Read the previous week’s Investment Matters.

Photo © Bambambu from Via Canva.com

Copyright 2025 First Samuel Limited

Clients have appreciated the strong growth in the Aurelia Metals’ share price over the past couple of years. FY25 YTD, the stock is up more than 50% after doubling in FY24. Aurelia’s share price was above 30c this week, and we have trimmed the position slightly in recent weeks.

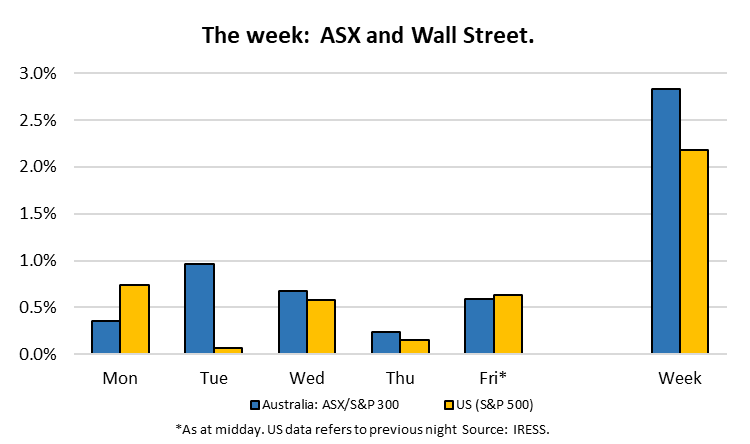

The Market

Aurelia Metals – a deep dive

Aurelia Metals is a polymetallic mining company based in the Cobar region of western New South Wales.

After a rocky FY22, subpar acquisition, and finally a change in leadership, we were fortunate to participate in a company-defining capital raise in May 2023, for $0.09 per share.

The fruit of the leadership change and the mixture of company assets have continued to bear fruit. Investment Matters this week will highlight some key features of the company, showcasing some of the characteristics of our investment style.

That is not to say the investment in Aurelia Metals hasn’t been without its stumbling blocks. At the end of FY22, our position had cost an average of 40c per share, and the stock was trading at 25c per share. A poor result indeed. Problems with a bolt-on acquisition were becoming apparent, and the capacity to fund future options was diminishing.

Figure 1: Aurelia Metals – average monthly share price since June 2022

Source: IRESS, First Samuel

The dilemma was a set of assets worth closer to 50c per share, but likely only realised after a potentially dilutive capital raising that could take 1-2 years to complete, and only if ASX market conditions and commodity prices were favourable. The additional complication was a management team that had made errors and lost the market’s confidence.

One of our core investment tenets is…

to purchase great assets that can survive poor management, as poor management can always be replaced or the entire company acquired

… was put to the test. As was our patience. The stock continued to sell off through fiscal 2023.

New management, led by Bryan Quinn (a 27-year veteran of BHP), was introduced at the same time as the capital raise at the end of fiscal 2023. As part of this raise, we significantly expanded our position.

With funding in place and options plentiful in late calendar 2023, significant execution risk remained, along with numerous strategic decisions still to be made. Ongoing discussion with the leadership team provided us with confidence in their understanding of the underlying value. They were also able to clearly outline the steps that needed to be completed and the order in which they needed to be done.

The market doesn’t generally appreciate miners that are undertaking mine development, the risks associated with building mines and the often-experienced cost overruns tend to weigh on stock prices. Patience was required in 2024.

We covered the risks of missing value due to Aurelia becoming a victim of an underpriced takeover bid. Clients acquired a small stake in Metals Acquisition Corporation, Aurelias’ likely acquirer and co-located Cobar copper miner.

Background on value and strategic priorities?

Critical to an understanding of Aurelia Metals is appreciating the area it mines, a mineralised strike zone extending more than 150kms through Cobar from north of the town of Cobar, SW past Nymagee. Aurelia owns mining tenements that cover a large part of the zone, but exclude the prolific CSA mine to the north, owned by Metal Acquisition Corporation (MAC). Aurelia’s Peak mine has been operating since 1896.

Figure 2: Cobar region – Aurelia assets and other opportunities

Source: Aurelia Company reports

The Peak mine area has, through the decades, exploited deep veins of mineralisation that continue to extend underground. Limited only by technology, ongoing exploration appetite, mining costs, and prevailing commodity prices, the company, in each of its forms for more than a century, has drilled and extended a variety of individual mines. Many modern mines were simply an extension of work by miners a century before, literally “only scratching the surface.”

Mines called Great Cobar, Perservence, Peak, New Occidental, Chesney, Jubilee are all examples of mines that still, or have done in the past, extend vertically deep into the earth from various locations along a strike zone south of Cobar of barely 10kms in length.

On the surface, Aurelia has utilised more centralised processing capacity, which itself has been expanded and developed over the decades for different capacities and different abundances of metals mined below. There are areas surrounding Peak rich in gold, others in copper and others in lead-zinc.

The task for great management is to optimise mining within those mines already developed, and then carefully invest in the mine development and exploration along the length of the mineralised zone.

The next Chesney or New Cobar awaits future development.

Further afield, surrounding the Peak Mine, past activities at Aurelia included the development of the Hera processing facilities, which were used to mine gold until recently. The new Federation mine, now completed and expected to commence commercial production imminently, lies south of the existing Hera infrastructure. One of the tasks of the current management was to optimise how the ore from Federation would be processed. In the end, the best solution will see the ore trucked all the way to the Peak Mine processing plant in Cobar (more than 80kms).

Federation Mine

Aurelia recently reported that “The Federation project has minimal activities to complete, with an upgrade to the mobile maintenance workshop planned for Q4 FY25, finalisation of the operational readiness programs, and then handover to management. Additionally, optimisation of power station efficiencies and completion of the highway intersection construction works in Q1 FY26 for the Kidman Highway are scheduled. The majority of the project team have now commenced demobilisation.”

The project commenced following the successful capital raising in 2023, which was completed on plan and the funding for its development proved a great success. Seeing the benefit of this investment in cashflows in FY26 is part of the reasons for the recent improvement in sentiment towards the stock.

The importance of the Federation project can be seen in the Figure below. The left-hand chart shows in yellow the proportion of future (FY26 and FY26) production attributable to Federation.

Figure 3: Historic and Forecast Production by Mine (LHS) and by metal (RHS)

Great Cobar Project

In recent weeks, Aurelia was able to announce the approval of the Great Cobar project. As a longtime investor in this company, and after reviewing historic mine plans for more than a decade, we have always been excited about the Great Cobar opportunity.

The difficulty in developing the Great Cobar opportunity previously lay mainly in the sequencing of the project amidst capital constraints. Although delayed we appreciated the work done by the new management team to exploring better ways of developing Great Cobar as compared to previous attempts. The value uplift has been considerable.

With a strong balance sheet and the completion of Federation, the development of Great Cobar is possible. Despite a capital cost for the project of +$90m over 3 years (against a market cap of circa $400m pre-announcement) the company now expect to have the capacity to start this project.

At long-term price the project added more than 15% to our valuation (largely already included). Even more promising for the companies that the project anticipates profits of more than twice that amount at current prevailing, or “spot,” prices.

The figure below shows that the Great Cobar project is itself built underneath historic working in the areas, and will be access by a twin-decline (tunnel) from existing operation in the New Cobar mine to the south (left) of the project. We expect the green area on the chart to continue to expand upon further drilling in future years.

Figure 4: Local area map of the mining opportunity at Great Cobar

What does the position offer to the portfolio?

Aurelia Metals offers clients’ Australian Equity sub-portfolios five features that we appreciate from both the company’s perspective and as an individual investment, as well as the characteristics it brings to the overall portfolio. The Aurelia holding represents:

- Part of the Gold basket, which includes Catalyst Metals, De Grey Mining and Newmont Mining. With more than 50% of Aurelia’s FY25 revenue sourced from gold, the rise in the gold price has been a significant contributor to the stock’s performance. The long-run share of Aurelia’s total value across its various mine attributable to gold is more than 25%, and could be greater at current prices for gold and the Australian dollar.

- Part of our Copper basket, which also includes Sandfire Metals and Metals Acquisition Corporation. More than one-third of Aurelia’s value is due to its copper exposure, and this embedded value is likely to grow as a percentage over time as non-gold assets are exhausted.

- Our key exposure to Base Metals, especially lead and zinc. Owning an efficient base metals miner with support from Copper and Gold credits is very attractive as it reduces the volatility that can sometimes impact pure base metals miners in high-cost jurisdictions, such as Australia. Other base metals exposure is contained in Develop Global.

- A company with a strong free cash flow yield. The company is forecast to generate a free cash flow yield of over 15% in 2026, making it one of the most attractive positions in the portfolio.

- Attractive level of optionality (scenarios in which further value is unlocked) the company still retains. There are three clear sources of this optionality:

- Regional M&A opportunities that leverage the company’s balance sheet and underutilised processing plants

- Additional exploration drilling opportunities close to the Peak mine in areas which have been consistently drilled and mined for more than 150 years.

- New opportunities to develop partly explored areas surrounding the mothballed Hera processing plant, including the Nymagee discovery.

What does Aurelia produce?

In the interest of explaining what owning a polymetallic miner means, we can seek out a definition such as “polymetallic ores are complex ores containing several chemical elements, among which the most important are lead and zinc”.

Or we can simply show what the decomposition of revenue looks like for a miner such as Aurelia Metals at current prices.

The cost of producing the ore is a function of the tonnes of processed material. Still, because the components have such variation in their value, and each material’s price is subject to variation, the composition of revenue can change a lot over time. Efficient mining and great processing (scale and volume of ore processed) are critical. At current prices, the 40- 50k oz (or 1 tonne) of gold is worth half of the expected revenue, whereas the 13,000 to 19,000 tonnes of lead is only worth 12% of revenue, the same as copper which weighs a fraction of the lead.

Figure 5: Value of current production by metal type

Funding for growth now secured

The company secured a minimum level of funding to begin its growth capex program in 2023, including the significant task of building the Federation mine in 2023. Since that time, the task, and hence the risks around not being able to complete development without additional capital raising has been made easier through strong operational outcomes at its Peak and Hera mines.

Over the past six months, we have seen a fabulous outcome, whereby the entire amount of growth capex was effectively funded by other mine operations. In the 1H25 result reported in February, the mining operation provided positive cash flows of $45m, and growth capital expenditure plus exploration only totalled $41m despite the intensive development at Federation and exploration drilling across many Aurelia assets.

The ability to fund growth through existing operations significantly improved the Aurelia balance sheet, with almost $100m in cash on hand and additional liquidity available. Cash alone is worth $0.06 per share.

Regional optionality

The stronger balance sheet, especially following the post-Federation cash flows in FY26, can now explore options, including Great Cobar, the restart of Hera, and the development of the Nymagee mine. Nymagee was a growth option for the company more than a decade ago.

We suspect that, given the optimisation of regional production assets now at Peak, developing the Nymagee mine may prove a viable option. If such a development could be combined with corporate M&A opportunities involving other miners in the region that lack processing capabilities, the upside could be considerable and move the company forward as a genuine consolidator of regional assets.

Summary

Strong management combined with great assets has realised value from this long-held portfolio position. Further upside remains, and the stock plays an important role in clients’ Australian Equities sub-portfolio.

Given the inherent volatility of mining of this type, the Aurelia position is unlikely to be the largest in a diversified portfolio, regardless of the price; however, with options remaining plentiful, Aurelia is likely to remain a core medium sized holding into the future.

The information in this article is of a general nature and does not take into consideration your personal objectives, financial situation or needs. Before acting on any of this information, you should consider whether it is appropriate for your personal circumstances and seek personal financial advice.