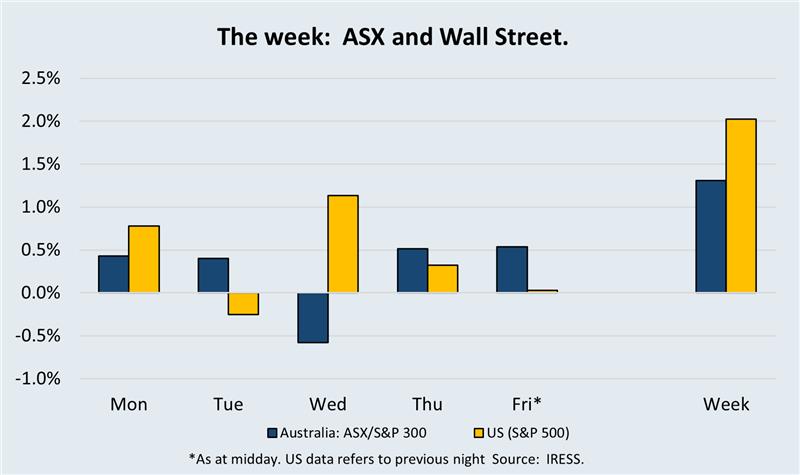

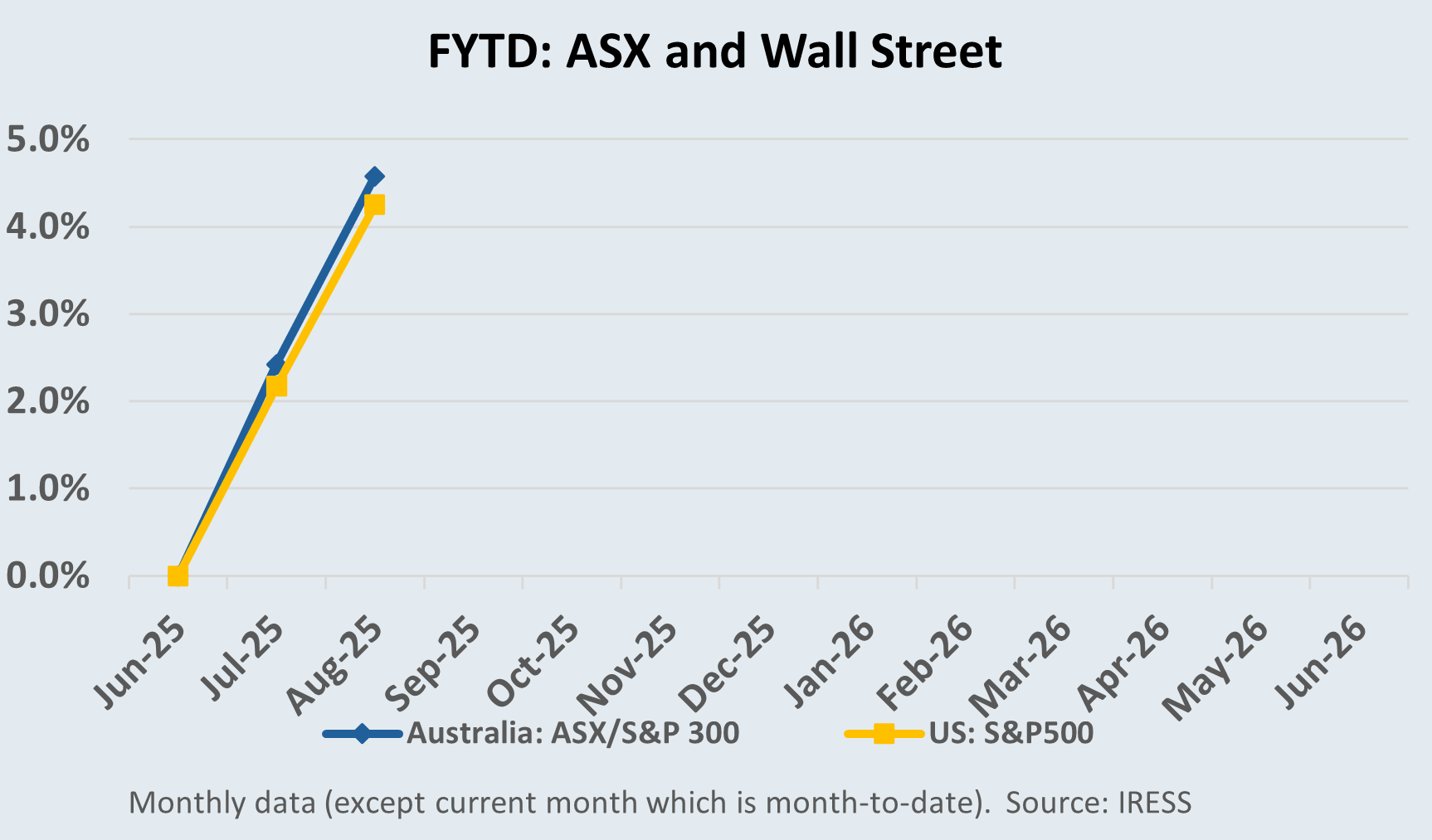

Deeper into Profit Reporting Season this week, with several portfolio companies reporting results. We flagged in recent weeks that we expect significant volatility in share prices associated with this year’s results. Twenty years ago, share price changes were more muted, but several issues have arisen that increase the volatility of results in ASX’s two reporting seasons in February and August.

- Global trends. Especially in the US, the higher volatility surrounding results has built an expectation in the global markets that a weaker-than-expected result will result in a relatively larger fall, and vice versa.

- Lower turnover in other parts of the year. Markets now have lower levels of trading turnover outside the reporting season period. We have less efficient markets in these periods. So when the opportunity for the combination of new information and higher trading volume arrives, price discovery in the trading on results day is more likely to find a pent-up equilibrium value.

- Passive index investment: Higher levels of index-hugging investment throughout the remainder of the year generate significant trades, which are not motivated by a desire to own a particular stock, but simply due to flows of money in and out of the market in general.

- Stale earnings estimates. Commentary will often refer to earnings estimates and whether a company met or exceeded expectations in its results. Twenty years ago, there were more publicly available forecasts by analysts, and these estimates were updated more regularly and monitored closely by companies. Today, public forecasts are more likely to be inaccurate and hence increase the potential value of different private views of active managers such as First Samuel.

- More important post result trading. Despite the higher volatility on the result day, we now see an opportunity over the following 7-10 days of trading for some of this volatility to wash out, as portfolio managers build new positions, the market and broker analysts have the opportunity to update their modelling.

The first two weeks of this reporting season have indeed delivered an outside number of companies whose share price changes by more than 7 per cent on the day. This will provide active managers, such as First Samuel, an opportunity to build positions at cheap prices and trim positions whose share price substantially exceeds our valuations.

For the next four weeks, Investment Matters will update clients on all the results for portfolio companies in a simple table that outlines the share price impact of the results, along with short notes on our views of the results. Readers should expect to see occasions in which we believe the result was positive, yet the share market reaction was the opposite, and vice versa. Such mismatches are often due to the difference in investment timeframes. We are assessing company results with a medium-term valuation perspective.

In the remainder of the document, we will provide more details on the larger portfolios’ positions and results of significance for our long-term valuations. When companies such as Origin Energy, which report late in the week, the longer description of the results will be retained for the following week. Occasionally, commentary on small positions in smaller companies will be retained until post-reporting season in September.

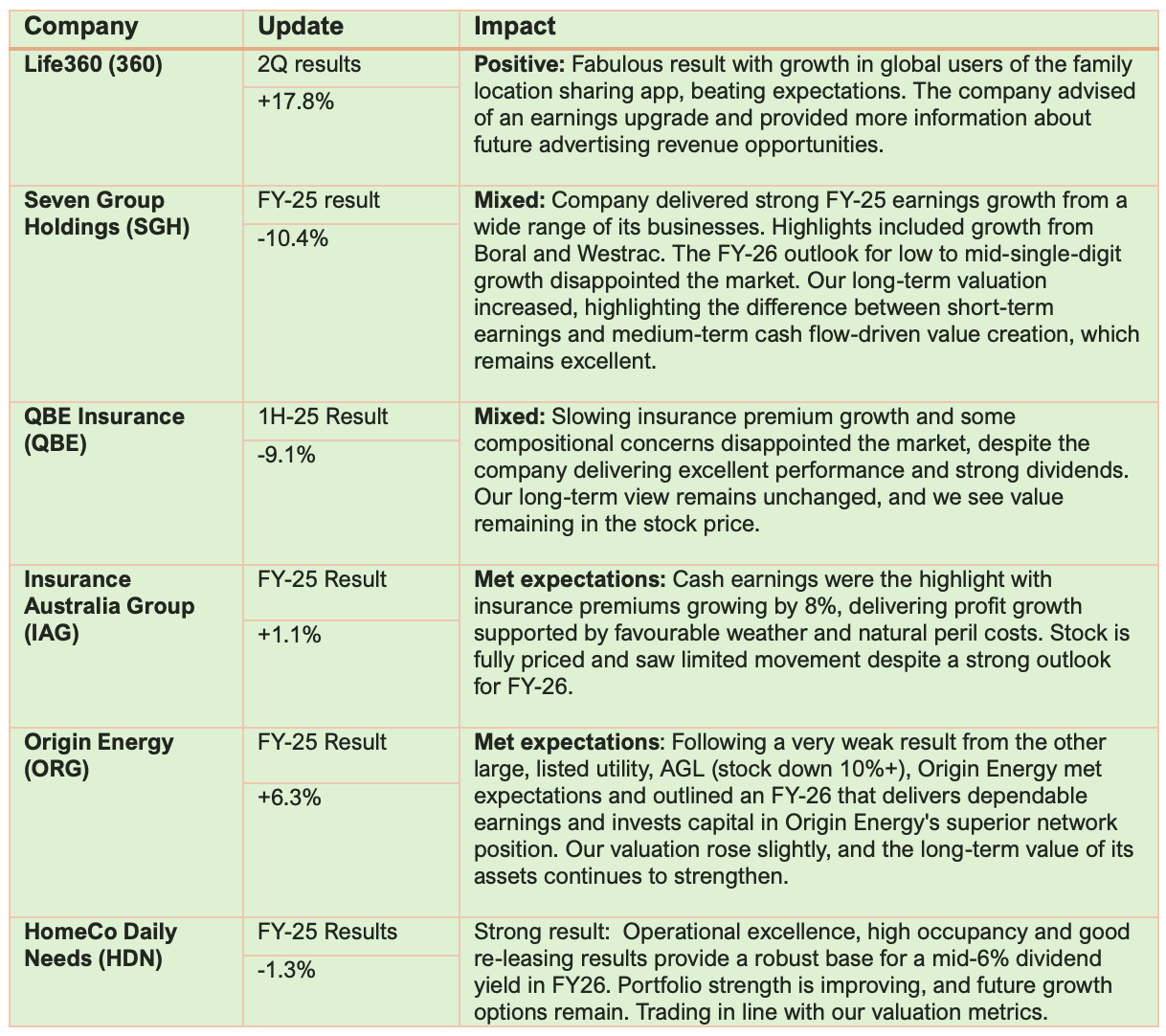

This week, we present detailed result commentary for Life360, QBE and SGH.

Read the previous week’s Investment Matters.

Copyright 2025 First Samuel Limited

The Market

Table 1: Company updates in early August

Life 360 (360): Tracking to higher profits

Life360 is now amongst the largest positions in clients’ portfolios, despite being a more modest position when first purchased in late 2024. Life360 is a location-based technology company specialising in family safety and connection. Its core offering is a freemium mobile app (launched around 2008), allowing users to create private “Circles”—typically family groups—to share locations, messaging, send alerts, and enable enhanced features.

Life360 delivered an impressive second-quarter performance this week. Reflecting its operational strength, the company upgraded its full-year guidance.

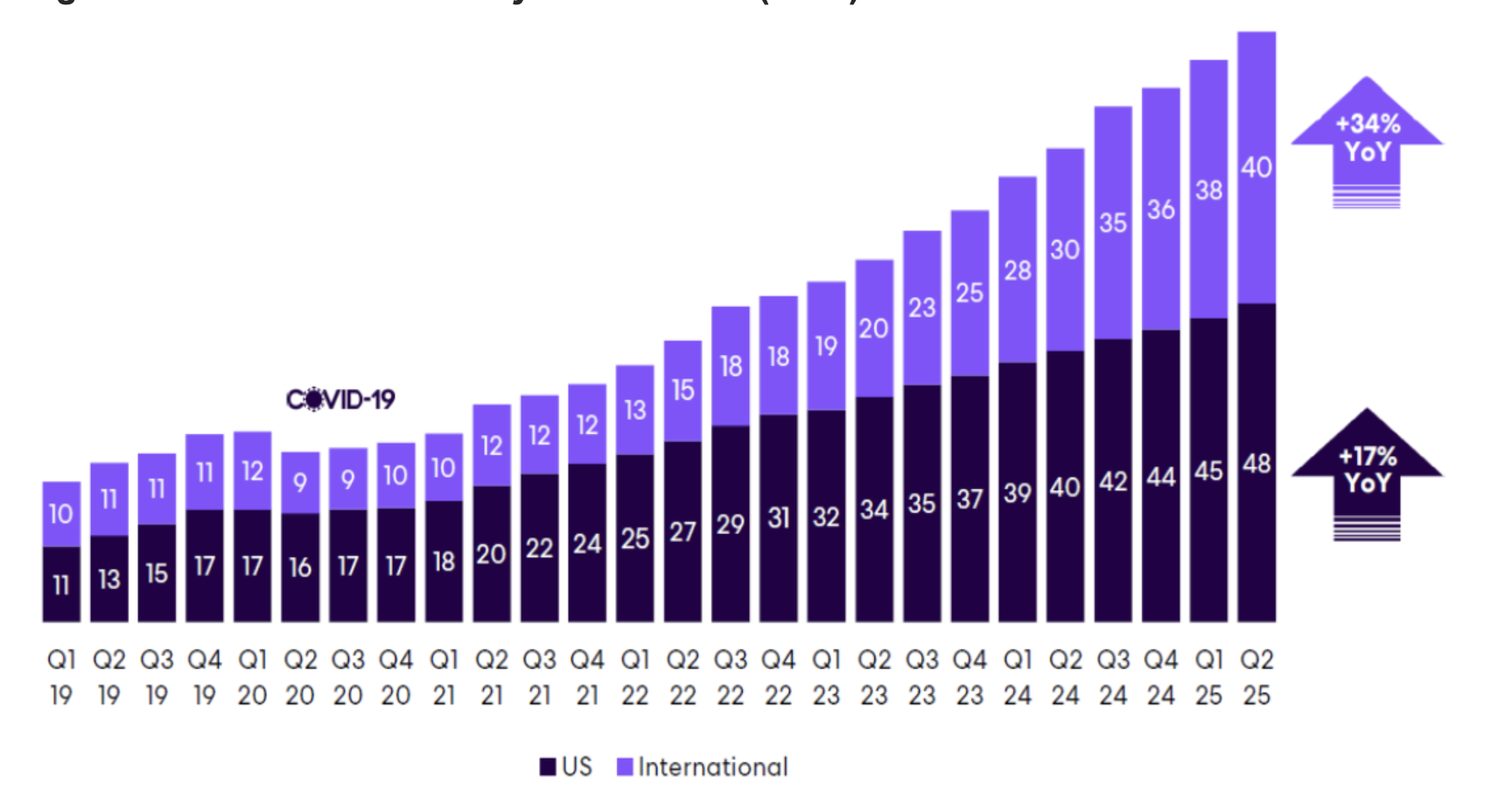

- Monthly active users (MAUs) surged by 25% year-over-year, reaching 88 million, up from approximately 70 million in Q2 2024.

- Paying Circles—the company’s premium subscription groups—grew as well, adding 136,000 new paying customers, bringing the total to about 2.5 million subscribers.

- The company turned profitable on an accounting basis; it has been profitable on an operating basis for longer.

- Revenue for the quarter rose 36% year-over-year to US$115.4 million. The pace at which Life360 turned the increase in revenue into higher profits, known as marginal productivity, was truly impressive.

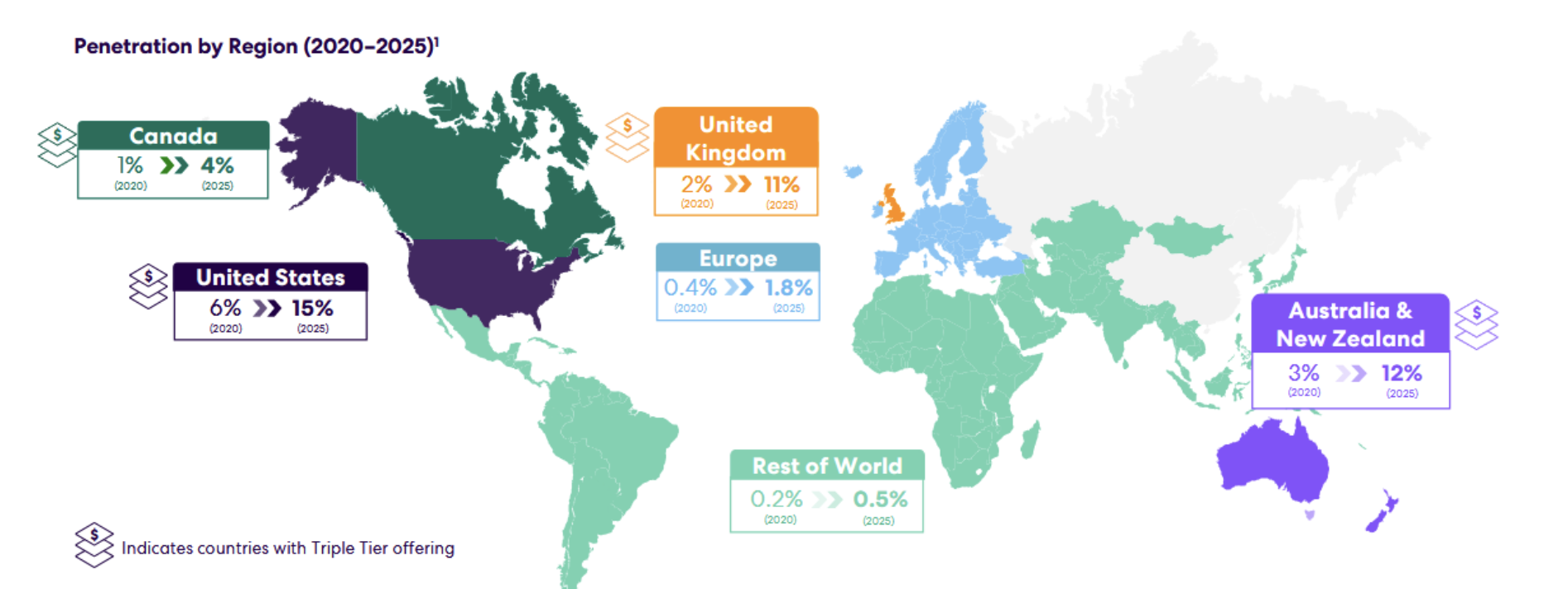

The breadth of app usage across the globe (Figure below) and the strength of its growth since 2020 are indicative of high levels of social change underpinning its usage. The 12 per cent usage in Australia refers to the percentage of the smartphone-enabled population that are Life360 members, a number which has grown from 3 per cent in 2020. With such a large number of users, there are exciting possibilities for the company to explore various monetisation options, which include but aren’t limited to Paying Circles. Its ambition for paying users is to evolve into a “super‑app” for families, encompassing safety, connection and other services. As Life360 has already achieved profitability with a smaller fraction of paying users, 2.5 million paying out of 88 million users, the runway for profit growth remains significant.

Life360 usage by region

Source: Company data

Along with strong operating outcomes, the company upgra›ded its full-year guidance. Revenue guidance targets now range from US$462 million to US$482 million, while adjusted EBITDA (a measure of operating profit) guidance has been lifted to US$72–82 million.

By the close of trading in Australia on Thursday, the stock had surged by 17%, reaching new all-time highs.

Likely driving the upgrade in expectations is the continuous quarter-on-quarter growth in users, as clearly shown in the chart below. Note the mix of both US and International growth.

Life360 Core Monthly Active Users (MAU)

Source: Company data

Our thesis in originally owning the company was that the market is underestimating the future growth in advertising-related revenue. Targeted, location-based advertising is likely to be extremely valuable in the future. The value of advertising not only includes the capacity to serve ads to users, but more importantly, leverage partnerships (e.g., with Uber) and deterministic location data to deliver personalised promotional content.

Extending their advertising capacity to compete with the likes of Facebook and Google is also a possibility. Today, when a website looks to sell advertising, it relies on a platform such as Facebook and Google to monetise its site by sending it traffic based on the type of site it is, and the type of customers or users who would appreciate the content. To do this, you need to know a lot about the user, and this is where Google and Facebook have built an enormous competitive advantage. Not only do Google and Facebook have sites, including YouTube and services, including Gmail, of their own, but they are also the infrastructure that sits behind the internet, serving advertising and collecting information that makes the internet profitable.

It is possible that, given the depth of connections Life360 has already built, along with the unique information it collects about location and family connections, it can be an effective alternative to Google and Facebook within the broader architecture of the internet.

In this respect, the room for more revenue growth may still be universally underestimated.

In terms of direct advertising, it is essential to note that there are already many globally successful apps that are monetising free services, including Spotify and Snapchat. These services can generate from USD$3-5 per user over the year. For instance, Spotify will generate more than USD$2.0bn in revenue this year.

Leadership change

In a planned leadership transition, Lauren Antonoff—formerly Chief Operating Officer—has been appointed Chief Executive Officer, effective early August 2025. Chris Hulls, co‑founder and long-time CEO, will transition to the role of Executive Chairman, focusing on product strategy and long-term vision. She brings experience from previous roles at Microsoft and GoDaddy, and emphasises Life360’s mission in the “anxiety economy”—providing peace of mind to families. She also highlighted growth potential in pet tracking and targeted ad offerings, such as the Uber partnership.

The discussions we have had with management and former employees universally highlight the client experience first approach that the company has emphasised. The key lead in this endeavour was Chris Hulls, and in our view, this will remain a critical determinant of future success.

Seven Group Holdings (SGH): High quality and higher expectations

Seven Group Holdings (SGH), a long-held and successful position in client portfolios, is a diversified investment group with interests in industrial services, media and energy sectors. Seven Group’s significant assets include the well-known dealer of Caterpillar products in WA/NSW/ACT called WesTrac, Coates Hire, the national equipment hire business, the building materials company Boral, and smaller holdings in ASX-listed Seven West Media (41% ownership) and Beach Energy (29%).

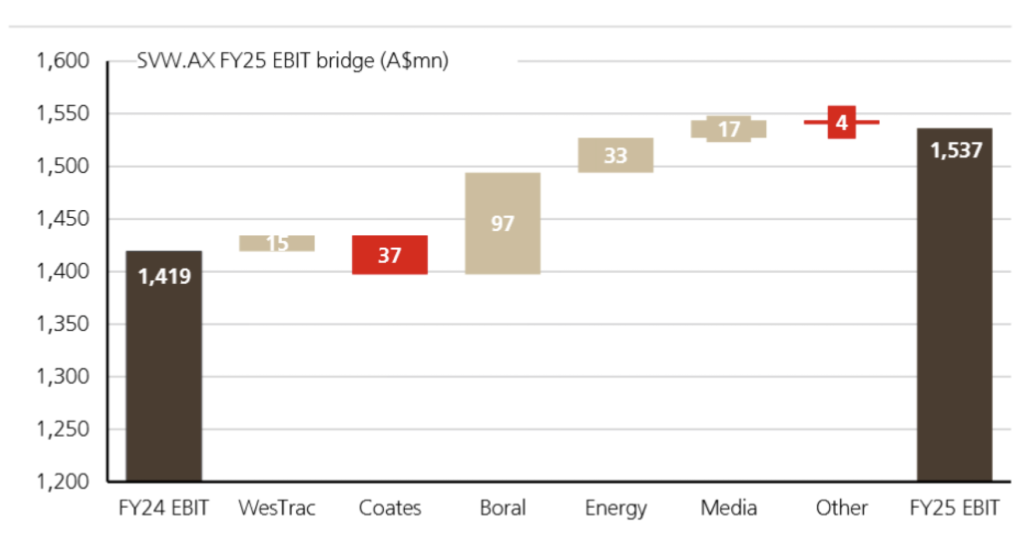

SGH delivered a robust FY25 result, growing EBIT (earnings before interest and tax, but after depreciation on capital charges) from 1.42 to 1.54bn. Cash flow was the highlight, and the team continued to reduce debt, enhancing a financial position that is now well-positioned for new investment.

Figure # below shows the contributions to EBIT growth, with additional earnings from Westrac, Boral and Energy. Weakness in Coates Hire was expected based on a slowing national economy and building sector.

FY25 EBIT bridge – consistent profit growth across group businesses

Source: Company data, UBS

Despite the strong earnings, the SGH share price sold off this week due to a weaker outlook for FY26 than the market expected. Although SGH is often conservative when providing forecasts to the markets, market expectations for FY26 proved too high.

Clients will note that we found the SGH share price extending beyond our valuation, prompting ongoing trimming in our position at these price levels and higher. SGH retains the scarce combination of significant assets, high-quality management, and a cash flow focus that we favour. The challenge with such a position is the price we are willing to pay, and the possibility of a decline in share price when lofty expectations are not met. Our approach is to trim our position in strength and look for opportunities that emerge over time to add when the share price is weak. We have sold 25 per cent of our position in the past 14 months, but still favour SGH as a long-term hold.

Highlighting the difference between short-term market movements and long-term value, the FY25 result prompted the rare combination of a 6 per cent increase in our long-term valuation, but an 8 per cent fall in the share price.

We anticipate an opportunity to add back to our position will emerge in FY26, especially coinciding with any acquisition activity the team undertakes.

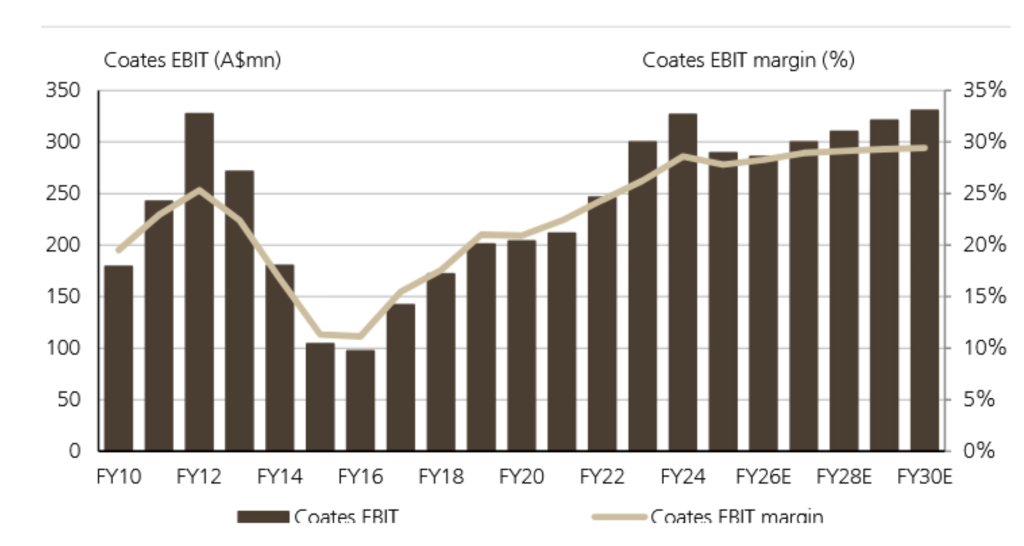

The stumble this year in Coates Hire earnings is shown in the Figure below (note the fall in EBIT between FY24 and FY25). The scale of improvement achieved in the past decade has been impressive, with significant improvements in operating activities and capital management driving the result. UBS estimates shown for FY26 through FY30 highlight ongoing growth expectations that are broadly consistent with our modelling, although we expect limited improvement in FY26. The facts in our mind point to Coates currently generating adequate returns on capital, and hence future growth from here is dependent on the strength of the Australian economy and construction.

Coates – Small stumble in FY25

Source: Company data, UBS

Outlook

Medium-term EBIT growth benefits from a range of cyclical tailwinds, including continued mining machinery maintenance and fleet replacement activity; sustained infrastructure investment, utilities and defence spending. Any recovery in Australian residential construction approvals will be a bonus.

Updates to the FY26 earnings growth guidance throughout the year will be highly anticipated by the market, and the added focus for FY26 will be on any M&A activity.

QBE Insurance Group (QBE): High quality and higher expectations

QBE released its 1H25 results last Friday and disappointed the market with a set of results that was in line with expectations on profits, consistent with our long-term valuation metrics, but compositionally weaker than anticipated. The share price fell 8 per cent since the result.

Instead of noting the operating strength, improvement in capital position and diversity of growth drivers, the market is now struggling with the outlook for revenue growth in the short-term. We tend to favour the long-term value is our driver of investment decisions but short-term expectations are also important to the market.

Keeping it simple, because global insurance is far from simple, it is easier for an insurance company to deliver earnings in any given year when premiums are rising fast, and interest rates are rising. Both earnings from the fund’s clients provide the company with increased returns when invested, and higher premiums make it easier to cover the increasing costs of insurance claims.

Indeed, the features of global insurance markets that have delivered clients a 125 per cent total return on QBE since June 2021 were rising interest rates and robust premium growth on the back of global inflation.

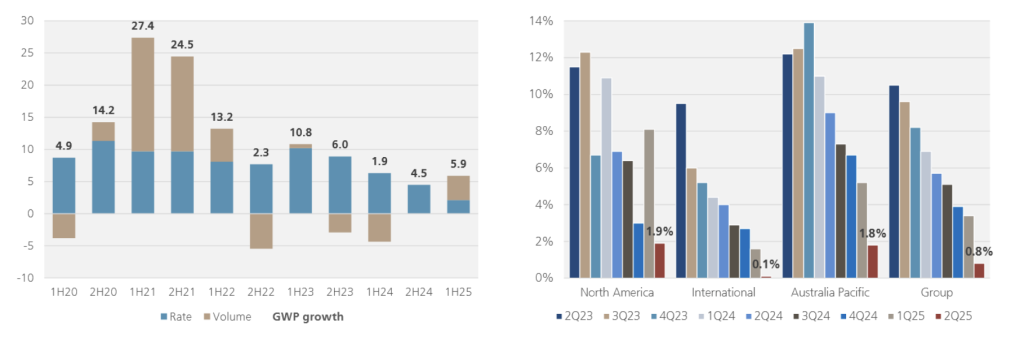

Today, global interest rates are falling, and the chart below shows that the rate of growth in premiums (right-hand side of Figure #) is declining. Running an insurance company is more challenging.

QBE: Growth in premiums by half since 2020 (GWP, LHS) and average premium inflation year on year since 2023 by quarter (RHS)

Source: Company data, UBS

In this environment, we need three features to make investing in a company such as QBE remain attractive.

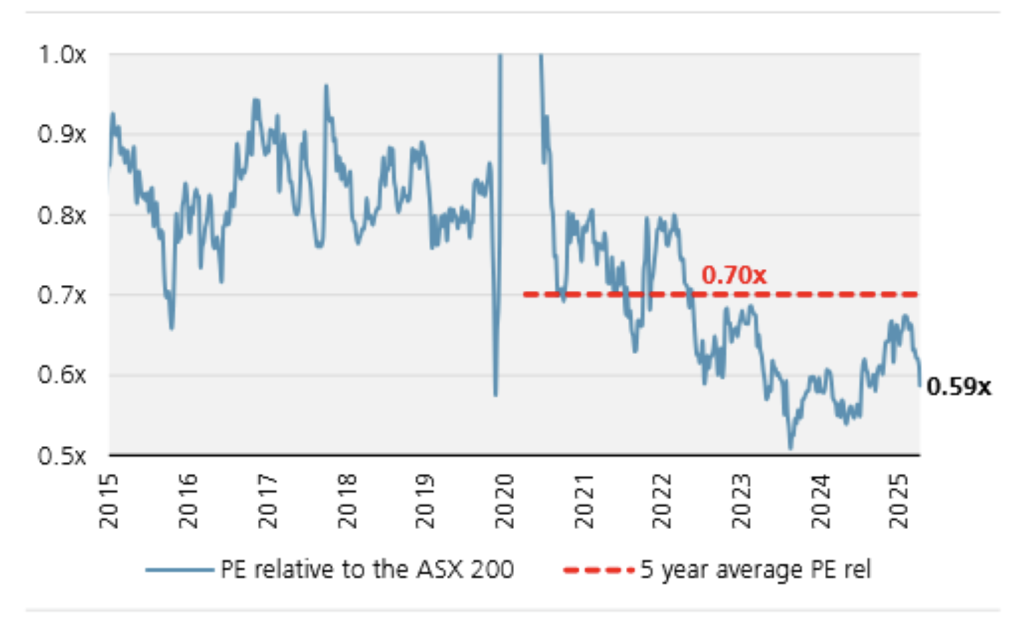

- The QBE stock price needs to be relatively inexpensive. With a forward price-to-earnings ratio (PE) of only 13.5 in an otherwise expensive market for large companies, QBE satisfies this condition.

- The company needs a viable pathway to generate volume growth. In an environment in which premium growth is weaker, volume growth helps the company maintain profits in the face of rising costs of running the company (excluding claims). QBE is beginning to demonstrate volume growth after several years of deliberate and prudent volume attrition, whilst premium growth was strong.

- The company needs to be good at insurance. The Combined ratio (COR) is a measure of the profitability of an insurer’s day-to-day underwriting activity. It is a measure of claims-related losses and expenses as a percentage of premiums earned. QBE has continued to deliver on COR in 1H25, and we anticipate a range of factors will see QBE maintain its COR at current levels over the next 2 years.

QBE: Remains attractive on a relative PE basis compared to the ASX200

Source: FactSet, UBS

Like SGH, we have managed our QBE holding conservatively in FY25/6 as the company delivered strong above-market returns. We have generally sought to trim as the price has risen above our valuation. We anticipate the opportunity to add to our position in FY26 in the event of further share price weakness.

The information in this article is of a general nature and does not take into consideration your personal objectives, financial situation or needs. Before acting on any of this information, you should consider whether it is appropriate for your personal circumstances and seek personal financial advice.