Copyright 2026 First Samuel Limited

Read the previous Investment Matters here:

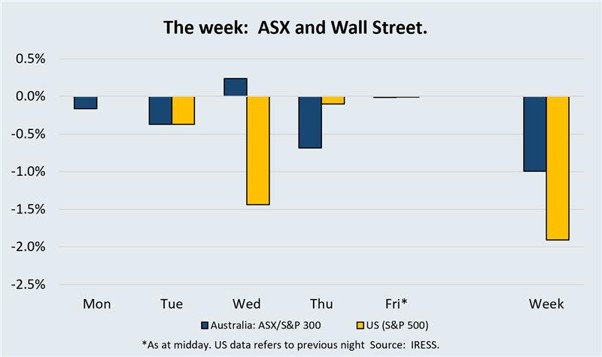

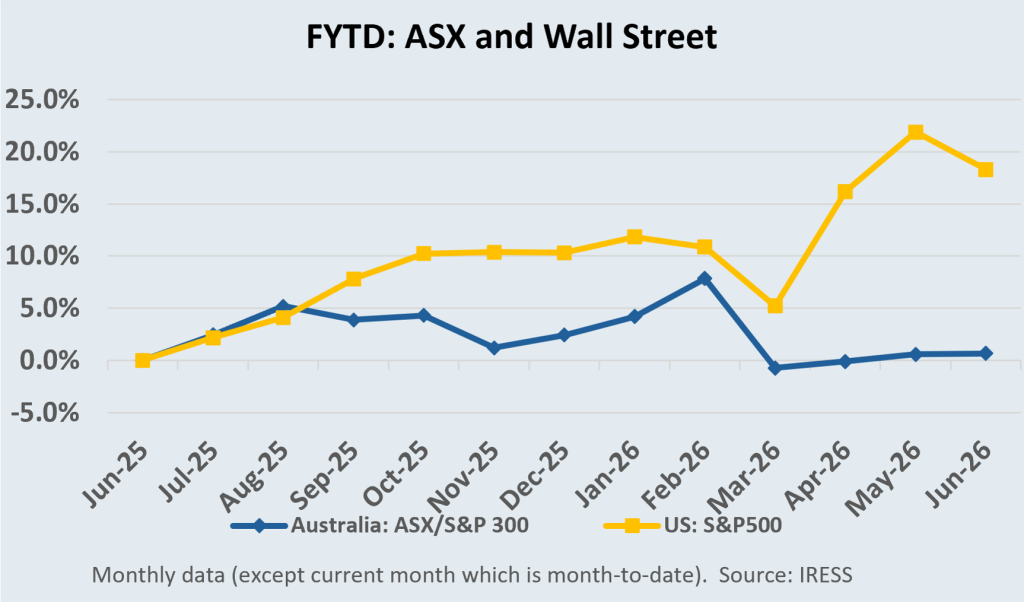

The market

Company news

This week’s Investment Matters is deliberately company focused. There is no need to force a single market theme across four very different company updates. Instead, the value lies in examining what each announcement tells us about the businesses we own, the risks we manage, and the decisions we have made in our portfolios.

Emeco

Emeco’s (EHL) update on 18th June focused on cash flow, balance sheet strength, and the path to higher utilisation.

Metcash

Early in the week, Metcash’s (MTS) FY26 result was defensive, but with more moving parts than a simple food-and-liquor story suggests. We were intrigued by not only their medium-term plans but also the way they are navigating a very complex consumer environment.

Reliance Worldwide

Reliance Worldwide’s (RWC) decision to close Australian brass manufacturing operations earlier this week was a useful, if uncomfortable, case study in why manufacturing capacity moves not only to China but also increasingly to the US.

Judo Capital

Judo Capital’s (JDO) unfortunate update on Thursday was a reminder that credit risk can emerge quickly and that position size must reflect uncertainty.

There is no single conclusion and more about portfolio discipline. We want companies that can adapt to weaker conditions, preserve balance sheet capacity, make rational capital allocation decisions, and avoid exposing clients to risks where the range of outcomes has widened too far.

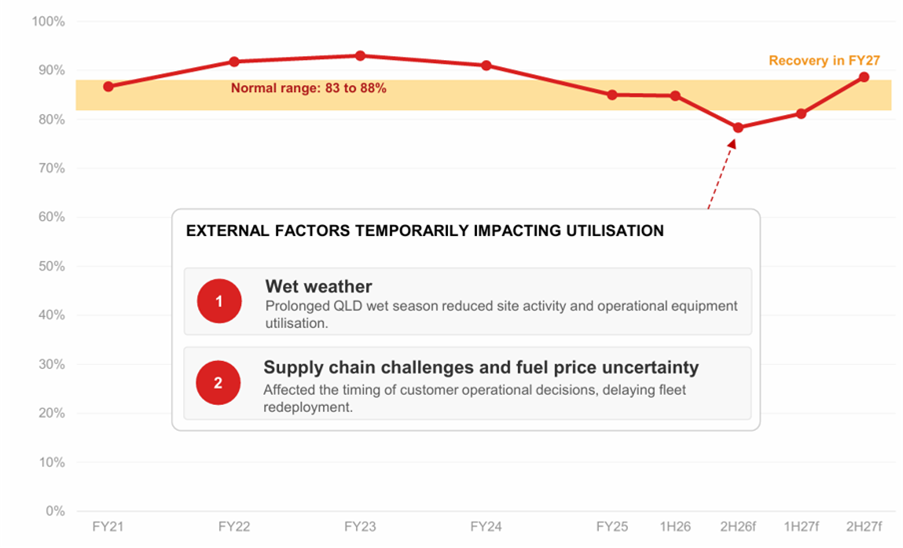

Emeco – Operational Update 18th June

Emeco’s update was softer than expected on the earnings line, but not a simple disappointment.

The company guided to lower near-term earnings as utilisation was affected by wet weather, delayed fleet deployment, supply chain disruptions, and uncertainty around higher fuel costs. In the current global setting, especially since the outbreak of war and the resulting pressure on commodity supply chains, fuel prices, and customer decisions, some slowing in utilisation was unsurprising. We had already expected that near-term earnings could be affected.

The chart below shows the dip in utilisation and the expected recovery into FY27.

Figure #1: Softer equipment utilisation – surface equipment

Source: EHL FY26 Results Presentation

Importantly, the share price had also already reacted. Before the announcement, Emeco’s share price had fallen by more than 30% since the start of the war, reflecting weakening conditions, higher fuel costs and investor caution toward mining services. Despite the war-related weakness, Emeco has been a strong performer in FY26, returning on average over 30%, with profit taking at much higher levels.

While the announcement saw an initial fall in the share price, most of those losses had been recovered by Wednesday this week. The reason is that the update was not simply about lower earnings..

Good cash flow

Emeco also showed good cash flow and better-than-expected leverage. In a cyclical business, balance sheet strength can be the difference between waiting for conditions to improve and using weaker conditions to create value. With the share price trading below Net Tangible Assets, the balance sheet strength provides significant capacity to stimulate growth.

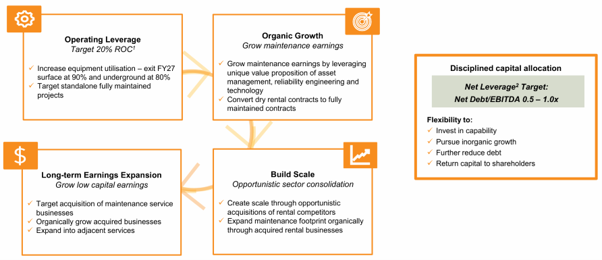

The market appreciates the way in which these elements of growth are forming around a much clearer message that in previous years. The following chart mapped out these options, including an explicit outline of the net leverage target. This target implies significant capacity for new acquisitions.

Figure #2: The Emeco growth model – including leverage targets

Source: EHL Macquarie Presentation June 2026.

Emeco now has several potential ways to use that capacity. The first is the organic redeployment of the existing fleet. If utilisation improves through FY27, the company can lift earnings without needing a major new fleet investment cycle. That is the cleanest path to better returns.

The second is acquisition. Management has previously shown a willingness to pursue M&A when it adds capability, geography, or maintenance revenue. That matters because maintenance and service revenue can reduce the business’s capital intensity. The risk, as always, is that mining services companies can be tempted to buy growth at the wrong point in the cycle. The opportunity is that a stronger balance sheet allows Emeco to act when others cannot.

The third is capital management. A resumption of dividends is possible if cash generation remains strong and leverage stays low. That would help broaden the investment case beyond earnings recovery alone.

For us, the key point is not that FY26 earnings were lower than hoped. It is that cash flow remained strong, leverage was better than expected, and the company still has options.

Emeco’s current share price implies an equity value of only about $500m, despite generating more than $100m in Operating Free Cash Flow (OFCF) after interest, tax, and SIB (stay-in-business) capex. With these cash flow yields and growth options abound, Emeco remains an attractive investment at these levels.

Reliance Worldwide: Manufacturing closure – what does it say about Australia?

Reliance Worldwide’s decision to close brass casting, forging and machining operations in Moorabbin and Braeside is more than a company cost-out announcement. It is also a case study in the economics of manufacturing location.

The company expects about 85 employees to be affected. It will take a large one-off charge, mostly non-cash, but expects an annual earnings benefit by the end of FY27. Production has been shifting away from Australia because the economics have changed. North American production is closer to the largest end market, SharkBite Max, the company’s next-generation push-to-connect plumbing system, designed to join water pipes without soldering, uses less brass per fitting. APAC brass components are increasingly being sourced from third-party vendors in Asia, and the group is also moving more of its product range from brass to stainless steel. That is the company’s explanation. The broader Australian lesson is more uncomfortable.

But this isn’t a story from the pages of the economics textbook.

Pioneered in Moorabbin, now built in US

Reliance Worldwide and its Sharkbite products were pioneered in Moorabbin and have achieved category dominance in the United States. SharkBite has achieved “generic trademark” status customers use the “SharkBite” name to describe the entire category of push-to-connect (PTC) fittings. It is the only plumbing brand of its kind stocked simultaneously by both massive US home improvement retailers, The Home Depot and Lowe’s. The products produced are immensely profitable.

Manufacturing isn’t moving to China or Eastern Europe; the company produces a vast range of products in across the globe. This move is from Melbourne to downtown USA.

Figure #3: Cullman, Alabama – Reliance Worldwide manufacturing site

Source: Google.com

So, where is Cullman, Alabama, and what are the broader implications? As a Melbournian, I set out hoping to find an unattractive location with miserable wages, low-quality housing, poor amenities, and limited prospects. As an investor, I hoped to find a vibrant, moderate-quality location. We found the latter.

Manufacturing location is not decided by sentiment. It is determined by customers, wages, logistics, taxes, housing, energy costs, regulations, suppliers, and the depth of the labour market. On those tests, Cullman, Alabama, has advantages that are difficult for Australia to match.

Within roughly 800 kilometres of Cullman, there are around 150 to 170 million people. That radius includes Atlanta, Nashville, Memphis, Louisville, New Orleans, Charlotte and St Louis. It sits on major logistics corridors and gives manufacturers access to a very large customer base, supplier base and business network within a day’s drive.

Critical location differences

That is very different from manufacturing in Australia. Melbourne’s south-east is a capable industrial region, but it sits inside a much smaller national market. Australia’s entire population is less than 30 million people. A manufacturing site in Alabama can reach several times Australia’s population within a single-day logistics radius. Having said that, Reliance has exported products from these plants for many years.

What has changed? Some things have changed quickly, including tariffs and copper prices. Both dramatically change the equation toward moving away from brass and moving manufacturing onshore in the US. But other issues have changed slowly. The US was once a higher-cost location; today, at least compared with Australia, it is a lower-cost location for the medium-skill positions that Reliance needs.

The table below highlights Cullman as an attractive location with an average US median household income, low crime and moderate housing costs. Your author found adequate golf courses, a couple of nice steak restaurants, and housing costs that would save an Australian family enough to pay for a tribe of children’s houses.

| Cullman, AL | US Non-Metro Average | Broader United States | Moorabbin Local Govt Area | |

| Median Household Income | $55,000 | ~$54,000 | ~$78,000 | $72,000 |

| Violent Crime Rate – per 1,000 resident population | ~1.1 | ~2.0+ | ~3.6 | ~1.2 |

| Property Crime Rate – per 1,000 resident population | ~15.4 | ~13.0-15.0 | ~20.0 | ~6.3 |

| Median House Price – Single Family Home | $250,000 | $165,000 | $400,000 | $850,000 |

| Machinist pay per hour | $21.54 | $21.00 | $25.00 | $30.00 |

All currency is USD. Source: First Samuel

The wage comparison also needs to be understood properly. It is not just the hourly wage rate in Cullman versus southeast Melbourne. It is the cost system behind the wage. If high-quality housing in Cullman can be purchased for around A$500,000, let alone median housing at half the rate, while housing costs in Melbourne are far higher, the required wage to attract and retain workers is different. Housing becomes an industrial competitiveness issue.

This is the point that is often missed in Australian manufacturing debates. We talk about skills, subsidies and sovereign capability. Those things matter. But a country that makes housing expensive, energy uncertain, logistics difficult and labour costly should not be surprised when companies choose to make products closer to their customers in cheaper, larger markets.

Reliance Worldwide is not moving production because it dislikes Australia (I presume). It is moving production because the economics of the product, customer base and cost structure have changed. That is rational for the company. It is less comfortable for Australia. A generation of malinvestment in unproductive assets is now demanding new policies.

Metcash FY26 Results

Metcash’s FY26 result was broadly solid. It remains a defensive business, but the detail is more complicated than the headline suggests.

Metcash is Australia’s leading wholesale distribution business serving food, liquor and hardware. Food was the standout. Earnings rose despite the continuing drag from tobacco, and the business remains the defensive anchor of the group. Liquor continued to gain share in a tough market, a good result given the pressure on consumer spending. Hardware and Tools showed better sales momentum in the second half, but margins remained under pressure.

Value of 3rd level retail

Put simply, Metcash once again demonstrated the value of the 3rd level of retail in Australia – local grocery (IGA), local hardware in Mitre10 and its range of local liquor options. None of the “pillars” is likely to grow at blistering rates, and execution remains the most important corporate challenge. But with Metcash trading at low earnings multiples and generating both good cash flow and decent dividends, the company represents an attractive investment at this point in the cycle.

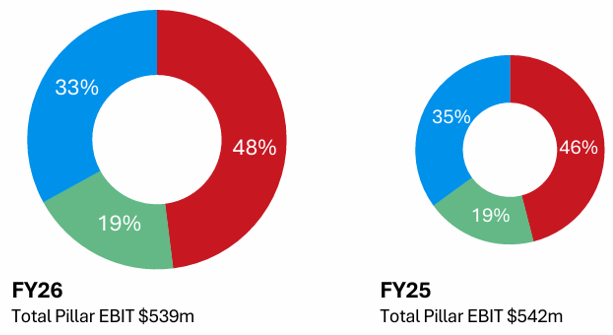

Figure #4: FY26 Metcash Operating Earnings (EBIT) by Pillar (Segment)

Source: FY26 Results Presentation

That mix of pillar profits (EBIT) explains the investment case. The attraction is its resilience, cash flow and dividend yield. The challenge is that each division has its own pressure points.

In Food, the key issue is whether Metcash can continue to protect the IGA network while managing tobacco disruption and competition from Coles and Woolworths. Narrowing the price gap to the majors is useful, but it also requires investment and discipline. In Liquor, the result was respectable because market share gains matter in a soft consumer environment. In Hardware, the sales trend is improving, but the margin recovery still looks gradual. Hardware is the most likely to remain under pressure in our view.

Further purchases of the client network

The most interesting strategic issue is Metcash’s plan to increase ownership of IGA stores. Historically, Metcash has been a wholesaler and network operator, not a major direct owner of supermarkets. Greater retail ownership may help protect the network, improve control and stabilise earnings. But it also changes the business. It increases capital intensity, adds execution risk and raises questions about why some stores need to be owned by Metcash rather than independent retailers.

The logic is that Metcash can use selective store ownership to defend and strengthen the IGA network, rather than simply watching weaker independent retailers disappear or lose share. The economics are not trivial. The company has indicated a willingness to spend $40 million to $60 million per year on store acquisitions, with a longer-term ambition to own stores representing 25% to 30% of IGA network revenue.

If executed well, this could improve network stability, give Metcash more influence over standards, pricing and ranging, and capture retail margin that currently sits outside the group. But it also suggests some independent retailers need support, and it moves Metcash further into operating risk.

More retail ownership can strengthen the network, but it also brings the company closer to the operating risks of retailing. If successful, the strategy will add value; if unsuccessful, it will increase risk and waste capital.

Our view remains that Metcash is a useful defensive holding, particularly in a market where cash flow and dividends are valuable. But the rerating case depends on more than one result. It requires evidence that sales trends are stabilising, Hardware margins can recover, and the move into greater store ownership improves the quality of earnings rather than simply adding complexity.

Judo Capital – credit stress changes the position size

Judo’s update on Thursday was disappointing enough that we reduced our position following the announcement. The extent of selling varied with the client’s tax position and the original purchase price. The stock was hard hit, falling approximately 40%.

Judo has been a very profitable investment for clients overall. The stock was first added to portfolios at around $1.20 per share, and we have taken significant profits over the past year as the share price appreciated. The entire investment case hasn’t failed; the growth of an alternative business lending franchise in the Australian market remains appealing, the latest update introduced too much uncertainty to justify anything more than a relatively small position.

Judo was designed as a proposition for SMEs, implying loans up to $20m. The update surprises the market in that it implied a level of exposure to lending that exceeds this size and carries undue lumpy risk.

The downgrade was material. Judo now expects FY26 profit before tax to be between $163 million and $169 million, compared with previous guidance toward the lower end of $180 million to $190 million. The main driver was asset quality. The company increased specific provisions for three exposures across different sectors: a window manufacturer, a construction business and a financial planning customer. Cost of risk is now expected to be between $116 million and $122 million for FY26, materially above consensus expectations of around $96 million.

Weaker outlook

The FY27 outlook was also weaker than previously implied. Judo now expects FY27 profit before tax of $210 million to $220 million, compared with consensus expectations closer to $254 million. Management noted the uncertain macroeconomic and geopolitical environment, but the market’s concern was more direct: this is what can happen when a lender moves further up the risk curve.

The most concerning feature was the timing. Only six weeks earlier, in the April update, Judo had already increased its expected provisioning. For another material deterioration to emerge so soon after that creates a confidence issue. Management may be right that these exposures are unrelated and not evidence of a broader underwriting problem. But investors do not need to hold the same position size while that question remains unresolved.

Judo is a specialist lender to small and medium-sized businesses. That is the attraction of the model, but also the risk. SME borrowers are exposed to wages, rent, interest rates, weak demand, delayed payments and tighter working capital. When pressure appears, it can move quickly. A short period between updates makes it difficult to know whether this is a contained asset-quality issue or an early warning of broader stress.

Relevance in broader portfolio construction

This is also relevant to our broader portfolio positioning. We have been underweight the major banks, and that position has already been working. We do not want that broader view to be obscured by direct Judo-specific issues. If we are cautious about the domestic economy and banking-sector valuations, then holding too large a position in a specialist SME lender after a credit shock is inconsistent with that caution.

Judo may still have a valuable franchise. The bank has built a strong position in SME lending in a market where the major banks have not always served business customers well. But after this update, the burden of proof has shifted. Until credit quality is clearer, capital preservation matters more than upside.

Conclusion

This week’s company updates did not point in any one direction, but they were useful.

Emeco showed that cash flow and balance sheet capacity can matter more than a short-term earnings downgrade. Reliance Worldwide showed how quickly manufacturing decisions change when customers, costs and logistics point offshore. Judo reminded us that credit risk can emerge suddenly and that position size must change when uncertainty rises. We are concerned that recent policy changes may have a larger impact on a broader range of companies than the markets appreciate.

Metcash showed that defensive earnings remain valuable, but even defensive businesses are becoming more complicated.

The portfolio response is consistent with our broader approach. We want balance sheet strength. We want companies with options. We are cautious about domestic credit risk. We are wary of businesses where higher costs, weak demand or capital intensity can reduce flexibility. And when the facts change, we are prepared to change position sizes.

The information in this article is of a general nature and does not take into consideration your personal objectives, financial situation or needs. Before acting on any of this information, you should consider whether it is appropriate for your personal circumstances and seek personal financial advice.