Copyright 2026 First Samuel Limited

This week in Investment Matters:

- If the guns fall silent: markets and the peace dividend

- SGH Investor Day: relentless compounding

Read the previous Investment Matters here:

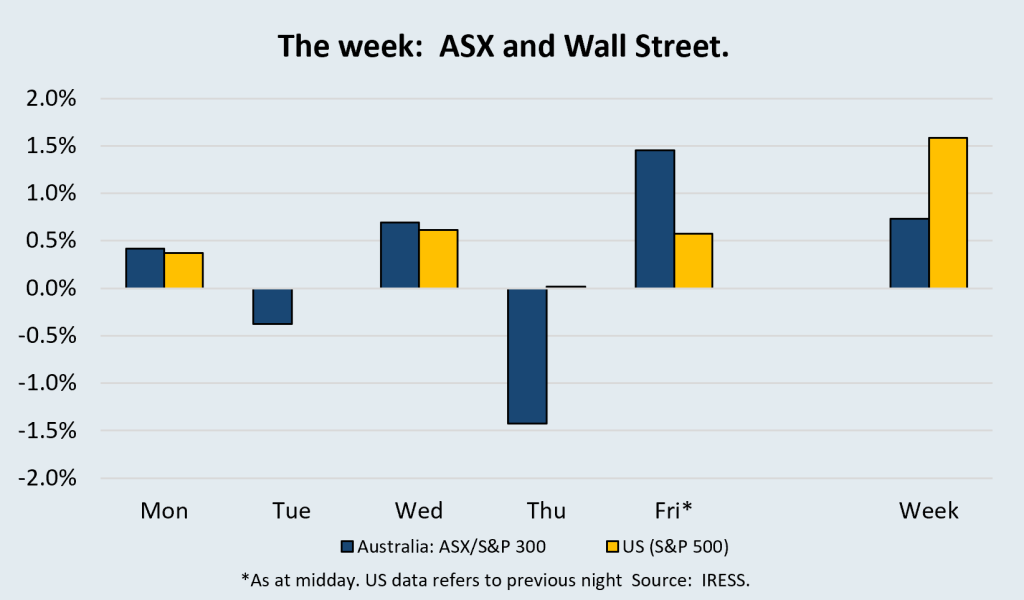

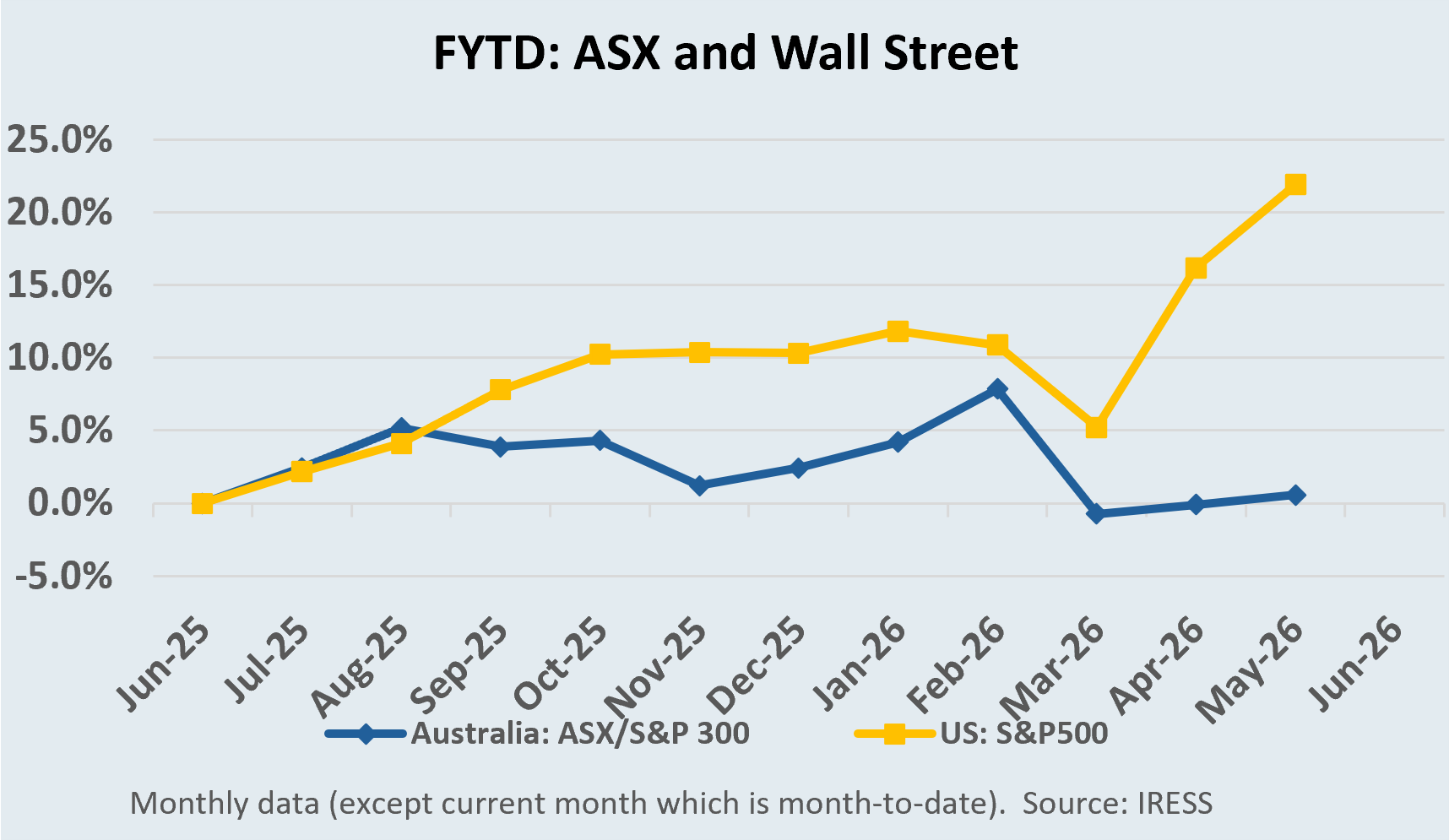

The market

The Upside in De-escalation

Last week we noted that global bond markets were not prepared to give investors much credit for the possibility of Middle East de-escalation. US long bond yields remained elevated: the chart below shows the US 10 year Treasury yield for the month of May.

Markets were still pricing the risk of further tightening, and the broader economic backdrop remained cautious. This week tangible moves towards resolution have seen yields compress from 20 May and oil prices to fall.

Figure #1: US 10 Year Treasury yield has fallen in the last week.

Figure #2: Brent crude oil price has fallen to its lowest since early April

But the investment question is not only whether the current environment is difficult. It is whether the balance of risks is beginning to shift.

Oil

The key variable is oil. At around US$110 a barrel, oil is doing a lot of work in the current inflation outlook. It is lifting headline inflation, adding pressure to transport, logistics and industrial costs, and complicating central bank decision-making. In that sense, the oil price has become one of the main channels through which geopolitical risk is being transmitted into markets.

A durable ceasefire would not solve every inflation problem. Domestic services inflation, wages, rents, insurance and energy costs would still matter. But it would remove one of the clearest external pressures on the inflation outlook. That would be helpful for bond markets, helpful for central banks and helpful for equity valuations.

This matters because financial conditions have already tightened materially. A US 30-year Treasury yield near 5.2% is a meaningful headwind for asset prices. It increases discount rates, raises corporate funding costs and weighs on long-duration investments. If oil were to fall on a credible improvement in the geopolitical backdrop, some of that pressure could ease.

First Samuel portfolios

We believe that First Samuel portfolios are well positioned for the combination of: [note new bullets and semi-colons]

- persistent moderate inflation, increasing the importance of industrial and consumer pricing power;

- higher levels of interest rates than we saw for the past 20 years, increasing the attractiveness of hard assets, existing capital and value-oriented cash flows;

- a resolution of Middle East conflict; and

- without doubling down on the hype of AI and semi-conductor over investment.

For equity markets, the areas most likely to benefit would be those that have been most affected by higher yields and higher input costs. Infrastructure, property, construction materials and other long-duration assets would be obvious candidates. Industrials exposed to freight, energy and fuel costs would also see some relief.

The Australian market would not be immune from this shift. The RBA is still dealing with inflation that is too high, and households are still adjusting to a more difficult cost environment. But lower oil prices would make the inflation task less complicated. It would reduce the risk that central banks are forced to respond to external price shocks, rather than the underlying economy.

Market weights

The current market is already carrying the weight of high inflation, elevated bond yields and geopolitical risk. If one of those pressures begins to ease, the market response could be meaningful. The upside case is now easier to describe.

A durable ceasefire would reduce pressure on oil, improve the short-term inflation outlook, ease strain in bond markets and create a more constructive setting for selected equities. In a cautious market, even a credible reduction in the probability of the worst outcomes can be enough to change the direction of returns.

SGH Investor Day: relentless compounding

We attended the SGH (formerly Seven Group Holdings) investor day on Thursday 21 May.

Catching up with senior management across the businesses was appreciated, and once again we were reminded of the depth of the management teams.

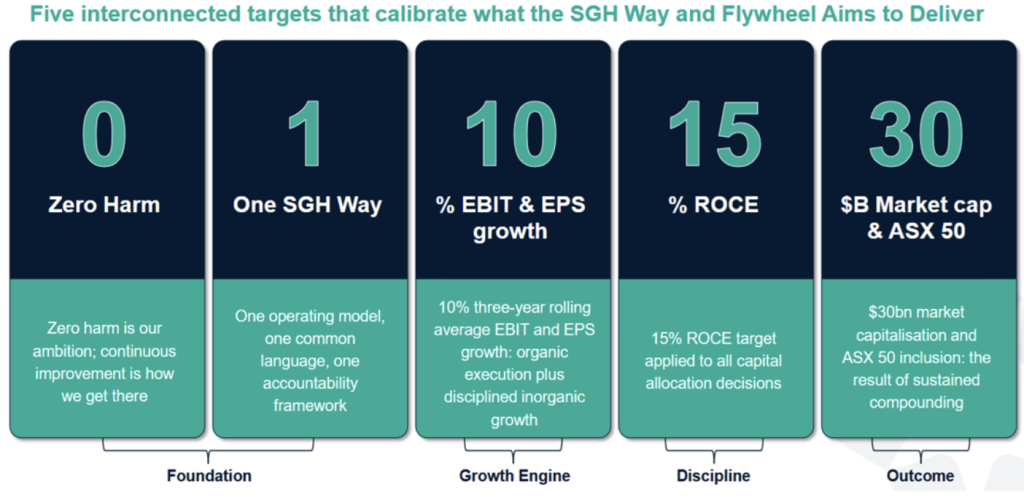

The aim of SGH to build a compounding industrial business is one we appreciate. The figure below, which was the setting for the presentations across the day, is useful to explain the way SGH pursues growth.

Growth is not represented as a standalone ambition. We have seen countless high growth companies that are unbalanced and unsustainable. It links culture, operating process, earnings growth, capital discipline and market value into one operating model.

The model: culture, process, growth, returns and outcome

The model works because each target supports the next. Safety and operating discipline should create a better business system. The common operating model should make improvement more repeatable. Earnings growth should come from both organic execution and disciplined inorganic growth. The ROCE target is the check that keeps growth from becoming empire-building. The market capitalisation target is the consequence, not the starting point.

Figure #3: SGH’s model

Source: SGH presentation

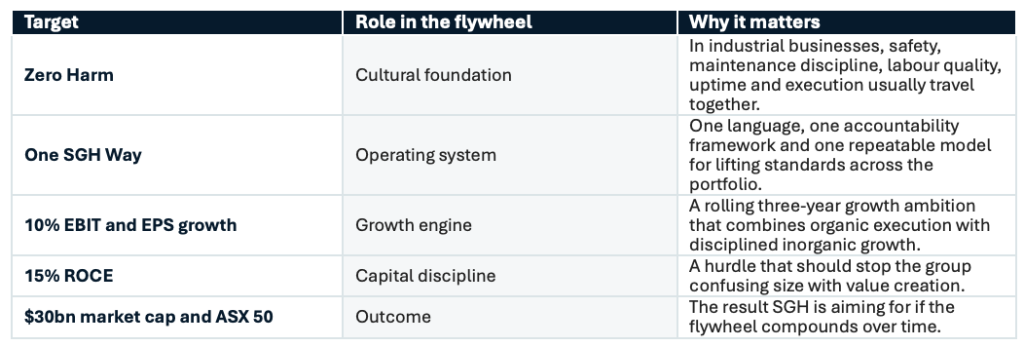

Figure #4: Why the components matter

What we like

SGH is trying to create a company where the same operating ideas travel across businesses. That is valuable because it gives management more ways to improve returns than simply buying another asset.

Why the model suits Australia

When we link this operating model [?] to a respect for cash, we find a company building a durable business well suited to grow in an Australian economy with its own strategic advantages. Australia remains advantaged in mining and minerals, while population growth continues to support infrastructure and construction-hungry activity. SGH sits across these themes with businesses that should benefit from activity, scale, equipment demand, services demand and disciplined execution.

The investor day message was therefore attractive. SGH is not just exposed to activity; it is trying to build a system that can convert that activity into earnings and cash. The opportunity is stronger if the group can take lessons from one business and apply them across the portfolio, rather than allowing each business to operateas a separate island.

Throughout the day as each team discussed the approaches to data, artificial intelligence and cash flow generation, it was clear one system was applied without exception across WesTrac, Boral and Coates, creating the consistency of execution that makes compounding possible.

Boral

Boral remains the most compelling example of what this model produces. The EBIT margin has moved from 3.8% in FY22 to 14.1% today — a transformation driven by pricing discipline, cost control and a simplified asset base. The business is now less volume-dependent, more pricing-led, and focused on return on capital rather than tonnage. Infrastructure and energy transition work continue to underpin demand. We remain watchful about how Boral performs in genuinely weak market conditions — that test has not fully arrived — but the sustainability of earnings through normal industry fluctuations has been impressive, and structurally the business looks stronger than at any point in more than two decades of coverage.

BlueScope Steel bid

SGH’s revised proposal for BlueScope Steel — alongside US Steel Dynamics — is relevant to the same theme. The structure would see SGH retain BlueScope’s Australian and rest-of-world operations while Steel Dynamics acquires the North American business. Ryan Stokes’ articulation of the investment rationale was clear: BlueScope’s Australian steel assets are privileged assets earning a ROIC of around 5%. That is too low, and SGH’s track record suggests it knows how to fix it. The path is familiar — discipline, operational focus, capital allocation rigour — applied to a business with structural advantages that its current returns do not yet reflect. We support the proposal as SGH shareholders and look forward to watching it unfold.

Why the respect for cash matters

The natural question is why SGH will not simply pursue growth through debt, capital raisings and higher risk. This is where ownership matters. The Stokes stake does not want dilution, but it does want intergenerational wealth. That creates a different incentive set from a company primarily rewarded for near-term scale. The family economic interest should favour durable compounding over growth that risks the future.

That does not remove all risk. Any industrial company with a growth ambition can be tempted to stretch the balance sheet or overpay for acquisitions. But the ownership structure gives SGH a reason to respect cash. The better version of the company is not one that constantly raises equity to buy growth. It is one that compounds cash flows, redeploys capital well, and uses the operating system to lift returns inside the existing portfolio and adjacent opportunities.

How we would frame SGH

A cash-backed industrial compounder: operationally disciplined, exposed to Australian structural growth, and supported by an ownership structure that should prefer intergenerational wealth creation over dilution-led expansion.

Valuation discipline still matters

Having said that, quality does not remove price risk. Stock prices are sometimes too high and sometimes too cheap. A compounding business can become over-owned or over-loved, particularly when the market starts to capitalise long-term growth too aggressively. For that reason, we have consistently traded SGH around our valuation metrics, rather than treating it as a stock that should be owned at any price.

The quality of the business model argues for ownership. The respect for cash and the ownership structure support the case that growth can be durable. But the valuation framework determines position size. When the share price moves ahead of our view of value, discipline requires us to be prepared to trim. When the price is too low relative to the compounding opportunity, the same discipline allows us to add.

Signposts to watch

The model will be most credible if growth remains cash backed, acquisitions are disciplined, leverage stays within a sensible range, and the 15% ROCE ambition remains visible in capital allocation decisions. The warning signs would be persistent reliance on new equity, debt-funded growth that reduces future flexibility, or acquisitions that lift earnings but weaken returns.

Conclusion

SGH’s investor day gave us a clearer way to describe the attraction of the company. The SGH Way and Flywheel are not just management language; they are a framework for turning safety, operating discipline, earnings growth and capital returns into sustained compounding. Our role is to own that compounding opportunity when valuation is attractive, while continuing to trade around our valuation metrics when the share price becomes too demanding.

The information in this article is of a general nature and does not take into consideration your personal objectives, financial situation or needs. Before acting on any of this information, you should consider whether it is appropriate for your personal circumstances and seek personal financial advice.