Copyright 2025 First Samuel Limited

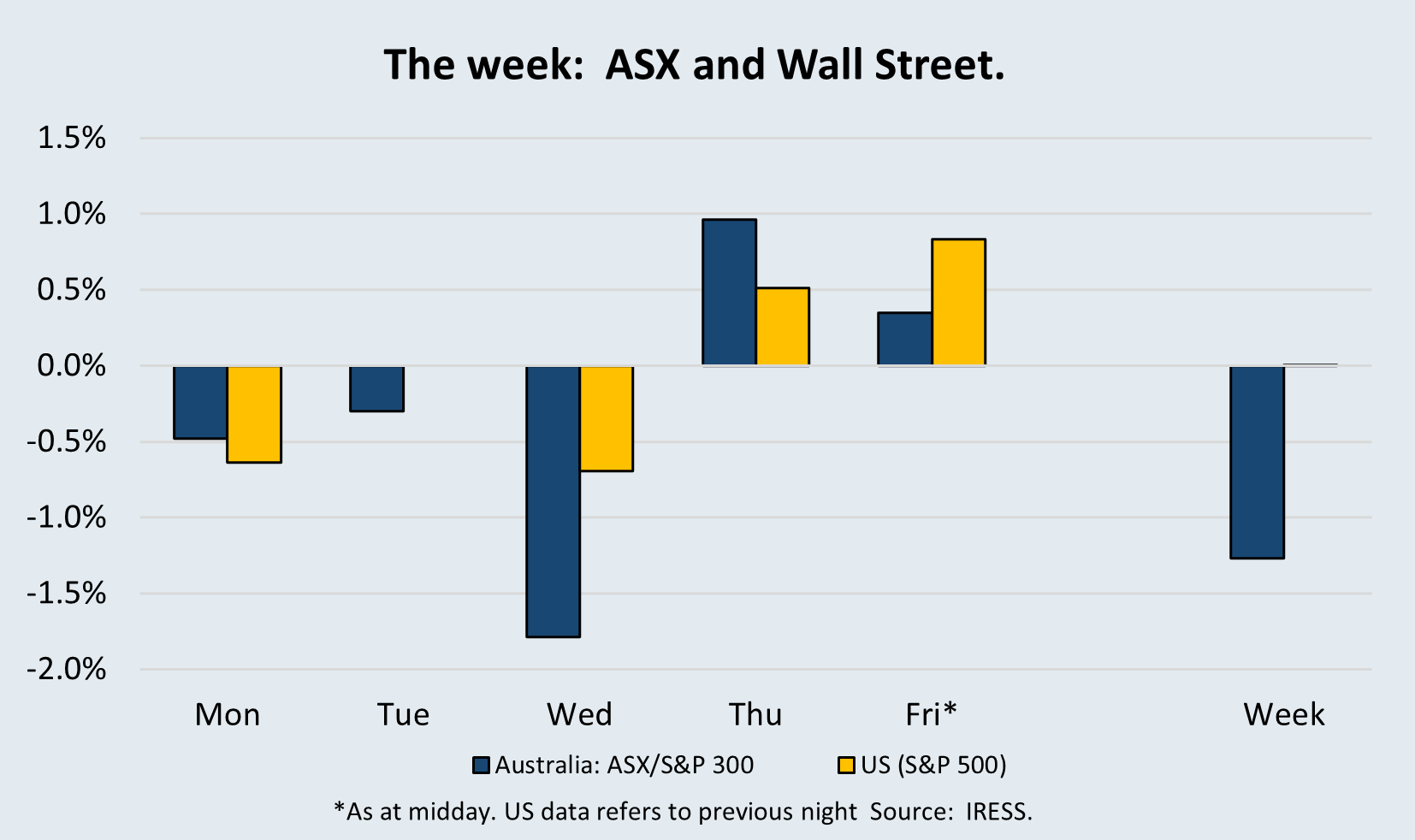

The profit reporting season concluded last week, and we were pleased with the overall market growth and the relative performance of our client portfolios.

This week’s Investment Matters covers some interesting economic data and results from three portfolio companies, EarlyPay, Helius and Inghams.

Read the previous week’s Investment Matters.

The Market

Some interesting economic data from the Commonwealth Bank

Whilst not a portfolio position, the reporting season result presented by CBA is vital for several reasons. The first often discussed is the impact of the Commonwealth Bank on the entire market, given its extraordinary price and high ASX300 index weighting (>10%). Since peaking at more than $190 per share, CBA has continued to underperform, finishing Wednesday this week at just under $165 per share.

The 2nd reason we look forward to the result is the quality of information that the Investor presentation provides on the business, the broader banking sector and the health of the Australian economy. The first slide in this year’s deck was the most interesting.

We have noted over the past year, the structural weakness in the economy, manifest in weak wages and poor productivity, is colliding with vast intergenerational wealth transfers and a frightening, inequitable tax system.

The impact is a decline in living standards among younger age cohorts and a significant improvement in the wealth and lifestyle of older Australians.

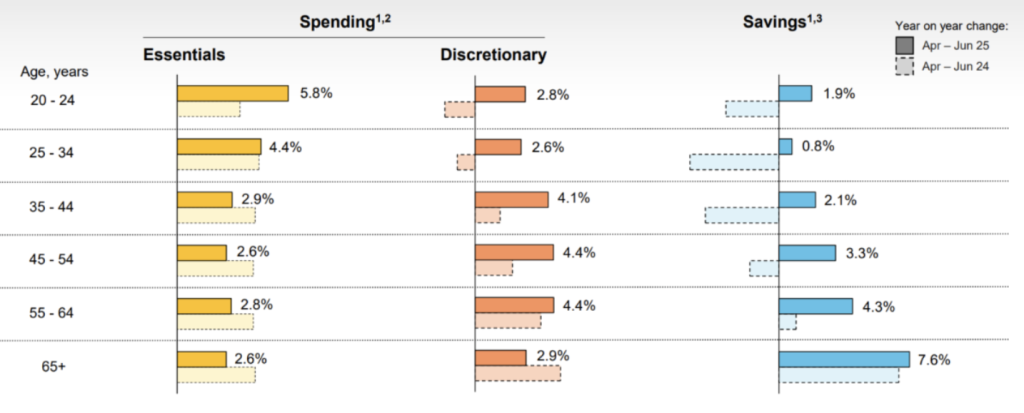

Figure 1 below shows the changes in spending on Essential or Discretionary items, along with changes in the amount of savings for clients. The metrics are derived from CBA customer card transactions (spend) and deposit balances (savings), measured per customer over the 13 weeks to end-June and trimmed to remove outliers.

Figure 1: View of the Australian consumer – Commonwealth Bank account data June 2025

In a perfect world, depending a little on your politics and values, you could see each age group achieving similar growth in spending, perhaps a little more growth in Discretionary vs Essential (“La Dolce Vita”), and strong increases in savings amongst the young, with less savings in mid-life and lower growth in savings amongst the oldest.

Australia is achieving almost the exact opposite.

The highest growth in spending (when aggregated across the two years) is amongst the eldest, with massive real decreases in spending in age groups under 35 over the past two years. The growth rates in the Figure are nominal, including the impact of inflation. Total growth across the two years needs to be above 6 per cent, not have fallen in inflation-adjusted terms.

And weaker spending hasn’t resulted in higher savings; young people are literally worse off.

Every age group under 65 has experienced a decline in real savings, not only a decline in spending. Despite this, we know from other information in the CBA result that total deposits in bank balances are growing extremely strongly. But on average, they are barely growing, and they are falling for the young.

All the wealth in liquid savings (excluding superannuation) is becoming frighteningly concentrated.

The only saving grace is that this year’s numbers aren’t as bad as last year’s.

Some of the other results:

- Essentials spend rose across all ages but was strongest for the young: about +5.8% (20–24) and +4.4% (25–34), then moderating to ~2.6–2.9% for ages 35+—consistent with easing goods inflation for older cohorts but ongoing price pressure on younger households’ must-haves (rent, transport, groceries). The cost-of-living impacts are strongest amongst the young households.

- Discretionary spend was led by mid-life cohorts: ~+4.1–4.4% for 35–64, versus ~+2.6–2.8% for under-35s and ~+2.9% for 65+. That pattern suggests an improvement in confidence among higher-earning, still-working customers, while younger adults remain cautious.

- Savings balances show the starkest generational split: 65+ up ~+7.6% and 55–64 up ~+4.3%, compared with ~+0.8–2.1% for those under 45. Older customers are clearly rebuilding buffers—helped by higher deposit rates and lower housing leverage.

Bottom line: 2025 presents a broadly better picture than 2024, but Australia’s recovery is uneven by age—older cohorts are rebuilding their savings and spending steadily, while younger cohorts are still paying the bills.

EarlyPay (EPY): Mixed result – cheap with growth to follow

EarlyPay released its FY25 results on 26th August, and the stock price is broadly flat since.

Clients will recall that First Samuel has been a substantial shareholder in EarlyPay for many years. The company is an Australian non-bank lender that specialises in providing working capital finance and equipment finance to small and medium-sized enterprises (SMEs). EarlyPay helps SMEs smooth cash flow, fund growth, and invest in assets, positioning itself as a flexible alternative to the banks.

Key Financial Results

Underlying NPAT (Net Profit After Tax) rose to A$5.1 million, a 24% increase from the previous year. Earnings per share improved to 1.9 cents per share, up 30% (FY24: 1.4 cents per share). Considering the stock trades in the range of $ 0.20 to $0.25 per share, the underlying earnings represent a significant return to existing investors.

Although profits rose, EarlyPay, already a small company, is not growing very quickly. Net revenue was A$33.7 million, a decrease from the previous year. Invoice financing was the slower-growing segment, with the amount outstanding (lent to businesses) falling through FY25.

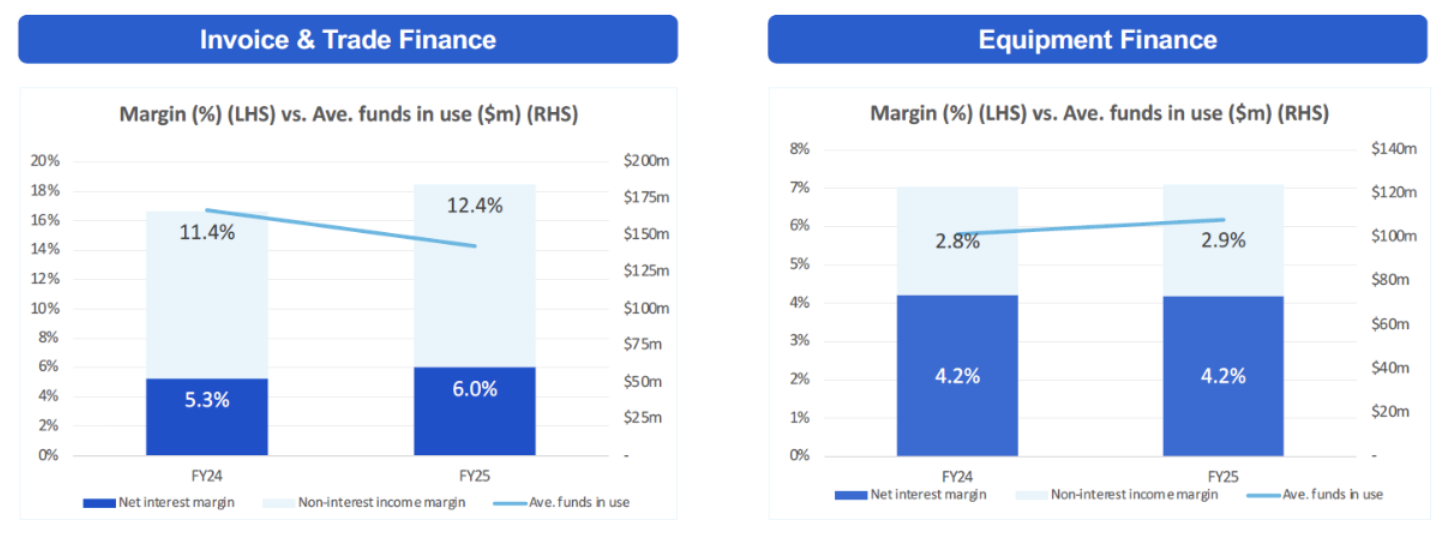

Figure 2: Where is the momentum in EarlyPay?

Although revenue was falling, the net revenue margin increased to 13.4%, indicating that the company is now generating more profit on lower volumes. Lower credit loss expense (halved to 0.75% of Funds in Use) was a testament to improved process.

Higher margins and lower bad debts added to reasonable operating outcomes and created an operating cash flow of more than A$9 m. The combination of strong cash generation and an improved balance sheet means the company now has a surplus capital position in our view. We can see scenarios in which the company could return up to 5 cents per share to shareholders without impacting the underlying profitability of the business.

Consistent with capacity for capital returns, the company announced a franked final dividend of 0.65 cps. This is the highest dividend since 2022.

The following figures illustrate how the margins in Invoice/Trade finance increased in FY25, despite the average funds in use falling. Equipment finance grew margins and volume, but it is arguably of lower quality, especially if the business is growing in other areas.

Figure 3: EarlyPay operating margins by segment, FY24 and FY25

Source: EPY FY25 Results Presentation

Searching for growth

With solid cash flows, robust capital reserves, and a healthy dividend, the company enters FY26 well-positioned for growth and further margin expansion.

We see two preferred areas of future growth: technology and increased Invoice Financing volumes. Both require the business to engage more closely with a broader range of Australian SMEs. To achieve this, the company needs to either build closer relationships with businesses that already service SME’s in other areas of finance, or it needs to merge with them.

In many respects, EarlyPay has already done the hard work of building the systems and establishing a viable scale in its existing Invoice Financing book. Growth from this point on adds incremental earnings at a very high margin. We would prefer to see Invoice Financing grow.

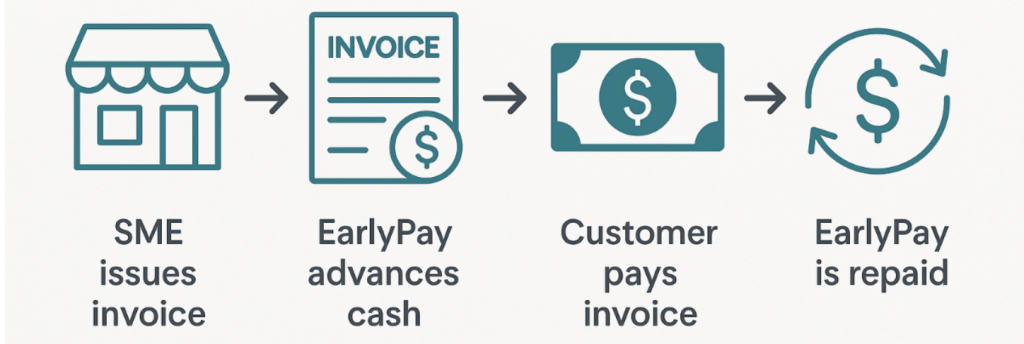

As a reminder, Invoice Finance is where EarlyPay advances cash against a business’s unpaid invoices. Instead of waiting 30–90 days for customers to pay, SMEs can unlock immediate cash flow. This helps cover wages, supplier payments, or growth opportunities.

Figure 3: What is invoice financing?

Source: First Samuel

In the medium term, we see value in EarlyPay continuing to improve its technology. The company already integrates with cloud accounting systems (like Xero and MYOB) to streamline invoice and customer data, allowing businesses to access finance quickly and with less paperwork.

There is also a range of Embedded Finance services that are likely to grow in the medium term. EarlyPay is well placed to benefit from them. The company describes the opportunity to provide fully embedded financial services in non-financial platforms. These platforms would enable EarlyPay to scale at a relatively low cost with attractive margins, especially if it develops strong risk management capabilities.

Corporate Activity

A disappointing element of the FY25 presentation was notification by the company that “Active discussions relating to a potential change of control transaction have ceased”. The reader may recall that in January 2025, the company advised that the Board of EarlyPay confirmed that its corporate adviser, Highbury Partnership, is assisting with strategic initiatives in relation to the Company.

On January 23rd the Australian Financial Review’s Street Talk column reported that “ASX-listed invoice financing business EarlyPay is ready for another spin on the auction block.”

Quoting the AFR from January, “Street Talk can reveal EarlyPay’s board has mandated boutique corporate adviser, Highbury Partnership, to seek bids for the business…”

“Sources said EarlyPay chairman Geoffrey Sam had called in the bankers after learning of its largest shareholder, the ASX-listed COG Financial Services’ intention to sell its 21.4 per cent stake in the company should a decent-enough offer present itself. They added that EarlyPay’s board had decided it was better off hanging the for-sale sign than making a home with a new majority shareholder.”

Since that time, the ASX-listed company Solvar (SVR) has taken a 20 per cent holding.

EarlyPay, of which First Samuel is a major shareholder, has once before headed down the path for sale in 2020. We still view the possible sale of the business as the most likely way to extract value from our long-held position.

Healius (HLS): Simplified business with many options

Healius released its FY25 results on 21th August, and despite a dramatic and inexplicable fall on the day of the announcement, the stock is now more than 5 per cent higher today, than prior to the result release.

The market remains sceptical that the company can control costs, but this result provides initial supporting evidence and medium-term goals that are achievable in our view.

Following the large special dividend payment in FY25, the share price has been weak and represents a high-quality future source of profits in the portfolio. Once again, we retain an eye for the quality of the assets rather than the short-term earnings volatility.

Financial results

Healius reported group revenue of A$1.34 billion, up 5.7% from the previous year, driven by its core pathology business.

Underlying EBITDA of A$239.3 million and the underlying EBIT of A$17 million meet market expectations. We really appreciate the medium-term revenue growth that we can expect from Pathology. Pathology is a critical component of the Australian health care system. There is long-term growth of ~5% per annum, driven by consistent factors including a growing and ageing population, the prevalence of chronic diseases, and the benefits of additional tests.

The group ended the year with a net cash position of A$57.2 million, thanks to proceeds from the A$375.2 million sale of Lumus Imaging, and following the special dividends clients received.

Operations and assets

Healius (HLS) is the second largest private pathology provider in Australia. It has operations across all Australian states/territories, spanning metropolitan, regional and remote areas. Post the sale of Lumus Imaging, it is now one of two listed pure-play pathology providers on the ASX. It also owns Agilex Biolabs, a leading bioanalytical laboratory in the Asia Pacific.

The company has over 2100 pathology sites, including more than 2000 collection centres and almost 100 laboratories.

The other listed pathology provider, Australian Clinical Labs, was a fantastically profitable addition to client portfolios over the past 12 months. Following a quick gain, we no longer hold the position. Interestingly, discussions around a potential merger with Australian Clinical Labs (ACL) resurfaced again at this result. Consolidation could unlock cost synergies, but regulatory hurdles remain.

Healius continues to struggle with the delicate balance in maintaining its top-line whilst keeping costs at bay. We like that an increase in its average fee reflects an improvement in its specialist and non-MBS revenue mix.

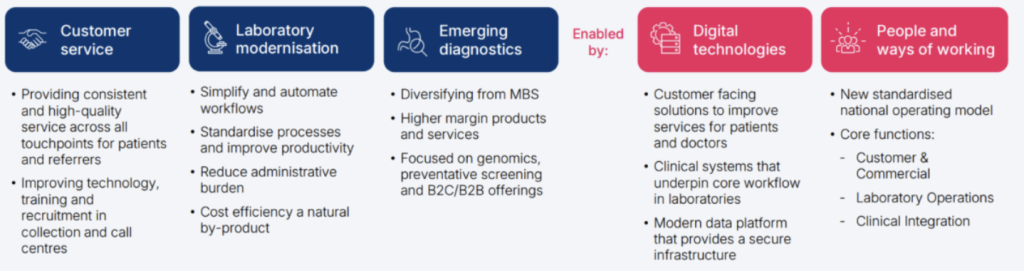

Management’s current plans, shown in the figure below, are both straightforward and achievable. There is significant upside available to the current price if management achieves even 50% of its aims.

Figure 4: Simple prescription for growing the HLS Pathology business

Source: FY25 HLS Results Presentation

In the long run, we believe the market has misunderstood the capacity to permanently and structurally reduce operational costs. Whilst a great deal of focus is on labour, scale and technical improvement, we suggest that greater savings from a restructuring of the property solution and changes in the competitive landscape will be much more critical.

At the recent strategy day, the company emphasised the importance of conducting a critical assessment of independent and medical centre opportunities in existing and targeted catchments and actively undertaking property lease negotiations. There are gains to be made by adopting a whole-network lens and exiting sites that do not meet benchmark metrics. This will take several years to achieve.

On a positive note, we have found that the market analyst focus is now shifting toward FY26 execution—particularly on delivering savings and operational improvements in the second half. Delivering on expectations through FY26 is likely to unlock the more than 30 per cent upside value we see in the current share price, excluding any value created through corporate activity.

Inghams (ING): Cheap chickens – slow roast required

Inghams released its FY25 results on 22nd August. There was a dramatic sell-off of 20 per cent on the day, and the stock has continued to sell off since, falling another 5 per cent.

Clients sold a portion of their position, reflecting the time expected for Inghams to recover from the earnings dent experienced in the 2HFY25 period. This hit is likely short-term (12-18 months) in nature, and we anticipate increasing our holding again in the medium term.

We continue to appreciate the long-term growth, high-quality assets, and market position of Inghams. We also recognise that there will be short-term fluctuations in pricing, feed costs, timing of customer contracts and capital spending programs. These fluctuations provide an opportunity to trade the stock in line with our long-term valuation.

But the simple fact is that a weak wholesale chicken price impacted Inghams’ earnings in late FY25 and risks any growth in FY26.

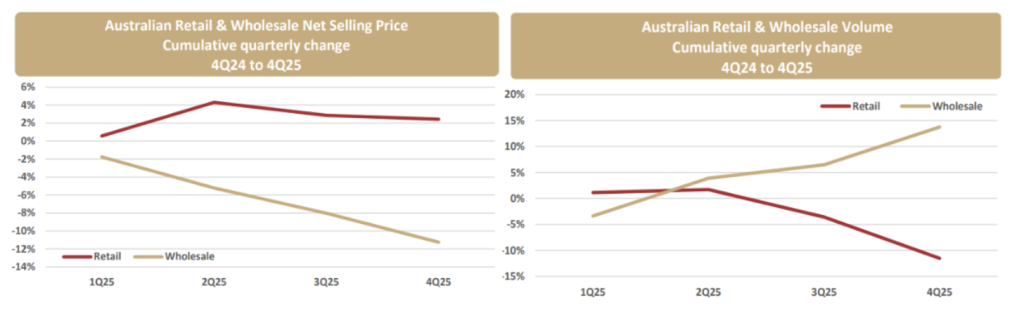

The figures 5 below show what happened. The wholesale poultry net selling price (NSP) fell significantly, down approximately 10% year-over-year, reflecting acute pricing pressure in this channel. At the same time, the amount of chicken that Inghams was required to sell in this channel continued to grow.

Our interpretation is that Inghams has flooded the wholesale market with chicken it couldn’t sell due to changes in its customer contracts announced at the last results.

Figure 5: Weak wholesale prices and more volume impacted Inghams’ earnings

Source: FY25 Inghams Results Presentation

Financial results

Inghams Group reported flat underlying EBITDA at A$236.4 million, broadly flat on the previous year, but it was the pace of the deterioration in pricing and volumes that dominated the result.

Multiple brokers downgraded their ratings in response to the soft outlook. With the ASX generally displaying more volatility than in previous years, a significant reaction was almost guaranteed, especially considering investor sentiment amid uncertainty around wholesale pricing was largely unexpected.

The oversupply arose because Inghams thought it could replace the lost Woolworths volumes. Oversupply will hurt Inghams’ “forecast 1HFY26 EBITDA but then should correct itself as production is reset.

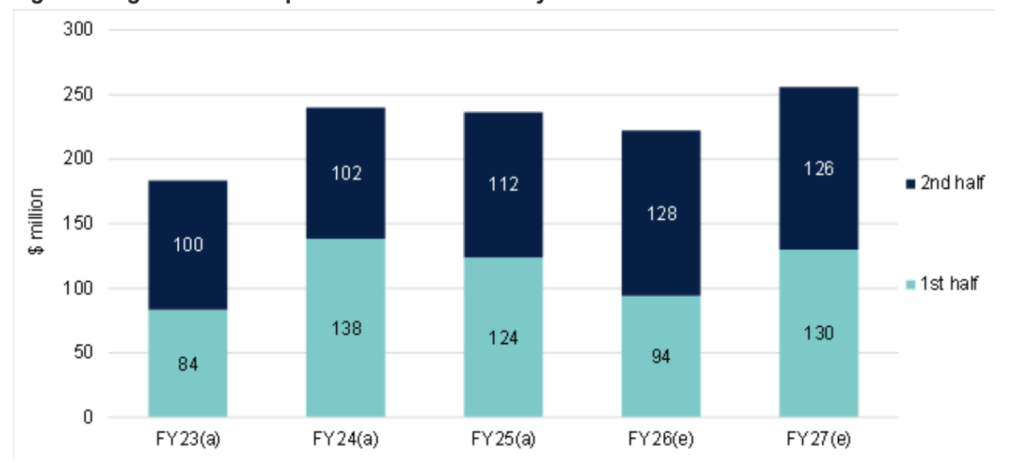

The excellent analyst Craig Woolford from MST Marque provided the following chart of Inghams’ earnings. Note the expected decline in earnings in 1HFY26 and the subsequent rebound in earnings for FY27. We suspect it may be possible to achieve a quicker than expected rebound should additional operational changes soak up remaining excess volume.

Figure 6: Inghams EBITDA pre AASB-16 outlook – by half

Source: Company reports, MST Marquee

Medium-term support remains

Clients will appreciate that we have been able to build significant positions in Inghams when the market was overly pessimistic and sell when excessively optimistic.

We suspect the market misunderstands how well-behaved the chicken meat industry is, and simultaneously understates the strength of the long-term trends in demand, improvements in efficiency of production, and changes in consumer tastes, which create additional value.

We believe that Inghams is worth closer to $3.50 per share, and should the competitive balance in the market return upside to $4.00.

The information in this article is of a general nature and does not take into consideration your personal objectives, financial situation or needs. Before acting on any of this information, you should consider whether it is appropriate for your personal circumstances and seek personal financial advice.