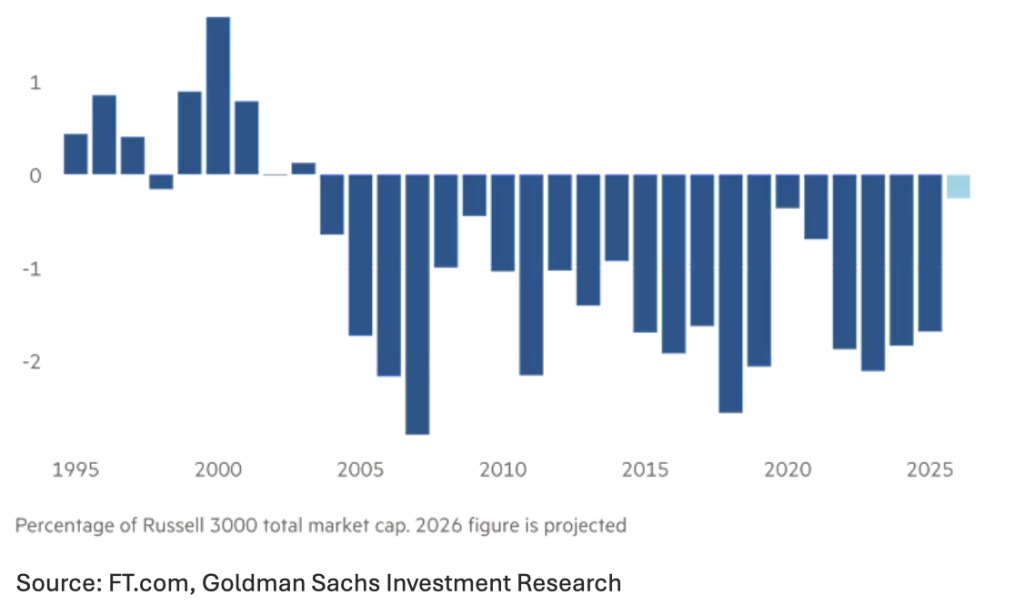

Finally, the size of potential IPOs also strains the US markets’ capacity to add new equity, especially when these funds are used to finance a capital expenditure bill that is growing dramatically. A point to note about the US markets is that for many years, the total amount of new equity injected into the markets has been negative.

That may initially strike readers as strange, but the US is a curious market. Without franking credits and with a growth focus, many companies pay zero or very small dividends. Companies return capital to shareholders through share buybacks, in which they buy back shares and cancel them, reducing the number of outstanding shares and providing additional value to remaining owners.

The figure below shows the net issuance being negative since the early 2000s, with the previous dotcom bubble the last sustained period of positive issuance (IPOs + equity raising > buybacks). The current IPO boom could push the US toward neutral levels again in 2026. This dynamic, which tests underlying demand in the absence of net buybacks, is an interesting feature when combined with the scale of the IPOs and their aggressive pricing.

Figure #4: IPO Boom: Stock supply towards positive levels: US net equity supply % of market cap

Source: FT.com, Goldman Sachs Investment Research

Importance of valuation

Despite all the hype and limited information, valuation isn’t impossible, and there have been a range of valiant attempts to determine what price one should pay for SpaceX. Your author can comfortably say that using his experience the number that he would arrive at would be a fraction of the price offered, but all who look at valuation are ultimately undertaking a similar exercise. All are trying to ascertain what future cash flows, profitability and asset investment is likely to deliver in the medium term.

Within this context we were excited to read the work on SpaceX of a valuation legend. Aswath Damodaran is a renowned professor of finance at the NYU Stern School of Business, widely celebrated as the “Dean of Valuation”. He is an iconic figure in the global financial community, globally recognised for his expertise in corporate finance, investment philosophies, and Discounted Cash Flow (DCF) analysis. We use some of his parameters and assumptions regarding companies in general on an everyday basis.

Because he was writing for a broader audience Aswath Damodaran’s work on SpaceX is useful because it separates two things markets often deliberately blur: story and value. He does not dismiss the story. In fact, he describes SpaceX as a unique company with immense competitive advantages, and argues that its engineering record has repeatedly embarrassed the sceptics. But his framework forces the narrative into numbers: target revenues, margins, reinvestment, cost of capital, share count and governance. That is precisely the discipline an IPO of this scale requires.

His conclusion was not that SpaceX is a poor business. It was that, at its IPO price, it is too expensive for an investor using intrinsic value as the anchor.

This distinction matters for the IPO. A trader may still want the stock because of scarcity, momentum, index demand, Musk, Starlink, AI and the sheer cultural force of the event. But for a long-term investor, the question is does the company’s future cash flows justify the entry price?

This was a useful reminder of the merits of our underlying process – but it doesn’t detract from the interest in the SpaceX story and how it trades. Definitely one to watch.

The information in this article is of a general nature and does not take into consideration your personal objectives, financial situation or needs. Before acting on any of this information, you should consider whether it is appropriate for your personal circumstances and seek personal financial advice.