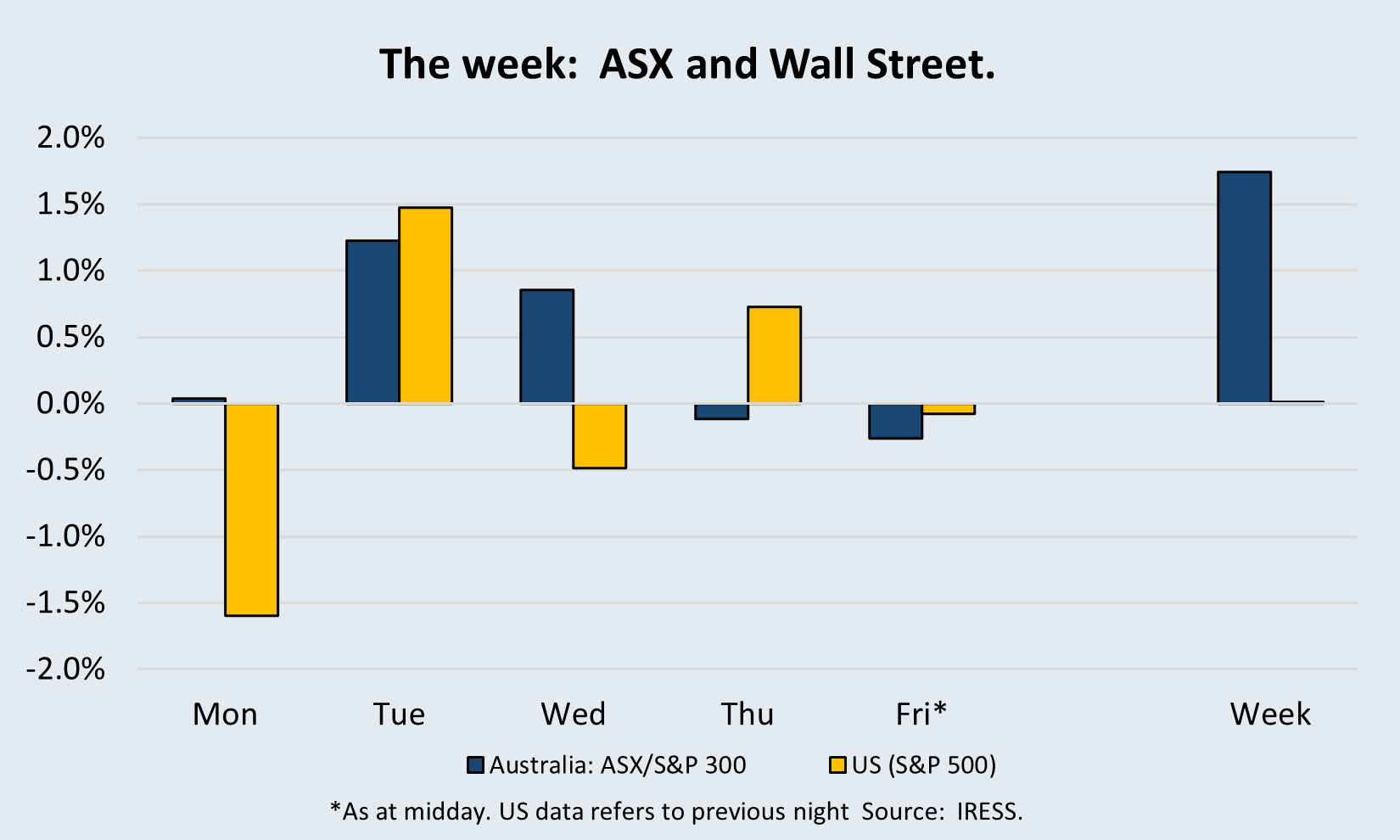

An uneventful first week of Profit Reporting Season with only Beach Energy bringing forward its results to Monday. We also caught up with the management team of our strong-performing Garda Property Group this week.

In this edition of Investment Matters, we update clients on the Beach Energy and Garda results.

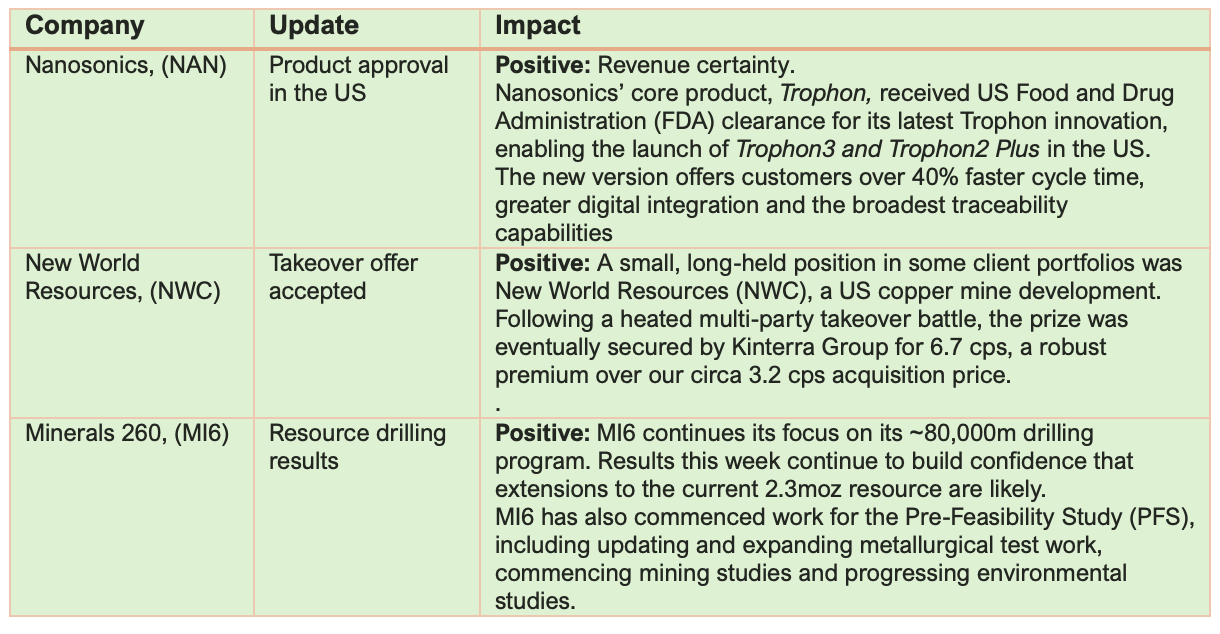

There was a small number of noteworthy, smaller and new items in the portfolio outlined in the table below.

Read the previous week’s Investment Matters.

Copyright 2025 First Samuel Limited

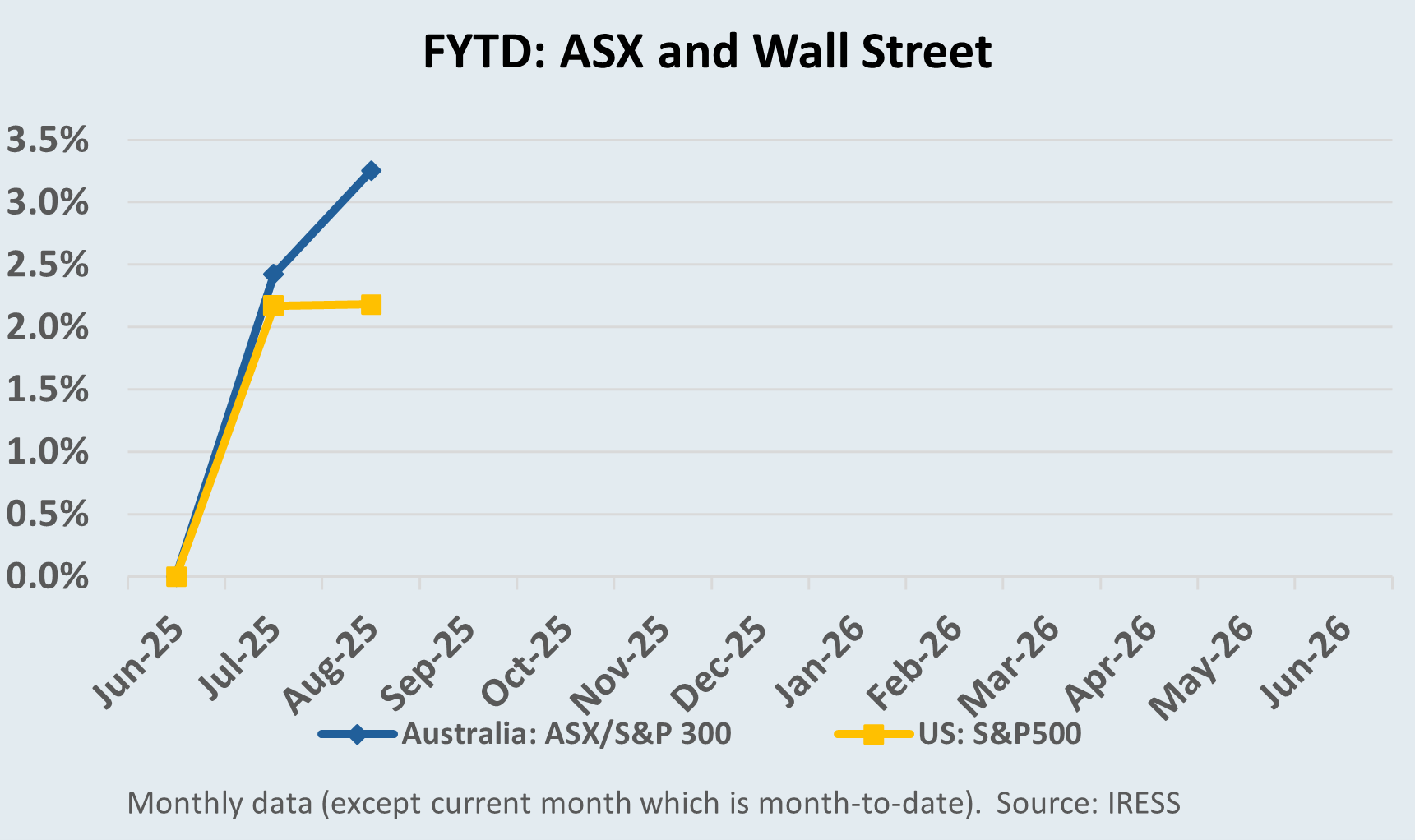

The Market

Table 1: Company updates in early August

Beach Energy (BPT):

Mixed update – M&A comments place pressure on investment case

Beach Energy Limited explores for and produces oil and gas in the Cooper Basin, Otway Basin in offshore Victoria, onshore gas developments in Western Australia and the Kupe offshore gas field in New Zealand. Its main growth project is the Waitsia Gas Plant in WA, with commissioning underway and expected to be completed in 2025.

First Samuel clients entered a small Beach Energy (BPT) position at $1.40 in June and July last year, attracted by what appeared to be robust future cash flows underpinned by a portfolio of Australian gas assets, especially the high-potential Waitsia project.

Our original investment thesis was straightforward: reliable, long-life production, a disciplined balance sheet, and the prospect of strong free cash flow (FCF) generation supporting attractive shareholder returns. The Perth Basin, which contains the Waitsia project, also presents as a genuinely strategic asset in Western Australia, one crucial for the future economic development of the state. The investment is consistent with several of our core principles regarding strategic assets, strong management (supported by Seven Group Holdings) and FCF focus with additional optionality.

While some fundamentals still support this view, recent developments—operational, financial, and strategic—have made the outlook more complicated. With an opening Friday this week of $1.24 and around 7cps in dividends, Beach Energy is yet to prove a successful investment.

Production and financial results released in the past week highlight additional concerns. Discussions by the CEO and additional media coverage have highlighted further risks of the company pursuing merger and acquisition (M&A) activity that would, in our view, generate limited value. In this review, we look at each of the drivers that risk our underlying valuation of $1.65 for the company.

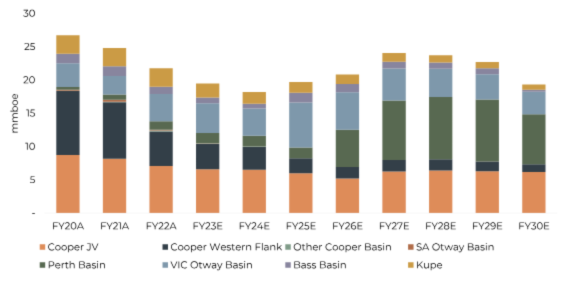

The chart below shows future production, and what is clear is that the Waitsia (Perth Basin) volume is key to generating consistently growing output in the medium term.

Table #2: Production expectations by asset – Barrenjoey estimates from company sources

Source: Company data, Barrenjoey estimates

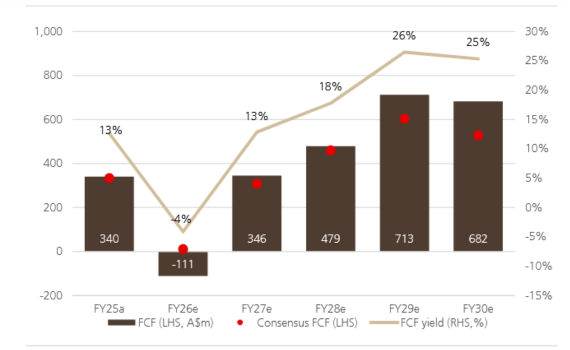

Once fully ramped up, Waitsia’s gas is expected to be sold into the lucrative LNG export market via the North West Shelf (NWS), potentially providing Beach with higher, spot-linked prices and a material uplift in FCF. Management has flagged that, post-Waitsia, Beach could generate free cash flow yields of around 20% from FY28 onward—an enticing prospect for investors such as First Samuel, which appreciates strong cash flow yield.

Table 3: Free cash flow and free cash flow yield – BPT to 2030

Source: Company data, UBS

However, recent production downgrades—particularly in the Perth (-10.7mmboe – million barrels of oil equivalent) and Otway (-2.3mmboe) basins—have called into question the longevity and predictability of these future cash flows. Lower reserves mean less future production, a shorter asset life, and ultimately, lower free cash generation than previously anticipated.

Table #4: Change to Beach’s reserves

Source: Company data, UBS

To be clear, reduced 2P (‘proven and probable’) reserves directly relate to future falls in revenue but rarely result in a fall in existing or planned capital expenditure. They rarely allow for any other offset savings either. Lower revenue accentuates the importance of providing realistic future capex, depreciation, and abandonment costs.

The market now, quite reasonably, is cautious of these forecasts, especially offshore abandonment costs, which industry experience suggests are often underestimated. In terms of non-Waitsia existing assets, Otway basin work programmes are expensive and logistically demanding. Execution risk remains elevated: delays or cost overruns here could further erode free cash flow.

The shortened reserve life now also means that sustaining and organic growth capex will be a persistent feature of the next decade, not a temporary hurdle, further increasing risks associated with the performance of Waitsia.

With production imminent, any further delay or underperformance would have an outsized impact on Beach’s overall value. Positively, management remains confident of first gas from Waitsia in the September quarter, and this was appreciated by the market this week.

M&A Ambitions and the Growth Dilemma

In many respects, the uncertainty regarding project delivery and the ups and downs of reserve estimation are a constant in these types of investments in general, and the history of Beach Energy in particular. However, the core plan to generate cash from Waitisa for the clear benefit of shareholders in the major shareholder Seven Group Holdings was rarely brought into question.

Now, in July 2025, the most notable strategic shift is Beach’s increased openness to mergers and acquisitions. Management has signalled a willingness to raise gearing to 25–35% to fund “the right asset”—a move that would unlock $500 million to $1 billion of buying capacity. This is a material departure from a purely organic growth strategy and injects a significant new layer of uncertainty into the investment case.

History has shown that, in the Australian oil and gas industry, M&A rarely delivers transformational value for shareholders. Most deals are priced at a small discount to fair value, but synergies are challenging to realise, and integration risks abound. For Beach, a mid-cap with a solid operational platform but limited reserve life, the risk is that future cash flows—intended for dividends—are redirected into acquisitions that struggle to deliver meaningful uplift to group earnings or value.

Further, this shift in focus has already cast a shadow over the company’s dividend policy.

We have reduced our valuation to allow for the risks of value-destroying corporate activity, whereas we would usually consider M&A a possible upside event for most well-run companies.

Santos, Seven Group Holdings and Politics

Adding to the complexity is the situation with Santos, one of Beach’s key partners and Australia’s largest listed oil and gas producers. Clients would be aware that Santos is a successful client sub-portfolio position subject to a takeover bid. Whilst we have sold a portion of our Santos position, we remain firmly of the view that we prefer the deal to be successfully completed.

The $36.4 billion takeover bid for Santos by Abu Dhabi’s ADNOC and Carlyle Group has stirred national interest and political debate about foreign control of critical energy assets. Beach CEO Brett Woods has publicly questioned whether such a deal is in the national interest and hinted that Beach could be interested in acquiring assets spun out of any eventual Santos shake-up.

Seven Group CEO Ryan Stokes also talked up the role that Beach may play in the Santos deal this week. While asset “carve-outs” from larger peers can be attractive in theory—especially for a well-run mid-cap like Beach—the reality is such deals are rare, politically fraught, and operationally complex. Any move here would likely face government scrutiny and long execution timelines, making it difficult to bank on such scenarios as a pillar of the investment case.

Garda Property Group (GDF): Exceptional management demonstrates capability again

One of the most successful investments in clients’ Property Securities sub-portfolios over the past five years has been Garda Diversified (returning about 9.2% p.a.). Clients first bought the company’s stock in 2020 as the company sought to combat the challenges of COVID-19 as a business with a stretched balance sheet and a mix of office and industrial assets.

Having followed the management team since 2016, we were confident that the team, led by Managing Director and Executive Chairman Matthew Madsen, would be able to trade out its existing positions, develop new options and repair the balance sheet for the new realities of property post-COVID.

We appreciated the Garda model, which accentuates the importance of a transactional real estate strategy, championing the Group’s develop-to-own industrial model and fine-tuned capital management focus.

FY25 represented the conclusion of the process, one that has generated substantial returns and continues to provide strong future income and growth options.

The highlights of the year included;

- North Lakes industrial land sale. In October 2024, Garda exchanged contracts to sell North Lakes for $113.6m. FIRB approval was received in December 2024, with construction completed in July 2025. Settlement is in September 2025.

- Cairns’ office sale, its landmark 15-storey office in the Cairns CBA, was the last of Garda’s office properties. The sale, which will be completed in August, will secure proceeds of $77.5m.

- Successful property management. 15,287m² of industrial property was leased across a range of assets.

- Increased capital allocation to lending. At year-end, Garda has lent $44m, with a loan book consisting of 14 active loans in higher-yielding debt.

Once all the proceeds are collected, leverage in the fund will fall to a mere 14%.

Trading at $1.27, the company is trading at a significant discount to NTA. The discount neither reflects the existing asset nor the flexibility the balance sheet provides to pursue new opportunities in the medium term.

The quality of the remaining portfolio assets, all industrial land in the Brisbane suburbs, benefits from tailwinds associated with changes in supply chains, along with the underlying Olympics-related growth and investment.

Conclusion

To sum up, we continue to see value in Beach’s core gas assets and the future cash flows they could generate, particularly as Waitsia comes online and spot-linked pricing lifts revenues. However, recent reserve downgrades, looming execution risks, and the company’s pivot toward M&A introduce significant uncertainties.

The share price reflects excess caution at the current level, but there is less upside than when we initially established the position. We will continue to monitor the key outcome of the company delivering FCF growth in 12-18 months.

The information in this article is of a general nature and does not take into consideration your personal objectives, financial situation or needs. Before acting on any of this information, you should consider whether it is appropriate for your personal circumstances and seek personal financial advice.