Copyright 2026 First Samuel Limited

Read the previous edition of Investment Matters.

In this week’s Investment Matters, we highlight a range of companies reporting season results from SGH Limited, Macquarier Group and HomeCo Daily Needs and provide some commentary from a visit to Perth and Kalgoorlie.

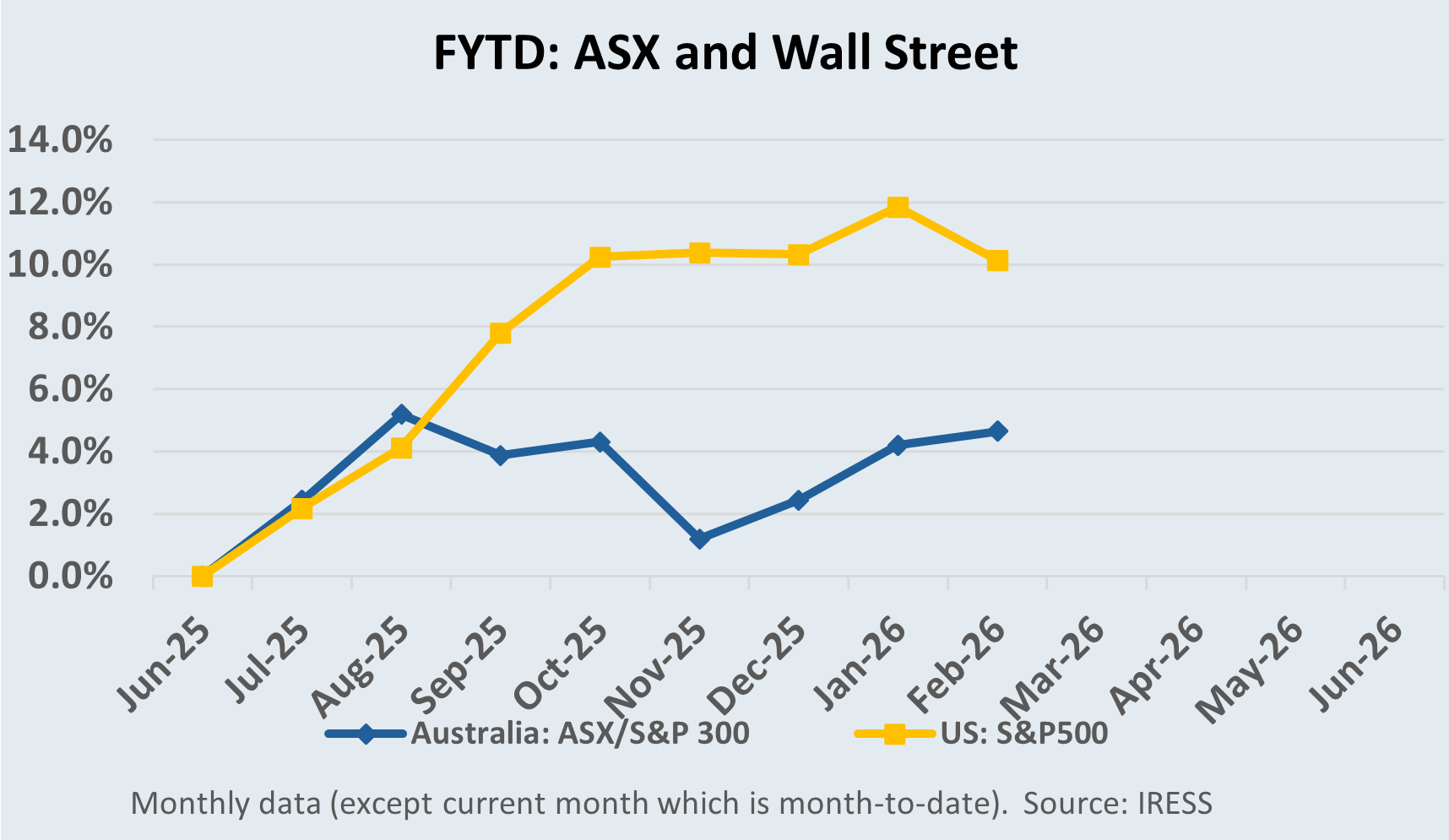

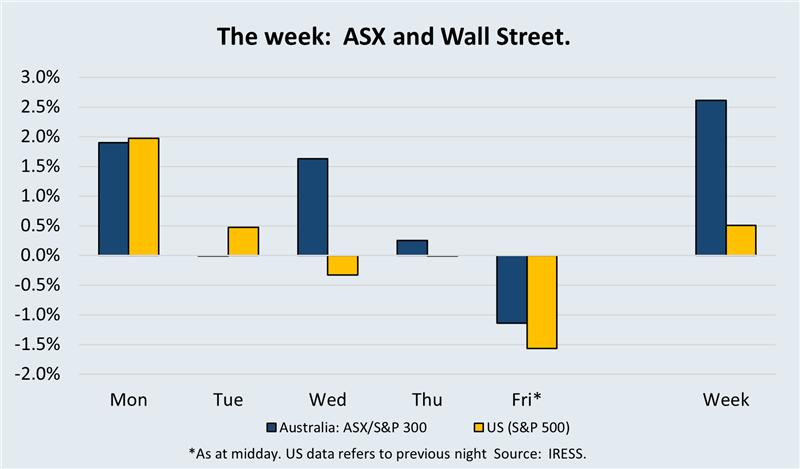

The Market

Company Profit Reporting season

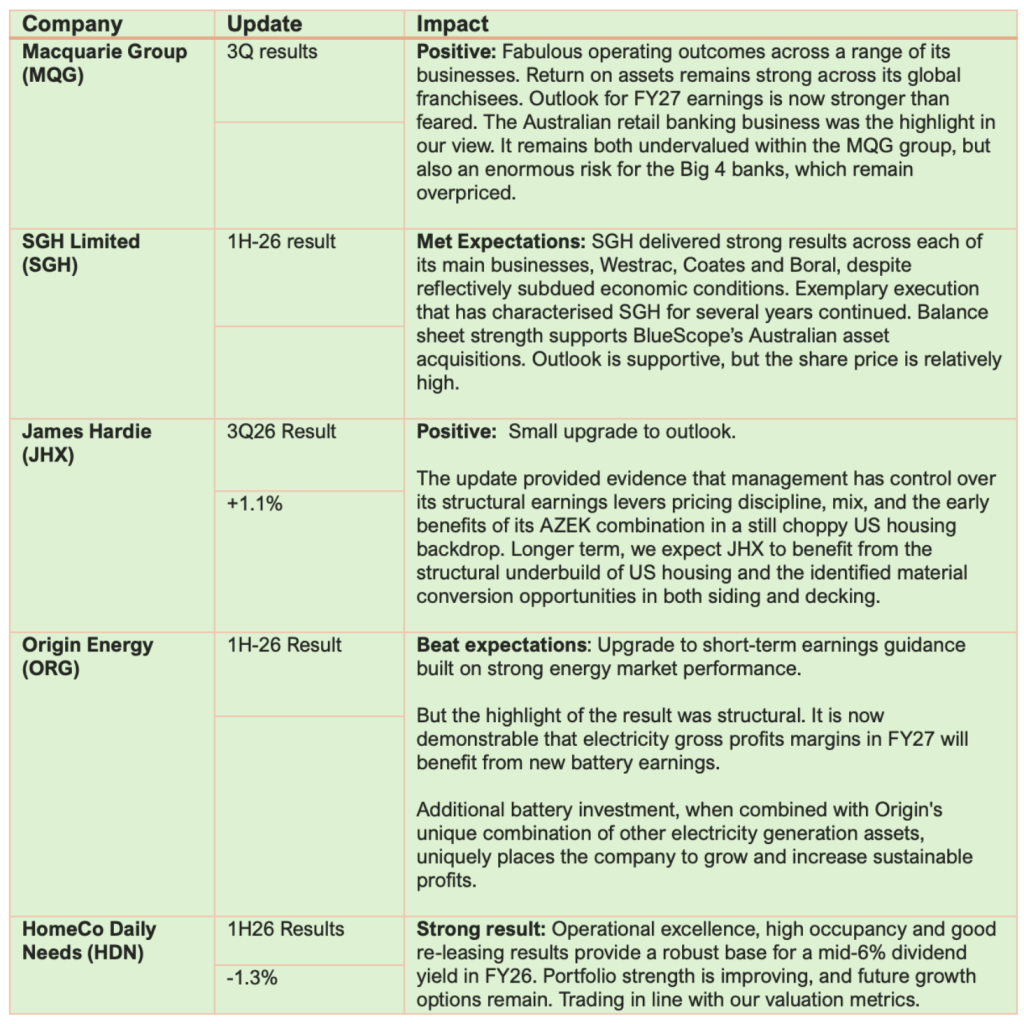

Over the remainder of February, most companies will report to the market. Investment Matters will present our weekly results snapshot in the following table format. What company reported, for what period the reporting reflected results, our view on the results, and the change in share price from the time of the result to the time of publishing.

In time, we will provide more detailed information, mainly regarding the ways in which the results changed, reinforced or destroyed our investment thesis. We will also include graphs and charts from the presentations that clearly capture the key trends that impact the long term.

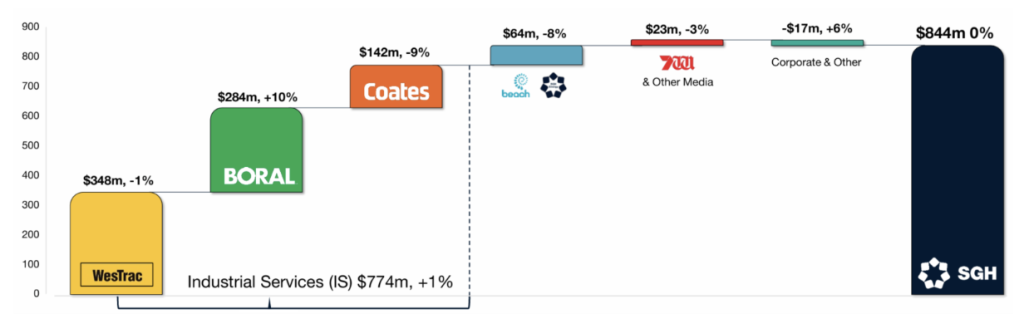

SGH Limited– H1 FY26 Result: Structural Quality Emerging

SGH’s first-half 2026 result was not spectacular in growth terms, but it was high quality. Revenue was broadly flat, and underlying profit growth was modest. What stood out instead was margin resilience, cash conversion and operational discipline across the portfolio. In our view, that matters more.

SGH remains a long-term position in clients’ Australian shares sub-portfolios, and despite the relatively high share price relative to our long-term valuation, the market continues to reward the company’s execution.

Its recent role in the potential takeover of BlueScope Steel, with assistance from US Steel Dynamics, further reinforces our view that the company has a unique lens on Australian Industrial businesses, highlighting industry structure, pricing power, capital discipline, and cash flow optimisation.

Led by CEO Ryan Stokes and a fantastic board, SGH continues to resemble a listed industrial private equity firm: disciplined capital allocation, improving asset quality, and growing recurring earnings streams. The headline growth may appear modest, but structurally the portfolio is stronger than it has been in many years.

Source: SGH 1HFY26 Result Presentation

At Boral, the margin story continues to impress. Pricing discipline, cost control and a simplified asset base are driving operating leverage even in mixed end-markets. Residential activity remains subdued, yet Boral expanded EBIT and lifted margins. This is structurally different to the pre-SGH Boral that your author has covered for more than 20 years. Boral is now less volume-dependent, more pricing-led, and focused on return on capital rather than tonnage. Infrastructure and energy transition work continue to underpin demand.

The business now looks more like a steady cyclical swing factor. We remain sceptical about Boral’s performance in genuinely weak market conditions but are impressed by the sustainability of earnings during periods of normal industry fluctuations.

Performance in periods of volatility is a key input in valuing businesses; the more stable the earnings, the higher the business’s value, as it carries a lower cost of capital.

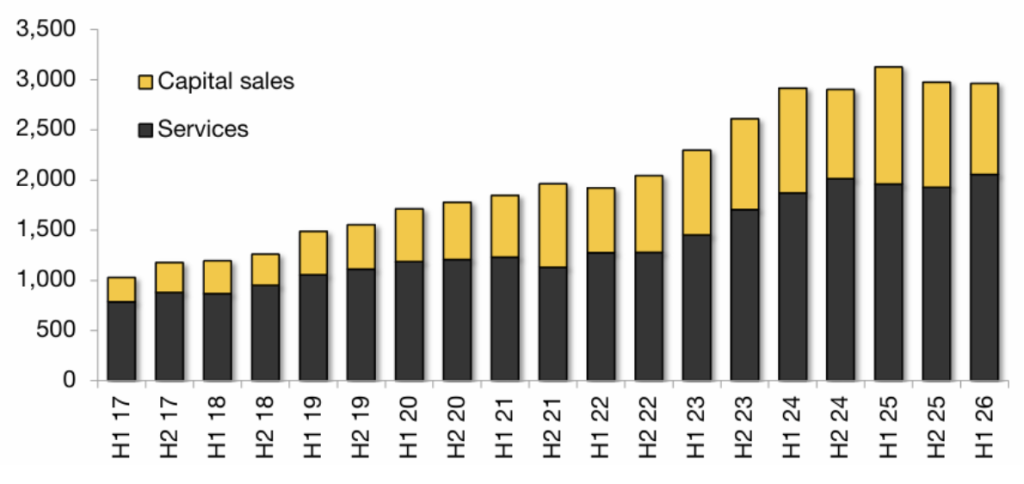

At WesTrac, the dealer of Caterpillar in WA/NSW, the structural strength of its maintenance services revenue continues to dominate earnings quality.

Equipment sales inevitably fluctuate, but the installed base continues to expand. Aftermarket support, maintenance contracts, and technology upgrades are higher-margin and recurring. Mining customers remain focused on productivity and emissions efficiency, sustaining demand for both new fleet and optimisation spend. The result reinforces our view that WesTrac’s earnings durability is underappreciated.

Figure #2: Westrac revenue split by type by half year

Source: SGH Limited 1HFY26 Result Presentation

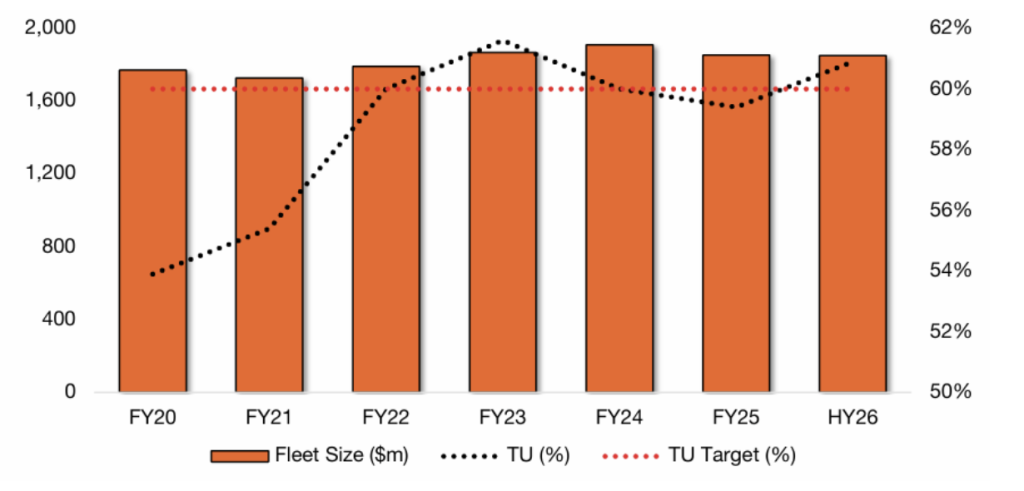

Meanwhile, Coates delivered what we would describe as an optimised outcome in weak conditions. Hire markets are softer, particularly in residential construction, yet margins were defended through utilisation management, cost discipline and fleet optimisation. That is a sign of a well-run business rather than a cyclical casualty.

The chart below shows Coates’s evolution into a company with a high and sustainable return on invested capital (ROCE) of 13.0%. On average, for the past four years, the company has achieved time utilisation rates above target (60%) without needing to increase the amount invested in the fleet ($m, LHS)

Figure #3: Time Utilisation (TU %, RHS) and Fleet Size ($m, LHS)

Source: SGH 1HFY26 Result Presentation

Result snapshot – Macquarie Bank 3Q meets CBA headlines

The biggest market impact this week was the stunning rebound in bank stocks. Despite their elevated price-to-earnings ratios and exceptionally high price-to-book ratios, the clean results delivered by ANZ and CBA highlighted their short-term appeal as haven stocks in an otherwise volatile market.

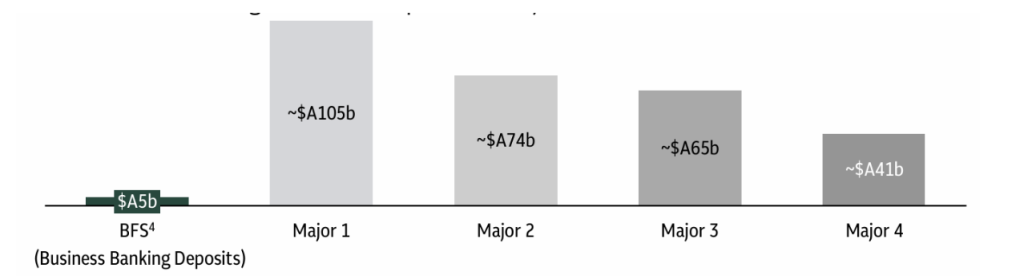

Both CBA and ANZ reported exceptionally low levels of bad debts, and relatively stable (falling slowly) interest rate margins. Interest rate margins remain supported by large customer deposits, which are not earning interest despite RBA rate increases.

Many of these accounts are held by the most vulnerable, poorest Australians, often funded by government payments. Equally problematic, other deposits are held in small-business accounts that could be earning interest to support employment. Instead, they are creating artificial earnings for equity holders

Figure #4: Non-interest-bearing deposits – Big 4 vs. Macquarie Bank

Source: MQG 3Q Operating Result Presentation

Particularly galling to those taking an interest this week was the endless spin from CBA, which espoused their mantra of “building a brighter future for all” ad-infinitum.

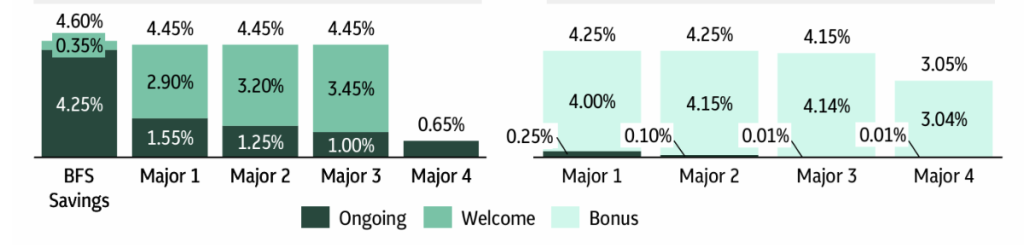

But not all banks were silent on this price-gouging practice in Australian banking; in fact, Macquarie Bank, in its excellent 3Q operating update, went to great lengths to highlight the sustainable domestic banking business it is building without the deposit gouge.

The following figure compares Macquarie Bank’s retail offering for standard savings accounts. The change at MQG isn’t solely driven by competitive forces, whereby Macquarie is looking to increase its domestic funding; the lead they are developing is fundamentally structural and technological.

Figure #5: Comparison of deposit interest rates between

Source: MQG 3Q Operating Result Presentation

With current technology, there is no reason app-enabled consumers shouldn’t be able to access competitive interest rates in their daily banking.

With this price and technological advantage, MQG grew deposits by an extraordinary 24% over the past 12 months.

The momentum for technological change is only increasing amid discussions of central bank digital currencies and stablecoins. Yet major Australian banks are priced as if not any of (a) competition for deposits from the likes of Judo Bank and Macquarie, (b) policy reform from the government, or (c) the evolution of product technology puts these excess profits at risk.

Noted analyst Matt Wilson (Jarden) put it well “we now find this a precarious economic model vulnerable to disruption in a time when IT advancement has removed any proprietary distribution advantage that historically justified vast below-market payment on deposits.”

But in the short term, CBA is benefiting from an extraordinary increase in the number of people simply leaving money in accounts that earn little to no interest. The Big 4 banks would say that consumers should choose term deposits (TDs) instead, but modern life, especially in times ofhigh inflation, suggests that higher balances in transactions are required, and TDs are too time-consuming and cumbersome.

Unless customers switch banks, they remain forced to play the big banks’ game. We suggest the cost of switching banks continues to fall, and the prize for doing so continues to rise.

Why are deposit margins and bad debt important for bank stock prices?

A bank’s profit level is fundamentally determined by the gap between the cost of its funding and the interest rate it can charge. The largest bank, CBA, has the highest level of incorrectly priced deposits, so, despite not having to lead on price to achieve a high market share, it simultaneously over-earns on these loans.

The second element of bank profitability is the number and size of bad debts it incurs. In any given year, the level of bad debt may be low, but we understand that through economic cycles, there will be periods in which bad debts reach high levels.

The lumpiness of these periods of bad debts necessitates that well-run banks “put-away” provisions for bad debts as part of their calculations of underlying profitability, but experience shows that these measures alone cannot smooth out bank earnings in practice.

A combination of low bad-debt provisions and higher unsustainable interest margins can drive up short-term earnings. But markets rarely overpay for such years when assessing the value of bank shares. Instead, investors either adjust earnings to a sustainable level or apply a lower multiple to current earnings, reflecting that such earnings will not be delivered every year.

Now, the Australian share market is not applying such a filter, presumably assuming it will be fast enough to sell when the deposit competition and bad-debt cycle turns.

With rising interest rates, emerging technology, and increased competition for deposits, we don’t choose to play such a game; we prefer to buy banks when they are cheap after accounting for these factors and sell when they are expensive.

What about the remainder of the Macquarie Group (MQG) update?

We thought the 3Q update was excellent. Note that Macquarie Group is a significant position in client portfolios, and along with Judo Bank, represents a significant divergence from the index in terms of the types of banking exposure we prefer. The MQG group’s diverse features were on display.

The market took from the update that, alongside “satisfactory” conditions today, there was clear evidence of improving near-term momentum in the market-facing businesses.

- Macquarie Asset Management (MAM) was the standout: net profit contribution substantially higher, largely reflecting the gain on sale from divesting the North American & European public investments business (and performance fees).

- Commodities & Global Markets (CGM) strengthened: Macquarie shifted its short-term markers to rising commodities income (a step up from earlier “flat” framing). This part of the business is inherently volatilie but current conditions appear supportive.

- Macquarie Capital: investment-related income expected higher, supported by asset realisations and private credit contribution.

- Balance sheet/capital: Macquarie reiterated a strong position, including a reported capital surplus (~$7.5bn).

Property sub-portfolio: HomeCo Daily Needs REIT (HDN)

Cashflow First, with Embedded Development Optionality

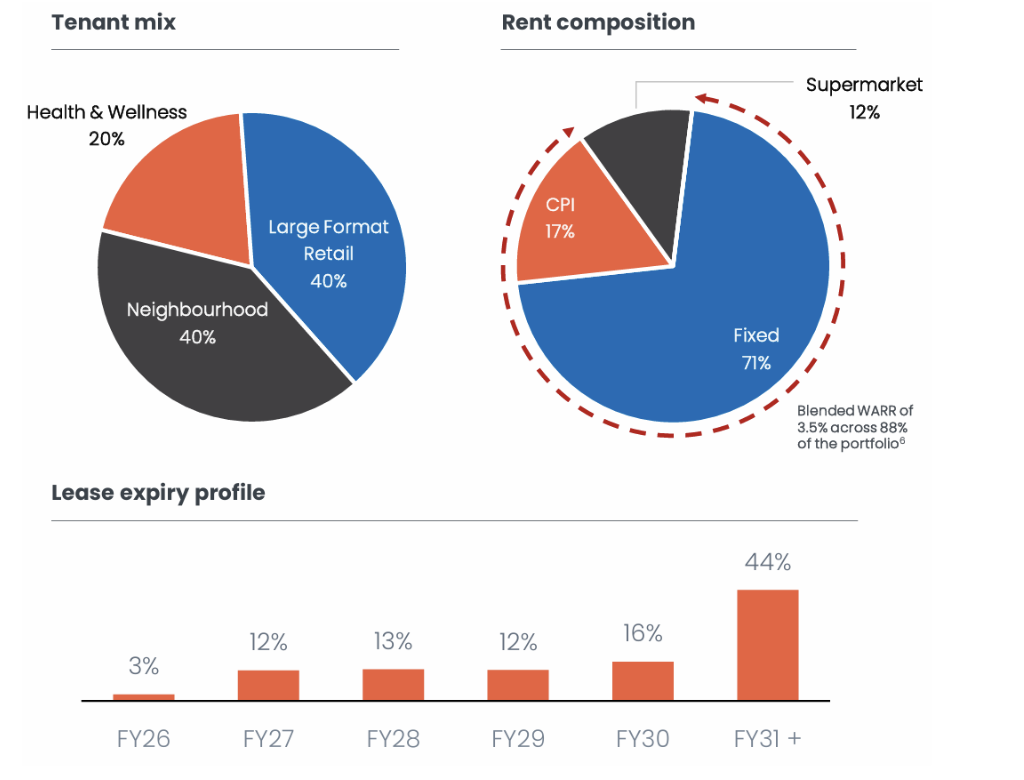

HomeCo Daily Needs REIT is an ASX-listed property trust focused on “daily needs” real estate, convenience-based assets across neighbourhood retail, large-format retail, and health & services. The appeal is simple: non-discretionary tenants, especially supermarkets, high occupancy, and a portfolio deliberately constructed to deliver resilient distributions through the cycle.

Built largely on the foundation of the failed Master’s home improvement portfolio, the portfolio today spans roughly $5.1bn in assets, 46 properties, ~99% occupancy, and a ~4.9-year WALE, supported by a deep tenant base. 83 per cent of tenants are national retail brands.

The figure below shows the tenant mix, which relies on large-format, neighbourhood, and health businesses. Future rent growth is largely fixed, and almost 50% of tenants are in place till post 2030.

Figure #6: HDN retain an impressive mix of long-term tenants

Source: 1H26 HDN results presentation

The 1H26 result was a strong example of that model working as intended. Funds From Operations per security (FFOps) of 4.4 cents was in line with expectations, and full-year guidance was reaffirmed at 9.0cps FFO and 8.6cps distributions. HDN continues to present as a relatively predictable cashflow vehicle.

Operationally, occupancy and cash collections remained above 99%, and the properties remain in high demand, with re-lettings spread very positively (+6.2%). People are paying more to stay.

From our perspective as investors focused on cash flows, this rent momentum through leasing and underlying trading conditions is genuinely value-creating.

Historically, REITs often highlight the non-cash earnings from property revaluations. But with rising interest rates, and heavy market discounts to NTA (net tangible asset value), we view the book value of property portfolios for these companies with a large grain of salt.

In theory, the NTA for HDN is $1.55 per share, and the company trades at $1.29. In our view, the size of the discount is largely due to the use of incorrect valuation, which in turn is based on incorrect interest rate, growth and investment assumptions. Having said that, with a forecast dividend of 8.6cps (yield of 6.7%) and future growth options, the company is attractively priced at these levels.

We also appreciated the value-creation mechanics on display: capital recycling and balance-sheet optimisation. During the half, HDN completed $87m of net disposals, reportedly at a premium to book value, recycling capital toward accretive opportunities. In a market where many REITs have been forced into defensive capital management, HDN’s ability to sell non-core assets and redeploy into higher-return pathways is a genuine advantage and one that tends to compound quietly over time.

On funding, the refinancing work was meaningful. HDN refinanced $810m of debt out to July 2028, with a margin improvement that helped offset rising interest rates.

Optionality is where HDN differentiates itself from more “plain vanilla” income REITs. The trust’s development pipeline is substantial (often referenced as $650m+) and, importantly, the portfolio’s relatively low site utilisation provides room to add value through intensification and staged projects rather than purely acquiring stabilised assets at tight yields.

FY26 development commencements are targeted at $100–120m, including Williams Landing, two Coles-anchored centres in the HUG Fund, and Warilla Grove.

Stepping back, this result reinforced what we find attractive about HDN: stable, visible cashflows today, with credible internal growth levers tomorrow and a demonstrated willingness to create value through recycling rather than simply “owning assets and hoping.” The near-term watchpoint is the development cadence, but the underlying operating performance remains strong.

Perth mining tour

Last week, your author travelled to Perth and regional WA for a series of company meetings across the lithium, uranium, gold and emerging material sectors. We were pleased with updates from portfolio positions in Minerals260 and IGO Group.

Ora Banda Mining – Site Visit

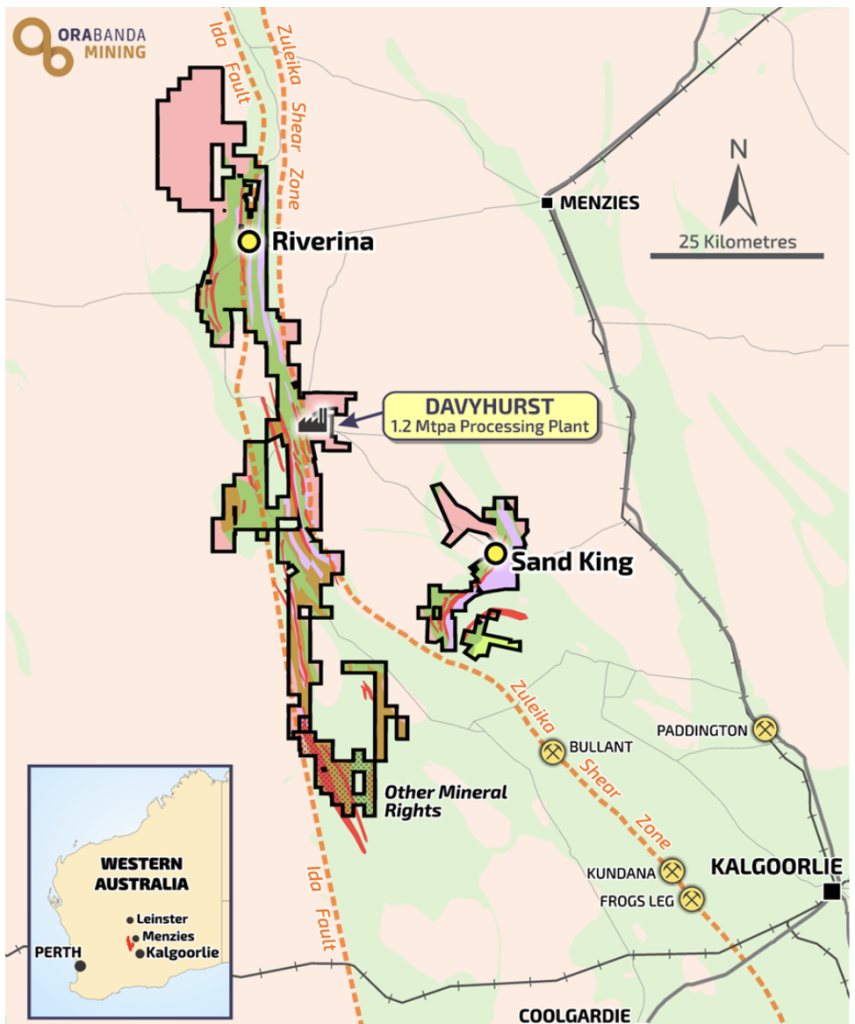

Flying into a red clay runway perched on a scrubby headland roughly 150 kilometres north-west of Kalgoorlie, the first impression is distance, and then scale. Davyhurst is best understood as a hub-and-spoke system: a central processing plant surrounded by operating open pits, underground mines, and a growing pipeline of satellite ore sources spread across Western Australia’s Eastern Goldfields. It is not a single deposit. It is a district. The physical footprint indicates that Ora Banda’s opportunity set is larger than the business currently reflects in its production numbers.

Ora Banda Mining’s gold processing plant site at Davyhurst, 120km north-west of Kalgoorlie.

Source: https://thewest.com.au , 2019

The tour was led by CEO Luke Creagh, whose operating background is central to our confidence in the story. Luke served as COO of Northern Star Resources and previously held senior roles at Barminco, experience that is reflected in a pragmatic focus on mine sequencing, fleet productivity, dilution control, and capital discipline. Since taking the top job in 2022, the priority has been straightforward: stabilise, simplify, then scale. Ultimately, credibility will be reinforced by decisions in 2026 on future processing plant capacity and the exploration choices made today.

Figure #7: Davyhurst Region: OBM tenements – note the vast distance North /South

Source: Company reports January 2026

Ora Banda’s central Davyhurst processing hub and surrounding satellite mines remain in a ramp-up phase, and management continues to report performance improvements across the operation. We saw evidence of a business working to increase consistency: incremental gains in throughput, stronger plant stability and improving alignment between mining fronts and mill feed.

OBM has been a small but successful holding within client portfolios as part of our gold basket. We built the position when the share price was in the low 70c range; despite recent weakness, the stock finished last week in the high $1.20s. Amongst our gold exposures, OBM has been particularly well placed to convert a rising gold price into value. Deposits and satellite sources that were sub-economic five years ago are now genuinely actionable — provided the mine plan is disciplined and execution remains strong.

The recent quarterly results, however, were a reminder that this remains an operating turnaround and growth story rather than a finished product. All-in sustaining costs (AISC) of A$3,505/oz were more than $500/oz above market expectations, driven primarily by a significant increase in tonnes processed via third-party milling during the transition. It is disappointing to incur higher costs precisely when the gold price is most supportive of cash flows.

Management framed this as a transitional feature rather than a structural problem, but the market will want to see cost control reassert itself as the ramp-up matures.

Multi-site exploration and enhancement

When we scan the broader gold universe, OBM appears optically expensive on current production. That, in our view, is not a red flag so much as a signal: the market is already looking through today’s output toward a larger business. It is effectively underwriting an expansion in plant capacity and an uplift in reserves. The key uncertainty and the principal source of upside is how much additional gold can be delineated and economically developed across the broader tenement package.

On that front, the opportunity set is tangible. Across the tenements, there are development and feed options at Riverina, Sand King and Little Gem, each capable of supporting mill utilisation and mine plan flexibility over time.

We visited the Sand King underground mine. The Sand King mine was OBM’s second development and is currently delivering steady production. We were impressed by the mine’s capacity to be expanded beyond current plans and by the likelihood of achieving its production cost targets.

More recently, Round Dam has emerged as another high-quality source of potential future ore. The current drilling program is nearing completion: OBM has drilled over 280 holes for ~53,000 metres as part of Phase 1, with ~62,000 metres planned. Importantly, drilling has confirmed multiple lodes up to six subparallel, continuous gold lodes and identified mineralisation in areas previously unrecognised from historical drilling. That matters because it expands not only resource potential but also scheduling, blending, and future mine design options.

Being on site chatting with geologists about continuity and formations, and with mining engineers about sequencing and plant constraints provides a more concrete picture of how the growth pathway could be achieved. There is ample gold in the ground. The investment question is how effectively OBM converts that endowment into profitable ounces through disciplined execution, particularly on costs, plant performance and the integration of new ore sources.

In short, OBM remains one of the more leveraged exposures to a strong gold price within our coverage universe. The market already prices in growth, which raises the bar for delivery. But the district-scale opportunity is real, the drilling is encouraging, and the operational focus under Luke Creagh is consistent with what we look for when optionality must be converted into earnings.

The information in this article is of a general nature and does not take into consideration your personal objectives, financial situation or needs. Before acting on any of this information, you should consider whether it is appropriate for your personal circumstances and seek personal financial advice.