Read the previous Investment Matters.

Photo © WIlliam_Potter from Getty Images Via Canva.com

Copyright 2025 First Samuel Limited

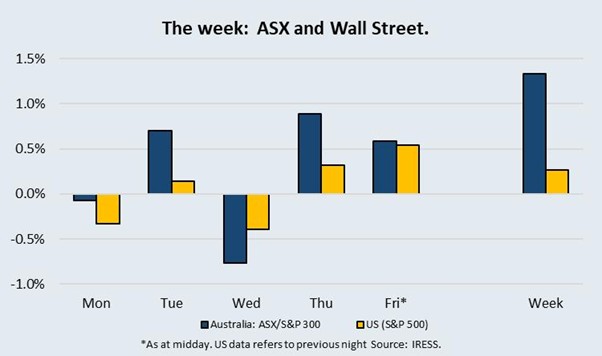

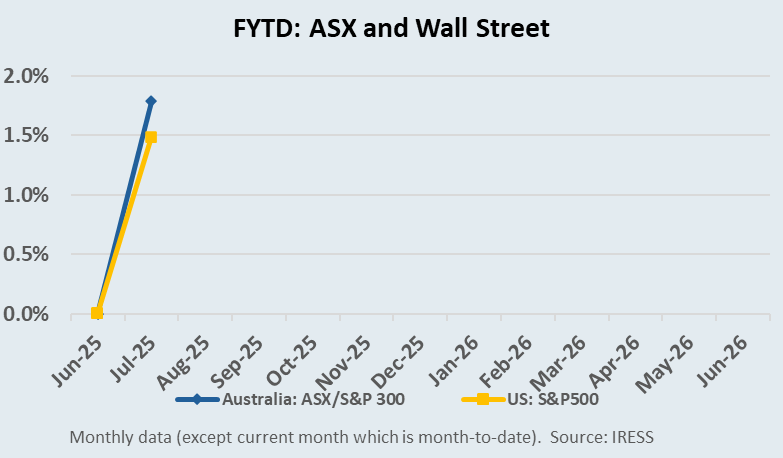

The Market

Introduction

Readers will be familiar with our concerns about the concentration of the ASX 300 index and, in particular, the current representation of CBA as a 12% constituent of the index. Investing 12% of an equity portfolio in a single stock adds undue portfolio risk. Yet the ‘Your Future, Your Super’ regulatory regime, which is having a heavy influence upon Industry Superannuation Fund investment behaviour (in a fight to avoid the scrutiny of being a bottom quartile performer), is effectively mandating this index-hugging approach. Ridiculous.

This week we will review First Samuel’s approach to risk management; examine Australian Equity sub-portfolio’s largest holdings, some of the influences behind our stock selection and each stock’s respective share price performance.

Adjusting for risk and return

So, in contrast to ‘index hugging’ investors, how do we think about sensible risk-adjusted equity portfolio attribution?

There are several factors that we take into account. These factors include the stock’s beta (its correlation with the market), potential alpha generation (the extent to which we expect the stock’s price to appreciate more than the index), and ensuring diversification through industry exposure and different investment themes.

Most client’s Australian Equity sub-portfolios have around 40 stocks. On a simple average, equally weighted basis, and adjusting for approximately 5-10% cash holdings for tactical reasons, this would yield an average stock holding weight of slightly over 2% per stock.

Still, we have higher conviction in some stocks and a core of high-quality names to which we tilt a little higher in our portfolios. These might occupy around 3-4% of our portfolio, with less liquid and more speculative exposures being allocated a smaller holding of around 1-2% to better balance things.

From a portfolio construction perspective, positions of this size enable opportunities to trade around our valuation and provide a significant impact on overall portfolio performance if value is unlocked quickly. In recent years, you may have noticed that companies in the portfolio that are subject to a takeover soon become the largest position in the portfolio. This provides us with an opportunity to sell down circa 25-40% of the holding and still maintain a reasonable position size through the machinations of takeovers. For example, in recent weeks we have seen our position in Santos Limited perform in such a manner.

The final vital issue to note with our most prominent positions is that they often provide significant direct diversification benefits to the portfolio through their size and correlation with other portfolio holdings. This is especially important in mining and financial services, given their high levels of concentration in the ASX 300 index.

Members of the 3-4% club

Each of the following stocks accounts for a weight of between 3% and 4% in our average client’s Australian Equities sub-portfolio. We have included some short notes on a range of these companies in this week’s Investment Matters.

For some companies, recent performance is highlighted; for others, we reintroduce readers to the main themes behind the investment; and for the remainder, attention is warranted due to recent news flow.

Life360 (ASX Code: 360)

Our investment in this emerging technology company has rapidly become our largest portfolio holding. We built our position in late calendar 2024 at around $22 per share. The stock closed at almost $36 at the time of writing.

Life360 operates a family-tracking app that continues to grow its worldwide user base (over 85 million). Researching the company, we quickly identified the factors that appear to drive adoption and believe the company retains enormous tailwinds. At the core, these drivers are the twin effects of increasing social anxiety and a premium on social connectedness at a time when people are less and less confident of their surroundings.

Life360 operates a freemium model, which is a business strategy that offers basic features of a free product or service while charging for more advanced or premium features. This approach aims to attract a large user base with the free version, with the hope of converting some of those users into paying customers for the premium features.

Life360 currently has less than 5% of its users paying for the services, and despite the rates of conversion to paid subscribers rising, it remains very small. Despite this, the company is already profitable.

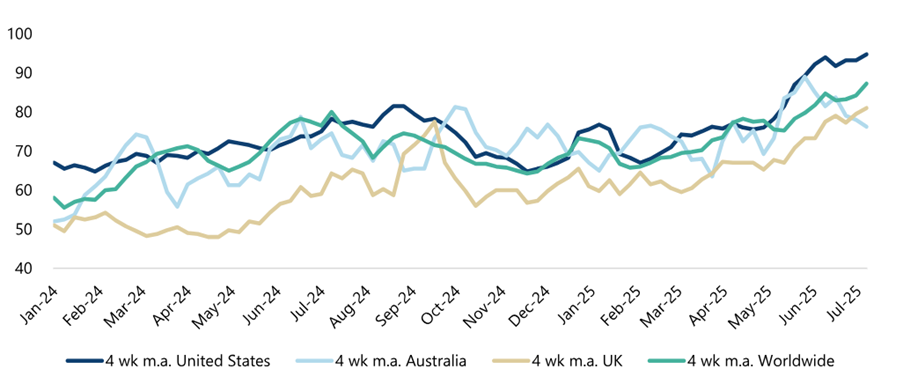

Within the context of already fantastic user numbers, it has been encouraging to see that Google Trends, a data service that measures search interest in products, points to increasing levels of interest in the Life360 product.

Figure 1: Growing Google traffic interest in Life360

Source: Jefferies, Google Trends

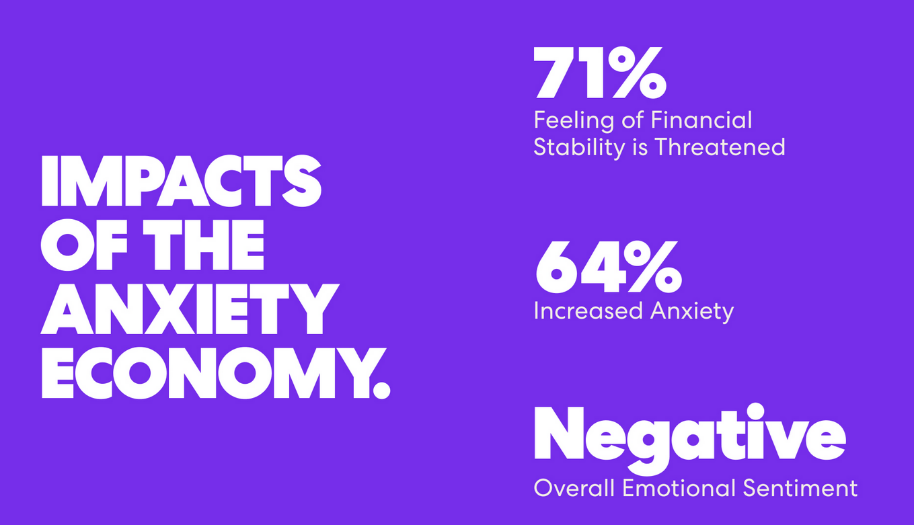

Supporting both the trends shown above and our underlying thesis regarding social anxiety, it was not surprising to see the following research (from Life360, so a grain of salt is required) released this week.

“To better understand how Americans are responding, Life360 conducted a national survey of 1,000 U.S. adults to explore current economic sentiment and spending decisions. The results show a clear emotional undercurrent: 71% of Americans feel economically vulnerable, and two-thirds describe the economy as “uncertain.” That unease is growing; 64% say their anxiety has increased since the start of the year.

While 65% report cutting back on spending, the bigger shift is in how people are choosing to spend. Many are moving their money toward comfort and peace of mind, redefining what counts as essential in today’s economic climate.”

Figure 2: Life360 survey of American consumers shows anxiety

Source: Life360

Life360 notes that the findings point to an emerging trend described as the Anxiety Economy, a shift where people are making emotionally driven trade-offs and holding onto the tools that help them feel safer, more in control, and less anxious.

We consider the combination of demand tailwinds and improved conversion to paid subscriptions as the core drivers of value for our position. However, the most significant upside skew, and the reason we have allowed the position to run higher, is the capacity for Life360 to leverage its connections to drive value as an advertiser and an engine for advertising demand across platforms.

We believe the recent tie up with Uber is a positive development in this respect, leveraging Life360’s position tracking capability and vast user base.

BlueScope Steel (ASX Code: BSL)

BlueScope Steel Limited produces and sells metal-coated and painted steel building products in Australia, China, India, Indonesia, Thailand, Vietnam, Malaysia, and North America. It operates through five segments: North Star BlueScope Steel, Australian Steel Products (think Colorbond), Building Products Asia & North America, Buildings North America, and New Zealand & Pacific Steel.

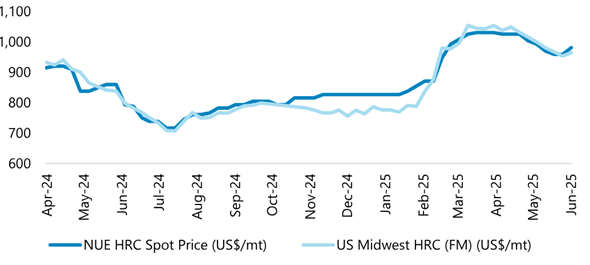

We appreciate the long-term value of the number of strategic assets owned by the company, especially the NorthStar plant in the US. Our current valuation of more than $28 provides significant upside, whilst current conditions see higher prices (Figure 3) and likely improvement in US and Australian domestic steelmaking volumes.

Figure 3: Nucor and Fastmarkets pricing for spot Hot Rolled Coil – FY26 prices significantly higher than FY25

Source: Company reports, Fastmarkets, Jefferies estimates

The share price has recovered more than 25% since the end of calendar 2024 and has continued to improve in FY26.

Interestingly, the Australian Financial Review reported on 15 July that the company has been granted the last right of refusal to the Whyalla Steelworks in SA, which the South Australian Government is in the process of selling. There may be an opportunity for BlueScope to acquire the residual assets from the collapse of Whyalla at a discounted price.

RIO Tinto Limited (ASX Code: RIO)

During the recent period of volatility, First Samuel clients saw their portfolios rotate out of BHP and into Rio Limited. Depending on individual tax considerations, this was executed either late in June or early July.

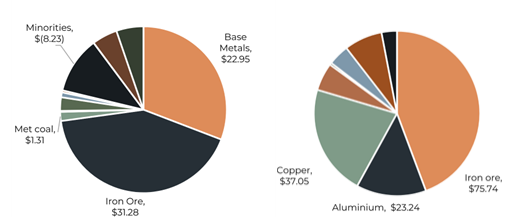

Based on our long-run valuations, we see more upside in RIO than BHP at current levels. In addition to pure valuation, there are six key features that RIO provide more opportunities for upside:

- Increase copper exposure in a range of geographic regions

- More diversified iron ore capacity, including ultra-low-cost production in Australia and new emerging opportunities in Africa. RIO will be bringing Simandou, Africa’s (Guineau) largest resource project iron ore on board later this calendar year.

- RIO has aggressively sought to protect itself from the downside risk in Australian iron ore.

- RIO has exploited downturns in lithium prices to expand its capacity. BHP has failed to diversify

- RIO’s aluminium assets are reasonably priced and tend to perform well in periods of higher inflation

- RIO’s dual listing structure (ASX & UK) is likely to be collapsed in the long term. This may provide opportunities for the franking credits the company generates to be valued higher.

Figure 4: A comparison of Net Present Value – BHP (left) versus RIO (right)

This week, we also saw RIO announce the appointment of a new CEO. Simon Trott, who heads RIO’s Iron Ore business, will assume the CEO role on 25 August, succeeding Jakob Stausholm.

RIO’s Chairman, Dominic Barton, says Trott’s mandate is to unlock “significant value” from the existing portfolio by sharpening the operational performance & lowering costs, while executing the four-pillared future-facing organic growth strategy. We like the approach and agree that execution is the critical issue facing RIO.

Origin Energy

There are many reasons why Origin Energy is a top 10 position in clients’ Australian Shares sub-portfolios, but this week there was media talk (Financial Times and AFR) that has added another string to the bow to the investment case and prompted First Samuel to reconsider its valuation.

Origin Energy is, of course, the integrated Australian utilities company that generates electricity to

sell into the National Electricity Market, and sells electricity, gas and LPG to over 4 million retail and business customers.

In addition, it owns a stake in oil and gas through Origin’s key 27.5% stake in the 9 mtpa APLNG project in Queensland. We see Origin as being core to the energy transformation that will be executed in Australia over the next 20 years, with opportunities for the company to profit across a range of technological and generation types, including gas and renewables.

In recent years, it has become apparent that Origin’s 22.7% equity stake in the UK-based high-growth utility, Octopus Energy was becoming more valuable. Meetings we have had with the Octopus team have only served to reinforce this view.

Part of Octopus Energy’s business is a licensing model for its proprietary ‘Kraken’ operating platform, which it licenses to utilities worldwide. Kraken is a cloud-based customer software platform used by utility companies and has been integrated within Origin’s Octopus-branded energy retailing business in the UK/Europe.

This week, a UK Financial Times article suggested that Kraken Technologies’ business could be valued at up to US$10 billion, which would, if realised, suggest a conservative value for the remainder of Origin’s business at current share prices.

The stock price rose almost 10% on the chance the report is accurate, and any further developments that could prove up such a value for Kraken would add up to 15% to our valuation.

Given the wide range of positive upside factors than Origin Energy retains we suspect it will remain a long-term holding that will only grow its importance to client performance.

Summary

The companies listed above form some of the core holdings in your Australian Equities sub-portfolio. Along with names such as Macquarie Group, QBE Insurance, Reliance Worldwide and Seven Group Holdings, we think these companies underpin a high quality and higher growth foundation from which to seek to deliver above-market investment performance over the next 3-5 years.

The information in this article is of a general nature and does not take into consideration your personal objectives, financial situation or needs. Before acting on any of this information, you should consider whether it is appropriate for your personal circumstances and seek personal financial advice.