Read the previous week’s Investment matters.

Photo © STILLFX from Via Canva.com

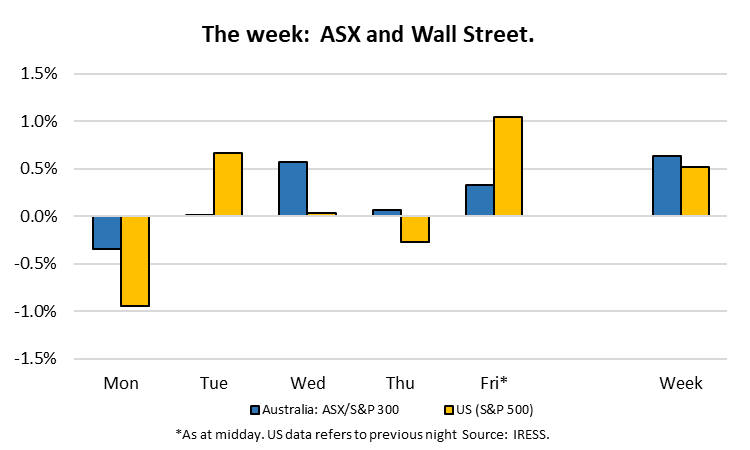

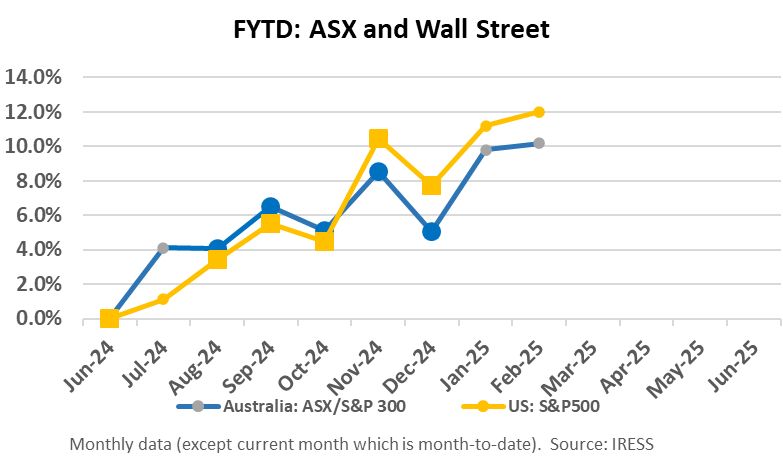

The Market

Reporting season begins in earnest

Each of the following month’s Investment Matters will provide a review of key stocks that have been reported. The reviews are designed to provide context covering;

- How the financial and operating update could change our view of the company, especially our outlook for future growth.

- Exploring the new options and overlooked value that the result provides clarification or insight into; and

- The market’s reaction to the result, our overall impression, and the share price change.

In addition, we will include a table (below) of all of the portfolio companies reporting and brief notes on each.

| Company | Our view | Share price reaction to close 13/2 | Notes |

| Core equities portfolio | |||

| Macquarie Group | Positive | 3.7% | Met expectations: is the earnings upgrade cycle about to start? |

| SGH Limited | Positive | 9.5% | High-quality result – only minor blemishes from Coates Hire. |

| Imdex Limited | Positive | 9.8% | Cost-based discipline was evident in the 1H25 result. Operating leverage into FY26e is apparent should conditions improve. Fully priced, however. |

| Other sub-portfolios and portfolio preferences | |||

| HomeCo Daily Needs | Positive | -1.7% | Strong portfolio of neighbourhood centres and good execution – some development upside – well priced, good dividend. |

| IAG Group | Mixed | -12.6% | Operationally great result. The market focused on premium price growth moderation and a dividend which was light versus expectations. |

| CSL Limited | Negative | -6.1% | Weak demand in specialities and from recent acquisitions. Growth limitations highlight weak upside to current share price despite core business strength |

This week’s Investment Matters will concentrate on two large holdings Macquarie Group and SGH Limited (formerly Seven Group Holdings).

Macquarie Group 3Q trading update: Nearing the end of the earnings downgrade cycle?

Macquarie Group is one of our largest portfolio holdings. Along with Judo Bank, it is our preferred way to gain access to the Australian Banking sector rather than holding prohibitively expensive shares in the four major banks.

Macquarie Group is, of course, more than an Australian domestic banking business. It is a global investment company with significant businesses in Asset Management, Investment Banking and Advisory, Commodities and Markets Trading as well as also being the operator of the fastest-growing domestic banking franchise over the past decade.

Macquarie Group has global reach

Source: Company reports

With so much variance in its operations, geographically and by line of business, its earnings performance is also prone to variability. While the company has an unblemished record of generating profitability over the past ~50 years, it does naturally feature cyclicality in earnings with movements in asset prices, market volatility and activity, and currency shifts.

Current trading performance

Broadly, Macquarie delineates its four divisions

- Macquarie Asset Management

- Banking and Financial Services

- Macquarie Capital

- Commodities and Global Markets

As either Annuity-style (which has steadier, more predictable revenue profiles accordingly) or Markets-Facing (which has more seasonal revenues associated with trading activity. The split of earnings is broadly even across the two designations.

Near-term factors influencing results

Source: Company reports

While 9-month financial year-to-date NPAT is reported to be broadly in line with FY24, the implications drawn for the 3Q was that, in the aggregate, earnings were a little softer than the pcp and run-rate of the first half.

Currently, Macquarie’s annuity-style businesses are continuing to grow steadily and impressively, being ’substantially up’ on the 3Q last financial year, with performance fees accruing within the Asset Management business (in part from the successful sale of AirTrunk) and ongoing growth in customer lending and deposits in its Banking and Financial Services division.

By contrast, its Market-facing businesses have continued to struggle to replicate the cyclical high earnings generated in the 2022 and 2023 fiscal periods.

In particular, the Commodities and Global Markets business has been unable to match the ‘supernormal’ profits earned in the spike in Oil prices as the Russian invasion of Ukraine commenced and the opportunities created in Gas Pricing in the US Winter in calendar 2022.

End of the earnings downgrade cycle?

Still, for the past seven quarterly disclosures, earnings have generally disappointed, so the investment community has been seeking an end to the decline. In a stock market which has been heavily earnings momentum-driven for each of the past 2 years, this has likely been somewhat of a hand brake upon share price performance.

That Macquarie has indicated that FY25 earnings would be in line with FY24 was seen as a positive factor by the market and the bump in share price on the day reflected this.

As is apparent from the company’s 3Q earnings disclosure, Macquarie is currently generating a Return On Equity (ROE) which is about 30% lower than the long-run average achieved over the past 18 years.

Long run Returns on Equity – currently in a trough

Source: Company reports

Long run return outlook is exciting

We think that there are significant medium to long run opportunities for Macquarie Group to be able to continue to find high-return, high-growth investment opportunities.

The organisation’s entrepreneurial spirit, high-calibre and long-serving talent pool, risk disciplines and reinforcement via a lucrative and long-term focussed remuneration structure are all ingredients that have spurned a long-term financial services success story.

Identifiable in our reasons for having confidence in Macquarie’s medium-term prospects is that the organisation:

- has made early and significant investments in data centre capability within its Global Asset Management business.

- has well-developed capability in Infrastructure and Green Energy/Renewables within its Macquarie Capital and Asset Management franchises.

- remains a leader in trading the largest commodities markets such as Oil and Gas; and

- has the best-performing domestic banking franchise, which has made significant investments in its technology capability.

No change to our view or position

We did not change our long-term views on the outlook or valuation of Macquarie Group. The position is an attractive alternative to the expensive Big Four banks, and critically it provides a diversified exposure to growing and sustainable markets.

In an era of global underinvestment by business, increasing local opportunities as supply chains are shortened, and the perpetual opportunities provided by catch up infrastructure investment in Western economies, Macquarie Group provides world class solutions.

SGH Limited (formerly Seven Group Holdings) 1HFY25 Result

(Positive, stock up 9.5%)

High-quality results but priced for optimal outcomes

Clients will recall that SGH (formerly Seven Group Holdings) has been a portfolio position since late 2022, purchased for approximately $20 per share. SGH had initially bought a stake in the once-struggling Boral Limited, a stock clients acquired at low prices in 2019.

We were attracted to the commitment that Seven Group made to continue to grow its business through pursuing active management of its portfolio, and a concentration on free cash generation.

This period’s results highlight their core approach, as outlined below.

- Committed to serving our customers

- Disciplined execution to achieve sustainable, long-term growth

- Strong cash flows support the efficient use of leverage

- Owner’s mindset fosters performance and accountability culture

- Operating leverage focus to drive incremental margin

Each makes perfect sense and is closely aligned to our approach in valuing companies.

Since 2022, the SGH management team led by Ryan Stokes has optimised the Boral investment, arguably the first management team in over a decade that has correctly understood the pricing power and operational excellence embedded in the Boral Australian assets. The company have been assisted by a strong government-led investment cycle but have also been held back by a subdued housing construction market, especially over the past 18 months.

The group’s Caterpillar mining equipment and servicing business (Westrac) has continued to generate strong cash flows, and the dedication to detail apparent in the operations of Coates (Hire) has driven margins to a level we did not expect.

The combination of the economic cycle, increasing trust in management, and the removal of a perceived discount due to the conglomerate nature of the Group’s operating structure has seen the stock price rise from around $20 to close above $50 per share this week.

As the share price has grown, we have trimmed our position, but it remains a significant one in client portfolios. At this share price, we are balancing the desire to retain such a high-quality, well-run, and strategically well-placed company with the risk of owning the stock moderately higher than our long-run valuation.

This result highlighted three issues relevant to the balancing act we are executing as an investment team.

- Operational excellence and pricing power in Boral and Westrac are driving higher margins.

- The market is now assuming that Boral margins will remain elevated despite apparent cyclicality in returns over the past 25 years.

- Weaker economic activity in construction-related sectors, especially Victoria, drove lower utilisation and weaker financial outcomes for Coates. This highlighted the risk of assuming a higher long-run valuation for a fundamentally cyclical and capital-heavy business.

WesTrac ( Caterpillar licensee in WA & NSW )

For almost two decades increasing tonnes of production in the mining sector has helped grow Australia’s wealth. For most companies and especially for government coffers, the price these tonnes are sold for is much more important than the number of tonnes mined.

For a company such as Caterpillar (US-listed) the critical factor remains the tonnes mined and aged of the equipment used to mine it. The more tonnes, the more equipment, the older the fleet, the more likely it needs maintenance and replacement.

For Westrac, the SGH company that sells, services, and provides parts for Caterpillar, the growth in the number of tonnes mined has led to a powerful combination of capital sales, service revenue, and spare parts.

This is highlighted by the next graphic

Cycle of mining equipment

Source: Company presentation

The increase in revenue, along with the EBIT margin achieved, is shown in the chart below.

After consolidation in the mining malaise of FY14-FY18, the rise in Australian Terms of Trade has facilitated ever-increasing revenue and mildly expanded EBIT margins.

WesTrac earnings performance over time

Whilst we expect that WesTrac can maintain healthy EBIT margins, we are also conscious that sales are no likely to continue to expand at the same rate. Westrac revenue has benefited from a falling AUD and global inflation. Whilst technological improvements in Caterpillar equipment are likely to provide some real price growth in the future, the cyclical nature of this business also needs to be included in our valuation. In 1H25, we saw the impact of declining prices for parts as an example of factors that will limit meteoric revenue growth in the medium term.

Long-run EBIT margins for Boral

We owned Boral when SGH first purchased the company, and the thesis for owning the business was aligned with the thesis that SGH management used to justify the acquisition. We thought that margins were artificially low and pricing power was poorly-utilised.

SGH has proven that margins can rise, generating a huge increase in EBIT ($m) as shown in the chart below (including forecasts (FY26 onwards) by respected UBS analyst Nathan Reilly). We are not convinced that Boral can sustain EBIT margins at these levels after covering the company for nearly 20 years but acknowledge that there are some change of industry dynamics with several powerful international players now having a stronger influence. However, we will not value the Boral business as if these margins can be sustained, preferring to consider a “through the cycle” EBIT margin closer to 11 per cent.

This is the risk for the current SGH share price- exceptional business and management and great fundamentals but a share price that will take some time to grow into.

Boral EBIT ($M) and EBIT margin (%) – including UBS forecasts

SGH will continue to grow through acquisition

Another way of finding growth is continuing to acquire businesses at great prices, replicating the success seen with the Boral transaction across other Australian industrial businesses. In order to do this without significantly reducing the influence of existing shareholders, including the Stokes family, requires SGH to have a healthy balance sheet.

One of the factors that the market has perpetually worried about regarding SGH is balance sheet leverage. Leverage (Debt/EBITDA) is expected to moderate to c.2x by the end-FY25 (2.5x is generally considered as a high rule-of-thumb threshold by some in the investment community), stoking interest in potential inorganic investment options. Despite decades of proven capacity to manage debt and acquisitions in an “aggressive” manner, the market continues to swing wildly on the leverage equation. The market overly rewards SGH for achieving lower leverage and overly punishes the company share price when it has higher levels of debt.

We see a range of industrial companies, both listed and unlisted, that would suit the combination of existing interests and SGH’s investment philosophy. A number of portfolio holdings we hold would be suitable for SGH ownership.

Conclusion

SGH is a great company which has produced a fine set of results and has opportunities for additional corporate activity to add value. But we feel the stock is also somewhat fully priced. SGH will remain a core holding but one we would not be surprised if we had opportunities to add to at lower price levels in coming years.

The information in this article is of a general nature and does not take into consideration your personal objectives, financial situation or needs. Before acting on any of this information, you should consider whether it is appropriate for your personal circumstances and seek personal financial advice.