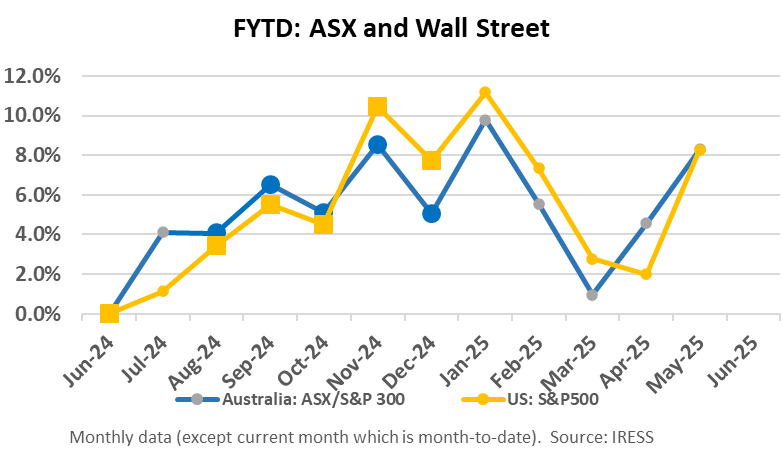

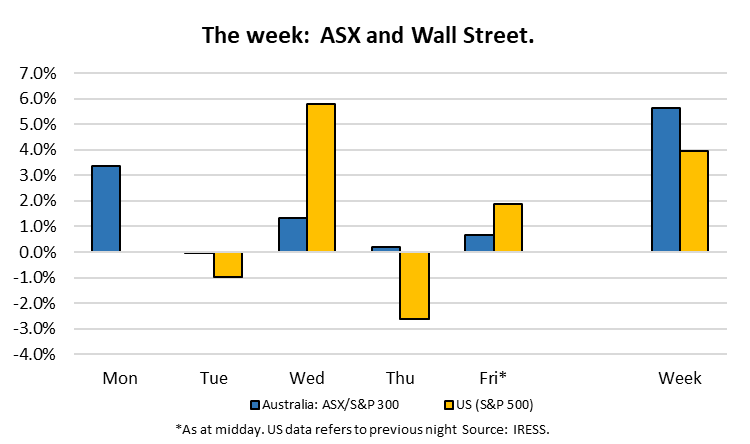

A relatively quiet week in markets, where global markets have drifted higher. US markets experienced a rapid rise through May, following the tumult of April.

In Australia, we saw the takeover of another portfolio position in Metals Acquisition Corporation (MAC). Readers may recall that we owned the Cobar NSW-based MAC in combination with Aurelia Metals, a company discussed in detail in Investment Matters recently.

Harmony Gold Mining Company Ltd, a USD 9 billion company listed in South Africa and New York, bid for MAC. Harmony’s operations are truly global, including in Papua New Guinea. As they further develop the MAC Cobar mine and gain a better understanding of the entire region, they may seek to consolidate other regional players. They can certainly buy Aurelia Metals, with a mere A$500m in market capitalisation.

This week’s Investment Matters highlights two portfolio positions, Lynas Corporation and Develop Global.

Read the previous week’s Investment Matters.

Lynas Corporation a deep dive

Lynas Corporation is a Rare Earths mining and processing business with mine assets in Western Australia and production facilities in Kalgoorlie and Malaysia. It plans to establish additional facilities in Texas in the future.

Mt Weld, one of the world’s highest grade Rare Earths mines, is located 35km south of Laverton in Western Australia.

Rapid technological advances have led to the growing importance of Rare Earth minerals in various domestic, medical, industrial, and strategic applications due to their unique catalytic, metallurgical, nuclear, electrical, magnetic, and luminescent properties.

Examples of the many applications for Rare Earth elements are their use in magnets and super magnets, motors, metal alloys, electronic and computing equipment, batteries, catalytic converters, petroleum refining, medical imaging, colouring agents in glass and ceramics, phosphors, lasers and special glass.

Figure 1: Rare earth elements (REE) – Applications

Source: MRS Bulletin June 2022, Recent advances in the global rare-earth supply chain

Our portfolio position in Lynas Corporation was first purchased in January 2020 for $2.00 per share. Following the recovery of markets post-COVID, and increased understanding of the likelihood of geopolitical conflict with China, the Lynas share price rapidly grew. With assistance from the Australian and US governments, the company was identified as a critical piece in developing global resilience in the supply of Rare Earths.

We retain approximately 15% of the original holdings, and the position in Lynas accounts for around 1% of clients’ Australian Equity sub-portfolios. Despite the share price appreciation since 2020 (to $9 per share in 2021), we continue to see value in the position, especially on a 5+ years view. Lynas possesses a unique combination of features that provides an additional benefit for the portfolio overall.

Lynas provides benefits to the portfolio greater than it would as a stand-alone investment.

These features include;

- Long life assets – at current mining rates, without further exploration, the Mount Weld mine will run for more than 20 years, and exploration and drilling are likely to expand this supply. Durable long-term assets reduce portfolio risks and increase resilience against inflation.

- Government-subsidised capital investment in critical markets, including Australia and the US.

- The outlook for rare earths pricing is positively skewed. There is a higher risk of much higher prices than much lower prices.

- It is possible that critical minerals pricing becomes bifurcated, with two global prices from two separate global supply chains.

- A supply chain that excludes China will result in higher prices. Materially higher margins and ROE would be expected on existing investment in plant and equipment.

- Absent higher rare earths prices, Lynas’s position on the lower part of the non-Chinese supply chain would limit downside.

- Lynas’s stock price tends to rise as geopolitical tensions increase. Stock markets are generally negatively impacted by rising geopolitical tension. A holding in Lynas, which appreciates when the rest of the market is suffering, reduces overall portfolio volatility. One of the reasons for updating readers regarding Lynas in this week’s Investment Matters is to note the stock’s performance surrounding recent Trump tariff uncertainty.

Why is the geopolitical aspect so crucial to Lynas Corporation?

The current global Rare Earth element (REE) supply chain is highly imbalanced and tightly controlled by just a few countries. Such an imbalance of the critical metals supply chain poses a significant challenge to the energy transition strategies and the national security of many nations.

Lynas holds a unique position as the only significant producer of scale of separated Rare Earths outside of China. Rare Earths are essential inputs to high-growth global manufacturing supply chains, including digital age technologies and green technologies such as electric vehicles and wind turbines.

But the industry has become dependent on China through a range of strategic interventions by the Chinese Government.

A journal article titled Rechttps://inldigitallibrary.inl.gov/sites/sti/sti/Sort_57446.pdfent advances in the global rare-earth supply chain, MRS Bulletin (Materials Research Society) published in 2022, provided a clear diagram of the way in which China has created a concentration of supply.

Figure 2: What drove global industry concentration in Rare Earths towards China

Source: MRS Bulletin June 2022, Recent advances in the global rare-earth supply chain

The similarities between the diagram above and the rhetoric of tariffs and geopolitical brinkmanship in 2025 should be transparent. It remains our contention, as outlined in recent Investment Matters reports, that the latest tariff skirmishes between China and the US are rooted in long-term economic development as much as they are the whims of a political leader.

Recognising the problem with the concentration of supply for products at the core of future defence and electronics industries, the US and Australian governments developed a joint Critical Minerals policy. The aim was clearly to create an alternative supply chain to the one dominated by China. In time, we also believe that Europe, particularly its defence and automotive industries, will need a dedicated non-Chinese supply chain.

After the joint political response, Lynas Rare Earths signed a follow-on contract with the U.S. Department of Defence (DoD) for the construction of the Heavy Rare Earths component of the Lynas U.S. Rare Earths Processing Facility in Texas (August 2023). The updated contract includes a contribution by the U.S. Government of approximately US$258 million, an increase from the approximately US$120 million announced in June 2022. The direct subsidy of almost A$400m is not inconsequential in a market cap of $7.4bn today and approximately $2bn at the time of the original acquisition.

The recent outbreak of uncertainty regarding Trump and tariffs provided a perfect example of how Lynas trades in such periods (Figure 3). In addition to general unease, the importance of rare earths to geopolitics was underlined by April.

Beijing introduced new export controls in early April on seven rare earth elements and related permanent magnets, materials crucial for the production of electric vehicles (EVs), wind turbines, fighter jets, and advanced electronics. The move followed sweeping US tariffs, announced by President Donald Trump.

The value of Lynas’s non-Chinese supply chain came to the fore. The figure below shows the higher prices and increased market volumes traded in Lynas following the Trump tariff announcements. In response to a pause and reduction in US tariffs on China, the Lynas share price fell again.

Figure 3: The response to Lynas’ share to rising tariffs and geopolitical uncertainty

Source: First Samuel, IRESS

Current operations

As noted, one of the strengths of the Lynas asset is the long life of its Mount Weld mine located in Western Australia. In February, the latest financial result, the company noted a substantial uplift in the Mt Weld mineral resource and ore reserve. The 2024 Mt Weld Mineral Resource and Reserve Update supports a 20+ year life of mine at the target 12,000 tonnes per annum of NdPr (neodymium-praseodymium) finished product production capacity.

The company continues to progress its major projects, delivering increased capacity, efficiency, and sustainability. While prevailing market prices have been weak, Lynas is well-positioned to benefit from improvements in market prices. With most of our valuation of Lynas based on its assets and future capacity, the short-term issues with price are not critical. The company remains well-funded.

During the 1H25 financial year, Stage 1 of the Mt Weld Expansion project went into operation, ramping up production occurred at the Kalgoorlie Rare Earths Processing Facility. Lynas continued work on a Texas Rare Earth plant in January-March. The company is in talks with the US government over additional funding support for the project. Recent US tariffs and water treatment issues have increased its Texas project costs. The first Trump administration backed Lynas’ US project in 2019, invoking the Defence Production Act to fund marketing, engineering, and design work.

The Department of Defence noted that Rare Earths are critical inputs to advanced technologies in commercial and defence applications. At the time of the announcement, the Lynas project, when completed, will be the only scale producer of separated Heavy Rare Earths outside of China.

Once operational, the Texas Facility will source its feedstock from the Lynas Mt Weld rare earths deposit and the Kalgoorlie Rare Earths Processing Facility in Western Australia.

What are the risks?

As investment managers, we are sometimes questioned on the need to reduce the size of positions as they become successful; why not simply let them grow?

Often, company stock prices can be cyclical; share prices fluctuate between cheap and expensive with regularity. This is especially the case for well-understood positions. Buying cheap, selling expensive makes sense.

For other companies, especially those with fast growth or strategic assets, where the range of outcomes remains particularly uncertain, scenario analysis is crucial. Scenarios can be defined in terms of scrap value, downside case, base case, and a range of upside cases.

Excellent investments occur when we pay only the downside or scrap value of a business, despite believing that the base case or upside cases are still possible. This was the case when we first investigated Lynas. As a stock price approaches the base case, we would generally reduce our holdings.

As the share price rises, however, fleshing out the various upside cases and gaining a clearer understanding of what drives the downside becomes more critical.

With Lynas and the influence of geopolitics, tightly specifying the upside cases is challenging but exciting. Markets can be dazzled by the prospect of upside scenarios. Unfortunately, in my experience, downside cases tend to be just as important and often much less exciting.

What is the unexciting downside factor for Lynas? A higher global supply that permanently reduces Rare Earth prices, despite a positive geopolitical environment.

Despite being called Rare Earths, the name is a bit of a misnomer. There is generally a lot of Rare Earths, but not in high concentrations, and not in locations that benefit from cheap electricity, favourable demographics and a plentiful water supply. But prolonged high prices of Rare Earths—and the fear of not having them—makes bold solutions seem reasonable. Investors in Brazil are demanding the opening of the Amazon rainforest to mining, while entrepreneurs propose extracting Rare Earths from the sea floor or harvesting them from the Moon.

And to prove that most of 2025 begins and ends with Trump, many point to the securing of Rare Earth resources in Greenland as vital to the supply of these critical minerals.

We have ultimately chosen to keep a relatively small 1% position in Lynas, expecting to profit as the development of the global supply chain becomes clearer through 2030.

Develop Global

Another interesting, smaller position in clients’ Australian shares sub-the portfolio is Develop Global. The company owns a recommissioned mine near Canberra, known as Woodlawn, a mining services company with industry-leading management and experience, as well as a range of options for future mine development.

The company is concentrating on the new energy type materials, predominantly copper and zinc. The combination means the stock plays a role in our mining services, as well as our copper and base metals baskets.

The restarted Woodlawn project is fast approaching a sustainable operating rhythm. First copper production was declared, and the concentrator was turned on in the second half of March. Ahead of the internal schedule and on budget, producing saleable copper concentrate. It will still take time to get the polymetallic circuit humming, but it is already producing saleable concentrate.

Figure 4: Woodlawn Mine ROM pad ore stockpiles

Source: Company reports

We purchased our position in December 2024 for clients with capacity in their mining services basket. The investment followed extensive meetings over the past couple of years and a tour of its Woodlawn Project.

Our entry price for Develop Global is $2.30. The share price is likely to remain volatile. Trading closer to $4.00 per share today, the market is appreciating the value of its assets as they come on stream. More evidence from operations will be required over the coming 2-3 years to realise all the possible value we envisage.

Building on the themes developed in the previous section, we believed that we could purchase Develop Global shares at a price consistent with its downside case. The optionality contained in its business plan and other assets was “free”.

Management style and flexibility

Part of the optionality in Develop Global that was especially interesting to value was the explicit sequencing of growth ambitions that the CEO Bill Beament, was able to plan out. Mining services and their ability to generate low-risk cash flow would be utilised to build equity stakes in mining operations that require the mining expertise and capital markets access provided by Develop Global.

Like a great retailer keeping their first local supermarket as the cash cow to develop new retail ideas that leverage their understanding of the customer, Beament was doing the same in the mining services industry. The difference was that Beament’s previous success with listed companies meant that the firepower he could secure to grow was much larger. But still, it all starts with mining….

The figure below outlines the plan to leverage mining services to build and own underground mining assets. All the while using cash flow to avoid share dilution and create wealth for early investors.

For the plan to work, the assets they develop will still need to be as viable as any other mine, but the focus on cash flow and optionality aligns closely with the way we like to invest. In addition, the emphasis on leveraging one success into another and derisking the balance sheet through time increases the positive skew in the potential value of the company.

The Group is continuing to work with HSBC on a potential strategic asset-level sale for the Woodlawn asset. Develop will consider a sale of up to 20% of the Woodlawn asset. Several parties have been taken through to the next phase of the process.

Figure 5: Develop Global Business Plan

Source: Develop Global Company reports

This week saw more evidence of the business plan in action.

Success in the Woodlawn restart and expectations that the company sells part of the operating Woodlawn mine to generate additional cash appear to be already unlocking future options. The company announced that it has commenced substantial works, including the construction of the boxcut for the underground decline and preparations for surface infrastructure, at its Sulphur Springs zinc-copper project in Western Australia.

Over the next six months, operations at Woodlawn will be crucial. The more cash the business can generate in a shorter time frame, the less reliant the company is on a partial Woodlawn asset sell-down to fund new growth options including Sulphur Springs.

Sulphur Springs

For several years, we have been excited by the opportunity to develop their Sulphur Springs asset. The difficulty has always been coordinating the funding of its development in a value-enhancing manner. The combination of strong copper and zinc prices, along with the expectations of free cash flow generation in other assets, has unlocked such an opportunity for Develop Global through FY26.

As shown in the figure below, the Sulphur Springs project is located 144 km to the southeast of Port Hedland and includes the Sulphur Springs and Kangaroo Caves deposits together with other tenements. The targets have returned intersections of commercial-grade copper and zinc in previous feasibility studies in 2023.

Figure 6: Sulphur Springs project location

The preliminary work is being undertaken alongside an updated definitive feasibility study (DFS), scheduled for completion in the December 2025 quarter. This will pave the way for project funding and a Final Investment Decision (FID). We anticipated that the project could be worth more $1.00 per share.

Figure 7: Site view of current progress at Sulphur Springs

Summary

Develop and Lynas each loom as small, but highly prospective, near and long-term investment opportunities in client portfolios. We look forward to keeping readers informed of each company’s respective progress and as well as each contributing further to positive investment performance.

The information in this article is of a general nature and does not take into consideration your personal objectives, financial situation or needs. Before acting on any of this information, you should consider whether it is appropriate for your personal circumstances and seek personal financial advice.