The first of August marks the beginning of the financial reporting season for most ASX-listed companies. This period, commonly referred to as “reporting season,” sees companies with a June year-end update the market—usually in August—on recent trading activity and provide interim reports on their financial position for the past six or twelve months.

Photo © WIlliam_Potter from Getty Images Via Canva.com

Copyright 2025 First Samuel Limited

The Market

Introduction

This year, we anticipate the reporting season to be especially volatile, with several factors contributing to greater-than-usual uncertainty:

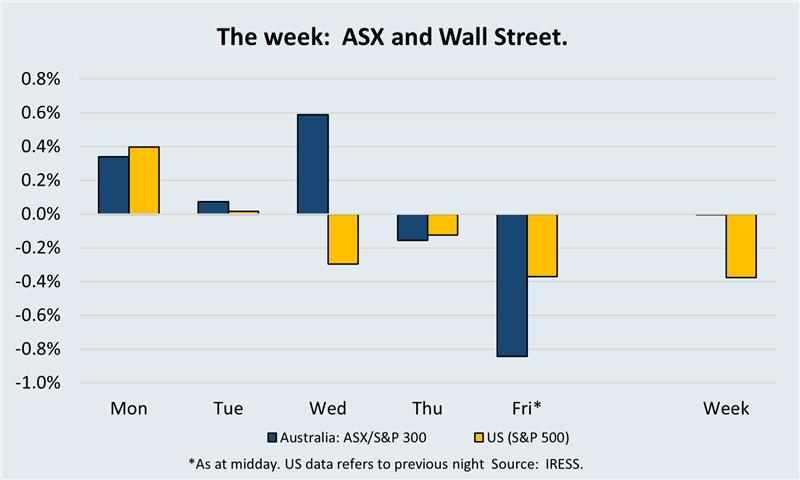

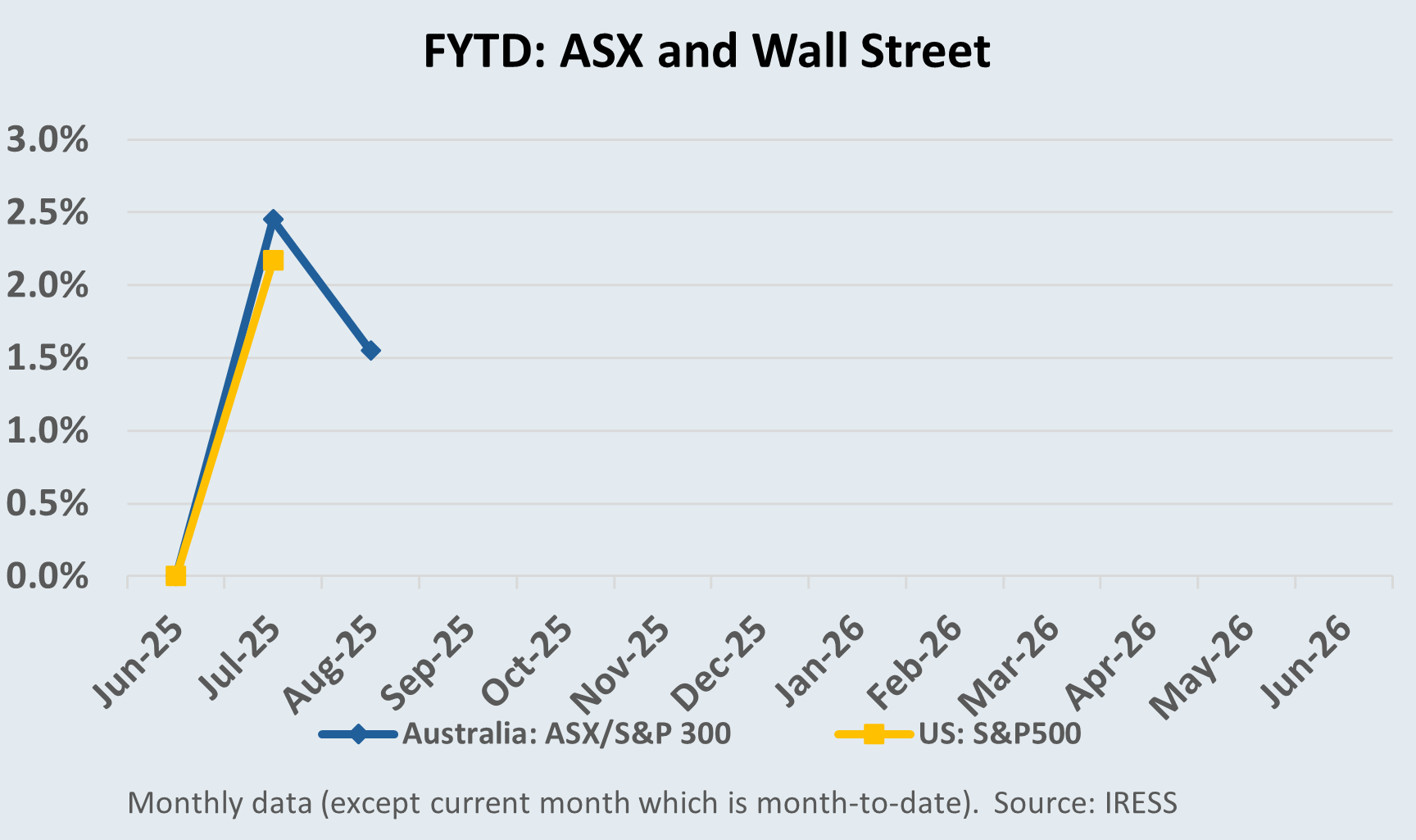

- Strong market gains leading into August, with the ASX300 up 2.4% in July.

- Momentum that propelled the market from April to July is showing signs of fatigue. Companies that disappoint—especially those with stretched valuations—may see significant share price corrections.

- Early signs of sector rotation, particularly away from high-priced, larger-cap stocks, are beginning to appear.

- Low expectations for many “left behind” stocks—those that have underperformed or delivered weaker results recently. Even modest improvements could trigger outsized share price gains during this reporting period.

At the company level, several key themes are likely to emerge:

- Uncertainty around Australia’s economic outlook remains, with pockets of weakness offset by resilient consumer spending and robust government support.

- Increased focus on innovation and AI investment. We expect many companies to comment on their use of artificial intelligence and new product development pipelines. In a low-productivity environment, we are watching for genuine innovation leaders to emerge—companies that can back up claims of improved efficiency and competitive advantage.

- Companies delivering credible progress on innovation and productivity are likely to be rewarded by the market this season.

Within your portfolios, you hold a mix of companies impacted by recent market momentum—such as 360 Limited, BlueScope Steel, and Block (XYZ)—alongside others that have lagged the broader market, including Healius (following its special dividend), and solid FY24/25 performers like Seven Group Holdings (SGH) and Paragon Care (PGC) that have recently paused.

We are also watching for updates from names such as Cleanaway, Worley, QBE, and nib Insurance, each of which may reveal more about their innovation strategies. The market currently assigns little value to potential upside from these initiatives, so positive surprises could be significant.

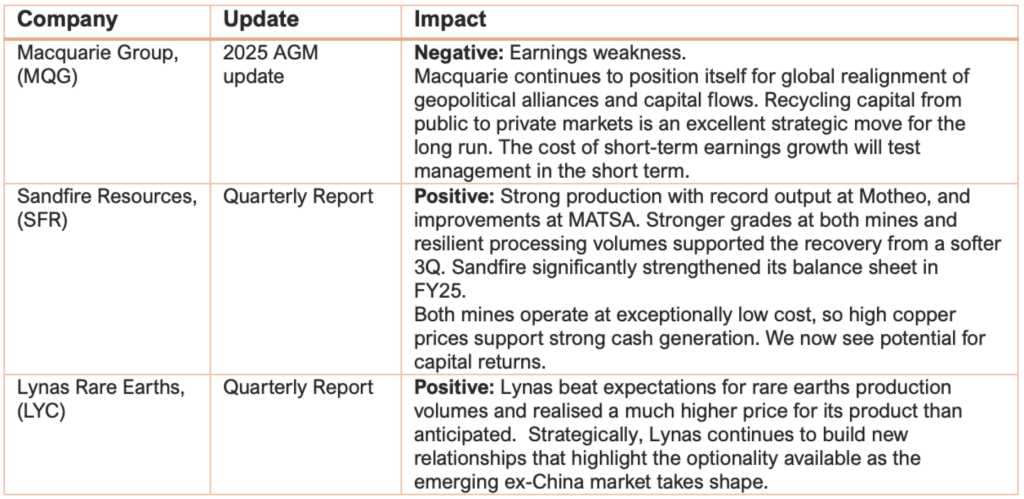

As the reporting season approaches, a handful of companies—most notably mining firms (quarterly production reports), financial companies such as Macquarie Group, and others with material changes to their outlook provide market updates ahead of their full results.

The table below outlines key updates.

Table 1: Market updates in July

In this edition of Investment Matters, we also update clients on three smaller portfolio positions: Imdex, Bapcor, and Viva Energy (recently added to select portfolios based on individual preferences and tax positions).

Imdex (IDX): Acquiring Earth Science Analytics

Since initiating our Imdex position between May and October 2023, we’ve generated an 80%+ uplift in value, progressively realising gains by selling more than 75% of the holding across 2024 and early 2025.

With the share price reaching our target valuation, we’ve closely monitored the company’s next moves, particularly how it would deploy its expanded debt funding. Only highly accretive investments or a clear leap in digital innovation could justify a higher valuation, in our view.

The Imdex share price has rapidly gone from “cheap” with the market being overly concerned with current conditions and the integration of previous acquisitions to being relatively expensive, and the market excited about future acquisitions.

This week, Imdex announced the acquisition of Earth Science Analytics (ESA), a Norwegian-based software company specialising in AI-driven geoscience solutions. The purchase price is A$26 million (with a path to 100% ownership through a put/call structure), funded via existing debt facilities, and adds to Imdex’s digital orebody knowledge platform.

ESA’s flagship product, EarthNET, is a cloud-based platform leveraging machine learning to ingest and interpret vast geoscience datasets rapidly, from seismic and core imagery to geophysical sensor data. Initially developed for the energy sector, EarthNET has demonstrated the ability to cut interpretation times by up to 90% and achieve over 95% accuracy in rock property prediction. Imdex sees strong potential to translate these capabilities to mining, integrating EarthNET with its own HUB IQ, Datarock, and Krux offerings. The result: more powerful decision-support tools for geoscientists and customers alike, and an acceleration of Imdex’s digital transformation strategy.

ESA isn’t a large business, with around A$4 million in revenue in FY26 (breakeven EBITDA). The deal effectively accelerates R&D that Imdex would have undertaken anyway, giving it an immediate leap in capability and time-to-market for digital solutions. We see this as consistent with management’s strategy, which targets “sticky”, scalable and high-margin SaaS revenues.

As drilling activity accelerates globally and orebody knowledge becomes more data-driven, Imdex’s latest move positions it strongly for future growth. Industry feedback suggests a strong finish to FY25, and we anticipate positive momentum into FY26.

In terms of portfolio construction, this is a good example of originally investing for value and market dislocation; taking profits off the table and then using our research process and company interaction to learn more about future options. We have retained a small position in most client portfolios and will await the coming results with interest.

Bapcor: Navigating a Classic Turnaround, Lynch-Style

Legendary investor Peter Lynch once said, “Turnarounds seldom turn,” cautioning investors against expecting quick fixes—yet also recognising that successful turnarounds can be some of the most rewarding investments. Our approach typically favours high-quality, patient holdings, and as many readers know, our portfolio companies are often the subject of takeover approaches. Bapcor, the owners of brands such as Burson’s, Autobarn, Autopro and Midas, is a timely illustration: a turnaround story that also attracted high-profile private equity interest.

The key consideration from a portfolio construction perspective is to have limited “turnaround stories” in the portfolio. Indeed, we consider only Bapcor and Healius to be in such a category, and neither generally represents a top 20 position in client portfolios.

Recent Developments

Bapcor’s latest trading update unsettled the market, revealing a sharp deterioration in sales across all segments and the immediate departure of three board members. While this has understandably rattled confidence, we interpret management’s guidance for FY25 as a “reset,” cleaning out the financials and establishing a new, more achievable base.

Some value has been lost with the anticipated reduction in earnings across FY25/26 of slightly more than 10%, but our medium-term targets remain. If ours and the BAP CEO’s projections prove correct, the company could deliver compound annual EPS growth of more than 15% FY30. We still believe that the company is worth considerably more than $5.00 per share.

Interpreting the Weakness

The deterioration in Bapcor’s sales trends during the second half is partly an industry issue. Still, it more so reflects internal disruption from management turnover and a shift in retail promotional tactics. As the business undergoes simplification—including prudent store closures—the sales base will shrink but could become more robust over time.

Positively, EBITDA margins improved by 40 basis points in 2H25, signalling early cost management gains. Still, around $6–7 million of the EBITDA decline is considered permanent, with management resetting retained earnings by $24 million.

Private Equity Interest

In June 2024, Bapcor received a takeover proposal from Bain Capital, one of the world’s largest private equity firms. Bain offered $5.40 per share—a substantial premium to where the stock was trading at the time, valuing Bapcor at over $1.8 billion. After due diligence, the bid was ultimately withdrawn in July, reportedly due to further trading softness and boardroom instability. However, the approach underscores the strategic value and latent quality of Bapcor’s assets, highlighting our view that even companies in transition can attract strong outside interest.

Conclusion

In summary, Bapcor remains a high-conviction turnaround for us, aligning with Peter Lynch’s view that a few well-chosen recovery stories can add meaningful upside to a quality portfolio. The recent reset presents both risk and opportunity, and we remain patient as new management works to restore growth and confidence.

Viva Energy: Where’s the cigs?

A relatively small number of clients hold a moderate-sized position in Viva Energy in their Australian equity portfolio. Clients who had excess cash and limited restrictions bought into the company in late March and early April. The stock had sold off heavily due to a mix of concerns, including the impact of the illicit tobacco trade, particularly following a Four Corners piece on the industry. There were also concerns regarding Viva Energy’s capacity to execute its development and expansion of the OTR (On The Run) brand.

Viva Energy was a company that we used as a bench list position.

A bench list of vetted stocks is intended to support the core portfolio by providing additional exposure or diversification when current holdings fall below allocation targets or when rebalancing is required. This can be especially important when undertaking tax management. Clients who can realise capital gains in some positions to offset losses in others will often need a stock from the bench list.

Bench list stocks are not necessarily short-term positions either; clients holding IAG in their portfolios have held the position for many years. Additional bench positions in the current portfolio include Premier Investments (PMV).

Clients may recall that we owned a very profitable position in Viva Energy stock during the COVID-19 pandemic.

Quick recovery of share price

Since April, the VEA stock price recovered more than 40 per cent, and there were high expectations for the 1H2025 trading update. Although the stock price fell 6 per cent, the result was a sequential improvement in underlying performance.

Our valuation is likely to rise following the result.

As background, Viva Energy’s profitability comes from a mixture of refinery assets, fuel retailing, wholesale sales of fuel, including aviation fuel, and an extensive convenience store network, including Shell Coles Express/Reddy Express, OTR, Liberty, and Westside Petroleum.

Viva Energy’s first-half 2025 trading update presented a mixed picture, with unaudited group EBITDA of A$300 million coming in about 7% below consensus expectations (A$323 million), largely due to short-term refining headwinds. The refining segment was hit by unplanned outages, planned maintenance, and higher energy costs. While the headline miss triggered a sharp share price reaction, it’s important to note that the core Convenience & Mobility (C&M) segment continues to show underlying strength.

Viva also made solid operational progress: nine new OTR stores opened in the quarter, with eleven more under conversion, and the transition away from legacy Coles agreements is now complete. Synergies and cost-out initiatives—targeted at A$30 million and A$50 million, respectively—are expected to support second-half results.

A key challenge for Viva Energy this year has been the steep decline in tobacco sales, following a shift in consumer behaviour, and the impact of illicit tobacco sales. Tobacco has long been a significant traffic driver for traditional service station retailers. Based on the author’s travel across the mainland US, the future direction of convenience retail is for a much larger, more substantial breadth of offerings.

While the tobacco traffic impact is being felt in the short term, Viva’s response is to double down on what it sees as the future: high-quality, modern convenience retailing.

The ongoing rollout of the OTR (On The Run) format is central to this evolution. These stores offer an expanded range of food, coffee, and everyday essentials, creating reasons for customers to visit beyond just filling up the tank. Despite some market anxiety over the speed of store conversions and near-term sales softness, early feedback on new OTR sites has been positive.

Summary

Core to a higher valuation of VEA will be our assessment of the company’s success in executing its cost-out program and the achievement of higher operating margins within OTR.

We are currently sceptical that higher operating margins can be sustainably driven by pure expansion in gross margins (higher price for goods). Convenience always needs to balance pricing with availability, and we believe that pricing is now extended. As such, higher margins will need to be driven by higher foot traffic, a more extensive offering leading to higher average spend, and a better mix of products.

Regulatory targeting of illicit tobacco (including recent changes in some Australian states), along with increased police enforcement surrounding illegal activity, is also likely to improve foot traffic to petrol convenience stores in the medium term.

The information in this article is of a general nature and does not take into consideration your personal objectives, financial situation or needs. Before acting on any of this information, you should consider whether it is appropriate for your personal circumstances and seek personal financial advice.