Photo © imaginima from Via Canva.com

January 2025: Fabulous start to the year with much to ponder

The ASX is off to a hot start in January 2025 with a range of themes we observed at the end of 2024 being realised. We remain excited about how the market is set up for calendar 2025; for the first time since 2019, we can see large and straightforward sector dispersion. Some sectors are more expensive than ever, and others are relatively cheap, this provides us with an opportunity to profit from the inevitable rebalance.

January has shown the first evidence of this rebalance.

2024 saw a narrow band of stock leadership, a small number of large companies drove the majority of outperformance, and high momentum, where yesterday’s price rises led to even higher prices today, regardless of the underlying strength of company earnings. In January we saw waning returns to some of the leaders, and a reduction in market momentum.

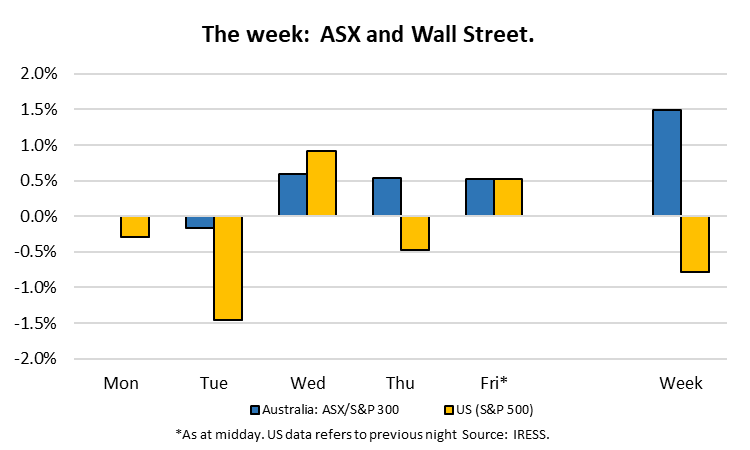

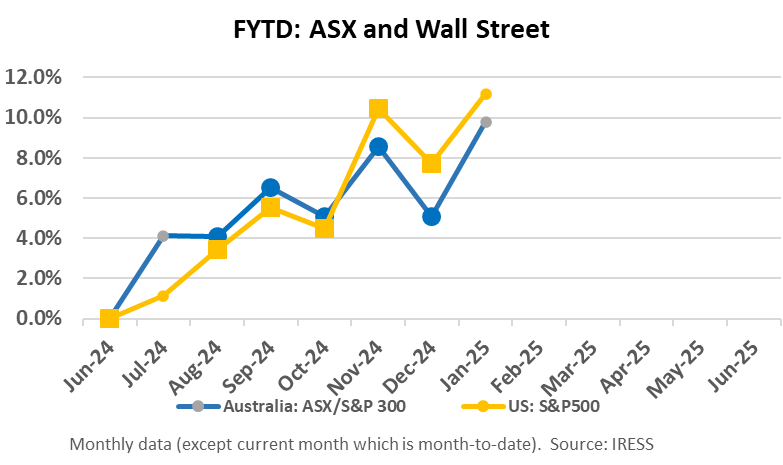

The Benchmark ASX300 is up almost 4 per cent this month with First Samuel client’s Australian Equity portfolios performing stronger still. The combination of stable economic growth, a moderately-priced market, and the prospect of interest rate cuts is providing some comfort. The operating performance of most sectors of the market also continues to support a cautiously positive outlook for most sectors of the economy.

This week’s Investment Matters will touch on relevant news items related to the portfolio and macroeconomic conditions.

We also touch on news surrounding Chinese AI firm DeepSeek, and its impact on global markets.

The Market

December inflation estimates: Will the Reserve Bank cut interest rates this month?

On January 29th the ABS released the latest estimates of inflation, and the figures sharply increased the market’s perceived likelihood of an interest rate cut by the Reserve Bank in February.

The softer-than-expected inflation data led political pundits to increase the chances of an April Federal election.

Lower interest rates, supporting Australian households who are otherwise struggling from a range cost of living pressures, combined with an early resolution of political uncertainty was a powerful fillip for markets.

Turning to the inflation data itself, the surprise of lower-than-expected inflation was comprehensive.

- The Q4 2024 CPI was below expected, and materially below the RBA’s forecast.

- The trimmed mean CPI which is the preferred measure of the RBA showed (annualised) inflation growth in the final quarter of only 2%, the bottom of the RBA’s target.

- The average rise in inflation across Q3-24 and Q4-24 was just above ~2½% annualised which is close to the RBA’s mid-point.

The slowing rate of inflation is clearly observed in the chart below. The element to concentrate on is the speed of reduction in the black line (year-on-year inflation) and the pace of fall of the blue bars (the quarterly contribution to inflation).

Following the release of the data the respected UBS economist Geroge Tharenou changed his view of when the rate cut would occur from May to February. We can still see a case for caution regarding the use of interest rate cuts, but the preconditions for a lower interest rate over 2025 have clearly been met.

The support provided by a rate cut will be important for range of companies in clients’ portfolios, including Macquarie Group, Seven Group (SGH), Inghams, Seek, EarlyPay and Woolworths.

EarlyPay: AFR reports corporate activity

On January 23rd the Australian Financial Review’s Street Talk column reported that “ASX-listed invoice financing business EarlyPay is ready for another spin on the auction block.”

Quoting the AFR; “Street Talk can reveal EarlyPay’s board has mandated boutique corporate adviser, Highbury Partnership, to seek bids for the business which had a $249 million book at June 30, and made $35 million in revenue and $4.9 million underlying net profit.”

“Sources said EarlyPay chairman Geoffrey Sam had called in the bankers after learning of its largest shareholder, the ASX-listed COG Financial Services’ intention to sell its 21.4 per cent stake in the company should a decent-enough offer present itself. They added that EarlyPay’s board had decided it was better off hanging the for-sale sign than making home with a new majority shareholder.”

Clients will recall that EarlyPay, of which First Samuel is a major shareholder, has once before headed down the path for sale in 2020. We view the possible sale of the business as the most likely way to extract value from our long-held position. However, a sale at any price is not likely.

EarlyPay has undertaken an extensive recalibration of its business model in recent years and its current earnings are robust. Our expected free cash flow yield from this investment, both this year and over the next 3 years justify a higher share price than the price EarlyPay traded at the end of 2024.

Activity reports and updates from mining companies

Known as Activity Reports mining companies provide critical quarterly updates on their progress. Released prior to any periodic company financial reports they concentrate on;

- Mining activity, including analysis of the grades of ore extracted;

- The prices realised for material extracted;

- The direct costs of mining over the preceding quarter;

- Changes, if any, the company has with respect to their plans for total production and average costs over the reminder of the year, and

- Irregular updates on the exploration plans and past success depending on the maturity of the mining undertaken.

Because of the breadth of the information supplied and the specificity of the task of mining itself, the quarterly Activity Reports for miners are often more important than the subsequently released financial results.

For smaller miners, especially those with variable operations or operations in ramp up or development, the activity reports become critical.

All of our mining companies have released such reports, and a snapshot of outcomes is provided below.

| Mining company | Our view | Rationale | Stock price post release |

| Aurelia Metals (AMI | Positive | Great cash flow | +11% |

| Sandfire | Positive | Cost control fantastic | +5% |

| Lynas (LYC) | Negative | Weak market conditions | -12% |

| BHP | Neutral | As expected, | -2% |

| Mineral Resources (MIN) | Negative | Weak debt position despite asset sales | -2% |

| Develop Global (DVP) | Positive | Woodlawn mine on track | +8% |

| Catalyst Metals (CYL) | Positive | Cash and production robust | +7% |

| IGO | Negative | Volumes soft, higher capital spend | -4% |

We were especially pleased with the report from Aurelia Metals and Sandfire Metals. Aurelia is a long-held position which has recovered substantially through 2024 and now looks forward to first production from its Federation deposit. Our meetings with management this week continue to highlight both the value in the existing assets and the range of strategic options available within the Cobar region.

Sandfire continues to operate its global copper mines with a level of operational excellence which isn’t always guaranteed in complicated systems. Its new mines in Africa (Motheo) are continuing to deliver outperformance. In the medium term the success the company has had in commissioning and early operations will be even more important should exploration success or acquisitions in the region follow.

The update by Mineral Resources, a position we had already largely sold out of, was disappointing and we have now exited. Despite the volatility of the position over the past 4 years, and a weak outcome in 2024, Mineral Resources remains a significantly profitable position in client portfolios since 2020.

DeepSeek: NVIDIA, AI and China – a perspective

The biggest global news this week surrounded the world’s reaction to an update by a previously unheralded Chinese artificial intelligence company called DeepSeek. The company released details of a new AI model, including OpenSource (available to all) code, a widely available App, and tools for use by global developers.

Companies, including OpenAI the owner of ChatGPT, and mega companies such as Meta, Google and Microsoft are constantly releasing new AI models. With each new release a new AI model is likely to set a new benchmark of performance, offer new services or generally expand the future scope of opportunities for real life usage.

What made the DeepSeek release different was at least five drastically different outcomes.

- The DeepSeek model was suggested, in an accompanying technical paper to have been developed using a fraction of the computing capacity normally required. The implications for future demand of powerful AI chips, especially those developed by NVIDIA could be significant.

- As a result, the model cost a fraction (~1/20th) of the amount that the markets are currently seeing its competitors spend. This suggests that the lead that current large companies can develop over future competitors may be overstated. In turn it highlights the value which likely remains in the ability to collect data and own it, rather than simply transform it.

- The impact of the lower development spend, translated directly into the amount that DeepSeek is now charging developers to integrate their model into business and internet applications. Overnight the price of using an AI system fell by 90 per cent, compared to ChatGPT for instance. This change offers the probability that future gains in productivity that we see being possible for the economy from AI are likely to be materially cheaper than previously envisaged.

- The nature of the algorithms used to develop the new DeepSeek R1 model has the potential to dramatically changed the way in which all AI developers train their models. Potentially the method of training is more closely aligned to the way in which humans reason and may offer the opportunity to develop better “reasoning” models that mimic and eventually exceed the capacity of everyday human problem-solving.

- Some market participants were surprised that a smaller Chinese company would have made such strides. We would have thought that American exceptionalism didn’t extend to the US being the only country that that can take existing inventions, and through sheer incremental innovation, help to drive down the costs and lift the access to technology. Indeed we should expect that.

- Overpaying for a short-term technological lead is one of the core reasons why we have chosen to avoid the most expensive of the US tech stocks over the past year. The rise of BYD in the face of Tesla’s initial lead appears another example.

Just some of the reactions, which include political reactions from President Trump, included:

- The share price of NVIDIA, US listed high powered AI chip maker, and the world’s biggest company by market capitalisation, whipsawed. Its market value fell approximately US$590 billion Monday, but rose by roughly $260 billion Tuesday and dropped $130 billion Wednesday.

- Billionaire venture capital investor Marc Andreeson described the impact of the new DeepSeek R1 AI model as “AI’s Sputnik moment,” in a post on X on Sunday.

By the end of the week, when the dust had settled, there was reasonable scepticism about the motivations of the Chinese state behind some of the information. As noted by the The Economist on 23rd January 2025, China’s financial system is under brutal pressure. The pressure from a resurgent Trump and movements in global capital are pressuring the one-party state.

Questions regarding the access DeepSeek had to NVIDIA chips beyond the US export controls of NVIDIA chips to China has been raised, and there are suggestions that a great deal of the information that DeepSeek used to improve their system was “borrowed“ from other companies.

It is possible the development gains are overstated. The pricing of the DeepSeek software offer has a geopolitical element underlying the discount.

Despite this, the investment implications going forward are relatively straightforward. China’s conventional innovation of optimization, efficiency and scalability, rather than scientific breakthroughs continues to drive global economic outcomes. AI will prove no different.

DeepSeek demonstrates that you can significantly build AI models using a cheaper dataset more efficiently. It breaks the problem into elements that may be more intuitive, may be cheaper and, being OpenSource, more likely to be shared by large numbers of users.

Over and above the political impact, DeepSeek reinforced for First Samuel as investors a couple of core beliefs.

- Future productivity growth is a fundamental driver of equity returns, and the most powerful force behind the use of equities as a wealth-creation tool

- Valuing companies that generate consistent cashflows, who also own the capacity to grow and adapt is much more important and less risky, than simply assuming that existing advantages last forever. This week DeepSeek proved the case, next week it will be another company ….

The information in this article is of a general nature and does not take into consideration your personal objectives, financial situation or needs. Before acting on any of this information, you should consider whether it is appropriate for your personal circumstances and seek personal financial advice.