Copyright 2026 First Samuel Limited

Read the previous Investment Matters here:

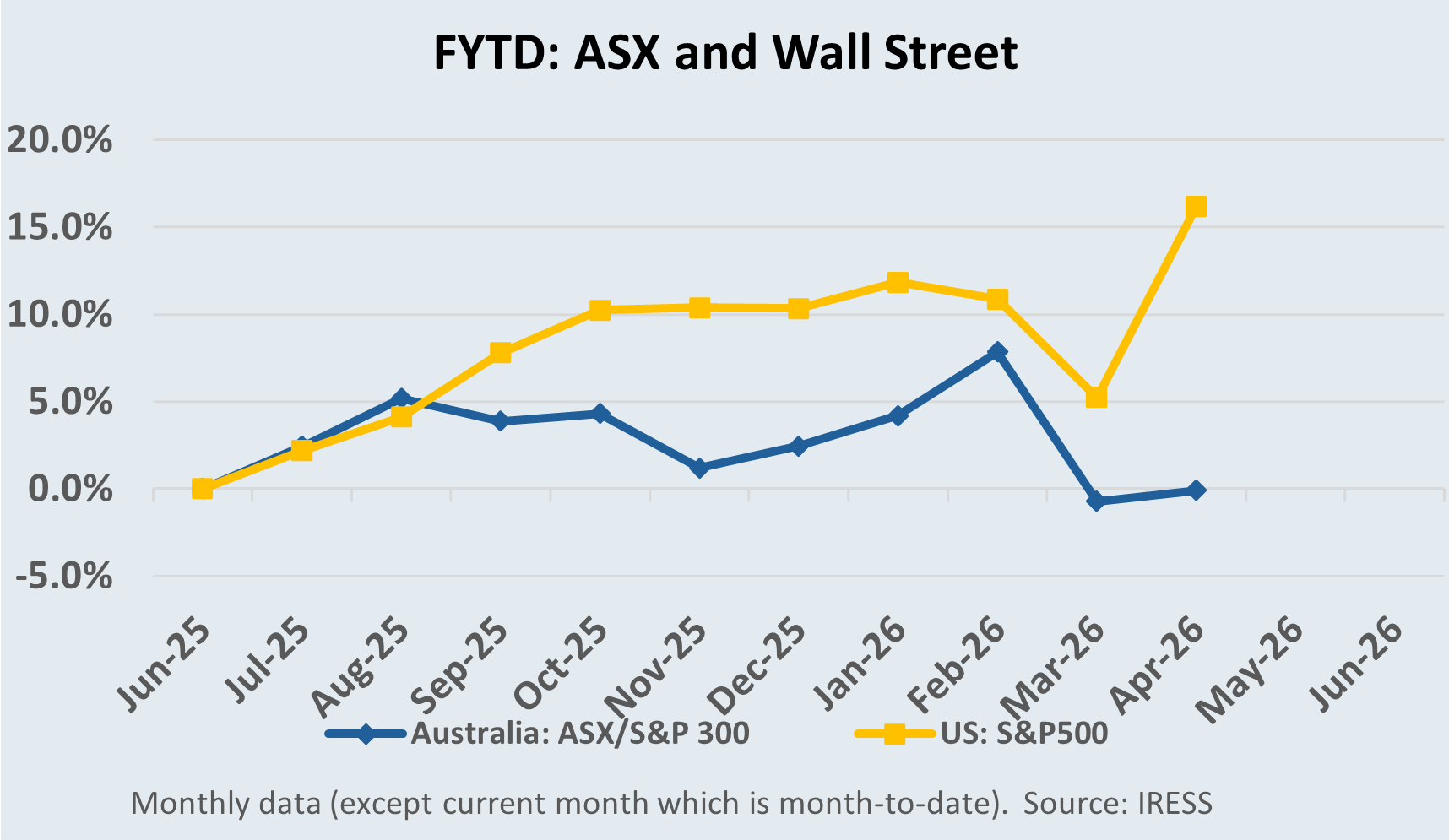

Inflation spike

In this week’s Investment Matters we won’t discuss the spike in the inflation rate. There has already been more commentary than can be sensibly digested.

The critical matter is what next? And the what next is the meeting of the RBA Monetary Policy Board on Tuesday. And the decision it makes about interest rates.

It is better to be armed with that outcome than the inflation outcome. So, please wait for next Friday’s Investment Matters for inflation and interest rate musings.

Strategic mineral investment

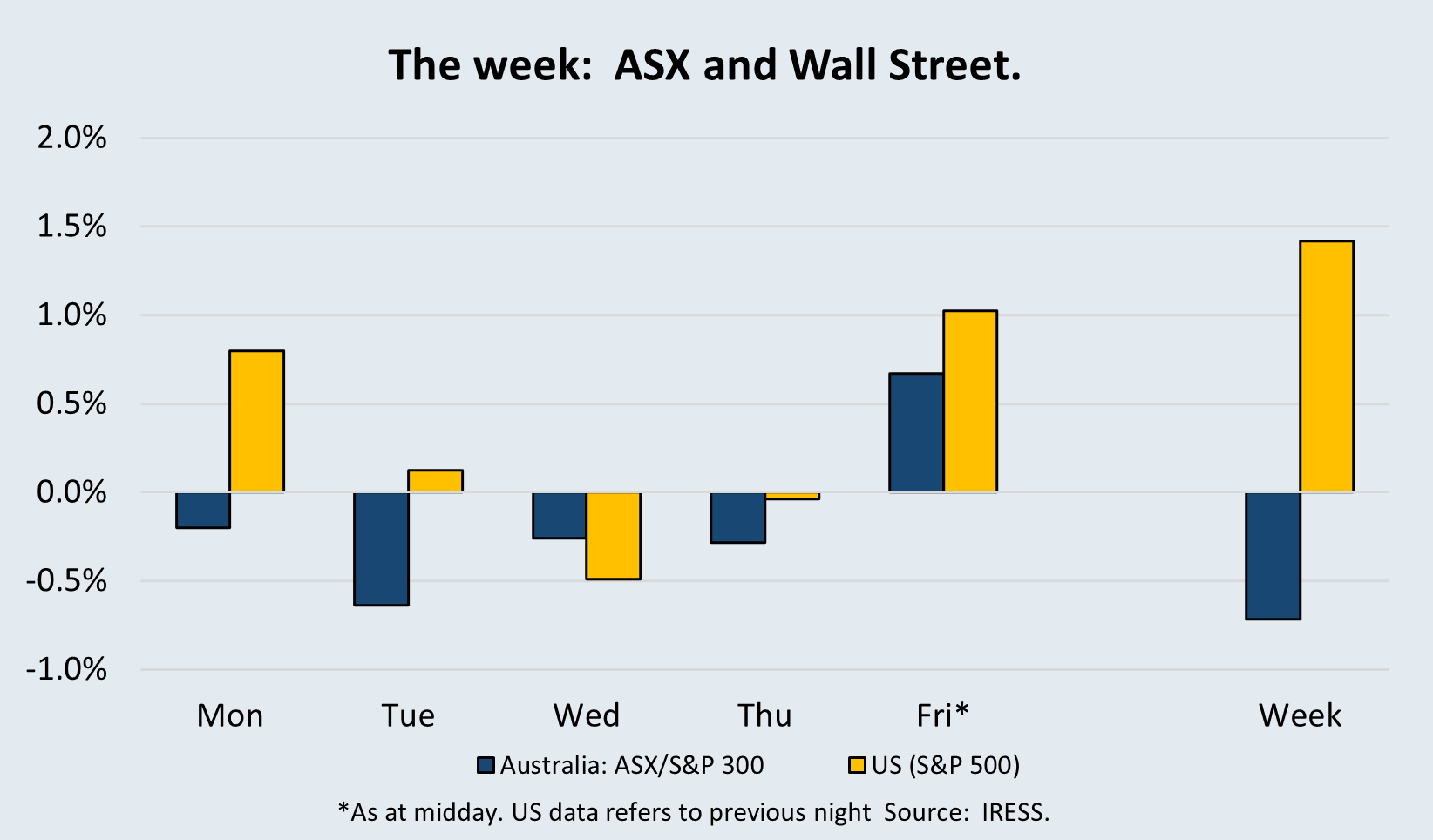

In this week’s Investment Matters… a hiatus follows the quiet of Anzac Day, with only an occasional company “confession” of downgraded expectations or a problematic quarterly update. But lying in wait is the Macquarie Group Australian Equities Research conference in Sydney at the beginning of May.

One of those yearly migrations of people that others are thankful to avoid, the funds management community gathers in Sydney to hear from a myriad of companies, engage in small-group and 1:1 meetings with management, and soak in wall-to-wall discussions of interest on a range of local, global, technological, and occasionally social topics. The Macquarie Conference, as it is affectionately called, is also the time when companies will update the market on current operating conditions.

While every year these updates feel more important than the last, timing on this occasion is critical. The Iran War began after the reporting season in February, and there has been a dearth of new data on customers and activity since. Hence, we eagerly await early May, and we note that Investment Matters will cover the highlights of the conference both next Friday and the following week.

This week, we have chosen to provide a deep dive into WA1 Resources. It is a small position that we anticipate growing, and one we are looking to hold over the medium term. It is topical from the perspective of catching up with MD Paul Savich in Melbourne last week, and a series of expert calls we have been engaging in over the past couple of months.

The Market

WA1 Resources: A Small Position in a Strategic Metal

CORE THESIS

We now own a small position in WA1 Resources because the company controls a large, high-quality Australian niobium asset in a concentrated market where customers may increasingly value credible alternative supply. Niobium is considered a critical mineral, and this position is an important addition to our future metals basket of portfolio positions.

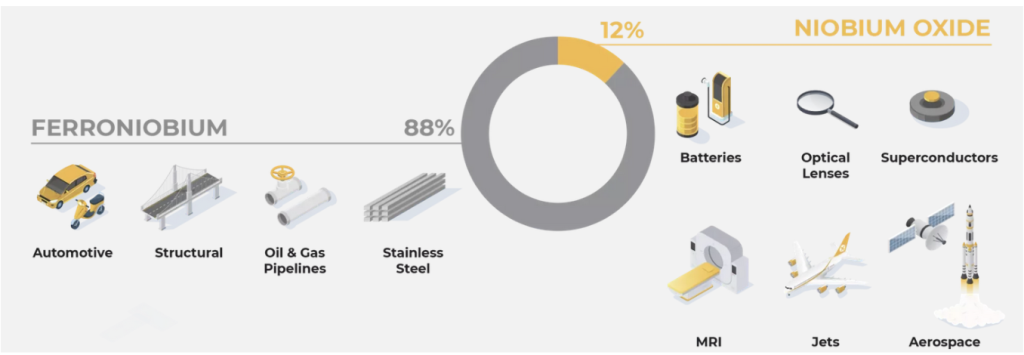

Figure #1: Niobium today is mainly a ferroniobium and steel story, but future uses in batteries, optical lenses, superconductors, MRI, jet engines and aerospace could broaden the demand base.

Source: WA1 Company Presentations

Why we own WA1

We have recently taken a small position in WA1 Resources. The position is deliberately small. WA1 is still a development-stage company; its Luni Niobium project will require more capital, more technical work and a great deal of infrastructure before it can become a mine.

But the asset (on paper, given drilling) appears unusually good, and the market it sits in is unusually concentrated. That combination is enough to make WA1 worth owning. The WA1 share price is at a considerable discount to our current valuation.

The thesis is not that niobium is the next hyped mineral, like lithium was once. Niobium hype is gone, with three-plus years passing since WA1 Resources first announced the Luni niobium discovery in Western Australia’s remote West Arunta region. WA1 now has cash on its balance sheet and is working towards mine development through the long process of planning and securing both funding and offtake agreements.

Critically, niobium is already useful, and future applications may broaden demand for this specialty mineral. WA1 will control a large Australian deposit in a market where credible alternative supply could become strategically valuable. We see significant upside if Luni is developed, partnered, or acquired at an appropriate strategic value. We also recognise the risks: the project must be built, funded, connected to infrastructure and qualified with customers.

Our experience with Lynas Corporation (LYC) is relevant. Lynas was not valuable simply because rare earths were interesting. It became valuable because it represented an alternative non-Chinese source of supply in a market where customers and governments increasingly cared about concentration risk. WA1 is not Lynas, and niobium is not a rare earth. But the portfolio lesson is useful: in strategic materials, the value of credible alternative supply can be much higher than it first appears.

The question we are trying to answer is therefore simple: if niobium already has a real industrial role, and future uses may broaden demand, how valuable is a large new Australian source of supply?

What niobium does

Niobium is not a household metal. It does not have the visibility of copper, iron ore, lithium or uranium. Its importance comes from the opposite feature: it is usually used in very small quantities, but those small quantities can materially improve the performance of much larger systems.

In steel, niobium can increase strength, reduce weight, improve durability and enhance corrosion resistance. That makes it valuable in automotive steel, bridges, buildings, rebar, pipelines and other infrastructure. The phrase that best captures the current market is this: in many applications, the only replacement for steel is better steel.

Tiny market

The entire global niobium market is highly concentrated, with annual production of ferroniobium (the primary product) currently sitting at roughly 100,000 to 125,000 tonnes. But the price per tonne is high, at USD30,000 to USD50,000.

Niobium’s current market is anchored in ferroniobium, which is used in steelmaking. That gives the metal an established industrial demand base. It is not a speculative material searching for a use. It already does a job. The more interesting feature is that the job may expand.

Beyond ferroniobium, niobium oxide and other niobium-based products are being explored or used in batteries, optics, superconductors, medical equipment, jet engines, aerospace and defence applications. This is what makes niobium unusual. It combines an established base with future optionality. The steel market gives it credibility. The emerging uses give it upside.

Future uses: more upside than we first appreciated

One of the more important outcomes of our work on WA1 has been a greater appreciation for the range of possible future uses for niobium.

We started with the conventional understanding: niobium improves steel. That remains the core market and should not be dismissed. But the more work we have done, the more interesting the future use case has become. Batteries are the most obvious example. Niobium oxides are being tested for applications where faster charging, safety and cycle life matter. This may be particularly relevant in heavy-duty uses where charging speed and battery durability are more important than simply maximising energy density.

Aerospace and jet engines are also important. These are harsh operating environments. Materials must withstand heat, stress, fatigue, and corrosion. In those settings, small improvements in material performance can be worth a great deal. Niobium-bearing alloys and niobium-containing materials can therefore matter in applications where failure is not merely expensive, but unacceptable.

Superconductors and MRI machines provide another example. Niobium-based superconductors, primarily niobium-titanium and niobium-tin are the most widely used industrial superconducting materials, accounting for roughly 95% of the market. This is not mass-market demand as with steel, but it reinforces the broader point: niobium keeps appearing in mission-critical applications where performance matters more than volume. Optical lenses, medical devices, defence systems and advanced manufacturing all point in the same direction.

The bullish case is not that any one of these uses becomes enormous overnight. The more realistic case is that the list of uses keeps expanding. In a small, concentrated market, that can still be powerful.

CBMM and the customer architecture of niobium

Any serious discussion of niobium has to start with CBMM (Companhia Brasileira de Metalurgia e Mineração or The Brazilian Metals and Minerals Company). It is not just the dominant producer. It is the company that helped build the market.

CBMM’s Araxá operation in Brazil has shaped the modern niobium industry. CBMM describes itself as having more than 70 years of history, beginning in Araxá in 1955, and says it now serves more than 500 customers in more than 50 countries. It also emphasises technology, customer relationships and reliable global supply rather than simply mining and selling product.

That matters because niobium is not traded like iron ore. It is a specialist industrial material sold into processes where consistency, reliability and technical support matter. Customers need to know the product works. They need confidence in supply.

This creates a barrier to entry for WA1 but also provides a roadmap. If Luni is developed, WA1 is unlikely to succeed by simply producing tonnes and pushing them into the market. It will need customers. It may need strategic partners or government backing for critical mineral investment.

CBMM’s role should not be underestimated. It has been extraordinarily important in building demand, educating customers and supporting applications. But there is a distinction between CBMM’s role in market development and the underlying value of niobium itself. Customers do not use niobium merely because CBMM sells it. They use niobium because it works. The science and performance benefits matter independently of the incumbent supplier. A good deal of our research agenda has focused on what CBMM would do in the face of a new competitor.

Figure #2: CBMM Brazil – the mine and its strategic partners. CBMM’s Araxá complex and strategic shareholder architecture illustrate how deeply customer relationships are embedded in the niobium market.

The three-player supply structure

The current niobium supply structure is unusually concentrated. USGS (United States Geological Survey), the definitive source of global mineral supply information, estimates that Brazil accounted for approximately 93% of global niobium production in 2025, followed by Canada with 5%. That is an extraordinary level of concentration for a material used across steel, infrastructure, aerospace, energy and medical applications.

For the purposes of WA1, there are three incumbent producers that matter: CBMM, CMOC and Niobec.

- CBMM is the dominant supplier and market architect. It is the benchmark against which every new niobium project must be judged.

- CMOC is the second major Brazilian producer. It matters because it shows that supply outside CBMM has been accommodated. CMOC describes its Brazilian business as the world’s second-largest niobium producer, with ferro-niobium as its main niobium product, and reported record niobium production of 10,348 tonnes in 2025.

- Niobec is based in Quebec, has been in production since 1976 and is the only one located outside Brazil. It is vertically integrated and sells ferroniobium directly to steel producers worldwide.

But CMOC is only partial diversification. It is still a Brazil-based supply, and it is now Chinese-owned. That does not make it a poor supplier, but it does mean it does not fully address the diversification question for customers or governments seeking additional jurisdictional redundancy.

Niobec is the key proof point for non-Brazilian supply. Niobec matters because it shows that a non-Brazilian source of niobium can work. In the North American market, that is strategically valuable. WA1 could potentially play a similar role for Asia: a credible regional source of niobium from a stable mining jurisdiction.

That is the central supply-side opportunity. The niobium market is not fragile because demand is enormous. It is fragile because the supply is narrow.

New supply can be accommodated — if introduced carefully

One of the natural concerns with WA1 is whether a small market can absorb another meaningful source of supply. That is the right question. A large new deposit is only valuable if the market can take the product at attractive economics.

The history of niobium suggests a market that can absorb new supply but prefers to do so carefully.

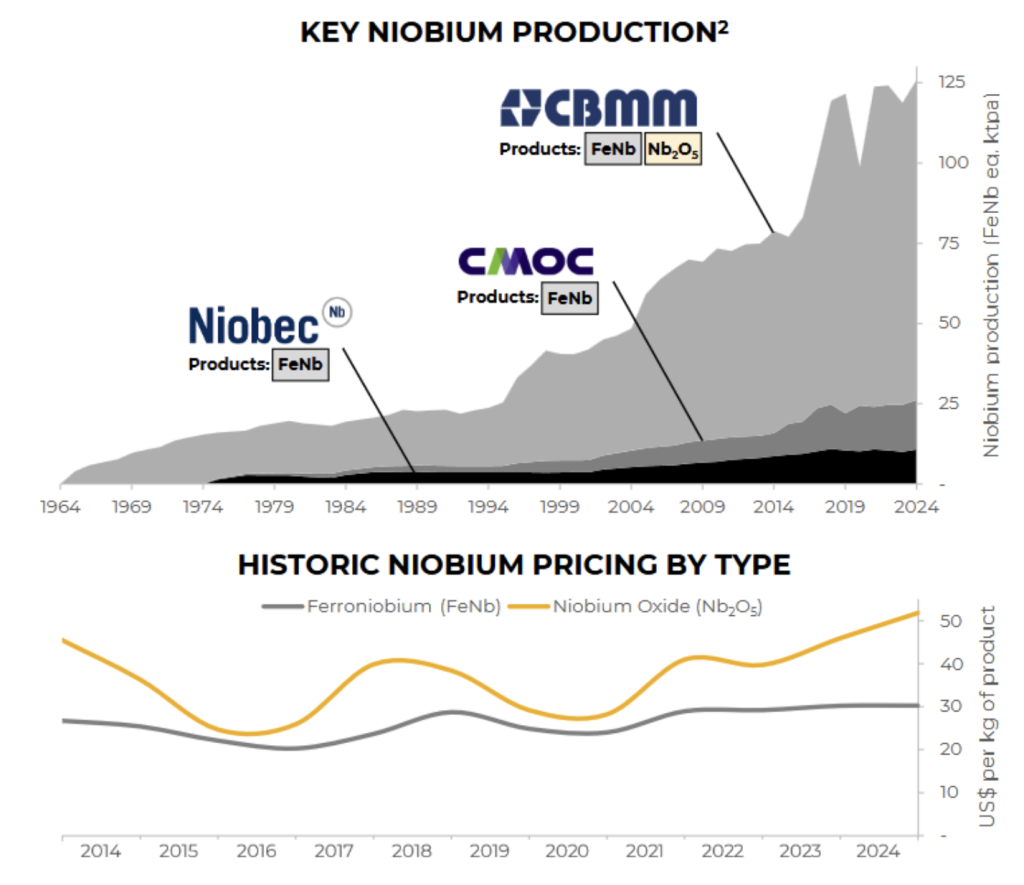

The long-term chart provided by WA1 Resources is particularly informative. Niobium supply has expanded over time with the emergence of Niobec and CMOC, while pricing (below) has remained relatively stable. The history suggests a market that can accommodate new supply, but does so through discipline, customer relationships and technical qualification rather than uncontrolled spot-market competition.

Figure #3: Niobium market history

Niobec entered the market and endured. CMOC became a meaningful second Brazilian producer. The market has grown over time rather than collapsing under the weight of additional production. At the same time, niobium pricing has historically been more stable than that of many other specialty or critical minerals.

That does not prove that future supply will be absorbed painlessly, but it does suggest that niobium has functioned more as a disciplined industrial market than a speculative commodity market.

This is important for WA1. The lesson is not that WA1 can simply produce tonnes and force them into the market. The lesson is that credible supply can be absorbed when it has a clear customer role. In our view, that role is likely to be diversification, reliability and regional supply security.

RESEARCH TAKEAWAY

The lesson is not that WA1 can simply dump tonnes into the market. The lesson is that credible new supply may be absorbed when it is developed with customers and has a clear strategic role.

What we have tested with industry experts

As part of our usual research process, we have made a series of calls with global niobium industry specialists and people close to the market. The purpose was not to confirm a preconceived view. It was to test how a small, concentrated and relationship-driven market might respond to a credible new source of supply.

Those conversations reinforced several points. First, CBMM’s role in the industry is extraordinarily important and should not be underestimated. Second, customers value reliability, technical support and product consistency. Third, there is increasing appreciation for diversification. Fourth, the range of future uses may be broader than we initially appreciated.

The conclusion was not that a new supply is easy. It was that credible new supply, developed with customers rather than pushed at them, may have a place.

Location: remote, but not necessarily stranded

Australia has a recurring resource challenge. We are very good at finding important minerals far from existing infrastructure. That has been true in iron ore, LNG, uranium, rare earths and many battery materials. The orebody is only the first half of the story. The second half is roads, power, water, workforce, processing, logistics and customer delivery.

Luni fits that pattern. The project is remote, located in the West Arunta region of Western Australia near the Northern Territory border. WA1’s project page describes the West Arunta Project as approximately 490 kilometres south of Halls Creek.

Figure #4: Luni is remote, but not necessarily stranded. The project sits between north-west Australian mining/export infrastructure and central Australian transport corridors.

The location map is useful because it makes the point visually. To the west sits the broader north-west Australian mining and export system, including the long-distance route toward Port Hedland. To the east and south are Alice Springs and central Australian transport corridors. To the north are routes toward Darwin and the north-west.

This is one reason a larger mining company could eventually be interested. The Pilbara and broader north-west Australian miners understand remote infrastructure, logistics, approvals and large-scale project delivery better than almost anyone. If Luni is as good as it appears, it is not hard to imagine larger companies asking whether they could develop it faster, cheaper or more reliably than a standalone junior.

That creates both opportunity and risk. A takeover premium would not necessarily be a bad outcome. But one risk is that the asset is acquired before public shareholders receive anything like full strategic value.

Luni: big enough and good enough to matter

We do not need to overcomplicate the geology. The appeal of Luni is that it appears large, high-grade and potentially developable in a market where very few new projects can credibly matter. Experts we spoke to were universally “impressed with the rocks” but all know that rocks alone don’t make a profitable project.

WA1 reports a Luni Mineral Resource Estimate of 220 million tonnes at 1.0% Nb2O5, a third of which is very high-grade (1.38% Nb2O5), and an Indicated Resource (the 2nd-highest level of confidence). Further drilling will help create a mine plan, a Measured Resource and a Feasibility study through 2028.

WA1 also notes that drilling has shown a shallow blanket of high-grade niobium mineralisation over a significant extent, and says grades compare favourably with the resource grade of the world’s operating niobium mines.

WA1’s says initial flotation work produced a high-grade niobium concentrate with low impurities and recovery rates comparable with industry experience. It also notes that further workstreams are underway across water, environment, power, transport and niobium marketing.

These are encouraging signs, but they are not the same as a mine. A resource estimate tells us there is niobium in the ground. The investment case requires proof that WA1 can turn that resource into a reliable industrial product at attractive economics.

The remaining questions are practical. Can the metallurgy be repeated across the orebody? What product should WA1 produce: concentrate, niobium oxide, ferroniobium or some staged pathway? What infrastructure is required? How much capital will be needed? Which customers will qualify the product? What partners might be required? How will the project be funded without excessive dilution?

Critical mineral status helps, but it is not the thesis

Niobium’s critical mineral status is useful, but it is not the reason we own WA1. Government recognition can help with attention, financing pathways, strategic engagement and customer interest. It may also matter in a world where governments are increasingly focused on secure supply chains for advanced manufacturing, defence, energy and infrastructure.

But critical-mineral status does not make a mine economically viable. It does not solve metallurgy. It does not build roads, generate power, find water, qualify customers or fund capex. The case for WA1 is more grounded: niobium has real uses, supply is narrow, customers may value diversification, and Luni may be good enough to become a credible Australian source.

Why WA1 may need partners — and why that could be good

The most likely successful pathway for WA1 may not be acting alone forever. Niobium is a relationship-driven market, and Luni is a large remote development project. Both factors point toward partnerships.

Those partners could be customers seeking long-term supply security. They could be trading houses or industrial groups that understand product qualification and distribution. They could be larger mining companies with infrastructure and project delivery capabilities. They could even be strategic investors that want exposure to a non-Brazilian niobium supply chain.

In a market like the niobium market, the right partner may increase the value of the project. We see natural partnerships being required in developing the niobium oxide production facilities, which are unlikely to be built in Australia. Partnerships could dramatically reduce financing risk, accelerate customer qualification and make the development pathway more credible.

WHAT WE NEED TO SEE NEXT

Resource conversion, repeated metallurgy, product strategy, infrastructure pathway, customer qualification, funding discipline and evidence that strategic customers value diversified non-Brazilian supply.

Why is the position small, and why do we own it

We see significant upside to the current WA1 share price if Luni becomes a recognised strategic niobium asset. The market is concentrated, the metal is useful, future applications look broader than we first appreciated, and customers may increasingly value an Australian source of supply.

But the position should remain small because the project is not yet a mine. The medium-term risks are about getting it built, metallurgy, infrastructure, approvals, capex, funding and customer qualification. The longer-term risk is how the market responds to new supply, including the roles of CBMM and the existing producers.

That is the balance. WA1 deserves a place in the portfolio because the asset is unusual and the upside could be significant. It deserves to be a small place because development risk is real, and the path to value will take time. Our conclusion is reserved but constructive. WA1 is a small position in a potentially strategic Australian asset.

The information in this article is of a general nature and does not take into consideration your personal objectives, financial situation or needs. Before acting on any of this information, you should consider whether it is appropriate for your personal circumstances and seek personal financial advice.