Copyright 2025 First Samuel Limited

Read the previous week’s Investment Matters.

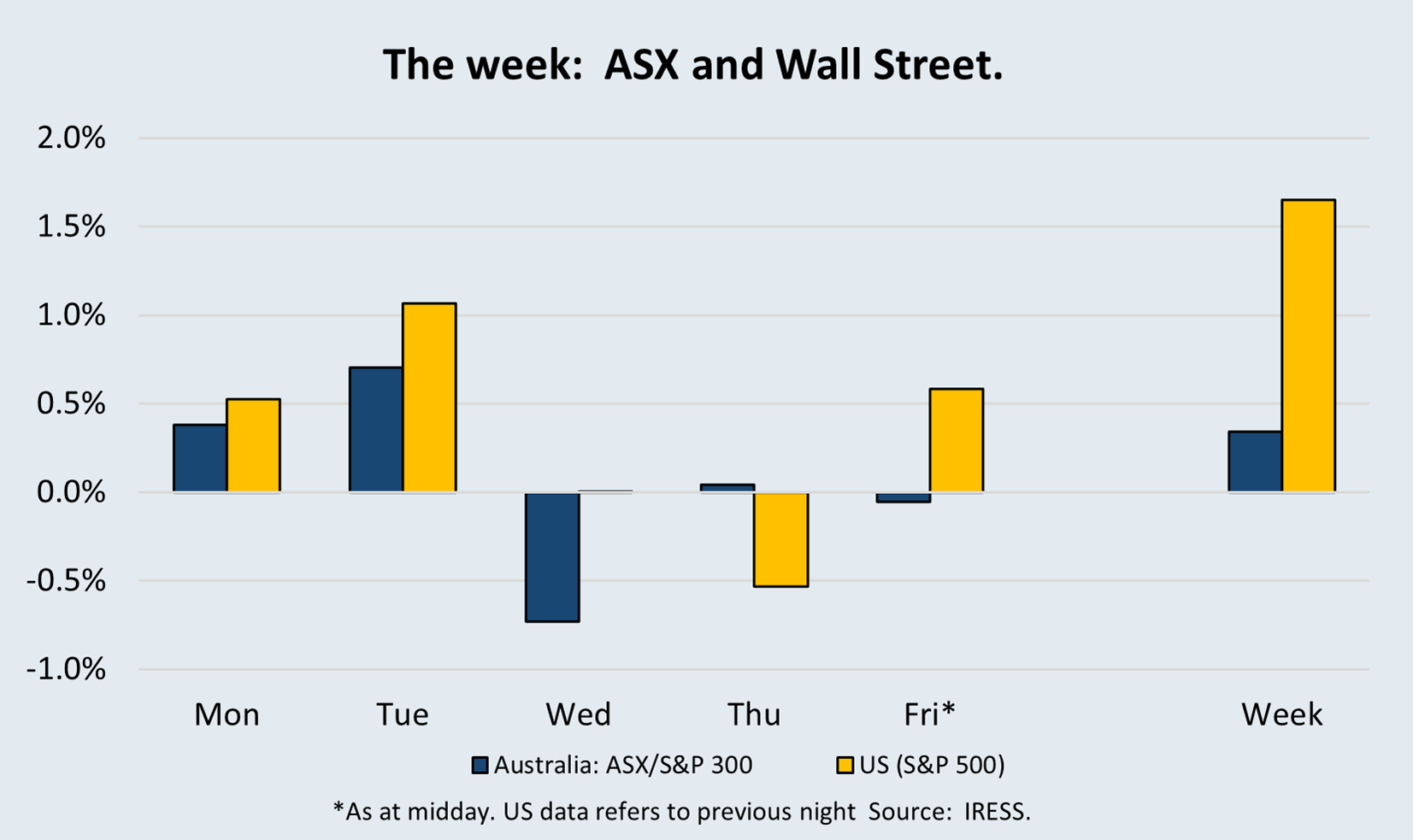

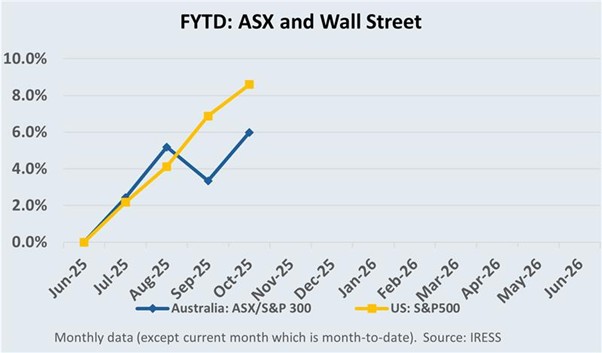

The Market

Catching up on the news

This week’s Investment Matters catches up on portfolio news and commentary on recent portfolio movements.

Summary

- The ASX and global markets are expensive compared to the economic outlook and historical prices.

- Sectors, including technology, gold, and rare earths, have seen meteoric rises in value, which are beginning to appear stretched. The week saw the first signs of fatigue in gold prices.

- The market appears to be overpaying for good news and tailwinds, and overly discounting short-term weakness and macroeconomic uncertainty.

In this situation, we have adhered to our long-term investment fundamentals. We are trimming positions that have exceeded our long-term valuations and raising cash levels.

In brief snippets, there was

- a weak update from our portfolio turnaround stock, Bapcorp (BAP). We continued to believe that, despite execution and governance issues, the value of this franchise is significantly larger than the current share price

- an update from Cleanaway (CWY) that noted subdued economic conditions in recent months. Despite reiterating FY26 earnings guidance, the market was concerned about short-term softness. We were not.

- Interesting commentary from a long-held position in TZ Limited.

“TZ Limited notes it has rejected a non-binding and indicative offer to acquire TZ’s US subsidiary… from Quadient SA, a company listed on Euronext Paris with a market capitalisation of AUD$868m. The Board of TZ gave due consideration to the offer which would have enabled TZ to restructure debt and provide additional working capital to fast-track expansion. However, the Board determined that the bid undervalued the US business and particularly its client base of significant, world-class companies.”

The three most significant news events for the portfolio, though, were rare earths, gold, and Reliance Worldwide, which we addressed in order.

A deal on rare earths

The answer appears to include a client sub-portfolio investment with the Macquarie Group. Based on the investment made over the last decade, they appear to be well-positioned in a period when players are desperate for capacity. Only time will tell if selling today is premature.

Still, we were thrilled by the announcement that it had sold a network of 50 data centres across North and South America to Global Infrastructure Partners and the Artificial Intelligence Infrastructure Partnership, a consortium including BlackRock, Nvidia, and Microsoft.

Aligned Data Centres was the Macquarie-owned and Texas-based firm it sold for $US40 billion ($A61 billion) in the asset class’s largest-ever deal. The markets expect that shareholders in Macquarie will benefit from significant fees and performance bonuses from the sale over the next 2 years.

The manhole cover?

This week saw a deal signed between President Trump and Prime Minister Anthony Albanese on rare-earth and critical minerals called “Framework for Securing Supply in the Mining and Processing of Critical Minerals and Rare Earths”.

Headlines are always problematic in the Trump Era, but the deal was described as a US$8.5 billion pipeline of priority projects across both countries. The speed of the project implementation plan, over the next six months, matched the hype, the political importance and the geopolitical context. As UBS noted in a recent report, “The Middle East has its oil, China has rare earths”.

The objectives included accelerating the mining, refining, and processing of rare-earth and other critical minerals in Australia and creating more secure supply chains for the U.S. that are less dependent on China.

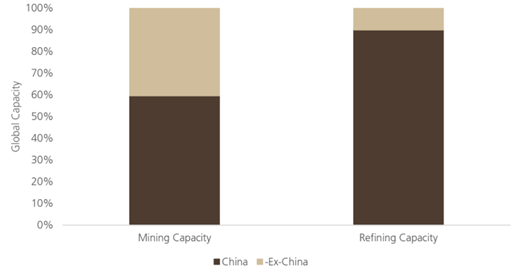

As we have noted on many occasions, rare earths are a problem that is not easily fixed but has been profitable for clients. The issues are a combination of supply at that mine level, which can be solved relatively quickly, and supply constraints at the processing level, which are much more difficult in our view (see Figure # below). China’s dominance in permanent magnet production, even further downstream, may be even more problematic.

Figure #1: China’s dominance in rare earths processing

Source: Wood Mackenzie, Company Filings, UBS.

Lynas (LYC) is playing a role in both the mining and processing solutions and has seen its share price rise 120% since June 2025, and more than 200% over the past eighteen months. The share price, in our view, entirely discounts the good news in the announcement and the long-term fundamentals. As such, we have continued to trim clients’ positions and retain a small portfolio position.

Addendum

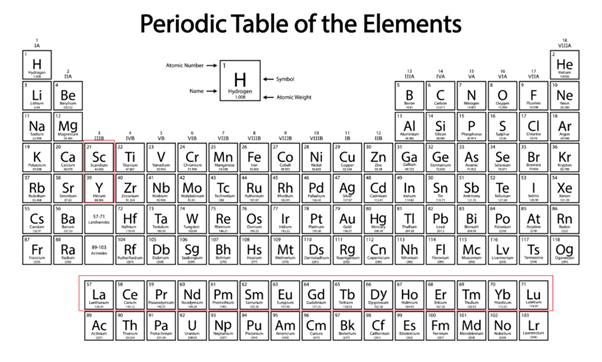

For readers inclined to remember their periodic table from school, I have included a handy picture showing which elements are “rare earths”. In addition, a table shows some uses for the elements. What is clear from that table is the strategic value of these uses. It was the strategic and geopolitical implications that first attracted us to this position many years ago.

| Rare Earth Element | Selected Uses |

| Lanthanum | Optics, Refining |

| Cerium | Catalytic Converters |

| Praseodymium | Magnets, High-Strength Metals, Glass |

| Neodymium | Magnets, Lasers |

| Samarium | Magnets, Nuclear Reactors |

| Europium | Phosphors, Lighting |

| Gadolinium | Shielding, MRI |

| Terbium | Fluorescent Lighting, Magnets |

| Dysprosium | Magnets, Lighting, Lasers |

Gold price falters

Over the course of the week, gold prices experienced a sharp pullback. Spot gold slid from around US$4,380/oz to about US$4,050/oz within a few days.

The rally since August earlier this year had been extraordinary. Whilst the drivers of enthusiasm for gold are well understood—political uncertainty and concerns about the supply of money —there can be times when markets display pure Irrational exuberance.

Pictures of queues for Gold in Martin Place, Sydney, supported that contention.

Figure #2: The rise and correction of gold over the past 12 months

Source: Facebook

Our long-run value of gold is circa $3,200 USD, based on a probability-mixture approach incorporating inflation-adjusted peak prices, the supply of money, global cost curves, and underlying economic certainty. Referring to the chart above, it was clear that there was support at the $3200 USD level in the middle of the year.

But with the rapid ascent since we have been taking profits in several portfolio gold miners. Strong profits have been realised in Ora Banda Mining and Minerals260. This is in addition to fully sold positions in Catalyst Metals and De Grey Mining.

Our core holding in Newmont Mining has been retained at this stage. Whilst valuation support is limited, the likelihood of persistent high prices ($3,200 USD or higher) is very supportive of Newmont Mining’s long-duration assets. The full value of such an outcome is not included in the current price.

Reliance Worldwide (RWC) – AGM and Investor Day

Reliance held an investor day in Sydney on Thursday, and we enjoyed the opportunity to catch up not only with the CEO, Heath Sharp, but also with several impressive senior leaders across the globe.

Reliance’s Investor Day followed the AGM, held the day before, during which they provided a much-anticipated trading update. The update met the market’s subdued expectations. The key points from RWC’s trading update are that RWC expects group sales for 1H26 to remain flat or decline by a low single-digit percentage year on year.

The last 12 months have continued to see soft sales momentum due to weak underlying conditions. The cycle was only exacerbated by the expected impact of Trump’s tariff policy, which has required Reliance to reassess its global supply chains, including where it plans to manufacture and assemble products.

Investor Day Presentation

After listening to management spin and consultant gobbledegook for 25 years, your author has become a little jaded by long presentations on “strategy”, but strangely enough, after an hour or two of listening to examples and explanations regarding the Reliance strategy, I realised it was both sensible and consistent with our investment case—a pleasant surprise.

The strategy leverages the features of the business we believe give it a strategic advantage. The model can also readily accommodate significant M&A, which we believe is the key to growth in this business. What is the strategy?

- bringing innovative solutions to the job site

- a distribution model that offers real value to retail partners through deeply integrated supply relationships, and

- a strong execution ethos.

Reliance’s final customers are plumbers, DIY, and building companies, but their direct customers are the world’s biggest and best retailers, including Home Depot and Bunnings. It is vital that this business model.

Modern product manufacturing and distribution is highly integrated into businesses such as Bunnings. The picture below shows the role of RWC in Bunning, including training Bunnings staff, stocking shelves, hustling for shelf space and solving marketing challenges. In an era of social media and content creation, it was also impressive to see Reliance’s progress in developing “how-to-videos” on YouTube that have garnered more than 35 million views in the past 12 months.

This type of integrated value builds brand value and profits.

Figure #3: Integration with final users and retailers is RWC’s strategy – Bunnings example

Source: RWC Company presentation

On 29 August, we wrote that:

“We saw a few long-term difficulties and no negative impact on our long-term valuation. We remain attracted to high-quality assets, demonstrable value creation through acquisitions, and market-leading brand names. As US conditions improve and tariff pricing is resolved, we see significant upside from current levels.”

The presentation highlighted the progress the company has made in addressing the tariff challenges. We believe that their speed and flexibility in responding to the new world trade order is not only a tick for management but a future source of competitive advantage.

It also highlighted progress on new product development. And without getting into the weeds of behind-the-wall plumbing, some of the developments looked promising for both sales’ growth and deeper relationships with retail and end-user clients.

Analysts at the Investor Day tended to concentrate a little too much on short-term profits in our view. Regardless, this demand for short-term good news identified some material cost savings the company has been able to access as it rebuilt its supply chains.

But what are they going to buy?

The last leg of growth for Reliance beyond organic improvement and a rebound in the economic cycle is the appetite and ability to continue to find M&A targets. The industries and countries that Reliance operates in are prime for ongoing consolidation and Reliance has been successful at acquiring in the past.

It was pleasing to see explicit discussion of the types of opportunities that are actively being sought, with RWC focused on extending commercial market exposure, in particular. M&A markets have been quiet, but the group is seeing some inflection.

The role of M&A was critical to a significant update on the EMEA region. Europe always appears a challenge from Australia, and the company acquisition of John Guest has not necessarily delivered fabulous results, so we were keen to hear good news on the growth outlook for this market.

Internal focus in the region has clearly been on system and process redesign to address customer service challenges. Now growth is the objective, and we were excited by the mix of organic and inorganic opportunities.

We have increased our long-term valuation on the basis of this opportunity.

The information in this article is of a general nature and does not take into consideration your personal objectives, financial situation or needs. Before acting on any of this information, you should consider whether it is appropriate for your personal circumstances and seek personal financial advice.