During May there are many opportunities for companies to update the market. These include investor conferences such as Macquarie Bank’s in early May and dedicated Investor Days that individual companies provide to analysts and the broader investment community.

In addition, some companies with different financial year reporting timetables update the market. Companies such as Macquarie Bank and Nufarm are examples from this month.

Clients may have noticed the sharp rebound in the share market in recent weeks, and we would note that the opportunity the sell-off in April provided proved beneficial to returns. We were net buyers in clients’ Australian shares’ sub-portfolios, reducing our cash holdings in April. The selling provided opportunities to add to oil / energy and technology companies. A number of these positions have been handsomely rewarded.

The Macquarie Bank update pointed to long-run value creation.

This week’s Investment Matters will focus on the Nufarm result, Investor Day presentations from Seek Limited and Worley Limited.

Read the previous week’s Investment Matters.

Nufarm 1H25 Results

The most disappointing company update of the season was Nufarm, a long-held and ultimately as yet unsuccessful investment. Nufarm, headquartered in Melbourne, Australia, is a leading global crop protection and seed technologies company providing generic pesticides and seeds to agriculture markets worldwide.

The company released its 1H25 results on Wednesday.

Earnings were disappointing, as was effective guidance for a weaker second half of FY25. However, the real impact on the share price, which led to a 30%+ fall, was the company announcing a strategic review of its Seeds Technologies.

The implication is that the existing board and management have, as yet, failed to fully maximise this business’s potential. Many holders of the stock on the ASX in general and First Samuel in particular saw in this business as the crown jewels of Nufarm, especially from a long-term perspective.

Whilst a review and possible sale of the Seeds business could crystallise cash, the current condition of the overall Nufarm business, along with depressed earnings in Seeds, is unlikely to extract the full value of this asset. And once this part of the business is sold for a discount, the amount of upside remaining in Nufarm would be similarly limited.

Sometimes, being a successful seller is as much about the seller’s condition as it is about the conditions of the company being sold.

We believe the Strategic Review is a strategic mistake, especially if it leads to a sale of these assets to a third party. There is a risk that Nufarm, following this announcement, sells the Seeds Technologies business for up to $2 per share less than what it could be worth in 3-5 years.

Why such a dramatic difference?

The crop protection business is a lower multiple, high capital-intensive business that is subject to significant variation in input prices, agricultural risks, and product development costs. It does, however, benefit from structurally stable demand, moderate margins, and good returns on depreciated fixed capital, although it requires a high level of leverage to support working capital.

The Seed Technologies business is a distinct sector, benefiting from advancements in seed development, tailwinds from shifts in tastes, and environmentally sustainable fuels. It benefits from the desire to improve human health through better foods and can form the backbone of support for innovative farmers. Globally, seed businesses trade on much higher sustainable earnings multiples and are funded for growth by significant investment in R&D.

Figure 1: Seed Technologies: Medium-term growth with high value now at risk from review

Nufarm’s seed technology portfolio spans canola, sunflower and sorghum varieties and the new biofuel crop carinata, which will expand threefold in planting area this year

In the past, there were differences of opinion in the market regarding the appropriate leverage in the Crop Protection and Seeds business. The question is critical because each part of the overall company has fundamentally different needs, capital costs, and growth outcomes. Failing to fund the growth prospects for Seeds can impact the long-run value of Nufarm considerably.

We have always been proponents of breaking the businesses apart and funding each operation in two ways, or if they were to remain together, they would need be structured to have different funding sources.

A demerger would avoid a scenario where weak short-term performance in one or the other business impacted the funding of growth and value creation in Seeds. The worst scenario would be when Nufarm was forced to or cajoled into selling the Seeds business, instead of demerging or internally developing.

Short-term earnings

Near-term earnings overall were disappointing, with full-year profits now likely to be 40 per cent lower than our expectations and those of the market. The miss in earnings, however, was a mixture of isolated factors in the Seeds business, and the core business of crop protection was slightly ahead of expectations. Without the strategic review, the direct impact of the earnings disappointment on our valuation would have only been a 10-15% reduction, much less than the share price movement.

The concern is that a strategic review, especially one managed by a global investment bank, will likely be far more short-term oriented than we would appreciate as long-term investors.

This week’s changes have prompted a review of the size of our holding in Nufarm.

Seek: Investor Day

The Seek Investor Day provided a much-needed upgrade to their current earnings guidance and some strong messages regarding the medium-term outlook, consistent with our investment rationale.

The market appreciated the update, with the stock outperforming by 5 per cent this week.

Seek represents one of First Samuel’s core technology positions. It is more expensive than most companies in our portfolio in terms of the price-to-earnings ratio. Still, after accounting for market position and earnings growth, the company represents good value both at the time of purchase in 2023 and at current levels.

Investment Matters readership would appreciate that Seek Limited (seek.com.au) is the market leader in the online employment classifieds market in Australia and New Zealand. It also operates a learning business in Australia and New Zealand, owns several international assets in Southeast Asia and merging markets, and is the major reseller of online tertiary courses in Australia.

At the Investor Day, we particularly appreciated Seeks’ assessment of its current business. The company noted that its capital and software development investments in recent years have built a strong foundation for growth, a well-established customer franchise and a scalable platform.

The quality of the base to grow both the number of job ad placements and the yield (price per placement), will determine the operating leverage and earnings growth we can expect. At the current share price, the market either does not appreciate the scale of operating leverage possible or doubts the company’s ability to execute such an improvement. We do not share such concerns.

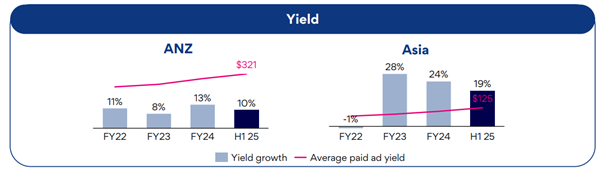

Part of the presentation at the Investor Day, which supports future operating leverage, focused on the recently completed “unified platform.” The investment behind unification has been considerable and should form the basis of controlled expense growth over the next 5 years. On the revenue side, ongoing increases in yield have been evident for some time, as outlined in the Figure below.

Figure 2: Seek yield improvement: The basis for future operation leverage

The incremental benefits are now emerging with Seek expecting to be in the top half of previously communicated revenue, EBITDA and adjusted profit guidance. This was rewarded by strong share price growth this week.

With this week’s RBA rate cuts improving the operating outlook, and product release post completion of the unification project, involving AI is accelerating and improving yield. Management appeared confident in continuing to grow topline revenue while leaving operating cost growth at lower levels.

In time, First Samuel believes Seek could still reduce expenses much further. We anticipated that a different management team or one with different incentives would achieve a material reduction in cost.

The current share price already represents a reasonable value with such improvement; hence, any possible change represents pure upside from our portfolio position.

Structural improvement and AI

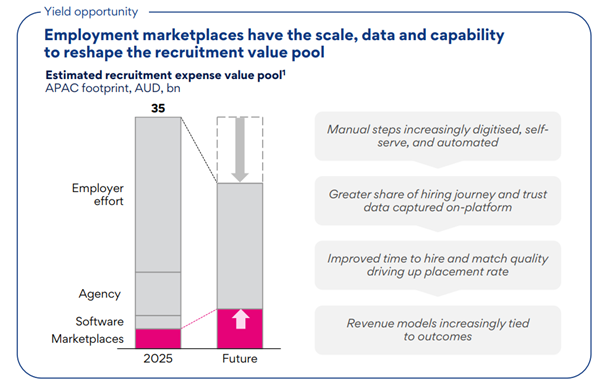

One of the diagrams presented on strategy day that we appreciated provided the Seek vision for the future of recruitment expenses. This view is likely to be very important if the benefits of AI can be harnessed at the enterprise level.

On the left-hand side, the current “value pool” highlights the vast amount of expended effort for recruitment that falls on the employer. In comparison, employment agencies and Marketplaces such as Seek capture a relatively small amount of the value.

We can imagine future solutions, including AI, with the recruitment process developed by Marketplaces such as Seek. Seek already provides various solutions to assist, and we anticipate future solutions enabling even lower overall recruitment costs. As noted by the chart below, lower overall costs will allow a greater share of the value to be captured by companies such as Seek.

We view this example as a perfect investment opportunity that captures some benefits of Enterprise-level Artificail Intelligence. Rather than invest in esoteric possible future businesses, we prefer to invest in existing enterprises that can be made better by the emerging technology.

Figure 3: Seek: The future of recruitment expenses: Seek’s opportunity

Worley Investor Day

We attended the Worley Investor Day on Tuesday this week. A long-held position in clients’ portfolios, Worley has the highest expected returns in our universe and remains undervalued by the market relative to other stocks and its own price history.

Some short-term issues require attention by management on the day, especially those relating to a significant project in the US called CP2. Still, in general, we were more interested in the long-term development of Worley’s range of services to its global clients. We felt there was a good balance between showcasing its growth strategy and a general business update.

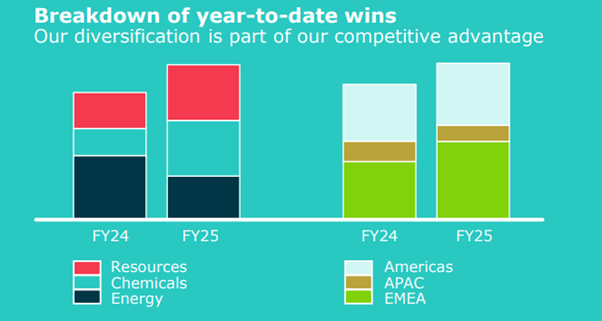

Regarding short-term earnings, there remains uncertainty regarding oil prices in a tariff-uneasy world. Still, there had been no material project cancellations or deferrals since the last update in February. The chart below shows the company being ahead regarding project wins in FY25 (TYD March) versus the previous year. The breadth of improvement across chemicals and resources is especially pleasing, given the upside potential in Energy in the medium term.

Figure 4: Worley: Strong progress building its project pipeline in FY25

As the chart above shows bookings for the 9mFY25 are running at A$9.4bn (+22% vs. pcp)

Progress on the critical CP2 project over the next 9-12 months is likely a key catalyst for the stock with target project mobilisation by mid CY25. We continue to see value in Worley, with the stock trading at a 1yr forward P/E of 16x (excl.CP2), well below the 24x the stock traded at during the early stages of the last energy capex cycle.

Lingering question?

We noted with amusement an article in the AFR Chanticleer column (22nd May) regarding the style of the Worley Investor Day. Both the written presentation and presentation style, as Chanticleer noted, were “like ….. had swallowed an MBA textbook”. We referred to the entire multi-hour presentation as management buzzword bingo.

Perhaps businesses in 2025 with a global workforce of 50,000 employees need scripted hollow and obfuscating language served up in bite-sized chunks. But we doubt effective decision-making is consistent with such a narrative style. So, either there is a dramatic difference between how the company operates and how it communicates, or its operations are limited by ineffective communications. A lingering question that limits the size of our investment in Worley.

The information in this article is of a general nature and does not take into consideration your personal objectives, financial situation or needs. Before acting on any of this information, you should consider whether it is appropriate for your personal circumstances and seek personal financial advice.