Copyright 2026 First Samuel Limited

This week in Investment Matters, Craig takes a deep look at:

- the investment consequences of the Iran-US ‘understanding’

- what it means for portfolio construction

- RBA’s difficult task

Read the previous Investment Matters here:

Iran resolution

The announcement of an Iran deal last week, followed by further details of the memorandum this week, has been received positively by markets. That is not surprising. The war had created obvious inflation, energy, and geopolitical tail risks. The prospect of an end to hostilities, the reopening of the Strait of Hormuz, and a reduction in immediate oil supply risk gave investors a reason to look beyond worst-case scenarios. Equity markets have responded constructively, oil prices have eased, and the immediate risk of a renewed energy-price shock has diminished.

The backdrop of the conflict resolution may also have helped the RBA pause its rate hikes at this week’s board meeting. A lower oil price does not solve Australia’s inflation problem, but it reduces the risk that an already difficult inflation picture is made worse by another external energy shock.

That is clearly positive. But the positive market outcome should not be confused with a simple strategic victory. The end of the Iran war reduces risk, but it also tells us something important about the changing structure of global power. The long-term consequences of the litany of failures surrounding this misadventure may affect markets for decades.

The market

The world changes

This week’s Investment Matters is therefore not a note about one war, one oil price move, or one central bank meeting. It is about the reminder that the world changes. Sometimes the change is obvious in real time. More often, it is visible only through a series of events that force investors to question assumptions that have long worked.

The Iran resolution may be one of those events. It may be the precursor to a changed world, or perhaps simply another piece of evidence that the world has already changed. Either way, it leads us to the same question: what are we doing as investors?

Our answer is becoming clearer. We are moving away from excessive dependence on American exceptionalism. We are reducing energy exposure where returns rely too heavily on oil price volatility. We remain conscious of the RBA’s competing inflation and growth risks. We believe Australia is well placed, but only if capital moves toward productive assets and the next generation of economic capacity, rather than simply continuing the financialisaton of housing. And we are setting portfolios that are diverse enough to benefit from change, not merely defend against it. Importantly, performance through this period has been good. Client Australian equities sub-portfolios are now slightly positive since the start of the war, having not fallen as far as the broader market and having recovered well since. That does not prove the thesis. But it does give us confidence that the portfolio is moving in the right direction

End of the war is good news, but…

Ian Bremmer, founder of Eurasia Group, is an analyst whom I have followed for more than 20 years, and his analysis is useful in making this distinction. Bremmer is one of the more prominent global political-risk analysts used by investors, corporates and policymakers to interpret the connection between geopolitics and markets. His political-risk advisory firm is built around understanding how politics changes the distribution of economic risk. His broader thesis is that the world is increasingly operating without a single reliable organising power.

Bremmer’s argument following the deal is not simply about whether the war has ended, or whether oil has fallen, or whether markets can rally. It is about what the episode says about the structure of global power. In a world where neither the United States, China, the G7, nor the G20 can consistently provide global public goods (security, safe passage, free trade, etc.), conflict may end, and trade may resume. But the underlying system becomes more fragmented, more transactional and less predictable.

Seen through that lens, the end of the Iran war is good news, but not necessarily evidence of restored American authority. Iran has survived. The United States has had to negotiate an exit. Regional partners have again been reminded that the US security guarantee can be powerful, but also conditional and unpredictable. China, by contrast, has been able to present itself as the more patient, commercially focused and less disruptive great power. The war’s end is positive; the manner of its end is less flattering to the US-led order.

MOU shaped by constraint, exhaustion and accommodation

Perusing the scope and language of the MOU is a sobering experience for anyone anchored to the worldview that has dominated international relations since the mid-1970s. The United States remains powerful, but the document does not read like a demonstration of uncontested American control. It reads like a settlement shaped by constraint, exhaustion and the need to accommodate powers that Washington can no longer simply instruct.

This distinction is important for investors. The market event is straightforward: the cessation of hostilities reduces the immediate risk of an oil shock, lowers the probability of a renewed inflation spike and supports global risk appetite. The strategic event is more complicated. The war appears to have reduced, rather than reinforced, the geopolitical power of the United States. It has also reinforced a world in which regional actors hedge, China gains relative influence, and the gap between American power and American control continues to widen.

The Iran war has elevated China geopolitically, not because Beijing has suddenly displaced Washington in the Middle East, but because the conflict has made China more central to every calculation: oil flows, Iranian reconstruction, diplomatic settlement, and the wider question of whether the US can remain focused on Asia while being pulled back into the Gulf. China has gained relevance without firing a shot.

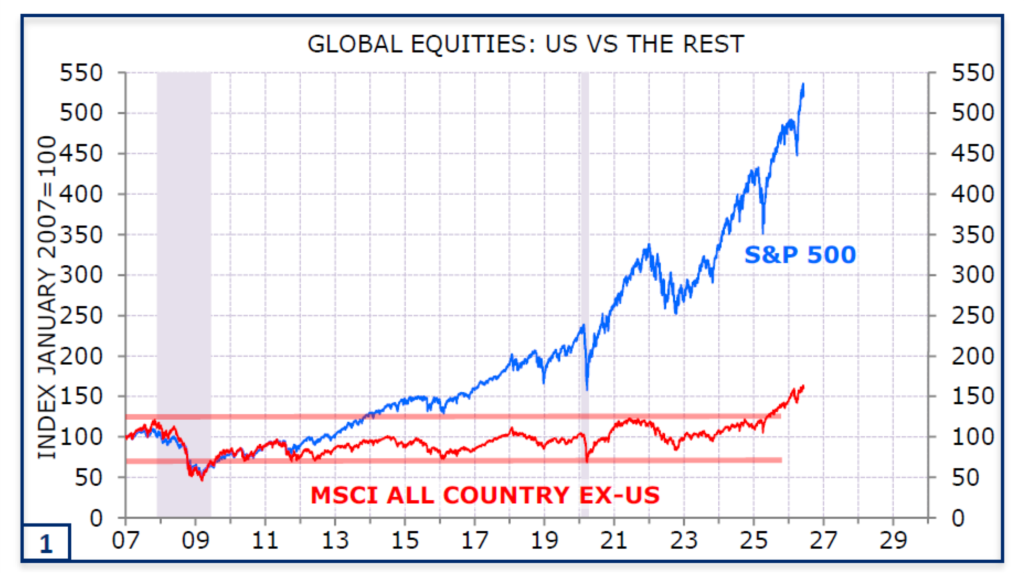

The implications for Australia, forever balancing the risk and benefits of China’s rise, this week may prove consequential in the medium term. For investors, changing geopolitical conditions may not affect stocks in the short term. However, medium-term trends have dominated relative returns for almost two decades. The relative performance of the United States versus the rest of the world has been one of the defining investment facts of this era.

Figure #1: American exceptionalism is clear

Source: Minack Advisors

American exceptionalism is powerful, but not riskless

American exceptionalism was on display last week with the SpaceX IPO. The IPO went well, with the stock trading towards US$200, up from the US$135 list price. In recent days the mood is weaker, and given the significant level of non-fundamental trading — index inclusion, options pricing, escrow release and momentum demand — the author’s value-investor bias screams: it is only a paper profit until you sell.

But the IPO event also ushered in a period in which the demand for additional capital to build out the AI future is vast. When factoring in corporate debt issuance alongside equity, the scale of capital raised over recent weeks has spiked dramatically, led by legacy technology giants funding enormous AI capital expenditure. Oracle and Nvidia joined SpaceX and Alphabet in reminding investors that the AI future is not simply a software story. It is a capital-intensive infrastructure story.

Dangerous conditions

The cash is being raised at a time when there is a dangerous set of conditions: equity is priced for perfection, the total capital requirements for AI investment are not clear, the returns expected from AI investment are still unknown, and higher returns are available from risk-free assets that would otherwise reduce demand for riskier debt.

We have continued to diversify holdings away from standard global indices, which are dominated by US equities and, in turn, concentrated in a relatively small number of stocks. This tilt away from the largest US companies has performed well. More importantly, it reflects a portfolio principle: a world that is becoming more fragmented, more capital-intensive, and more politically demanding should not be owned through a single narrow expression of growth.

This year, First Samuel clients have benefited from investment in Japan, in Emerging markets and in other parts of US equities. The past decade rewarded investors for owning the winners of American technology, low inflation, low interest rates and global financial integration. The next decade may still reward parts of that world. But it may also reward assets, production, materials, infrastructure, insurance, energy transition and companies that help economies build and adapt.

Australia is well placed, if we choose to be

It is the author’s view that in such a world, Australia is well placed — strategically, physically and through the assets with which we are endowed. We need skilled people and institutions to make the most of them, but we have a head start across the board.

Australia has energy, minerals, food, land, rule of law, financial depth, proximity to Asia and a strategic location that matters more in a fragmented world. We also have companies with real operating assets, engineering expertise, infrastructure capability and exposure to global supply chains.

But we do not necessarily have the political legacy that manages endowments well. From Menzies to Whitlam to Howard, let alone the rotation of leaders since 2008, Australia has often viewed endowments as lollies for distribution, candy for the ill-informed, rather than building blocks for national success. In many respects, Australia has been so advantaged by the existing world order since the 1950s that we did not need to maximise our advantages. When the appetite for reform waned in the early 2000’s, we benefited from China and a surge in the terms of trade (Figure 2 below). The evolution of the Middle East in 2026 should prompt Australian policymakers to consider how Australia would respond to a world in which key resources in Iron Ore and Coal no longer support the economy.

Figure #2: Advantage can be fleeting: Australia’s Terms of Trade

Source: ABS, RBA

This is the constructive challenge. A world with more geopolitical friction, greater infrastructure demand, a more rapid energy transition, higher defence spending, and more regionalised production should favour a country like Australia. But only if capital is directed toward productive capacity rather than endlessly recycled through existing domestic assets.

Australia can benefit from a world that needs to build. But that requires us to build as well. Our portfolio includes a range of companies that lead the building task, including SGH (Boral, Coates and Westrac) and Emeco, as well as miners that span the entire materials complex.

What oil taught us

There is also an important investment lesson from the oil market. The Iran war created a genuine supply shock, yet oil prices did not behave as if the world had no alternatives. Inventories were used, trade flows adjusted, demand was rationed, refinery runs were cut, and non-Middle East supply responded. The oil market was volatile, but it was also more adaptable than many traditional energy bulls expected.

China played a major role, including in the Australian case, in providing downside protection by supplying jet fuel, exposing yet another supply-chain vulnerability while also showing the speed with which markets can adapt.

Energy sector exposure

There is also an important investment lesson from the oil market from this Iran war that sets itself apart from previous conflicts. The war created a genuine supply shock, yet oil prices did not behave as if the world had no alternatives. Inventories were used, trade flows adjusted, demand was rationed, refinery runs were cut, and non-Middle East supply responded.

The oil market was volatile, but it was also more adaptable than many traditional energy bulls expected. China played a huge role, including in the Australian case, in providing downside protection in the provision of jet fuel, yet another gaping supply chain hole that was exposed Figure 3 should show that not only did the spike fail to reach the levels feared by many investors, but the point of potential resolution rapidly saw prices return toward pre-war levels. The point is not that oil volatility has disappeared. It has not. The point is that the market revealed more buffers than expected

Figure #3: Crude Oil (WTI) Price – more buffers than expected

Source: tradingeconomics.net

Agility in oil markets matters for investors

That matters for portfolio construction. A world with weaker demand growth, greater substitution, higher strategic storage, more flexible trade routes and an accelerating energy transition is not a world in which we should automatically pay for oil-price volatility as a permanent source of excess return. For Australian energy names, particularly gas producers, we still recognise the strategic value of LNG and the importance of disciplined capital allocation. But the war and its cessation reduce the upside skew we are prepared to underwrite from these investments.

Santos remains the best example of the nuance. Santos has been attractive and continues to trade at a discount to our long-term valuation, despite our bearish outlook for long-term oil prices. Santos remains a complicated Australian energy company, but it holds a portfolio of scarce, long-life LNG, oil and gas assets. The appeal is not simply oil-price leverage. Instead, Santos’s major projects are moving from construction to cash generation, with a clearer commitment to shareholder returns. With excellent asset quality, Santos can navigate the combination of political risk, execution risk and a capital allocation minefield. In this respect, it remains a compelling investment given the gap between the asset’s value and its listed-market price.

Clients will note that we used the war and its resolution to profitably lighten oil exposure. The balance of risk has changed. The geopolitical premium had become visible, the market had shown greater resilience than expected, and the end of the conflict reduced the probability that oil and gas equities would continue to be rewarded simply for owning exposure to volatility.

Since the outbreak of the war, clients’ Australian equities sub-portfolio average exposure to the energy sector, including Worley, is now around 30% lower. Worley is not a pure oil exposure. It operates across conventional energy, chemicals, resources and a growing range of sustainable industries. But it is still part of the broader energy and industrial capital expenditure ecosystem, and therefore sits within the same discussion about how much upside skew we are being paid to own.

Importantly, this reduction in energy exposure was achieved after the relevant investments returned approximately 10% in an otherwise falling market. We did not reduce energy because it failed to perform. We reduced it because it had performed, the geopolitical premium had become more visible, and the expected reward for continuing to carry that exposure had fallen.

Less energy, more assets

This does not change our broader preference for owning real assets linked to global production. If anything, it reinforces it. The distinction we are making is between:

- owning hard assets that are central to industrial activity, infrastructure, and supply-chain resilience; and

- owning energy exposure that relies too heavily on oil price volatility to generate excess returns.

Our recent portfolio focus has been on the former: for example, businesses such as BlueScope and SGH (Seven Group Holdings), where the assets, capabilities and market positions are connected to construction, production, equipment, logistics and the maintenance of the real economy.

That focus remains important in a world that is more fragmented, more capital intensive and more geopolitically contested. BlueScope gives us exposure to steel, manufacturing capability, North American industrial demand and the replacement value of difficult-to-replicate assets. SGH provides exposure to WesTrac, industrial services, infrastructure, energy, equipment and the compounding effect of disciplined ownership.

These are not abstract financial assets. They are operating assets tied to the physical economy, and we believe that matters more, not less, in a world of disrupted supply chains, defence spending, energy transition and regionalised production.

Clients’ Australian equities sub-portfolio’s performance during the conflict also supports this broader interpretation. Returns have been slightly positive since the start of the war, having not fallen as far as the broader market and having recovered nicely since then.

Critically, the sub-portfolio did not depend on a single macro bet, a single commodity price, or a single geopolitical outcome. It benefited from a broader exposure to the real economy and from companies able to operate in a world of higher uncertainty.

Figure #4: US Hot Rolled Coil Steel prices

Source: tradingeconomics.net

The best-performing stocks through the conflict included both those exposed to hard assets, including Rio Tinto and BlueScope, and those that build, repair and supply the physical economy, including James Hardie and Reliance Worldwide. These are businesses connected to materials, construction, infrastructure, and the supply chains that underpin real activity

Companies that facilitate

We also saw strong performance from companies that facilitate investment and activity rather than merely consume it. Macquarie Group rose around 20%, supported by trading gains and its continued focus on infrastructure. QBE, as a global insurer, continued to benefit from higher interest rates and disciplined pricing. More broadly, markets maintained their focus across a range of materials supply chains, including copper and base metals. The lesson was not that investors should avoid risk. It was that investors should be more precise about the type of risk they are being paid to own.

Medium-term portfolio lessons

The war, when combined with the ongoing political changes across Western democracies, reinforces a deeper portfolio lesson. Simply relying on old models of growth, capital allocation and politics — models that suited the financialisaton of domestic assets — has limited scope from here.

The RBA’s difficult position

The RBA faces a difficult task. Inflation remains too high, but growth is slowing. Lower oil prices help, but they do not solve the domestic inflation problem.

Listening to the press conference this week, we remain impressed by the Governor’s careful resolve and ability to explain both counterfactuals and trade-offs. Pleasingly, the balance between future rate rises and the capacity to cut if required appears more measured.

That is true. But the transmission mechanism of higher rates is also uneven. Higher interest rates work through housing, credit, confidence, investment, asset prices and eventually employment. The cure is not painless, and it does not fall evenly.

This is where the RBA’s problem becomes an investment problem. Australia’s old growth model was unusually dependent on housing credit, rising land values and expanding bank balance sheets. That model created wealth for many households, supported consumption and helped the major banks compound over a long period. But it also shifted capital toward domestic asset inflation and away from investment and drivers of productivity.

The next phase may be different.

Banks, housing and the limits of financialisation

The war, when combined with ongoing political changes across Western democracies, reinforces a deeper portfolio lesson. Simply relying on old models of growth, capital allocation and politics — models that suited the financialisaton of domestic assets — has limited scope from here.

The impacts of these trends are already visible at auctions and in the politics of housing across the East Coast. Markets, being forward-looking, are beginning to price some of the risks. Rising Japanese interest rates, continuing strength in US hot-rolled coil pricing, and the political demand for more tangible domestic outcomes are all examples of the changing landscape.

Increasingly, politics is focusing on the tangible needs of domestic constituents: energy security, housing, infrastructure, defence, manufacturing capacity, cost of living and access to essential services. Whether governments can provide these things efficiently is a separate question. The direction of political pressure is clearer than the quality of the policy response.

The classic Australian example is housing affordability. We do not need to add endless text to an already crowded debate, other than to note that “be careful what you wish for” remains one of life’s more durable lessons, sitting comfortably alongside “know how little you actually know” and “stay curious enough to fill in the gaps”. Policies designed to make housing cheaper, easier to build, more accessible, more regulated, more subsidised or more taxed can all produce second-round consequences. In some Melbourne suburbs the consequences are already clear.

Prime Minister Albanese has noted the support he has received from younger people regarding changes in the housing market following the removal of investor subsidies. RBA Governor Bullock, meanwhile, has observed that investors in the property market generally have higher incomes and lower default rates, and that the larger concern is not necessarily immediate financial stability but the way investors can exacerbate housing cycles by entering when markets are rising and exiting when markets are falling.

The implication is straightforward. The path that connects young people to affordable housing, jobs and financial security may not continue the 30-year trend of rising house prices, expanding mortgage credit and low-risk returns for the major banks.

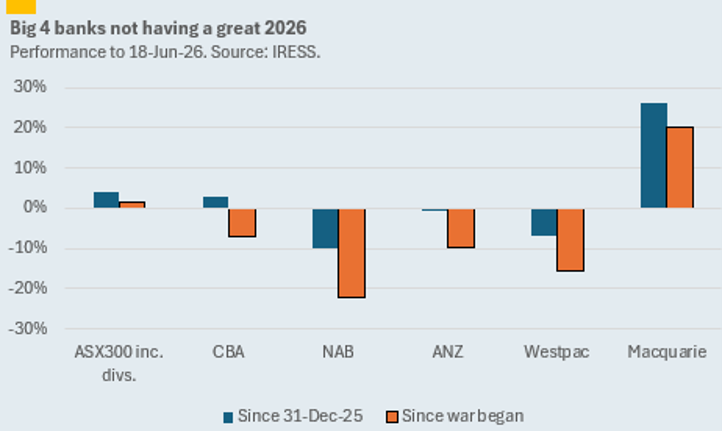

Markets are already responding to the combination of high starting prices for banks such as CBA and changing conditions. In fact, since the war began, there have been significant retracements in the big 4 banks and significant outperformance of Macquarie Group.

Figure #5: ASX already responding

Source: First Samuel; IRESS

That does not make the banks poor businesses. They remain highly profitable, well capitalised and deeply embedded in the Australian economy. But the market is beginning to recognise that the old model has limits. Higher interest rates, housing affordability pressure, slower credit growth, political scrutiny and the possibility of a different capital allocation mix all reduce the certainty that banks can continue to compound as they have in the past.

We are recognising that a portfolio built for the next decade should not rely too heavily on the financialisation of the family home as its central source of low-risk return.

Portfolio conclusion

The broader investment lesson from the past few weeks is constructive, not gloomy.

The world is changing. The Iran resolution may be part of that change, or simply another reminder of it. American exceptionalism remains powerful, but less unquestioned. Energy remains important, but the oil market has shown more adaptability than expected. Australia remains well placed, but only if capital is directed toward productive investment rather than endlessly recycled through housing. The RBA is trying to manage inflation and growth, but the economy it is managing is itself changing.

That is why the portfolio has been changing as well.

For portfolios, that means we want exposure to businesses connected to production, scarcity, infrastructure, and real-world problem-solving. But we do not want to confuse political demand with guaranteed investment returns. The opportunity is in owning companies with assets, capabilities, balance sheets, and pricing power that can operate in this environment. The risk is in assuming that every political promise, commodity shortage or infrastructure need will translate neatly into shareholder value.

We have reduced energy exposure after strong performance. We have maintained exposure to hard assets and global production. We have diversified away from a narrow concentration in US indices. We remain conscious of inflation, interest rates and the limits of Australia’s housing-led growth model. We own companies that build, repair, insure, finance, supply and operate the physical economy. And, importantly, client portfolio performance through this period has been good.

The opportunity is not in choosing between the old world and the new world. It is in owning companies that can operate as the world changes.

Markets will always move faster than conclusions. But this week’s conclusion is clear enough: when the world changes, investors should change with it.

The information in this article is of a general nature and does not take into consideration your personal objectives, financial situation or needs. Before acting on any of this information, you should consider whether it is appropriate for your personal circumstances and seek personal financial advice.