Read the previous week’s Investment matters.

Photo © vladimirsukhachev from Via Canva.com

Copyright 2025 First Samuel Limited

The Market

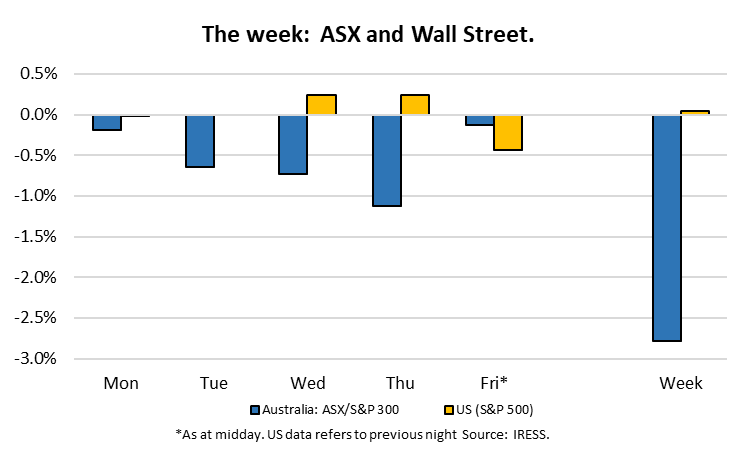

Week two

The semi-annual company reporting period reached its peak this week, with a large number of companies in which clients are invested coming to the market with their latest results. It was a successful week for clients.

Later editions of Investment Matters will provide a review of key stocks that have been reported. The reviews are designed to provide context covering:

- How the financial and operating update could change our view of the company, especially our outlook for future growth;

- Exploring the new options and overlooked value that the result provides clarification or insight into; and

- The market’s reaction to the result, our overall impression, and the share price change.

In addition, we will include a table (below) of all of the portfolio companies reporting and brief notes on each.

This week’s Investment Matters discussion will concentrate on three large holdings: Reliance Worldwide, Seek Limited and BlueScope Steel. We will return to provide more detail on remaining core equities positions post reporting season.

BlueScope Steel (BSL): Earnings tailwinds and long-term target impress market

Early in the week, BlueScope Steel, a name synonymous with Australian steelmaking and the ColorBond brand, reported improving results, highlighting ongoing business improvement and a progressive medium-term plan for earnings.

By the end of the week, BlueScope had rallied by 9.8% post-result and is up 31.5% in calendar 2025.

Clients will recall that the Australian heritage in steel is no longer the main asset of this company, which is valued at around $11 billion. This week’s chart below from the company presentations highlights the increasingly US-centric focus on earnings and sales volumes. In addition to a relatively high 42% of 1H earnings attributable to North America, the value of the underlying assets is even more heavily skewed to the US and the company’s main plant, North Star in Ohio.

The charts below show the increasing share of North American steelmaking since 2016, when BlueScope acquired complete control of North Star and began working on capacity enhancements and debottlenecking.

Another relevant point in the chart is the significant focus on value-added products globally, with similar volume contributions to rolled and coated steel products in North America, Australia, and Asia.

BlueScope Earnings and Volume Diversification

Source: BSL Company reports

1H25 Results

BlueScope experienced challenging market conditions in 1H25, leading to a significant reduction in earnings. Conditions are challenging with respect to the margin that the business makes producing and selling its steel products, not the underlying level of demand. As a price taker on raw materials as input costs and having an enormous, fixed cost base in running plants, the final price for manufactured steel, or more specifically, the final steel spread, the difference between the price of steel and the average cost of producing it is key.

Steel spreads in the US and worldwide were depressed in the first half of FY25, but we have seen improvements in spreads in recent months. The impact of weak steel spreads can be seen in the following figures for the key North American assets. Despatches refer to the quantity of steel produced, North Star is the plant in Ohio, and BCPNA is the total of all the BlueScope Coated Products.

BlueScope North American earnings: The impact of steel spreads

Source: BSL Company reports

We can see in the charts above that despite increasing production at North Star, the combination of moderating end-use demand for BCPNA products and lower steel spread reduced half-year earnings considerably (EBIT from $417m to $182m over 12 months).

The key to valuing a company such as BlueScope isn’t to hope the cycle in pricing will disappear; it won’t, but rather to assess how much money the operations are likely to make through the cycle.

One of the valuable parts of this company update was a firm clarification of the board and management teams’ expectations for such earnings after the completion of its capex program and the assumption of mid-cycle market conditions.

Their target EBIT range of $1.9-2.4bn was considerably higher than expectations, with the top end above our upside scenarios. Assuming the teams’ growth plans can be 100% realised would be folly. Still, the framework provides an execution target and an essential context for suitors looking to acquire BlueScope’s attractive assets.

Tweaks to strategic plans appear sensible.

Additional new information regarding the company’s FY30 framework included more concrete plans for realising value from its sizeable, underutilised property portfolio, circa $2 per share, and some variations in their plans for mid-stream growth.

The business can invest to improve the total asset value through a range of mid-stream acquisitions. In the steel industry, upstream refers to the supply of raw materials through the steel-making processes, including blast and electric arc furnaces. Midstream steel processes upstream raw materials into materials that can be further processed downstream. Examples include cold and hot rolled steel sheets and plates, reinforced steel coils, and other types of steel. Downstream examples would be the car plants and washing machine factories using rolled steel sheets in their products.

The growth of ColorBond globally, and especially in North America, is an example of mid-stream success. Uncertainty regarding the Trump impact on other assets they could acquire and/or growth options they could invest in has increased. As such, they are a little more cautious than we expected a year ago.

We don’t believe this necessarily reduces the value of the business; however, rising steal spreads and improving cash flow and balance sheet positions may indeed delay decisions even 1-2 years, ultimately making them more valuable post-Trump than they could be today.

Impact on valuation

We acquired a stake in BlueScope in clients’ Australian shares sub-portfolios at a significant discount to our view of the underlying asset value (circa 40 per cent discount). Factors leading to the discount included short-term weakness in steel margins and some uncertainty regarding the timelines for future cash flows to equity (after investment).

Regular readers will note that we had anticipated that having at least a portion of the portfolio that would benefit from increasing geopolitical polarisation and a Trump victory would be advisable. BlueScope is well-placed and still reasonably priced for any Trump-related upside.

We anticipated the capacity to deliver earnings of a quantum that easily surpassed market expectations and justified a share price materially higher than our acquisition price. FY25 earnings guidance and the accompanying medium-term commentary have provided a more explicit focus on the size of the future cash flows.

In addition, the upswing in cyclical conditions provided more reassurance regarding cash flows in the interim.

On average, the sell-side analyst community, on the back of this one result, raised their price targets by more than 15 percent – and they now approach our long-run valuation. We have raised our long-term valuation by a smaller amount. BlueScope remains an attractive portfolio holding in an era of global uncertainty.

Reliance Worldwide (RWC): 1H25 Results – Controlling the controllables

Among the largest and best-performing positions in client’s Australian shares sub-portfolios since 2020, Reliance Worldwide is a significant figure in the North American, UK and Australian plumbing markets. It predominantly services residential repair markets rather than purely new-build markets.

Reliance’s sales are from the Americas (60%), with a further 30% from EMEA (Europe/Middle East) and the remainder from the Asia Pacific. Significant levels of manufacturing are completed in the US, although components are sourced from around the world.

The impact of Trump is mixed; the promotion of manufacturing in America has been a core business strategy which is supported by Trump policies, but RWC also imports a range of products and inputs from China, as do most of its competitors. The business retains significant pricing power, as demonstrated through the recent period of global inflation, and we would suspect that any tariff-related cost increases would be quickly passed through.

From its unlisted early days in Australia to today, the business has grown through brand development (including SharkBite) and incremental acquisitions (M&A). Part of the company’s strength is its capacity to continue acquiring in a fragmented industry. Sales growth has been accompanied by increasing margins, as shown in the figure below.

Reliance Worldwide (RWC): Track record of growth, including from M&A

Source: Company reports

1H25 Results

Excluding acquisitions, RWC has seen weak sales growth in 1H25 as global housing market conditions have remained subdued. This is especially the case in its smaller markets of EMEA and Australia. Despite this top-line weakness, we were impressed by the ongoing margin expansion and unwavering commitment to business improvement.

The net result was slightly lower than expected sales revenue but higher than expected earnings. The company’s natural conservatism noted that headwinds to revenue growth in the 2nd half are likely to remain.

Its Holman Industries acquisition in February 2024 appears to have successfully achieved target cost out and revenue goals. The company retains enough balance sheet capacity for further short to medium-term acquisitions.

Market reaction to the results

The stock price fell by almost 4% on the day. The market reduced its expectations for the full-year results by a small amount. Markets, especially during reporting season, are very short-term focussed. We believe such circumstances provide opportunities to build long-term positions in great companies. The short-term concerns related to whether sales growth would be strong enough in the 2H25 to meet updated expectations.

End markets for RWC products, including the company’s opportunities in Europe, are likely to improve with the cycle, and the company is well-placed to capitalise on such an upswing. We are patient investors and find the opportunity to add to the quality of the portfolio when prices don’t reflect medium term opportunities.

The battle between the short-term and long-term is straightforward in commentary from sell-side analysts. Almost all noted that the business, on an underlying or fundamental basis, had improved over the past 6 months, but most were more concerned about the next 6 months. We continued to invest for medium-term outcomes.

Some medium-term outcomes we appreciated included a conservative management focus on controllable costs, evidenced by the drop in corporate expenses in the period, strong EMEA margins despite weak sales growth, and ongoing manufacturing optimisation. Watching the company operate for a decade reinforces the value it creates when they apply these skills to newly acquired assets.

An example of the operational success can be seen in the Figure 4 below. Presented in US dollars it is the segment result for the Americas business. We wouldn’t normally present information in such a manner, but we were interested in showing the power of operating leverage, despite relatively weak revenue growth.

Operational success in key Americas segment

Source: Company reports

Net sales only increase 3.3% or $16.4m. Considering rising input costs and general inflation levels, such a growth rate could have been expected to deliver, at best, the previous year’s margin (16.3%) or $2.7m of increased EBIT. Instead, The business increased EBIT by $6m, or at over twice the rate. Of course, this is a small amount for a company valued at US$2.5bn. However, the ability to grow earnings at twice the rate of growth as sales in a weak operating environment augurs exceptionally well for both long-term growth, as well as grow in better conditions.

Significant value at current share prices

We value RWC above $6 per share using conservative mid-cycle earnings and our long-run assumptions regarding cost of funding and future sales. In such a valuation, we do not include any additional value created through acquisition.

Including current balance sheet capacity and historical success would add another 20% plus to our valuation. With the stock trading in the low $5 the opportunity is clear.

To provide some graphical support to the contention, I have used the Macquarie Equities chart shown below that details the movement in total returns (black line) you would have experienced owning the stocks since listing, broken into the drivers of such a return. The three drivers shown are:

- Earnings growth (dark blue): Details how much the earnings of the company – per share increased since listing. As at today, earnings have improved more than 150%, that is the company makes 2.5 times as much per share as it did in 2016 when it was listed on the ASX.

- Dividends (yellow): Straightforward analysis of what dividends have been received as a percentage of the original price.

- The changes in the multiple paid for the earnings: expressed as the amount left over to derive the total return. For instance, if the total return is circa 100% and earnings have grown by 150% and dividends have provided +20% then the “amount paid” the change in a multiple must be responsible for negative 70%: (150% + 20% – 70% = Total Return of 100%)

RWC: Decomposition of stock price return since listing

Source: Macquarie Research

Clients first purchased the stock in 2020 and have experienced similar outcomes to that depicted in the black line in the chart above since 2020 – a more than 100% total return. But stock price growth has lagged earnings growth.

What drives a scenario in which earnings growth outperforms stock price growth?

The implication is that the company has outperformed earnings growth and delivered story dividends, but the market is paying less for the future (lower multiple) despite improvements in the business. The missing link to explain it is short-term concerns with market conditions.

As we have done for the past 5 years, we will look to accumulate during periods of weakness, and trim when the gap between price and earnings closes.

Seek Limited (SEK): Weak earnings – strategic success

Seek provided its 1HFY25 financial results this week, and management noted as a headline “strength in all strategic priorities, (market) share, yield and operating leverage.”

We rarely agree and doubtless never fully agree with management hype. Still, on balance, evidence of positive strategic outcomes littered this result despite the weaker headline earnings, which were driven by lower levels of job advertisements.

The share market reaction since the result was positive, although the RBA and Michelle Bullock can probably also claim some of the credit.

Our thesis for owning Seek Limited has five basic tenets:

- Seek has dominant or leading positions for online ads across a range of markets, and that dominance creates opportunities for pricing power.

- Seek has a cost base that is too high compared to other growing Online businesses, and slower cost growth in the future will accelerate margin expansion

- The Seek solution is increasingly built into the job-seeking and job-letting behaviour of corporates and employees alike. This integration and expansion of services offered further increases the value proposition the Seek brands create. This is evidenced by increased site use, regardless of revenue or ads placed.

- Seek owns a 83% stake in the $2.2bn Growth Fund ($5 per share) partly grown through seeded assets and partly through investment. The value of this stake heavily discounted by the market. Should it prove the worth accountants ascribe to it, and more importantly, actual cash, was distributed back to the company, there would be value attributable to the company that we are not currently paying for.

- In a similar vein to BlueScope and Reliance Worldwide in this week’s Investment matters, economic cycles come and go, and a well-run company with balance sheet strength and great brand and market position should not be too heavily discounted.

Unlike most other stocks in the portfolio, the company’s share is relatively expensive based on current-year earnings as such it needs to grow earnings quickly to justify the current share price regardless of the merit of the five tents outlined above.

Seek ticked, at least partially, all the strategic boxes in this half, despite earnings falling, not growing.

Thanks to the RBA and the outlook for rates post election the cycle may improve, but tenet 5 still holds we want to buy cyclical short-term factors dominate market outlooks. Looking at the four in detail follows.

Pricing power

Throughout 2023 and 2024 there has been a reduction in the numbers of job ads placed on the SEK Australian website. Figure 6 below shows the year-on-year growth rates since demand peaks in late 2022. With SEK revenue effectively a function of number of ads multiplied by price, the impact on revenue should be clear.

SEK: Lower numbers of job ads – cyclical factor

Source: SEK Job Ad index, Barrenjoey

Offsetting the weakness in volumes is continued increase in yield.

This is shown clearly in the water where despite the volume reductions overall revenue was only down 4 per cent due to significant increases in price.

SEK: ANZ Revenue waterfall from 1H24 to 1H25

Cost control

There were positive steps regarding cost control that we haven’t seen evidence of in the past. Total expenditure (operating and capital costs) was well controlled demonstration some with flexibility in the cost base. We are concerned that some of the improvement may be related more to the end of some development projects, but the proof of success with be seen over next twelve months.

Partial tick.

Value proposition: Imbedded usage

One series of chart provided in the update was worthy of presentation. It shows that despite the lower ads placed the health of the ecosystem or service SEK is providing in Australia is likely improving.

The top chart show the 145 reduction monthly paid ads. But more interestingly this involved only 3% less unique hirers. Companies were still using Seek.com.au they were just placing less ads.

The second chart shows that despite there being 14% less ads there was an 18% increase in monthly unique visitors. And the final chart shows that these visitors were not deterred from applying for the lesser number of ads. The number of applicants per role continued to grow through the period. Higher number of applicants over time drives increasing value and usage of support services that Seek also provides employers.

SEK How visitor numbers, users and their activity highlight system strength

Over the improvement in value proposition was a big tick

Growth Fund

A final chart shows the reported improvements in valuation of the Growth Fund since commencement. According to the valuations provide the Fund has generate significant value. The SEEK growth fund focuses on high-growth technology businesses across three themes: HR SaaS, Education and Contingent Labour. SEK holds an 83.8% stake in the Fund.

We have already referred to the discount the market applies to the valuation. The important news this week was the explicit notification of the sales of a Fund asset “Employment Hero”, along with news that notice was provided to the Fund that a liquidity draw would be sought in due course.

The long road to turning this Fund into cash in the hands of shareholders may be commencing. Tick.

SEK Growth Fund, portfolio movement since creation

The information in this article is of a general nature and does not take into consideration your personal objectives, financial situation or needs. Before acting on any of this information, you should consider whether it is appropriate for your personal circumstances and seek personal financial advice.