Read the previous week’s Investment Matters.

Photo © AndreyPopov from Via Canva.com

Copyright 2025 First Samuel Limited

It’s been arguably the most volatile week for investments since the depths of the GFC. But I’ll let others provide the details for market records that have been broken. For Investment Matters, it’s mostly about Trump’s tariffs and your investments. And a little on your investment in Challenger.

The Market

Trump’s Tariffs

Disclaimer

In our April client video, sent yesterday (click here for link), I said that whatever I write or say about markets or performance will be out of date by the time of reading or watching. But it’s not the exact size of the ups or downs that matters – it’s the trend, and why. With that caveat…

The shallow dive – ten points

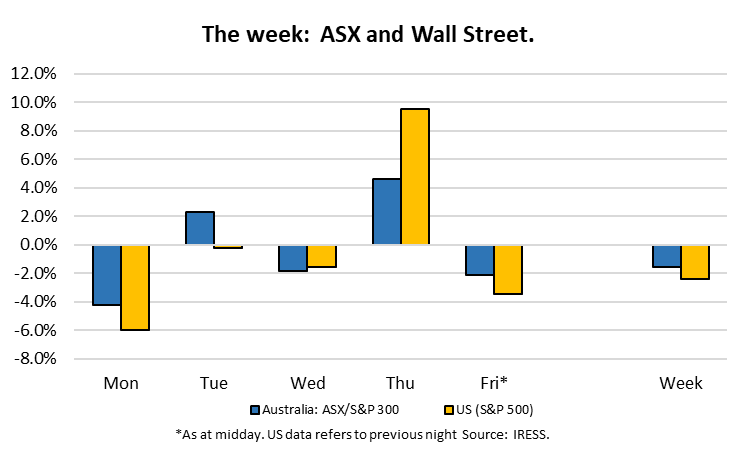

- The ASX300 rallied strongly yesterday. This follows the US rally following Trump’s 90-day tariff pause announcement.

- But China’s tariff has increased to 145% – this has the hallmarks of a trade war.

- The base cause of the market turnaround is a lessening of uncertainty. However, the ‘VIX’ (a market uncertainty metric) is still higher than pre-Trump.

- The tariff short story: Trump trying to re-organise world trade.

- World trade ‘order’ took decades of bureaucrats and businesspeople to establish.

- Trump is trying to unwind that in a few weeks. The outcome is disruption and risks for investment and economic growth.

- Trump’s crusade for trade reform remains, with non-tariff barriers and industrial policy (e.g. China dumping cheap cars) now foremost.

- We have parsed Trump’s tariffs into four clusters and are investing accordingly, especially increasing oil and tech companies’ exposure.

- Expect more Trump surprises, but as uncertainty declines so more opportunities arise.

We will sensibly be deploying cash.

The rebound

Yesterday’s big rebound in the ASX was due to a reduction in ‘uncertainty’. Markets will always fall sharply in times of considerable uncertainty. Recall that the ASX fell over 30% at the start of Covid. Before that, during the GFC, it fell by over 50%.

Each case was about uncertainty: the effect of a pandemic and a global banking crisis.

Figure 1: Trump Impact – ASX300 returns, pre-Liberation Day, post and Thursday recovery

Trump created increasing uncertainty because of his seeming change of mind about which countries were to be tariffed and by how much. The audacious breadth and scale of the tariffs capped the uncertainty.

The market measure of uncertainty (in the US) is what some called VIX – which is simply the price of market insurance against a downturn. The greater the uncertainty, the higher the insurance premia, hence the higher the VIX.

The figure below shows the history of the VIX since 2005, with the GFC and covid-19 peaks clearly visible in 2009 and 2020.

Figure 2: 20 years of volatility highlights the significance of Trump tariff announcements

Source: CBOE, Google

The VIX has declined but is still higher than pre-Trump. In the months leading up to Liberation Day, the VIX was less than 20. It peaked above 50 this week and ended trading at 32 on Wednesday, and had risen again overnight.

History shows us that uncertainty is a short-term circumstance and is always associated with lower share prices. But it does pass, and generally prices rise, with a lag, as uncertainty is reduced.

What changed?

Trump’s announcement on Wednesday (New York Time) that the application of so-called reciprocal tariffs would be delayed for 90 days (except for China) markedly reduced uncertainty. Hence the market responded.

There are two matters to note.

Firstly, the 10% base tariff remains. We consider that this will be a permanent imposition. Tariffs are a tax. And a 10% tax on all imports will provide a big boost to Trump’s need to reduce the US government’s deficit and debt. That is not to say it makes economic sense, nor does it mean that tariffs are an efficient way to address debt and deficits.

Secondly, China had responded to Trump’s first tariff increase with a retaliatory tariff of 84%. Trump responded in a Trumpian manner: US imports from China will now have a tariff of 145%. This is extraordinary. It shows that Trump sees China as a separate case and is happy to have a trade war.

It remains to be seen if Trump’s 145% response will cause Premier Xi to back down. Or will Xi have another less obvious tactic up his sleeve? Xi’s problem is that the Chinese economy is driven by exports – domestic consumption is weak, and investment is flat. Tariffs of 145% will cripple Chinese exports to the US. Tariffs as high as those proposed by both sides can now be called embargos, underlining the war-like positions taken.

We have noted in previous Investment Matters that Chinese devaluation over the next decade is highly likely. Tariffs only increase the likelihood.

Who will be the more enormous bull in the paddock?

The answer may lie in the fact that Trump is a short-term, transactional leader, albeit with long-held policy perspectives. Xi plays the long game. But how much damage can be done to China in the meantime?

Reorganise world trade order

Standing back from the Trump hyperbole and capriciousness and the market noise, there is a plan to reorganise the global trading order.

It is worth remembering that the current global trading order took decades, if not centuries, to be established. It is a product of bureaucrats and businesspeople that required evolved compromises, theft, and oftentimes wars. Political outcomes are a result of business decisions, not the other way around. Trump is driving business decisions and expects political outcomes to follow.

However, he is trying to undertake his crusade in a matter of weeks. The ‘shock and awe’ tactic has come up against market reality: increase uncertainty (which Trump loves to do) and markets will respond unhappily. And they have. Risks to investment and economic growth have quickly emerged.

Hence, the leap in the VIX. And now, Trump’s backdown (which he suggested was always plan).

But the 90-day pause is just that. Trump still has the will to drive a change to the global trade order. He will delight in making trade deals with the 60-odd countries that will need to pay respects, a very Chinese style of transaction.

And that is the rub. It’s not entirely a tariff matter. It’s about trade in the broad sense. The range of non-tariff barriers will now come into prominence. Also appearing will be an examination of industrial policy. China is the most obvious example of this, consider the wave of electric vehicles now being washed over the world.

But Europeans are masters of both non-tariff barriers and industrial barriers. Remember that the EU was established on the bedrock of these two practices (and plain vanilla tariffs). There will be much negotiation over the next 90 days. Ukraine and Gaza may be out of sight for a while.

For Australia, the problem is a second-order one. There is little to do in terms of trade negotiations with the US. The more significant issue will be China. The extent and depth of a China-US trade war is difficult to predict. It’s not just a matter of cheaper Chinese products being re-shipped to Australia (but all those BYD and Haval cars cannot be re-routed from the US – left-hand drive cars just don’t work in Australia), it’s a matter of Chinese demand for Australian commodities.

Market activity

There have been two market sell-offs this year, which have been well documented in the media. Clients have emerged from both with a better outcome that the ASX.

The first sell-off was in February. It will be recalled that we had been steadfast in holding against the momentum investment, the poster-child of which was the performance of the banks in the face of flat profit outlooks. The unwinding of the momentum trades and recovery in med-cap and smaller-cap stocks was good for clients.

The momentum trade has now reversed and is unlikely to be repeated.

The second sell-off is this week’s response (and partial recovery) to Trump’s tariffs. Some damage may be permanent. The market’s response to the China tariffs is yet to be clear.

Investment activity

We have not been idle.

Firstly, we have evolved to have over 10% cash in most clients’ Australian equities sub-portfolios. This provides opportunities.

Technology and oil

Secondly, some sectors have become somewhat inexpensive, especially technology and oil. We have increased exposure to both. Clients will notice technology stocks such as Block, Life360 and Seek Limited.

Our purchases of technology companies are all about price. We maintain target valuations for many companies not in the portfolio and wait for the opportunity to find bargains should they emerge.

Regarding oil we see significant short-term uncertainty regarding global demand but have looked for opportunities in Santos Limited, Beach Energy and Viva Energy at lower prices.

Industrials

Regarding industrial companies and mining stocks, reorganising global trade creates short-term adjustment pain. Trump overnight noted, “there’ll be a transition cost and transition problems, but in the end, it’s going to be a beautiful thing. We’re doing again what we should have done many years ago.”

Even Trump understands transition risks, and as investors, we need to look through many of the transition risks to find value.

Materials

The outlook for materials remains nuanced. Trade tensions and embargo-like conditions between China and the US create different risks for different commodities.

Rare Earths, for instance, will require reorganising global supply chains. We appreciated this likely development and have been a long-term investor in Lynas Corporation, which is building such a supply chain. Lynas stock price is 12% higher this month.

The outlook for copper is more complicated. Copper is at the heart of electrification. However, most of the demand for copper is China-based (>50%). Chinese primary demand ends up creating a mix of domestic goods (copper wire and electricity infrastructure, for instance) and products with embedded copper (electronics for example) for global distribution.

The supply of copper, however, is controlled by Western companies operating in South America, including BHP and RIO, in Indonesia (US company Freeport-McMoRan), in Africa (Glencore a Swiss company) and a range of local players around the world.

China, which imported over $60bn of copper ore in 2024, needs copper to continue manufacturing high-value products and support its investment-led economic growth. Our copper position is reflected in, amongst others, Sandfire Metals, which owns African and Spanish mines. Reorganising the global trade of copper will be very complicated, and this volatility was evident by large movements in its price this week. We retain a more than 5% share of the portfolio in our basket of copper exposures.

The outlook for iron ore is entirely political. China will need to stimulate additional investment to suppress the short-term economic risks to its economy from the embargo-like conditions imposed by the US. Building out the Chinese economy has resulted in most of the global demand for iron ore coming from China and the vast majority of ore supply from Australia and Brazil. Will iron ore become a political issue between Australia and China, and will China seek to diversify its supply of ore in the medium term?

Navigating the political tightrope of two-way economic reliance between China and Australia with the context of deeply antagonistic political and cultural heritages will remain the most critical role for the upcoming Prime Minister, regardless of persuasion.

Within this context, we retain a lower market weight exposure to iron ore and have used the volatility this week to switch, in a tax-effective manner, our holdings between BHP and RIO. RIO’s supply chains are now more diversified than BHP’s, including African iron ore mines. RIO’s diversification across minerals is superior, and the possible reorganisation of its market listing between the UK and Australia offers some long-term value.

Outlook for rates – portfolio impacts

This week and the four months since Trump’s election have highlighted rising long-dated interest rates. The market appreciates the risk of permanently higher inflation, a risk increased by tariffs. Inflation risk adds to concerns with US government deficits, especially given planned Trump tax cuts.

Higher long-term rates vary the outlook for investment, limit government spending, and, where slight inflation expectations are embedded, may encourage productivity-enhancing investment. We believe that slightly higher inflation and interest rates, when consumption is supported by government demand and intergenerational transfer, may encourage productive capital allocation while discouraging the increasing debt and inflating asset prices of the past two decades.

In such an environment, we want to invest in strong industrial companies, household-facing companies with brand power, and resources that benefit from infrastructure investment and electrification .

Whilst short-term interest rates are often controlled by central banks, including the RBA in Australia, long-term rates are market-derived. The tension between short-term and long-term rates needs to be managed, with management assisted by inflation and exchange rates. We believe Australia is generally well-placed from a monetary policy perspective to manage rates through the AUD, a point noted by RBA Governor Bullock this week.

Higher rates imply limited housing price growth and the need to move away from debt-fuelled, surging, population-led economic growth. Households will benefit from minor rate cuts this year but must manage their high debt levels over the medium term.

This is not the best environment for banks. We retain our limited portfolio position in the Big Four banks, preferring investment bank exposure through Macquarie Group and business lending through Judo Capital. Judo Capital’s share price allowed clients to own more of the company. After selling down much of our holding for close to $2 per share in recent months, we were able to add to our position around $1.50.

Within this mute growth environment, amid geopolitical tension, we expect industrial policy will find a larger role in Australia, as it has in China, Europe and the US. Our holdings in Cleanaway, SGH (Boral, Coates etc), will benefit.

Challenger – an investment

Just a follow-up to last week’s note about clients’ holding in Challenger Limited. The Japanese insurance giant Dai-ichi Life has bought a 15% stake in Challenger at a 54% premium to the market price. Through its Australian life insurer TAL it is set to become the largest shareholder in CGF.

Subject to FIRB and APRA approvals, this exceptional premium paid for the stake indicates the value the acquirer sees and the likelihood that it will pursue the complete acquisition in time. We share their view of the value in the stock as outlined last week.

There is a range of synergy opportunities between TAL and CGF in distribution, asset management, and product development. Whilst not intending to launch a takeover at this stage, we note that TAL has a strong track record of purchasing existing businesses in Australia and has not had a history of long-term holdings of only minority stakes.

As expected, the stock outperformed in an otherwise challenging market this week, and we see further scope for the stock price to move from current levels in the low $6 range towards the price paid by Dai-ichi Life.

The information in this article is of a general nature and does not take into consideration your personal objectives, financial situation or needs. Before acting on any of this information, you should consider whether it is appropriate for your personal circumstances and seek personal financial advice.