Key Takeaways

- The ABS National Accounts show falling GDP per capita, reflecting ongoing economic challenges in Australia.

- Global factors, including China’s influence, have contributed to rising wealth inequality and dependence on leverage.

- The Reserve Bank’s monetary policies face challenges amid weak consumer spending and wage growth, complicating future reforms.

- Investments in companies like Lynas and BlueScope Steel demonstrate potential growth amid changing economic dynamics.

- Assessing the connection between the operating economy and market performance reveals important distinctions for investors.

The latest ‘National Accounts’ (i.e. GDP and how its constituents contributed) released (this week) give cause to reflect on how your investments consider trends in the data.

The National Accounts is the scorecard for the RBA, politicians and policymakers alike.

It is useful to be reminded that the RBA and the US Fed have roughly similar aims.

“The Federal Reserve’s dual mandate is maximum employment and price stability. In its simplest terms, we want everyone who wants a job to be able to find one and for inflation to average 2 per cent per year.” John C. Williams, President and CEO, Federal Reserve Bank of San Francisco (March 2016)

In Australia, the Reserve Bank Act 1959 notes the Board’s duty to contribute to the stability of the currency, full employment, and the economic prosperity and welfare of the Australian people.

Similar goals often inform politicians, although it can reasonably be said that pure power and politics also play a part in their motivations.

Read the previous week’s Investment Matters.

The market

Reform

Between the 1960s and the mid-2000s, economies such as Australia and the US provided a narrow remit for monetary authorities (i.e. the RBA and the Fed), allowing the political process to shape policy and drive reform.

In Australia, reformers of the slap-dash variety, such as Whitlam, populists like Hawke, technocrats like Keating, and political realists like Howard and Gillard, played a reforming role. Reform was undertaken with economic tailwinds spurned on by financialisaton and high leverage.

China’s role

China since the early 2000s provided an external deflationary impetus to the global economy, helped fund global deficits, and purchased our expensive resources. Even Deng Xiaoping, the paramount leader of China, became famous for the slogan “to get rich is glorious,” whether he ever actually said it or not. China now leads the world in money growth and leverage expansion over the past 20 years.

But there are consequences.

Global imbalances began to grow in wealth and inequality, as well as in capital and trade flows between China and the rest of the world. Leverage (debt) grew exponentially throughout world. Wealth soared globally, along with leverage. “One man’s debts are another man’s assets” (Ray Dalio). Proverbs 22:7 says, “The rich rule over the poor, and the borrower is slave to the lender.”

Slaves

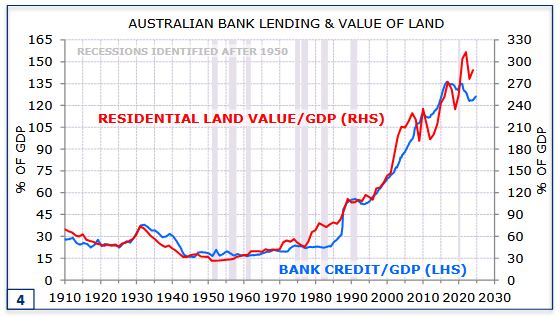

At sufficiently high levels of wealth and debt, an economy becomes a slave to both, especially in an economy like Australia, where our predominant source of wealth is an historical endowment of space and resources, with the remainder being real estate. The correlation between the explosion of Bank Credit leverage and land prices is clear.

Figure 1: Bank Credit availability has driven up land prices

Source: RBA, APRA

In Australia, we turned our advantage in the early years of leverage into reform (GST, labour relations, retirement incomes, R&D investment, mining investment).

Still, we fell short in so many ways:

- busting duopolies

- supporting business investment;

- reforming targeted rent-seeking landowners in critical parts of the economy;

- infrastructure development;

- Henry-like tax reform;

- intergenerational equity; and

- productivity-enhancing training and investment.

Why did we slow reform? There was an easier model, involving more people and more debt, with the hope that a massive intergenerational wealth transfer would bridge the gap to the next round of productivity and investment.

The ABS National Accounts release, including GDP growth this week, highlighted the uncertainty a generation of missed opportunities has created.

Weak operating economy

The operating economy is weak, but the share market remains strong, with total returns since June 30, 2024, of 13.5%, despite three corrections throughout the year.

Figure 2: Australian share market. ASX300 including dividends

Source: First Samuel, IRESS

We wanted to highlight why there can be a distinction between the operating economy and the wealth of the economy expressed in terms of share market capitalisation. Despite the connections, what’s best for markets may not be best for the broader economy in the short run. In the long run, we hold that the connection remains important.

Does Australia have the time and opportunity to course correct? Of course, we are fabulously wealthy and resilient, but the problem is that we now need to reform within the context of a changing global order in trade and capital flows, and at a time of geopolitical flux.

The best window for reform and policy is one with increasing wealth and leverage. Otherwise, the leverage and wealth ultimately define the reform and policy objectives. Why? As wealth and leverage grow, supporting the performance of wealth-related assets (such as stocks and real estate) drives real economic outcomes. On the flip side for debtor, the need for low inflation and low interest rates becomes more critical than wage growth or productivity.

We have reached this point.

At the same time, wealth seeks new opportunities that evade the risks of reform and adjustment. New companies that need a reform agenda, a duopoly-busting plan, or look to disintermediate existing business models face institutional and political barriers. Equity markets become increasingly disconnected from economic outcomes.

Successful companies and successful portfolios operate at the edge of the economy rather than at the core in circumstances such as these. For Australians, this has also involved investing a significant portion of our wealth, derived from domestic debt and historical endowments, in assets beyond our shores, including global equities and companies, the ultimate disconnect between wealth and the operating economy.

There are still linkages that we need to consider, especially those that drive discretionary spending. “The stock market isn’t the economy” is a well-worn adage. Still, economists at Oxford Economics have found that movements in equities and other financial assets are increasingly influencing how consumers perceive the future, with significant consequences for their spending.

What does this have to do with your portfolio?

Let’s look at the top 10 positions in the portfolio today. They represent the marginal exposure to the real economy that we have discussed. Whilst many are operating in Australia and nearly all are managed from Australia, their competitive position is either secured by industry concentration or only has tangential exposure to broad economic growth.

- QBE is a global insurer that benefits from higher interest rates, and a world that needs to continue to invest in new fixed assets, and insure the assts they already have in increasingly volatile conditions.

- Cleanaway takes out the rubbish. We create rubbish regardless of the profits we generate, and lower wages pressure is positive for Cleanaway’s margins. Almost duopoly conditions operate in the Australian waste market, and Cleanaway has around a 40% market share.

- BlueScope Steel benefits from trade conflict, infrastructure investment in Australia and the US, and from a world in which Chinese excesses are constrained by policy measures including tariffs.

- Life360 is a location-sharing and safety app that helps families and friends stay connected and safe. It provides almost the perfect anecdote to increasing societal anxiety, and is one of the best performing stocks on the ASX.

- Reliance Worldwide – global sales of plumbing supplies.

- Macquarie Group – leading global investment bank, market disruptor in Australia banking and poised to benefit from increasing investment.

- Sandfire Metals – global demand for copper, the core of electrification of the world.

- Inghams – duopoly chicken provider to near duopoly supermarkets and heavily concentrated fast food industry, and of course protected from international competition through quarantine restrictions

- Worley – global provider of engineering services.

- Santos – producer of oil & gas.

In the next 10 prominent positions we only have meaningful direct exposure to the Australian domestic economy through SGH (Boral, Coates Hire and Caterpillar WA), Seek and EarlyPay (invoice financing).

In many ways, our portfolio is a microcosm of the myriad decisions within the economy. There is limited investment in:

- investment-oriented companies or their operations;

- companies that rely on growing household consumption; or

- companies that benefit from new entrepreneurism or business formation.

And perhaps, most importantly, few positions rely on higher productivity within the economy.

What did the ABS National Accounts say?

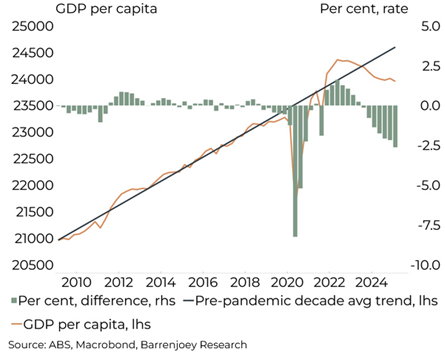

Critically, in our view, GDP per capita is still falling (-0.2% q/q; -0.5% y/y) and has continued to contract since Q3-22, marking the most prolonged ‘recession’ in history (since at least 1959).

Figure 3: GDP per capita per quarter: trends and recent performance

In terms of market expectations, the GDP outcome was below the RBA’s expectations (0.4% q/q) in its latest forecasts in May. It included weaker momentum in consumer spending than the RBA had expected. With retail sales in April also falling unexpectedly, the RBA is likely to revise its outlook for consumption growth and inflation downward.

The opportunity for the RBA to continue to cut interest rates remains throughout calendar 2025.

Unfortunately, the RBA continues to overestimate wage growth and consumption. It is not without good reason that the mistake is made. However, the simple reality in Australia today is that with an excess supply of workers, especially among the millions of temporary residents, and at a time when limited investment is taking place, there is little in the way of wage inflation, which exacerbates the intergenerational wealth divide.

The capacity to generate wage growth is also limited by the productivity of the labour being employed. Total cost of employment, that is, wages share, is rising, but that is enhanced by low productivity rather than by shortages per se, in our view.

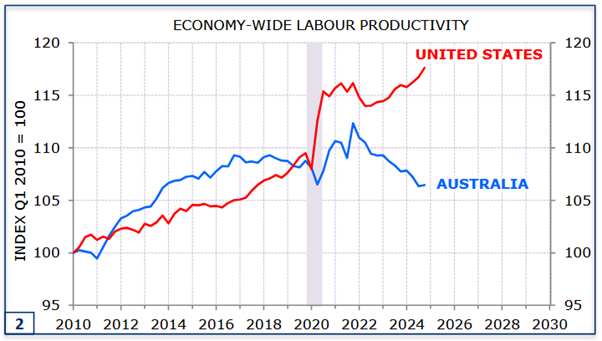

The haunting gaps in productivity between the US and Australia since 2010 have now become vast. Some of this is explained by the industry mix, including the NDIS, and lagged changes in mining investment, but all are long-run choices in our view. Ones that have led to weak overall outcomes, at a time when higher leverage and global demand provided alternatives.

Figure 4: GDP per capita trends and recent performance

Source : Minack Advisors

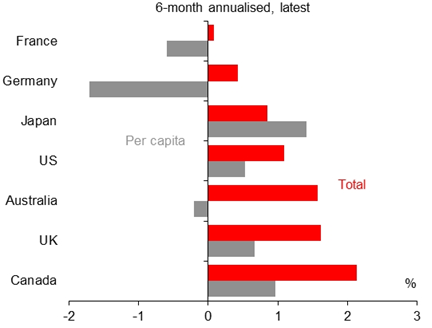

Low economic growth is a recurring phenomenon worldwide, which is one reason why the implications of our low growth are muted at this stage. The figure below shows Real GDP on a 6-month annualised basis across a range of countries. Note, however, that our per capita outcomes (grey bars in the chart) are not comparable in the UK, Canada, Japan or the US.

Figure 5: Real GDP growth – international comparison

Source: ABS Macquarie Research

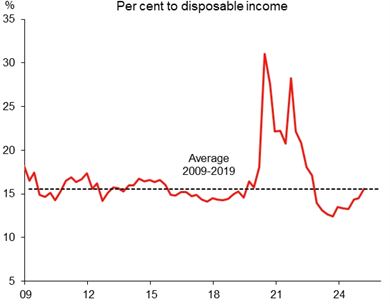

Rising savings rates also mirror the response to weak wealth creation drivers, shown in Figure 7 below. Today’s data show that households have limited appetite to lift spending (with consumer confidence still at below-average levels). While households’ real disposable incomes have risen, the pressure to save remains, with the gross savings rate having just returned to the average levels seen in the decade preceding the pandemic.

Figure 7: Australia Gross Household Savings Ratio

Source: ABS Macquarie Research

Part of the reason for the real income growth to be saved is the imbalance in who owns the vast levels of household deposits, versus those who have increasing costs of living. While higher interest rates have positive impacts on some households, the flip side is higher debt costs for those with mortgage payments. Those with existing savings generate higher real incomes, while those with limited savings experience limited income growth or utilise hard-won savings as an opportunity to pay down debts.

When the levels of savings and wealth on one side, and debt and liabilities on the other, were small, changes in the real economy, not the financial system, remained the primary policy lever.

Returning to the opening theme… At some point, reform and policy changes become so beholden to the tangential impacts on interest rates and wealth that otherwise sensible reform that can drive enhanced productivity, investment, capital growth and national savings is thwarted by near-term considerations.

Summary

In summary, we will continue to generate investment ideas that maximise wealth within the economic system in which we operate. But we are also always looking for changes in these trends, that is, when otherwise overlooked parts of the economy once again regain primacy through reform and policy options.

We have seen such a move in BlueScope Steel and Lynas in the past couple of years. Macquarie Group and SGH are always looking for such changes, and we suspect developments in private health could be an example in future years.

The information in this article is of a general nature and does not take into consideration your personal objectives, financial situation or needs. Before acting on any of this information, you should consider whether it is appropriate for your personal circumstances and seek personal financial advice.