This week in investment matters:

Australia has enjoyed one of the greatest terms-of-trade booms in its history, yet public finances feel increasingly constrained and major states are accumulating large debts.

This week we explore, how the nation’s growth taxes increasingly flow to Canberra while the infrastructure, services and debt required to support that growth sit with the states. The result is a growing fiscal imbalance that helps explain everything from Victoria’s debt burden to Australia’s broader economic malaise.

Copyright 2026 First Samuel Limited

Read the previous Investment Matters here:

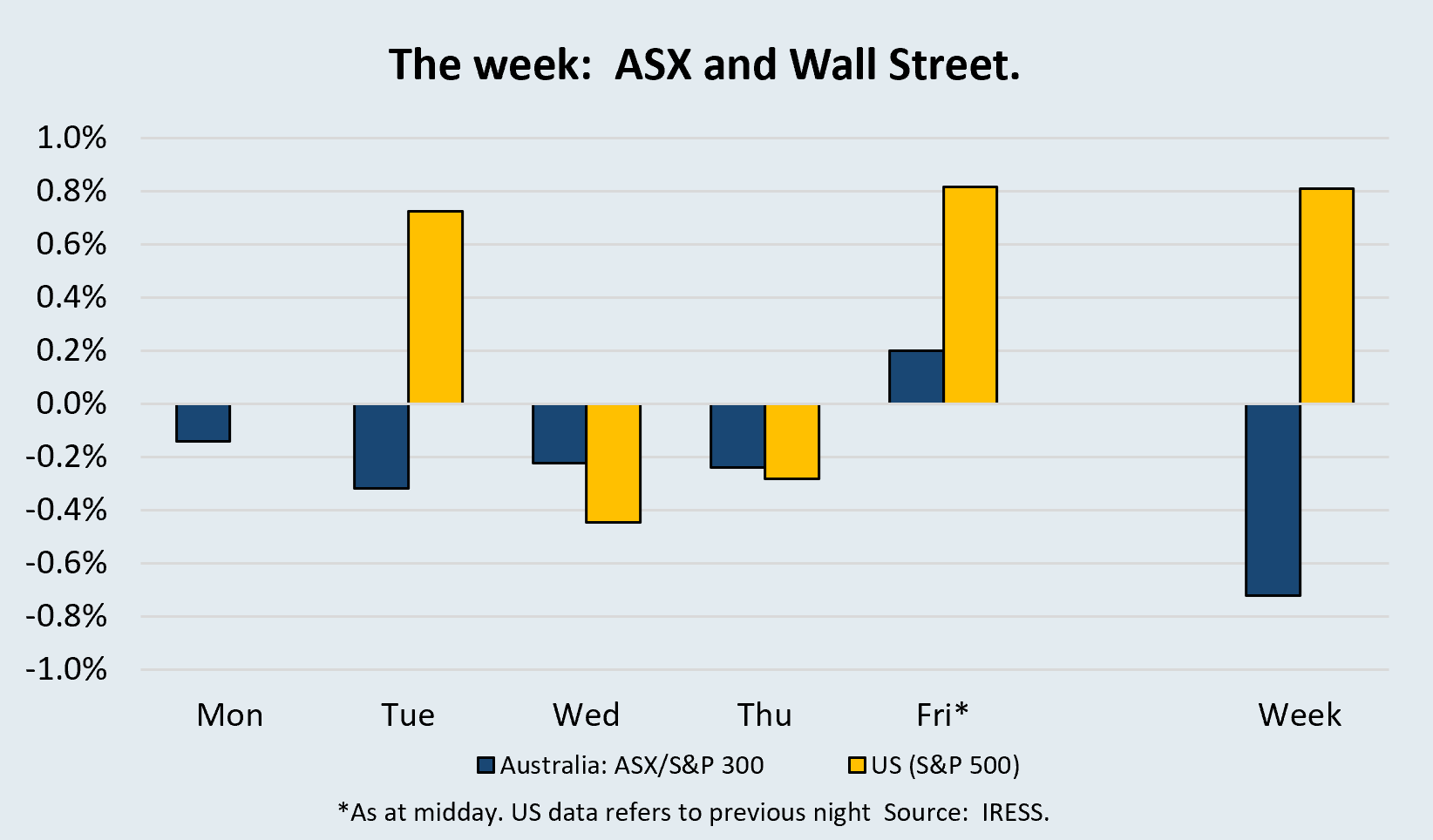

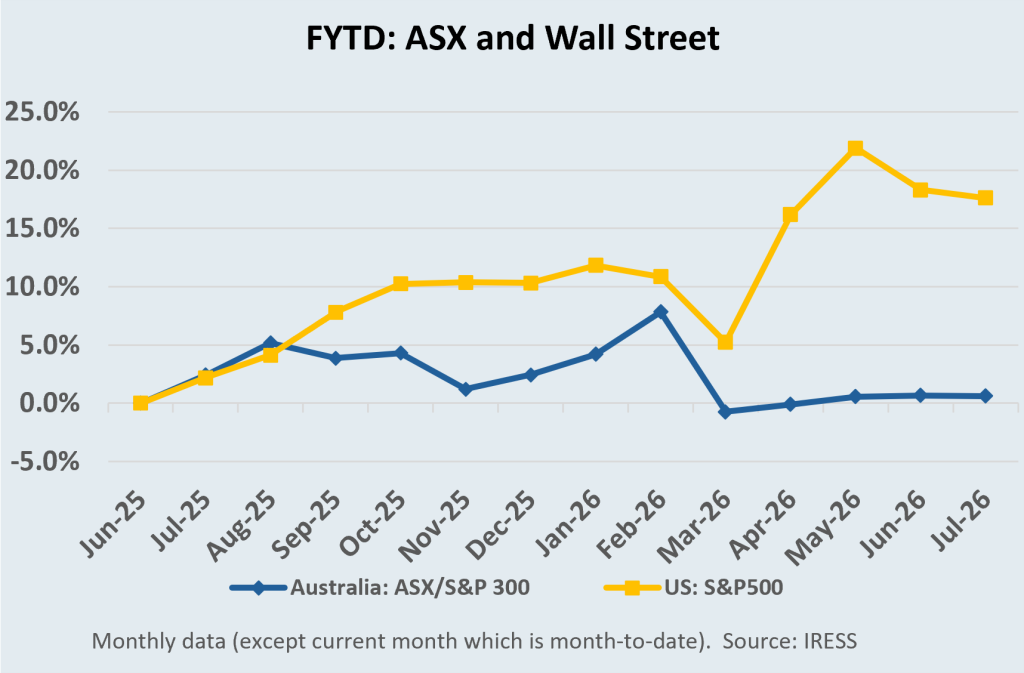

The market

Small changes, long shadows

This week marked 250 years since American independence. Its founding slogan — no taxation without representation — can sound distant from Australia. But the underlying issue is not distant at all. Taxation is always a settlement over property rights. The citizen gives up part of what is theirs because the state promises order, services, opportunity, defence and the public goods that make private property valuable in the first place.

Australia’s problem is not taxation without representation. It is taxation without alignment.

The federal government collects the taxes that grow with the modern economy. On the other hand, the state governments deliver many of the services, and almost all of the physical catch-up, required when that part of the economy grows. For a long time, that mismatch was hidden by good fortune.

Figure #1: Company profits

Source: ABS, RBA, Melbourne Institute, Minack Advisors

Company tax – federal

Company profits have risen materially as a share of GDP since the 1990s. Much of the change in Australia’s national income structure has been tied to the resources boom; the RBA has previously noted that the resources boom lifted mining company profits and increased the share of aggregate income going to non-financial companies. That matters because company tax is a Commonwealth tax. The physical location of the mine, the legal location of the taxpayer, and the population pressure created by national economic policy are not the same thing.

Income tax – federal

The same is true of personal income tax. In a progressive income tax system, bracket creep is not an accident. It is the design. Wages rise, nominal incomes rise, and the federal government receives more than proportionate revenue without ever needing to announce a tax increase. The Parliamentary Budget Office describes bracket creep as income growth causing individuals to pay higher average income tax rates each year, and projects personal income tax to make up nearly 54% of total tax receipts by 2032-33.

And despite the tax cuts of the 2000s, the income tax share of gross household income continues to rise. This income tax revenue is, of course, federal government revenue.

Figure #2: Income tax as a share of household income rises with brake creep in Australia rather than new taxes.

Source: ABS, Melbourne Institute

State taxes

The states, by contrast, are left with narrower, uglier taxes. Payroll tax grows with wages, but it taxes employment. Stamp duty increases when property changes hands, but it is volatile and discourages mobility. Land tax is economically preferable, loved by economists and newsletter writers, but politically problematic. Fines, feesand service charges can raise money, but they are not a modern growth tax. The only broad tax that naturally grows with nominal spending is the GST, which is collected by the federal government and distributed through a federal formula.

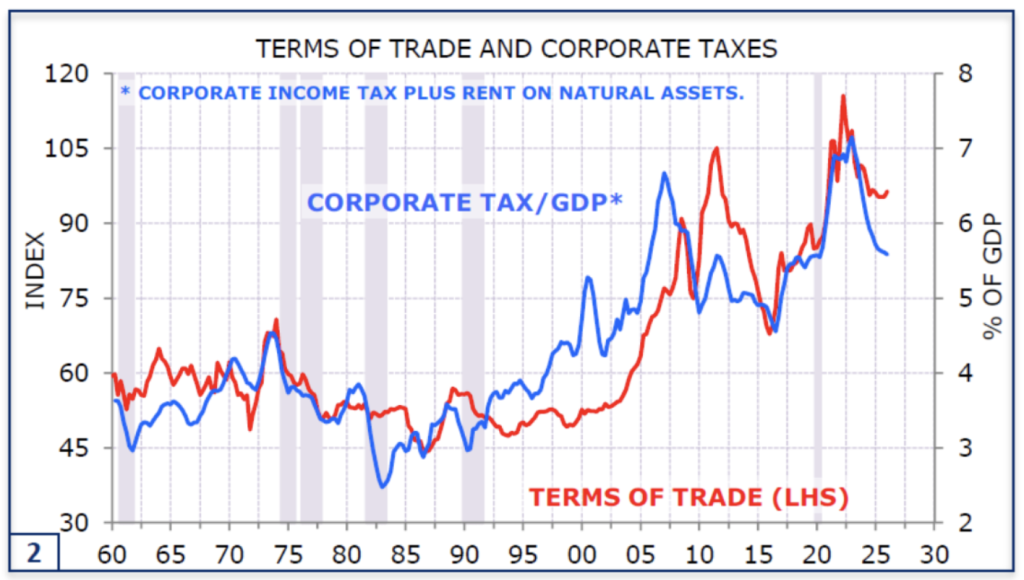

For two decades, that formula mattered less than it does now because Australia was rich enough to avoid hard choices. The terms of trade rose from a low of 47.5 in 1999 to a peak of 144.2 in 2022, and were still 117 in the March quarter of 2026.

Figure #3: Australia Terms of trade have improved, and corporate taxes as % of GDP have followed.

Source: ABS, Butlin, RBA, Melbourne Institute, Minack Advisors

That national income boom did a lot of work. It allowed lower effective tax rates for many households, expanded middle-class welfare, helped fund catch-up wages for teachers, nurses, and the public service, reduced federal deficits, held down interest rates, contained inflation for longer than would otherwise have been possible, and lifted asset prices. For almost two generations, prosperity without investment looked sustainable.

A pull-forward

It was not entirely sustainable. It was, in part, a pull-forward.

The generation that owned the assets received the compounding benefit of lower rates and higher prices. It also inherited infrastructure built by earlier generations: railways, ports, schools, hospitals, water systems and roads. In Victoria’s case, that inheritance reaches back to the 1890s. But the replacement cost was not paid as it accrued. The bill was deferred.

Then the population growth surge arrived, as it usually does, in the large eastern states. Until recently, much of the migration was pushed through two cities. In 2024, net overseas migration added around 107,000 people to New South Wales and 101,000 to Victoria. In 1996, the equivalent numbers were less than half for New South Wales and less than a quarter for Victoria; no wonder we didn’t build then.

Population growth drives housing construction, but it also requires trains, roads, hospitals, schools, police, water, parks, and power. Migration is largely a federal policy lever. The infrastructure consequences are state balance-sheet events.

Big Build

That is the prism through which Victoria’s Big Build should be judged. It is easy to mock the cost. Costs have been inflated by weak productivity, supply constraints, industrial relations issues, poor procurement, and poor policy. But the underlying need was real. Anyone who remembers the old Carrum station understands this intuitively: much of the Big Build is not decadence, but delayed replacement. The engineering geek in your author still loves a tunnel boring machine, a lifted bridge or a station rebuilt properly. The investor in your author asks why it took so long, and why the state doing the building is the one forced to carry so much of the debt.

Victoria’s own budget papers show the scale of the change. Government infrastructure investment is projected to be $21.4bn in 2025-26, before averaging $16.5bn across the budget and forward estimates.1 NSW is in the same world: its 2026-27 budget includes a $116.7bn infrastructure programme over four years, with more than $30bn expected in 2026-27 alone.

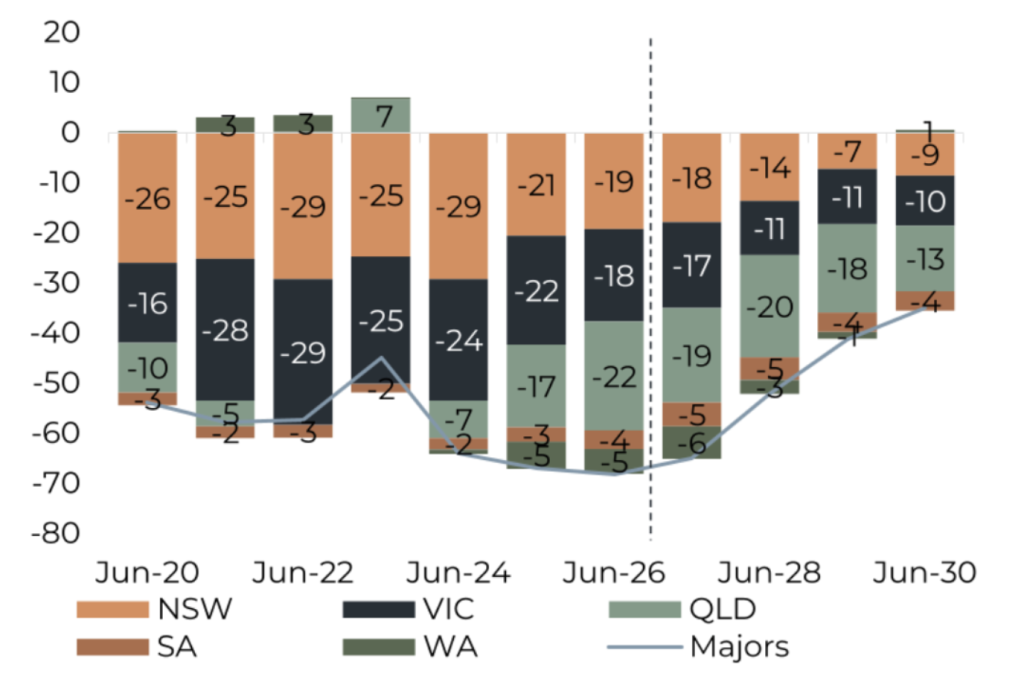

This leads to an almost permanent set of state deficits; only wishful thinking beyond FY28 would see the magnitude of the deficits fall.

Figure #4: Non–financial public sector fiscal balance, $bn by state including forecasts

Source: State Budget Papers, Barrenjoey Research

Victoria’s required catch-up

On our numbers, Victoria needed to spend around $26bn per annum for a decade simply to catch up on depreciation and the capital required to meet the demand of ten years of net overseas migration.

That number was before the huge rise in construction costs, before the productivity failures that fed inflation, before supply-side constraints, and before any serious attempt to build new industries, new technologies or productivity-enhancing growth. Victoria is now spending around $21 billion. In other words, Victoria is not overbuilding. It is still only just catching up. Most people who live here would struggle to believe the state is catching up on anything.

Four choices

If Victoria and NSW had to build but did not have access to the federal government’s growth taxes, they had only four choices: tax property harder, lift fees and charges, increase payroll tax, or borrow. The first is politically brutal. The second is regressive. The third is economically distorting. The fourth is inevitable.

That is ‘vertical fiscal imbalance’ in practice. This is why the GST distribution matters. Historically, ‘horizontal fiscal equalisation’ sought to give each state the capacity to provide a broadly comparable standard of services, taking into account their different revenue bases, including mining royalties, and their different costs of service provision.

Then came the 2018 GST changes. What looked like a technical change — floors, relativities, transition payments — became one of the most consequential fiscal decisions in modern Australia.

Western Australia

WA’s mineral royalties meant the original formula would have slashed its GST share. Treasurer Scott Morrison and WA Premier Mark McGowan struck a deal to introduce a floor instead. The Grants Commission now estimates WA will receive around $6.6bn more in 2026-27: $5.5bn in “no worse off” payments plus $1.1bn in pool top-ups. WA’s GST distribution hits $9.3bn, versus $26.1bn for NSW and $27.9bn for Victoria — but WA also pockets $11bn in mining royalties on top.

This is a permanent change in how the federation treats mining income, population pressure and fiscal need. Saul Eslake’s critique is hard to improve on: “heads Western Australia wins, tails the other states and territories lose.” He’s called it possibly the worst Australian public policy decision of the century so far.

The galling part is the need. WA has fiscal room and a stronger budget position — enough to fund electricity subsidies and outspend its own infrastructure requirements: $6.5bn in needed capex against $12bn+ invested. Victoria, by contrast, needs $26bn in capex and manages $21bn.

A simple citizen’s ledger sharpens this: state services delivered, minus your contribution, plus capex, plus subsidies, minus GST returned and payroll tax paid. In WA, that nets to roughly $4,500 per capita in the citizens’ favour. In Victoria, roughly zero — and once you add land tax, stamp duty and other state charges, Victoria falls about $4,000 behind while WA stays $1,000 ahead.

These numbers are deliberately simple — they don’t fully allocate Commonwealth grants — but that’s the point. Debt and GST inequity aren’t abstractions; they shape services, investment and growth. Investing in WA increasingly means investing in a state with money to spare. Investing in Victoria means investing in a state still catching up. Politics tends to collapse into arguments about wages and competence when the real questions are who pays for national underinvestment, who pays for population growth, and who benefits from minerals that took millions of years to form.

Tax design compounds. A CGT discount here, a GST floor there, bracket creep left untouched, state taxes unreformed, migration concentrated through two cities, infrastructure deferred for a generation – none of these looks decisive in isolation. Together, they explain why the public finances now feel tight despite Australia enjoying one of the great terms-of-trade booms in its history.

Generational difference

The federal government has no broad wealth tax. It has limited means of capturing asset-price uplift, except when value is converted into taxable income, often through discounted capital gains. Yet the uplift in asset prices was one of the largest transfers of wealth in modern Australian history. One generation received higher asset prices, lower rates, lower effective taxes and the infrastructure built by earlier generations. The next generation received higher house prices, higher rents, weaker productivity, larger public debts and a very large build program that could no longer be delayed.

This is the time transfer. It was not explained properly. There was no smoothing mechanism. There was no honest accounting for the fact that a country enjoying a mining boom, lower rates and rising asset prices was also consuming part of the money that would eventually be needed for capex.

Eventually, the Commonwealth also needs the money. Defence is no longer optional. The NDIS is no longer small. Electricity infrastructure has to be rebuilt. AI, data centres, new materials, new energy systems and the next layer of industrial capability all require public coordination and private investment.

And what happens if property taxes and payroll taxes are now both under threat, while the build is still needed and Victoria is already paying roughly $9bn a year in interest to fund a catch-up that benefits the entire nation?

Impact on markets

How do these issues drive weaker ASX market performance? Well, surprisingly to some, not these factors by themselves, but rather the sense that none of these factors will change. While current conditions affect earnings and profitability today, share prices are more about expectations for the future. Stock markets, in general,and investors like your author care much more about change and the pace of change rather than the starting point.

Malaise is a function of the view that substantive change is not likely.

Moves to reform GST, extend a federal tax system beyond bracket creep, and a reform agenda that builds upon the view that intergenerational equity can be solved through productivity growth are good places to start.

All these issues would increase long-run growth assumptions and lift share prices, often before such measures are delivered. Weak share price growth reflects the view that reform is unlikely.

So, issues regarding future economic conditions may appear merely contingent, but they are, in fact, highly relevant to investment decisions made today.

Taxation without representation caused a revolution. Taxation without alignment causes something slower but still dangerous: underinvestment, resentment and decline by increments.

The numbers look small at first. Over decades, they have become the country. Just like the Ship of Theseus is the classic philosophical thought experiment, is it still the same country?

The information in this article is of a general nature and does not take into consideration your personal objectives, financial situation or needs. Before acting on any of this information, you should consider whether it is appropriate for your personal circumstances and seek personal financial advice.