Copyright 2025 First Samuel Limited

Read the previous week’s Investment Matters.

Tuesday was not just about the Melbourne Cup

At Investment Matters, we try to avoid focusing on the minutiae of economic and interest-rate policy. Consuming seemingly endless writing on perceptions of the Reserve Bank (RBA) and changes in the underlying data may be a staple for the investment team, but not necessarily critical to Readers.

But there are exceptions, and the changes over the last week, including the RBA’s decision to hold the cash rate at 3.6% on Melbourne Cup Day, as widely expected, deserve attention due to their impact on markets and the Australian economy.

Respected commentators at Barrenjoey wrote “the overwhelming message is that the Board is highly uncertain on inflation and the labour market, and slightly more concerned about inflation at present.”

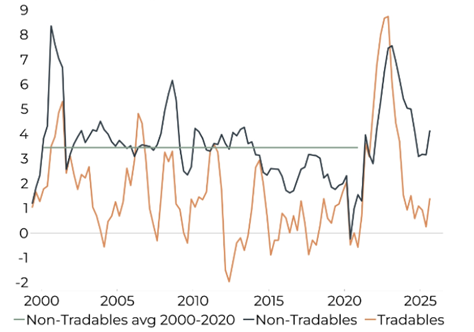

In early October, we wrote in Investment Matters that recent economic data had shifted the narrative surrounding monetary policy in Australia. While global inflation has shown tentative signs of moderation, the Australian experience highlights the structural persistence of price pressures in ‘non-tradable’ (i.e. services, utilities, and administration) goods and services.

Figure #1: Non-tradeable inflation remains too high for rate cuts, per cent year on year

Source: ABS MacroBond, Barrenjoey Research

This is critical because non-tradables represent the most domestically driven component of inflation, are deeply connected to labour market conditions, administered prices, and sectoral concentration, and are the least responsive to monetary easing.

Data from the ABS released the week before the RBA decision only strengthened concerns regarding non-tradeable inflation. We have positioned your portfolio for persistent inflation and a slower course of interest rate reductions.

All about domestic inflation pressures

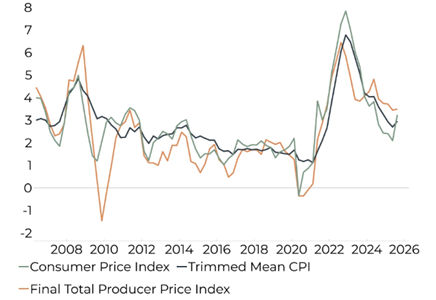

We won’t re-prosecute our case for inflation persistence, but we would highlight that the RBA is concerned about tensions in the labour market, which could risk higher wage growth, and that recent evidence from producer prices (the cost of inputs to producers) continues to rise.

Consistently strong input cost inflation worryingly suggests the Q3 inflation ‘shock’ wasn’t just a one-off – but was supported by cost-push fundamentals. Inflation in construction is clear, and the services sector remains strong.

Figure #2: Producer price inflation is higher than consumer prices, per cent year on year

Source: Barrenjoey Research

This is where the structural inadequacies of the Australian economy are highlighted. Slightly stronger economic growth in H1 25 and persistence in input cost growth drove a reduction in discounting behaviour across firms. The oligopoly structure of the Australian economy does not support price competition. Hence, the risk is that the green line on the chart above moves towards the orange rather than the other way around.

Higher rates: banks’ and retailers’ P/Es unsustainable

Without imported deflation from China, which we suspect is no longer guaranteed, and certainly should not be relied upon as part of economic policy, our inflation rate will be permanently above the RBA target range. So long as the target rate remains at current levels, the risk of higher than required rates remains.

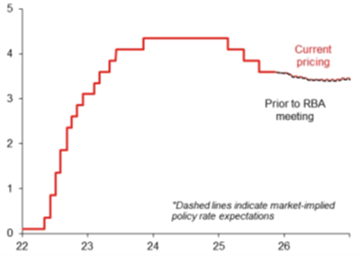

Our underlying concern for positions in banks and retailers is that rates need to remain at similar levels to today. The chart below shows market rate expectations, which now suggest limited downside in rates over the next 12 months.

We would argue, however, that current mortgage rates are already too high for wealth creation and business formation among younger households. As such, the market impact is clear. As economic pressure rises, the PE ratios of the most expensive Australian banks and retailers will look increasingly unsustainable.

Figure #3: RBA Policy rate expectations following inflation upside in November, per cent

Source: Macquarie Research

Woolworths 1Q Sales result

Last week, Woolworths updated the market on its 1st quarter sales. Whilst the overall sales growth of 2.7% is limited, total sales exceeded expectations. CEO Amanda Bardwell suggested sales were “below aspirations” and highlighted intense competition and a challenging market. The ongoing collapse in cigarette sales was a major contributor to the weakness, but subsequent Coles’ sales results showed that Woolworths continues to lose market share.

Clients may recall that we sold out of our Woolworths Group (ASX: WOW) position earlier in the year due to concerns about sales growth and store execution. Conservative clients retained a small holding after starting with a larger position size.

The share price has since fallen more than 11%, while the market has risen 10%. The trade was profitable, and the short-term concerns we have proven real.

In the long run, however, we remain attracted to Woolworths for many structural reasons, including its premier store network, fabulous supply chains, negative working capital position, and its capacity to navigate the shift of customers to an omni-channel world (in-store, pickup, online, and delivery). eCommerce remains a bright spot, with group sales surging 12.9% and penetration reaching 16.2% of total sales,

We were especially interested in levelling off pure delivery growth and an increasing pick-up mix (from 40% to 42.4% since 1Q FY25). In the long run, a higher pick-up mix is likely to drive higher margins (lower cost to serve) and perpetuate the advantage Woolworths has in its network (more stores in better places than Coles)

Figure #4: Woolworths Online sales metrics

Source: Company presentation

In recent months, we have also seen some improvement in promotional efficiency and store execution through our extensive store visit schedule. There really are no shortcuts in improving both beyond cash investment in both pricing and staffing.

Increased promotions, inventory, and staffing investments will stabilise its market share, but it will dent profit margins. We believe that despite this, Australian EBIT can remain positive and within the company’s guidance range.

Following the slight improvement and the share price decline, we added Woolworths back to the portfolio last week. It is only a small position at this stage, because, despite Woolworths’ valuation being appealing in an expensive market, its sales and margin recovery will be gradual and not without risk. We value Woolworths at around $32 per share, after appropriate execution risk adjustment.

The information in this article is of a general nature and does not take into consideration your personal objectives, financial situation or needs. Before acting on any of this information, you should consider whether it is appropriate for your personal circumstances and seek personal financial advice.