Read the previous week’s Investment matters.

Photo © alexlmx from Via Canva.com

Copyright 2025 First Samuel Limited

The Market

The past week of Trump tariffs

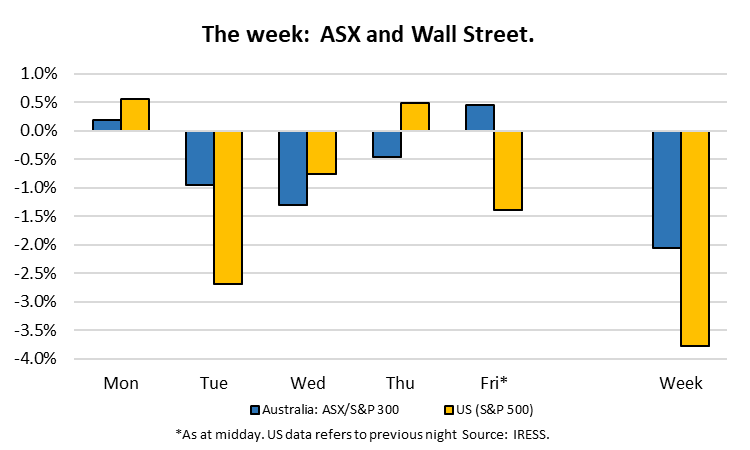

During the past week, Trump tariff uncertainty and mixed economic data created further angst in global markets. Circumstances in which uncertainty increases are almost always associated with lower equity prices.

US markets, including the S&P500 (down 7%) and Nasdaq (down 8%) have borne the brunt of the impact over the past fortnight. The Australian market has performed slightly better, down 5%. First Samuel clients did better still, depending on risk preferences. Clients should review the CIO’s upcoming and special video.

The key for long-term investors is to parse the trends changes (if any) that arise from these periods, knowing that uncertainty itself will almost certainly pass. With reducing uncertainty, share prices rise again.

The trend changes we are observing, and have noticed since the beginning of calendar 2025, are nonetheless important. There were three significant changes:

- Unwinding of the momentum in large capitalisation companies, globally. This includes “magnificent seven” tech names in the US; e.g. Tesla (-37%), Nvidia (-16%) and Google (-14%).

- In Australia: a relative switch away from the expensive Big 4 banks and other financials (-7%) and towards mining companies (-1%).

- Increased appreciation of ‘value’ companies with favourable cash flow yield and asset backing characteristics.

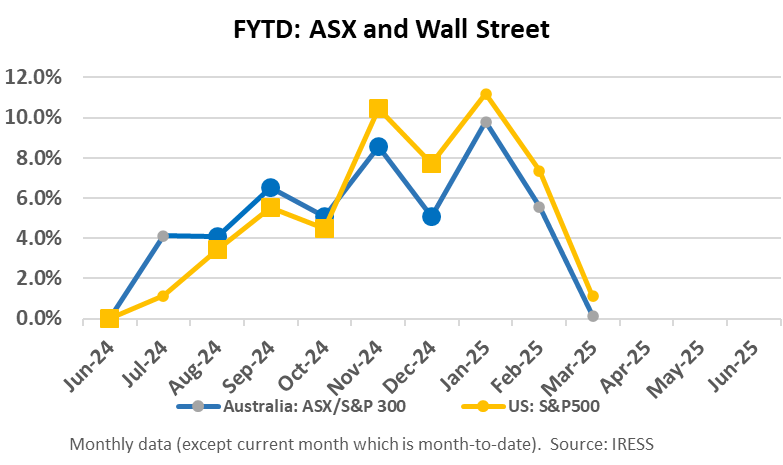

First Samuel clients have benefited from these trends, having limited exposure to the high momentum expensive components of the market. Despite the market (ASX300) falling more than 4% since 1st January, our clients have, on average, benefited from modest increases in the value of their Australian equities sub-portfolios over the same period.1

1 The outperformance noted (above) includes the impact of the loss in value of Innovate Access Group; see more below.

Reporting season

Investment Matters in March will concentrate on reporting on sub-portfolio companies that were not covered in detail in previous weeks. This week, we will highlight the results for Judo Bank and Life 360.

We also provide some background to the write-down of our investment in Innovate Access Group (effective late February).

Judo Bank

Judo Bank is a relationship-focussed business bank supplying capital to small and medium-sized businesses across Australia.

Judo has been a terrific story – representing a well-defined strategy as well as focused execution. In the past 12 months, it has rewarded shareholders with a continued improvement in business returns as well as the share price, which has doubled from its lows reached in late calendar 2023.

Judo delivered its 1HFY25 result on the 18th February.

We viewed the result as “positive” and the stock price rallied 8% on the day but its share price has retraced 5% per cent since the result, marginally better than the market as a whole.

More in the (share price) tank?

Despite the share price doubling from its lows, we perceive that there remains upside in the share price. The keys to business and share price success will be achievement of Judo’s ‘a scale’ profit metrics:

- Continued growth in lending and deposits

As the Australian economy rebalances away from being so heavily consumer-led towards more investment and business-driven, business credit is expanding at a faster pace than household credit. This has been the driving force behind major bank profitability in the past two to three decades. With only a 2% lending market share and expanding relationship banker and broker distribution capability, there remains plenty of scope for the bank to grow its balance sheet and build the necessary scale.

- Ongoing net-interest margin improvement to > 3%

The run-rate of Judo’s Net Interest Margin (the difference in the rate between (a) what the bank charges on its loans and earns on Treasury securities and (b) what it pays to deposit holders, bond investors and its equity capital) was tracking at close to 3% again in 1H25.

There remains further scope for upside based upon;

2H25 tailwinds from lending margins, funding mix and liquidity

Source: Company reports

- Improved cost efficiency, as scale is reached

The bank has largely built-out its corporate centre and moved its lending to a contemporary core banking platform (Thought Machine). The business can grow with minimal incremental expense. The aim being a Cost-to-Income ratio at a very competitive level, approaching 30% (versus major banks at ~45-50%).

- Equity capital efficiency

The bank is now able to target modest reductions in the proportion of equity capital it requires to run the business.

Implications of ‘at scale’ metrics for returns and share price?

Meeting this combination of factors in the next 2-3 years should see Judo Bank achieve a return on equity in the 12-15% range. This is competitive with the best of the Australian major banks and comfortably above its cost of capital.

At that level of profitability, we expect that the business can trade at a share price more than $3 per share (currently $1.86). Such an outcome is not guaranteed, but on a probability-adjusted basis there remains significant upside in the share price, much of which could be achieved over the next 12 months

Life 360…. Where are Fido and Fifi?

For those not familiar, Life 360 is a technology company that provides phone applications as well as devices (think Tile) to connect and keep families, friends and even pets safe via location data.

It is the largest platform of its kind in the market and is device-agnostic, being able to be used by people across both Apple and Android phone systems. This gives it a competitive advantage against its largest competitors/threats. Its biggest user base is in the US, where the majority of its 80 million users are located.

The business was listed first in Australia (360.ASX) and in 2024 also became dual-listed on the Nasdaq exchange (LIF.NAQ).

Life 360 is a relatively newly-added Australian equities sub-portfolio portfolio position. Life 360 delivered its FY24 results on 28th February. We viewed the result as “positive” and the stock price rallied 7% on the day. But it has fallen in line with decline in technology stocks in March (down 10%).

We have been using share price weakness to continue to add to our position.

The attractiveness of Life 360 stems from the following points:

- Market leadership, with a vast and fast-growing multi-national user base of 80 million people across the globe, as the clear market leader focused on this location and the family-safety segment

- Depth of services offered, including location tracking on phones, Tile devices for possessions such as keys, luggage, and soon to launch into pet-tracking, which will increasingly allow bundled pricing offers to maintain cost competitiveness

Life360 – Competitive Landscape – Comparison of product features

Source: 1H25 Company reports

3. High recurring nature of its revenue base given subscription-based pricing

Life360 –high recurring revenue mix $m

A more consistent, easier-to-predict revenue base is highly valued by the investment community

- High stickiness and interaction of the product by users. Life 360 is one of the highest use applications, particularly across social media platforms

Apple Phone (US) Application daily average user rankings

Advertising $ revenue per user – social media sites

5. A significant opportunity to monetise its large component of non-paying users via options such as becoming a platform for companies to advertisers on. The firm recently announced a partnership with Uber (e.g. sending alerts when people land at the airport and may need the service) as well as safe Uber Eats deliveries for children with authorised/screened drivers.

Conclusion

Access to technology companies with significant international growth opportunities and with profitable footprints is a challenge when investing across the ASX. Even more challenging is finding those investment fundamentals along with attractive valuations. The latest shakeout in US technology stock pricing presents us with opportunities to do so in a focused way with ASX-listed stocks such as Life 360.

Innovate Access Group

Innovate Access Group, (formerly Mr Rental), including the investment in Gimme, has been a long-held position, albeit modest, in clients’ Australian equities sub-portfolios.

After exploring a range of alternatives, we have decided to write off this holding. For completeness, I set out below our rationale.

Over the past five years, we have seen the group (Innovate Group) firm up the value in a range of its satellite businesses, including Rental NZ and its home-staging business called Solvd. Both companies have effectively been spun out of the main entity.

In turn, the core Gimme product had developed into an efficient operation selling household goods to customers with a similar economic profile to its former long-term rental clients.

At scale, it was anticipated that the Gimme business could leverage its effective brand, high consumer web traffic and low cost to acquire new customers. This combination would represent a viable long-term solution that could attract further investment and enable a First Samuel sell down.

At the end of FY24, we noted that following continued progress in the operational side, albeit at moderate scale, we would test the market for three strategic options. The objective was to make a final investment decision early in 2025. We pursued each option with capable partners with experience in the area. We demonstrated the viability of the business model and created interest in the business’s operational capabilities.

The team at Innovate Access was ultimately only offered funding for an exceptionally rapid growth strategy – with funding and growth aspirations more than double the size and pace required. Movements in domestic funding markets, and changes in economic conditions, have created a circumstance in which it is easier to source too much money, than it is to source a smaller amount.

New funding also would require a large, high-risk co-contribution from First Samuel clients. In the medium term, this co-contribution would equal the amount already invested and be substantially higher risk than the investment team felt comfortable including in clients’ equity sub-portfolios.

Proving out the holding value of the business would only occur over an extended timeframe, and as noted would create a higher than acceptable risk profile.

Ultimately, we have instead chosen to write-off the value of the investment. The value of any residual assets will be used to pay creditors.

In the remaining months of FY25 we anticipate being able to facilitate the sale of the existing shares in Innovate Access Group for a nominal sum, enabling clients to realise a capital loss. For most client accounts in a tax payable position, the realised capital loss will prove valuable in a year in which their portfolios have crystallised significant capital gains.

Despite comfort with the rationale and support for the decision, it remains a disappointing conclusion for the long-held position. Clients will notice that the value of this investment was written down on 21 February 2025. All discussion of average client portfolio returns in this document and discussion in the monthly CIO video includes the impact of this write-down.

The information in this article is of a general nature and does not take into consideration your personal objectives, financial situation or needs. Before acting on any of this information, you should consider whether it is appropriate for your personal circumstances and seek personal financial advice.