Read the previous week’s Investment matters.

Photo © vladimirsukhachev from Via Canva.com

Copyright 2025 First Samuel Limited

The Market

The results

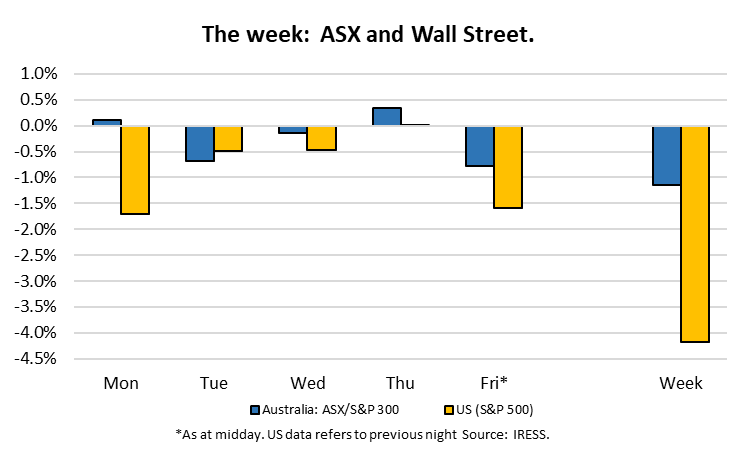

Reporting season concluded last Friday amid relatively soft conditions in the market. Uncertainty regarding Trump and tariffs and a gradual unwind in the momentum we have seen in pockets of global equities has put pressure on the ASX.

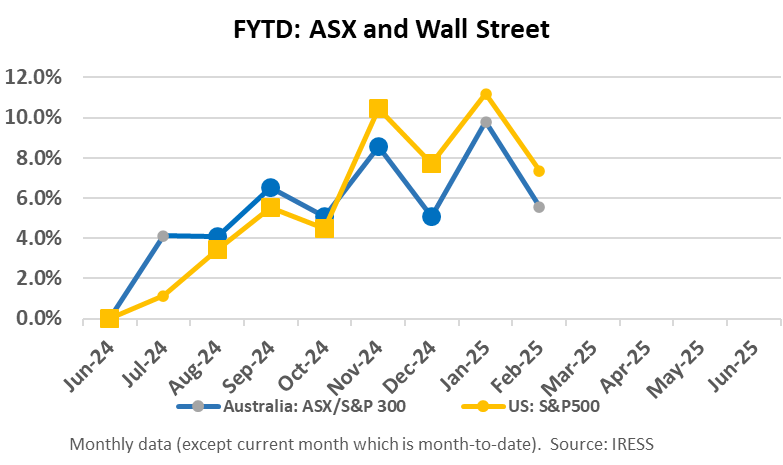

The ASX300 fell almost 4% during February, reversing gains made in January. Clients’ Australian equities sub-portfolios performed better than the market, with a rotation towards value stocks and miners.

This week, we saw improvements in Australian GDP growth rates, as reported by the ABS. When combined with slightly higher house prices, employment strength and stable credit growth, there remains significant uncertainty regarding the scope and timing of future RBA interest rate cuts through 2025. The economy may not need cuts despite the pain inflicted on mortgaged households.

In this environment, we anticipate that investment fundamentals such as free cash flow yield, earnings reliability and book value of assets will be more relevant.

In the final days of the reporting season, we saw results from two portfolio companies, our brief assessment is in the table below.

Investment Matters in March will concentrate on reporting on the portfolio companies that were not covered in detail in previous weeks. This week, we will highlight the results for Worley, Cleanaway, Emeco, and Steadfast.

Steadfast (SDF) – continued consistent growth

Steadfast operates a market-leading insurance broking and agency operation that has produced consistently excellent returns in its business (and share price) since listing on the ASX in 2013 at $1.20 per share.

Steadfast delivered its 1HFY25 result on the 25th February.

We viewed the result as “neutral” and the stock price has fallen 4 per cent since the result.

Enviable track record of growth since listing

Source: Company reports

The key underpinnings of Steadfast’s success as a business have been;

- Underlying increases in Insurance premiums, upon which SDF’s brokers earn a commission

- The level of demand for insurance coverage in the community, including coverage of new risk classes such as cyber insurance

- Increasing operating scale within the business, which allows the spread of corporate, head office and technology development costs over a broader client and business base

- Stickiness of insurance broking subsidiaries, which are attracted to the benefits of accessing the Steadfast underwriting platform, operational and administrative benefits from Steadfast’s business protocols and also an ability to unlock value in their franchises via the progressive sale of their businesses

- Strong stewardship by an experienced senior executive team.

1H25 Trading Results

The 1H25 result showed consistent growth in Gross Written Premiums (GWP) and accordingly Group profits.

Steadfast Broking and Underwriting– Australasia – it’s largest businesses

Broking GWP growth was 7.9% year-on-year, of which:

a) underlying growth was 5.2% across the various classes of business and products;

b) with a further 2.6% growth coming from additional (sometimes partial) acquisitions of network brokers.

Ongoing acquisitions of insurance broking businesses have been a progressive driver of growth since the Steadfast business was created. During the 1H25 period to end December, Steadfast added equity holdings in 16 new insurance franchises and increased holdings in 9 existing enterprises in which it already had an interest. Offsetting this, the company reduced its holdings in 5 network businesses.

SDF Consolidated EBITA margin by Division

Source: Company reports, Barrenjoey

Its Underwriting agencies, its most profitable operations, delivered even stronger growth in GWP of 11.7% yoy, of which 7% was organic growth and 4.7% was from recent acquisitions.

Steadfast International – Long term growth opportunity, particularly in the US

While Steadfast has been progressively developing an international presence, this medium-to-longer term growth opportunity was accelerated with the acquisition of the ISU network in 2024. The US market is a demonstrably larger insurance market than Steadfast’s domestic market but one where insurance broking has less utilisation and insurance broker ownership is more fragmented. The US operations will likely form the backbone of International growth over the next decade.

Initial signs for ISU have been positive, with Profit-sharing revenue growth of up 15%, and the business is expected to outperform the FY25 EBITA target set for the company.

Strata – a frustrating issue being put to bed

Strata building insurance and management has been a growing but problematic industry. It is one where regulation has been diverse across states, oversight has been lax, and disclosure has often been inconsistent and opaque. Accordingly, the complexities between (a) Insurance Companies (which carry the risk), (b) their Underwriting agencies (which are given limits by insurers to place business), (c) Insurance Brokers (which seek quotes and handle administration on behalf of the Body Corporates) and (d) Body Corporate managers (which may be professional entities for a fee but otherwise may be often-underqualified and/or dis-interested apartment owners) as well as Building maintenance services (which attend to insurance claims) has not been well understood.

There are many parties that stand between the insurance company and the owners of apartments and townhouses! There has also been a declining level of interest amongst Insurance companies to underwrite insurance in this area given the administrative intensity of this insurance segment, growing levels of portfolio concentration as peers have withdrawn and a low level of risk-adjusted returns.

In September last year, ABC’s 4 Corners program presented an ‘expose’ investigation into the domestic Strata Management industry, within which Steadfast is the largest placer of insurance business into the Australian market as an insurance agent and also having an underwriting placement capability with insurers such as QBE.

Despite Steadfast having taken a leadership role in underpinning the provision of insurance in the Strata market, having increased the professionalism of services to Body Corporates and having recently sponsored an industry-wide review into the industry which had been shared with Governments and regulatory bodies, the 4 Corners program had questioned industry practices and had sparked investment community concerns about the ability for Steadfast to be able to continue to expand its business profitably. This had resulted in a sharp retracement of its share price by 10% in a week and from which the share price is only now recovering to.

There have not been any regulatory interventions or inquiries in response to the 4 Corners program at this stage. It’s an issue from which Steadfast does not believe that it offers a conflict of interest nor has a need to withdraw its services. Management has been ‘steadfast’ about this!

Earnings outlook

Moderation of insurance premium rate increases to mid-single digit levels in aggregate, had been expected for some time by the experienced investment bank research analysts who cover the Insurance industry, but nonetheless, seen as a point of modest concern by some investors/traders in the equity markets who use short-term momentum as a basis for trading shares.

We note Steadfast’s enviable track record of delivering strong growth in earnings and executive incentives which require the company to meet Return on Capital/Equity targets (appropriately set in excess the company’s cost of capital) as well as delivery double-digit EPS growth.

Cleanaway (CWY) – one man’s trash….

We like the ‘privileged assets’ that exist within the company’s waste portfolio (including more significant landfill sites closer to the distribution of the population, meaning more efficient waste processing) and also view Cleanaway as a beneficiary of both ongoing population growth as well as the shift towards renewable energy in this country.

In the event of poor execution by management, we also believe that these waste infrastructure and land assets would have strategic value and be sought after by operators like Seven Group Holdings (SGH) or private equity firms.

Cleanaway delivered its 1HFY25 result on the 25th February.

We viewed the result as “neutral” and the stock price has fallen 2% since the result.

Blueprint 2030 growth strategy

In mid-2023, Mark Schubert, the incoming CEO laid out his strategic and financial ambitions for the company’s medium-term in its ‘Blueprint 2030’ Strategy.

Substantial uplift in earnings growth to come – EBIT > $450m in FY26

The company has set out the path to significant growth in earnings (EBIT = Earnings Before Interest and Tax) and returns over the next 2-3 years. Importantly for shareholders, executive incentives are focused on an earnings target of $500m (Mission 500), revealing significant ambition.

Achievement of these financial outcomes is to be driven by:

- operational efficiency initiatives including fleet transformation, Branch optimisation including the restoration of the troublesome Queensland Solids business, transformation of its Health Services business and an improvement in labour productivity which thus far has remained a little elusive within CWY (and within the Australian economy more broadly!);

- recovery in market conditions (predominantly in its core Metropolitan Regional Landfill (MRL) and Construction and Demolition Waste (C&D) business); and

- strategic initiatives such as landfill gas capture and expanding its footprint and services in Western Sydney MRF, Victoria CDS and its Food and Organic Waste (FOGO) transition as well as bolt-on M&A opportunities

The 1H25 result

Heading into the result, the market’s primary focus had been on the maintenance of stated earnings guidance – FY25 underlying EBIT target of $395-425m

While the 1H25 underlying EBIT result was a little softer than analyst expectations, pleasingly, the company’s management reiterated that it leaves the business on track to meet its FY25 guidance. A range of improvements across the company are continuing to uplift company profitability.

Cleanaway – Progression of profits since FY22

Source: Company reports

One disappointing element of the result was a higher than anticipated cost associated with the recent fire at its St Mary’s Liquid Waste operations in NSW. The interruption to this business is expected to be up to 6 months and for $20-40m net of insurance. This will be excluded from company earnings guidance for the full year.

While it is common practice for ASX companies to treat such incidents as ‘one-offs’ or ‘extraordinary’, we think such incidents are incurred in the ordinary course of a high-risk business. So too, large IT or restructuring initiatives are also part of the ongoing requirements of operating a company over the longer term and should not be excluded from earnings commentary and executive remuneration.

While the company still battles labour productivity challenges, a more judicious approach to managing capital expenditure and continued uplift in landfill levies will assist in 2H25.

Cleanaway is also assisted by Government focus on environmental requirements, increasing specialisation and value-added handling of both:

a) renewable associated with ‘Energy from Waste’ technology and

b) Per-and polyfluoroalkyl substances (PFAS) decontamination processes. PFAS chemicals are used in Scotchgard treatments and some firefighting applications.

Emeco Group (EHL) – Higher cash but limited market interest

The long-held position in Emeco has been profitable in FY25, with the share price rising by more than 20%. The rise in share price has reflected improving industry conditions, increasing confidence in 2025 operating earnings and an expectation that Emeco would produce strong cash flows in FY25.

Emeco delivered its 1HFY25 financial results on 19th February.

With the company generating free cash flow of $49m in the six months ending December 2024 and increasing the cash in its coffers by $32m (after dividends) over the same period, we rated this result amongst the best the company has achieved in recent years.

The market was less impressed with the stock returning to levels seen in November 2024, down 8% since the result, and 4% worse than the market.

The company is valued only at $450m, despite being on track to make $80m in cash in FY25. Emeco remains amongst our client’s cheapest portfolio positions with a net tangible asset backing of more than $600m and earnings momentum.

The discount that the company’s share price currently trades on (more than 20% to NTA) is a function of three issues in our minds:

- Uncertainty regarding the future level of growth-oriented capital expenditure. Ultimately strong operating earnings are of limited value if all funds are reinvested in uncertain growth. Emeco has historically not achieved an optimal balance between returning cash to shareholders and growth capex. Improvements in this balance over the past 12 months can now be rewarded if progress continues through FY25.

- Uncertainty regarding the intentions of the major shareholder Black Diamond. Owning more than 40% of the company, Black Diamond continues to creep higher, putting at risk the capacity of the company to execute a trade sale or pursue a merger with another similar company.

- Uncertainty regarding the business model. We appreciate Emeco’s model, which combines equipment refurbishment, mid-life equipment optimisation, integrated workshops, and a full-service operational model. However, the price paid for such business is ultimately measured in operating margins achieved and underlying ROC (return on capital). Until recently, both have been slightly below expectations. The following charts show the improvement in recent reporting periods.

Emeco – Margin recovery – Operating EBITDA and EBIT margin

Source: EHL 1HFY25 Results Presentation

Emeco – Return on Capital (ROC) improvements

Source: EHL 1HFY25 Results Presentation

Any resolution to uncertainty regarding the three issues will reduce the discount to NTA.

Balance sheet strength is now an asset

With its Net Debt/EBITDA ratio now only 0.8x and expected to reach 0.6x by the end of FY26, the company is at the lower end of its capacity to hold and service debt. Net Debt to EBITDA ratio tells us how many years of operating earnings are required to repay its debt. A ratio of 1 would indicate that the business needs to operate for 1 year to repay its debt (excluding interest and tax).

In a capital-intensive business backed by high-value mining equipment, we are comfortable with an elevated level of debt, and the net debt-to-EBITDA ratio could comfortably be as high as 1.75, especially if we have confidence regarding the value of assets, the level of utilisation and reasonably priced interest costs.

Emeco has a management target ratio of 1.0x, indicating that its balance sheet already has some capacity for additional debt.

Balance sheet optionality is critical for a business such as Emeco. We anticipated that in the coming 12 months, the company will use this strength to refinance its existing A$250m. Other options include resuming dividend payments (last paid in September 2023), increased use of buybacks, or selective acquisition of distressed assets.

Investment view

Exposure to mining services businesses remains a key thematic in the portfolio. Australia is underinvesting in mining development, despite our natural endowments, reliance on mining exports and new opportunities in various materials.

ABS National Accounts suggest that mining real capital stock per capita is going backwards. Historically periods of underinvestment have reversed rapidly. As underinvestment turns to rapid reinvestment, shortages are created in labour markets and equipment availability. In tighter, higher utilisation markets, the returns to existing assets, and spare capacity become elevated.

Owning mining services companies such as Emeco, Develop Global, Imdex and Perenti for reasonable prices, when each generates strong operating cash flows, with the promise of cyclical upside, remains attractive.

Emeco is expected to narrow its discount to NTA delivering strong returns through 2025/6.

The information in this article is of a general nature and does not take into consideration your personal objectives, financial situation or needs. Before acting on any of this information, you should consider whether it is appropriate for your personal circumstances and seek personal financial advice.