Copyright 2025 First Samuel Limited

Key Takeaways

- Bapcor reported disappointing FY25 results with a revenue decrease of 1.5% and a drop in NPAT by 8.4%.

- Despite recent shareholder interest, Bapcor’s share price fell by 12% in September, indicating market concerns over its turnaround timeline.

- The management’s guidance suggests a reset is needed, as past operational issues and market conditions pose challenges.

- In contrast, Nib Insurance showed resilience with a 35% return despite a tightened portfolio role due to limited valuation support.

- Lynas and IGO Limited both faced challenges but are positioned for growth with strategic investments and strong underlying assets.

The profit reporting season concluded last week, and we were pleased with the overall market growth and the relative performance of our client portfolios. See this month’s CIO video for more details.

This week’s Investment Matters covers some interesting economic data and results from four portfolio companies: Bapcor, Nib Insurance, Lynas Corporation and IGO Group.

Read the previous week’s Investment Matters.

The Market

Bapcor (BAP): Slow treading?

Despite the market responding with a limited reaction on results day (+1.0%), the company’s share price has been heavily sold off in September (-12%). This is especially disappointing considering the stock has seen additional buying from major shareholder Tannara Capital and members of the Bapcor board.

Key Financial Results of Bapcor

From its FY25 audited results, Bapcor reported:

- Pro-forma revenue of A$1,943.5 million, down ~1.5% year on year.

- Pro forma EBITDA was A$246.7 million, a decline of ~4.1% compared to FY24.

- Pro-forma NPAT (net profit after tax, excluding “significant items”) was A$80.4 million, down ~8.4% on the prior year.

In Investment Matters on August 1st, we provided an update on the market information that Bapcor had shared. The late July downgrade of sales and profit expectations was met poorly by the market, but risks remained leading into the final reported results, released on August 28th. This risk only grew when the company advised the market that its planned presentation would also be delayed until the last possible day to report.

We noted, in August, that our position in Bapcor was a “turnaround”. The result highlighted just how much progress needs to be made by the company in the coming 12-18months. Our view is that management’s guidance for FY25 is a “reset,” cleaning out the financials and establishing a new, more achievable base.

What did the financial results highlight?

Some of the headwinds are accounting-related, and the result is that concerns about additional write-downs may be reduced. There were many asset write-offs, uncollectable receivables, contractual disputes, inventory valuation adjustments, and store-level impairments. Each represents the cost of mistakes made over the past 2-7 years.

Additional challenges were evident in the Retail and New Zealand segments. We felt the disruptions, including consolidation and restructuring costs in the Specialist Wholesale business, were likely to add future value.

The highest value Trade segment performed in line with expectations, with revenue up ~1.3% and EBITDA up 5.4% vs FY24. This segment remains a core cash flow driver when run well. Improved cash conversion was seen across the business, up to ~81.8% (from ~76.9%) due to disciplined working capital management. This improvement needs to be delivered repeatedly before we get too excited about its sustainability.

We suspect the ongoing poor market response is mainly due to the extended time period over which improvements in Bapcor are likely to be achieved. A deteriorating retail environment (especially discretionary auto accessories, etc.) and increased competitive pressures when missed with operational disruptions aren’t likely to be smooth sailing over the next 12 months.

Critically, however, we believe that this is more than reflected in the price, and at a time when the market is generally expensive, a good portfolio should have a small number of turnaround positions such as Bapcor.

As we noted in August, in June 2024, Bapcor received a takeover proposal from Bain Capital, one of the world’s largest private equity firms. Bain offered $5.40 per share—a substantial premium to where the stock was trading at the time, valuing Bapcor at over $1.8 billion. After due diligence, the bid was ultimately withdrawn in July, reportedly due to further trading softness and boardroom instability. The approach continues to underscore the strategic value and latent quality of Bapcor’s assets, in our view.

Conclusion

Our conclusion regarding this position is unchanged since early August. Bapcor remains a high-conviction turnaround for us, aligning with Peter Lynch’s view that a few well-chosen recovery stories can add meaningful upside to a quality portfolio. The recent reset presents both risk and opportunity, and we remain patient as new management works to restore growth and confidence.

Central to our view is the stable of brands (see figure 1) and the almost $2bn of sales the business generates.

Figure 1: Stable of quality brands in auto repairs and maintenance

Source: FY25 Bap Results Presentation

Nib Insurance (NHF): Delivering healthy outcomes

Nib Insurance (NHF) delivered its FY25 results on 25 August. The share price rose dramatically upon the announcement (+8%) but ultimately settled only 2% ahead on the day. Since the result, the stock has traded down another 5%.

We now only see limited valuation support in the NHF share price; consequently, we see a much smaller role for NHF in the portfolio. We sold most of our position into the strength first seen post results. We would be keen to purchase more should the share price once again over-discount earnings in this high-quality business.

Given our initial purchase price in the high $5 range in October 2024, we have been very pleased with the more than 35 per cent return for our position.

Concerns from late 2024 proved unfounded

With almost 20 years of fantastic operational performance, the market was surprised in 2024 by ongoing weakness in several NHF’s satellite businesses, and weak outcomes in New Zealand, which could have been managed better in our view.

There were additional concerns regarding the political environment and the outlook for premium rate increases in Australia during an election year (2025).

Since October 2024, the government has delivered sustainable increases in premiums, regulatory changes have driven no additional imposts, and NHF has continued to grow its member numbers faster than the market (Figure 2 below).

Figure 2: Our investment thesis highlighted NIB’s long track record of outgrowing system member number growth

Source: FY25 NHF Results Presentation

As a result, NHF had, by June, returned to record profitability (Figure 3 below), and despite significant political pressure to understate future profitability, its outlook into FY26 remains strong. There has even been some improvement in the satellite businesses that have been a drain on earnings in recent years.

Adjacent businesses contributed $45.3m of underlying operating profit and continued to scale services that reinforce the insurance franchises. Nib Thrive processed 3.4 million NDIS claims worth $2.5bn for 43,000+ participants; Honeysuckle Health and Midnight Health combined for $70.2m in gross revenue (+51.6% y/y) and supported over 121,000 customers through wellbeing experiences and telehealth programs.

Figure 3: NHF has now returned to record profitability

Source: Barrenjoey Research

It would be tempting to retain the NHF position at its larger portfolio share; however, ultimately, a range of sector risks exists despite the strength of NIB Insurance itself. Clearly, Australians as consumers, and Australian politicians and health policy experts, have a love-hate relationship with private health insurance.

A necessary evil or a positive consumer choice outcome that supports the health industry – we all have our views over the long run. What is critical for investing in the industry is assessing the balance of risks. At this stage, with the rolling failure of Healthscope, limited success in not-for-profit health funds, and a quickly growing and aging population, speed bumps are possible in general.

We suspect that adding politics on top of these risks only magnifies the risks.

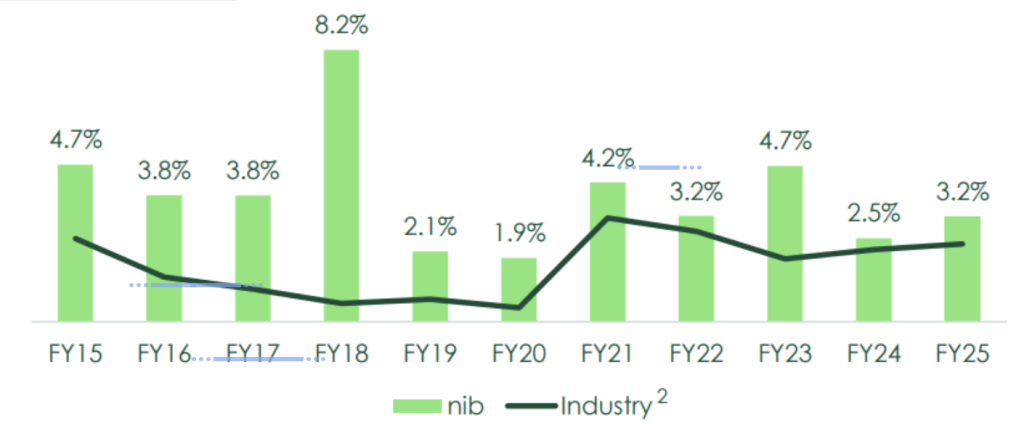

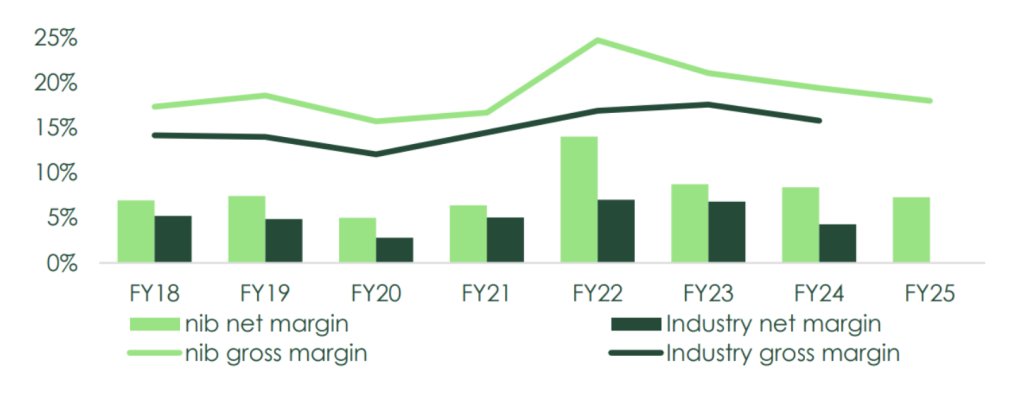

Figure 4: The health insurance industry is experiencing declining margins – although nib continues to outperform

Source: FY25 NHF Results Presentation

As the figure above shows, the industry margins are falling, and arguably, nib insurance is overearning. Will the government, at some point, reassess profitability with a keener eye on individual health fund returns?

We suggest that at the high $7 range, the NHF share price is high if the risks of government action on future rate increases or regulatory changes are evenly balanced. The NHF share price would still be a good value if we assumed that the government is unlikely to regulate returns.

Lynas Corporation (LYC): Success and capital raising

Lynas reported its FY25 results on 28 August, and at the same time announced a $750m equity raising at a 10% discount to the share price. The share price fell by around 6% when trading recommenced following the successful capital raising. Lynas has continued to increase in September (+3%).

The key feature of this company is its continued improvement in its global strategic value. Readers may recall that we have a set of 10 core investment thematics that help define our portfolios. Lynas qualifies for a remarkable six of thematics in one company. The six are Strategic Assets, Decarbonization, Superior Market Position, Demand driven by Technology Change, Growth, and Globally Significant.

Since June 30th, each theme has been strengthened, and the stock price has produced a return of +75% for clients in this short period. We have lightened our position prior to the equity raising.

Lynas is positively engaging with key governments on appropriate mechanisms to benefit all industry participants, including the Australian government’s Critical Minerals Strategic Reserve. As the only current non-China commercial producer of separated Light and Heavy Rare Earth oxides, governments around the world recognise Lynas as an industry leader.

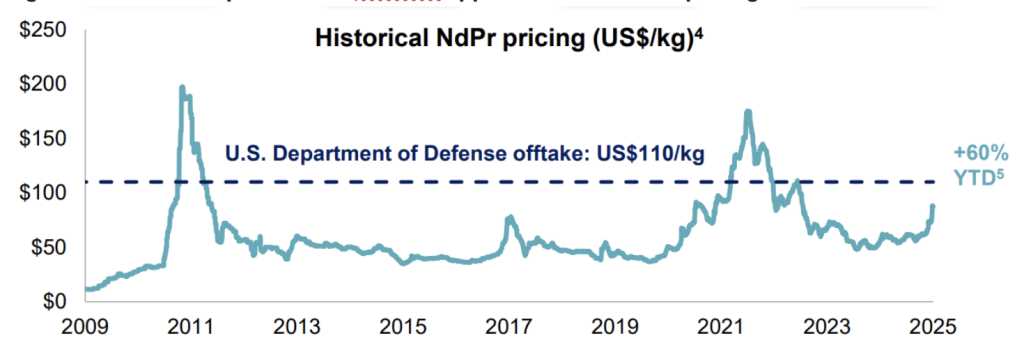

The decision of the US Department of Defence to underwrite pricing at $110 kg for a closely related competitor has increased market confidence in the future of Lynas. This is despite the volatility of NdPr (rare earths) pricing since 2008 (see below figure #5) and the large amount of investment still required for Lynas to achieve all its objectives.

Figure 5: The US Department of Defence appears to underwrite pricing

Key Financial Results

Lynas’ revenue rose to A$556.5m for the full year ended 30 June 2025, up from A$463.3m the prior year. However, EBITDA fell from roughly A$132m in FY24 to A$101m in FY25.

Lynas Rare Earths CEO and Managing Director, Amanda Lacaze, commented:

“It is exciting to see the investments made over the past five years as part of our Lynas 2025 growth plan come to fruition this year. In Australia, this includes the Mt Weld expansion project and fully integrating the Kalgoorlie Processing Facility into Lynas’ global operations. In Malaysia, significant upgrades have delivered new processes and products, including our first separated Heavy Rare Earth oxides, establishing Lynas as the only commercial producer of these products outside China. As the various projects were brought into operation, production of NdPr increased, and record production was achieved in the June quarter.”

The only downside was a weaker-than-expected outlook for the construction of the US production facility. We have been aware of additional funding requirements and changing economics for the project; however, we had assumed a higher probability of success than intimated by management in the commentary provided.

Towards 2030: Strategy and capital raising

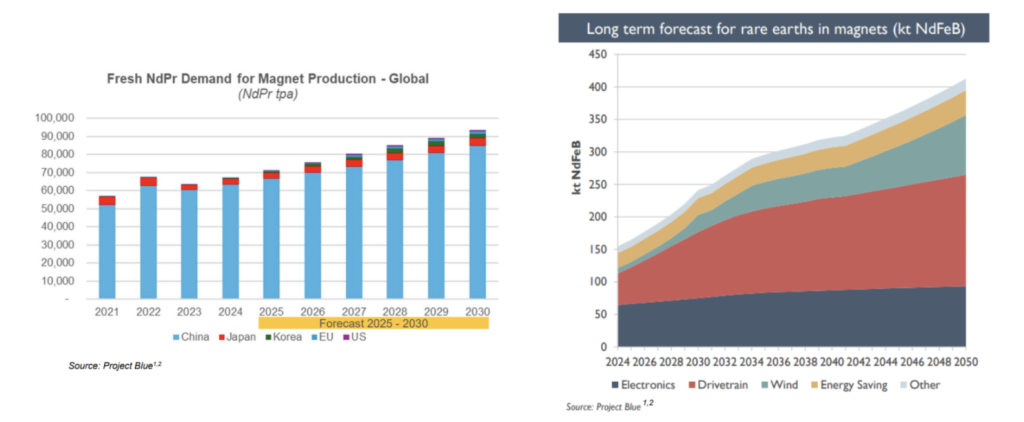

As noted, the company undertook a significant capital raising following the sharp rise in the Lynas share price in recent months. The confidence the company has in investing so heavily relates to the future forecast growth in magnet demand. The figure below was included in the result presentation and shows just how much demand is possible. Given the paucity of supply ex-China, such a forecast is bullish for Lynas’ future sales growth.

Figure 6: Lynas Corporation: Forecast growth drivers for Rare Earths include magnets

What is Lynas Corporation planning to spend the $750m on?

Add Resource and Scale

- Develop Mt Weld further with the objective to produce higher-grade NdPr concentrate

- Continue exploration and mine plan optimisation at Mt Weld, and add new feedstock sources

Increase Downstream capacity

- Expand Heavy Rare Earth separation capacity, and broaden product range in Malaysia

- Develop value-added specialty rare earth manufacturing capability

- Expand NdPr separation and the outside China metal and magnet supply chain

- Partner with companies that have proven expertise in rare earth metal and magnet production

If Lynas can execute operationally — ramping up new facilities, delivering downstream expansion, securing offtakes (especially in the U.S.) — then the raise should be value-accretive, though the dilution effect and risk of execution missteps will likely remain prominent concerns.

Conclusion

Lynas remains a core, albeit relatively small, long-term position. We are conscious that despite the range of possible positive developments and value accretive investments, Lynas is highly capitalised for its existing asset base. Ultimately, this high price limits the size of the position; however, as we have shown in the past two years, should the opportunity to add to the position at lower levels arise, we would do so.

IGO Limited (IGO): Ta

In late August 2025, IGO released its full-year financial results for the 12 months ending 30 June 2025.

Globally, lithium stocks have been a rollercoaster ride, driven by changes in the Chinese market.

| Month | Price Change since June 30th 2025 |

| May | -1% |

| June | +7% |

| July | +6% |

| August | +18% |

| September | -18% |

What happened to drive such volatility?

In early August, one of the world’s largest lithium battery producers, CATL, closed its Jianxiawo Mine due to an expired mining license. This mine contributed nearly 8% of the global lithium supply. The suspension triggered a sharp rise in lithium carbonate prices. Lithium prices in China have become highly sensitive to any supply disruptions.

The mine closure occurred at the same time as China continues to roll out stricter regulatory oversight for lithium mining. Recent reforms under the revised Mineral Resources Law now recognise lithium as a strategic mineral, a similar status is used in Australia and the US. Chinese authorities are also pushing to eliminate “vicious competition” and overcapacity—encouraging consolidation and enforcing mine environmental standards.

Analysts who specialise in lithium suggest these shifts indicate a strategic move away from scale-at-all-costs toward more controlled, resilient development of lithium capacities.

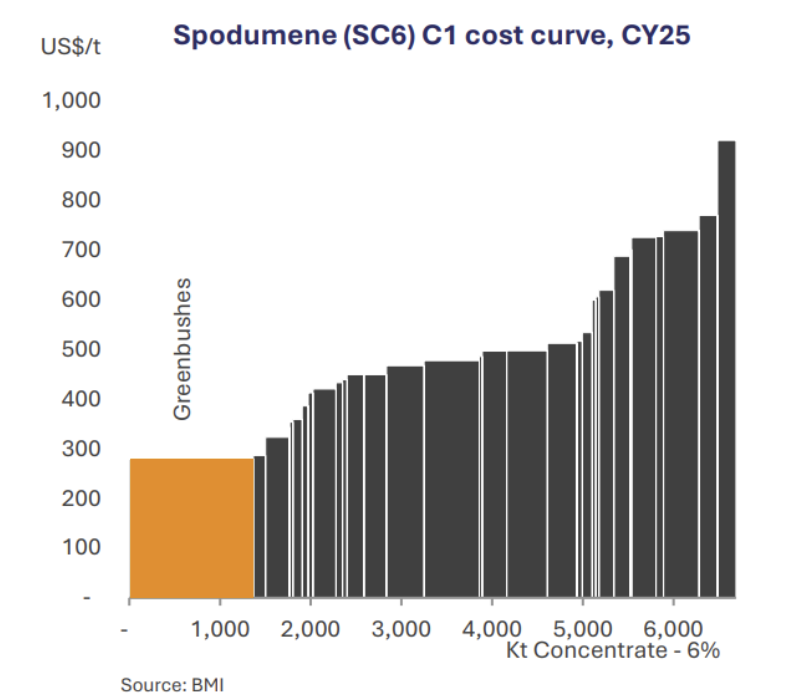

Such changes would be incredibly important for IGO, which already has the world’s cheapest production (see figure # below). Should global supply chains bifurcate into a China supply chain and an ex-China supply chain, stricter controls would only add to future profits for IGO.

Bifurcation would also improve the economics of the Kwinana facility, which was heavily written down in the recent result and given little value by the market at current share prices.

Key Financial Results

The financial result for IGO was not great, but likely no worse than expectations—a range of weaker operational outcomes, combined with many non-cash write-downs of the company’s assets.

- IGO’s total revenue plunged to A$528m, down a significant 37% from FY24’s A$841m

- Underlying EBITDA swung from a solid A$581m profit in FY24 to an A$43m loss in FY25.

- Including the non-cash items, and in line with expectations, the accounting profit was a massive A$955m loss after tax.

- Free cash flow wasn’t great either, and the company outlined higher anticipated closing costs for a number of mines due to close in the future.

The long-term value of the business, however, changed by very little, and it is almost certainly contained in the current share price. Why?

Because the value of IGO is primarily driven by its stake (25%) in the world’s best lithium mine in WA called Greenbushes/. Additional future value lies in its currently underperforming downstream processing facility at Kwinana.

Figure 7: IGO’s Greenbushes is the lowest cost spodumene mine in the world

Source: FY25 CWY Results Presentation

Greenbushes generated strong margins: full year spodumene (lithium precursor) production of ~1,479 kt, a unit cost of A$325, and an EBITDA margin of 66%. The mine produced an enormous amount of profits despite weak global prices, with operating cash flow from Greenbushes reaching A$1.5bn on a 100% basis.

Conclusion

IGO’s FY25 result franks our investment thesis in stark relief, despite the dramatic impairments and weak but volatile lithium prices, the underlying lithium business—particularly Greenbushes—remains strong and cash-generative.

Armed with the strategy outlined in Figure 8 below, IGO is well placed to make the most of its options and opportunities.

Figure 8: IGO’s Greenbushes is the lowest cost spodumene mine in the world

Source: FY25 IGO Results Presentation

The movements in lithium prices and changes in China provide us with further evidence that there are many future scenarios of both supply and demand in which IGO’s strategic assets are once again worth a multiple of today’s share price.

The information in this article is of a general nature and does not take into consideration your personal objectives, financial situation or needs. Before acting on any of this information, you should consider whether it is appropriate for your personal circumstances and seek personal financial advice.