Copyright 2025 First Samuel Limited

The Market

Market update

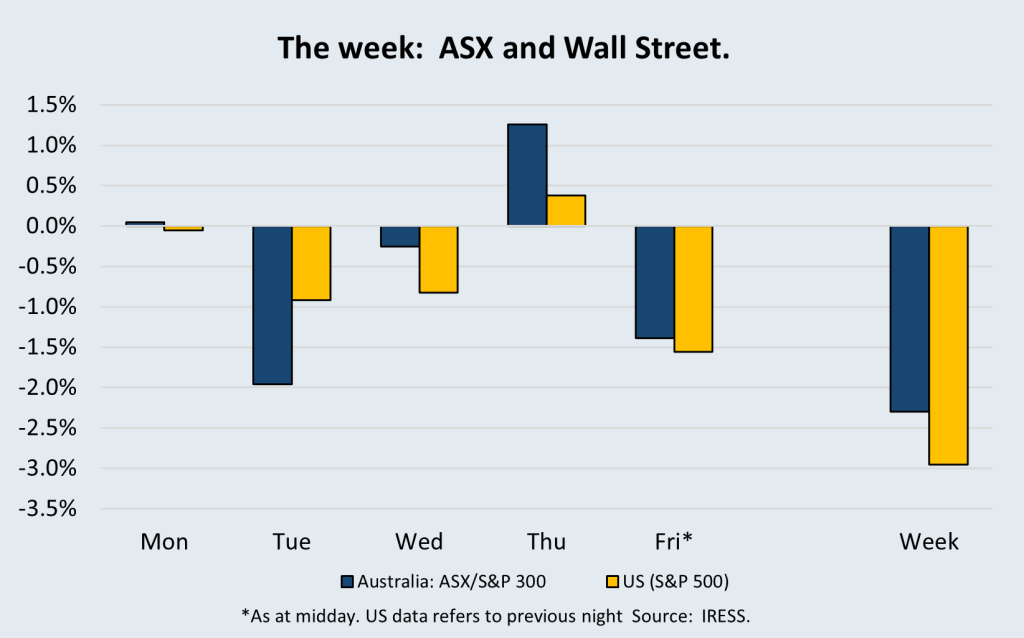

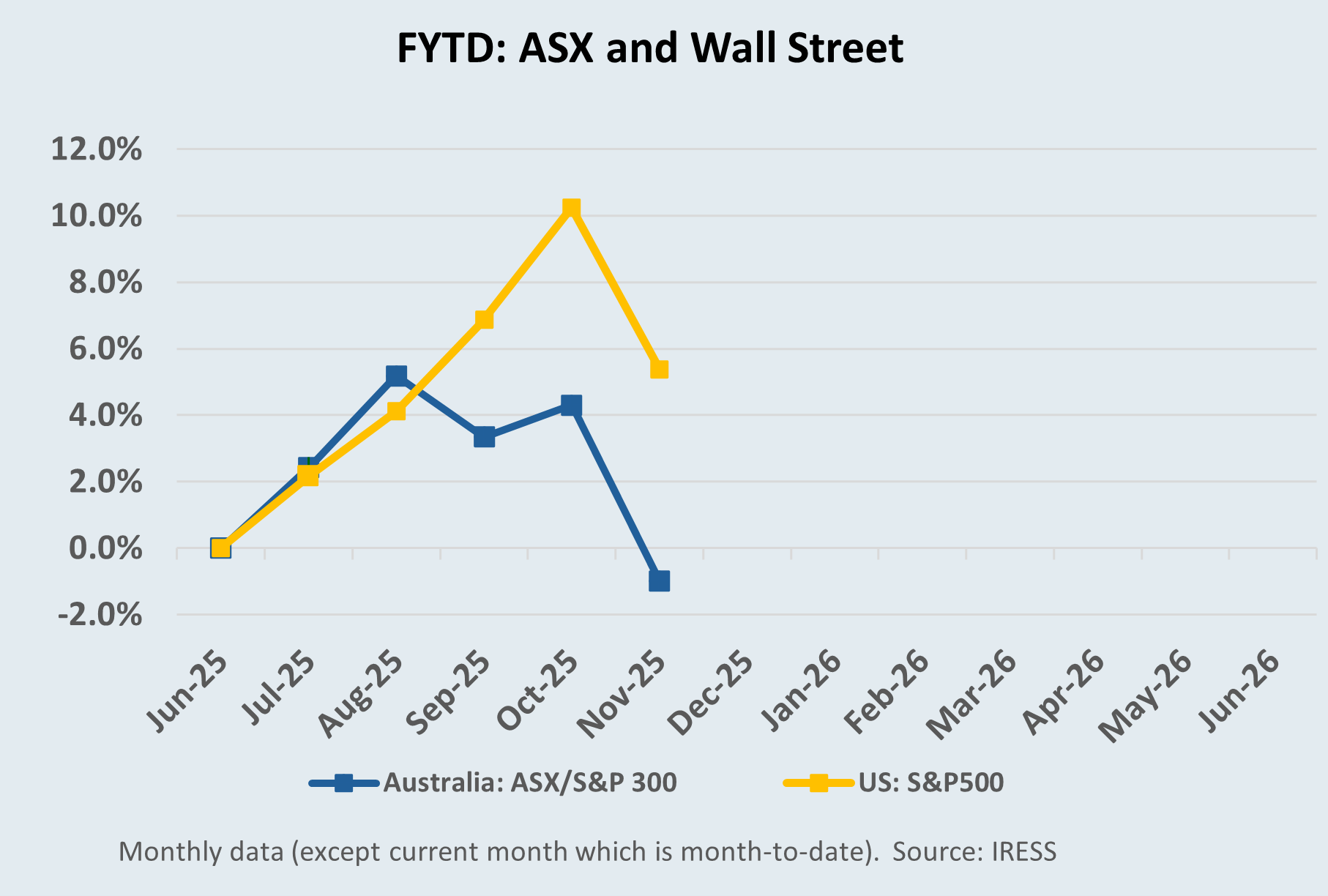

In recent weeks, the ASX has come under material pressure. The ASX 200 slipped to a five-month low and registered the worst daily session of the year (-1.94%) on 18 November. Over the past month, the index has fallen roughly 6.3% from its late-October peak.

Building cash

The market move is consistent with our expectations that the market was overpriced. The sectors that have seen the most significant drawdowns tend to include the most overpriced large capitalisation companies. We have been building cash levels in clients’ Australian shares sub-portfolios over the past couple of months in anticipation of a correction.

- Our bottom-up analysis showed a large number of companies were overpriced based on current and future earnings.

- Our response to recent highs has been to continue to increase cash levels and trim our exposure to the two sectors of the market which have been exceptionally strong – Gold and Technology.

- We have sold down more than half of our exposure to Life360 and a third of our position in Block,

- Our total exposure to Gold has also more than halved since Gold reached its record levels.

The market’s move is also consistent with three emerging issues that our clients are positioned for:

1. Global tech & momentum stocks unwind…

… as the market understands more clearly the long-run implications of investment in the AI sector. We have refused to participate in the current round of AI hype. The concerns we raised in recent Investment Matters articles include circular financing and overinvestment.

The critical issue is that the investment is likely to generate substantial technological progress for society as a whole and help manoeuvre developed market economies towards improved productivity outcomes. But that doesn’t mean the companies themselves will generate strong returns.

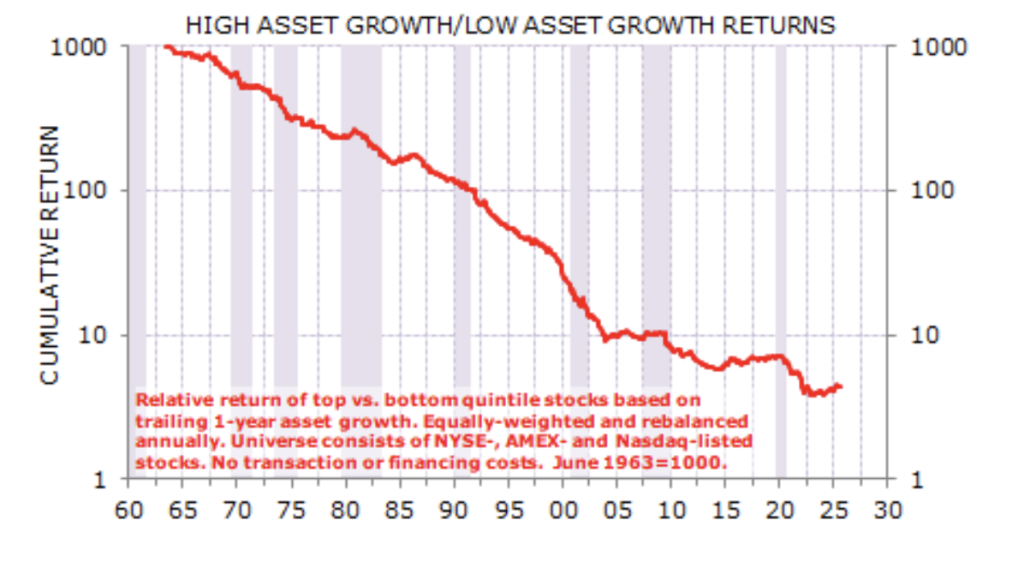

Growing assets quickly is typically a way to ensure return underperformance. Figure #1 shows the relative returns of the companies ranked in the top 20% of asset growth compared with those ranked in the bottom 20% of asset growth, with the baskets rebalanced annually. Companies that grow assets quickly have been underperformers for almost 60 years, with the past two years being an exception.

Figure #1: Cumulative returns for overinvesting companies

Source: Minack Advisors

2. Changes in market interest-rate expectations

Commentary from the Reserve Bank of Australia suggests that rate cuts may not be imminent, reducing the scope for valuations of rate-sensitive sectors. Regular readers will note that we continue to see entrenched domestic inflation as the barrier to significant rate cuts. As such, we have limited exposure to both the domestic banking sector and discretionary retail stocks.

3. Pressure on sectoral rotation trends

Often, the Australian market moves between periods of banks’ outperformance and miners’ outperformance. In recent weeks, concerns about the Chinese economy, especially medium-term expectations for the iron ore price, have coincided with the outlook for rate cuts, crimping any upside in the Big Four banks.

What to do?

We suspect that it is too early to wade into the market to deploy a significant level of cash, however, we are noting opportunities in a range of oversold and cheaper stocks emerging.

With pressure on mining in general, there have been pockets of outperformance in specific mining sectors such as Lithium, Rare Earths and Copper.

A huge rebound in global lithium prices has occurred in recent weeks, with prices rising by 23% since October, although they remain a fraction of those achieved in 2023. Client will recall that we have remained patient with our investment in IGO Limited. After being a strong contributor to performance in FY-23, the company has delivered among the weakest returns in recent years.

IGO’s lithium interests include a stake in the world-class Greenbushes Lithium Operation and an interest through a JV in the Kwinana Lithium Hydroxide Refinery, both located in Western Australia.

We believe that the quality of lithium assets held by IGO provided the most optionality and risk-adjusted future value.

Copper Market Outlook and Portfolio Positioning

The long-run fundamentals of the copper market continue to strengthen, driven by the interplay of structurally declining ore grades, rising extraction costs and persistent under-investment in new supply. For several years, our central thesis has been that copper prices must move higher over the medium term to incentivise the next generation of projects. That structural view now looks even more robust, with the industry experiencing an unusual cluster of significant mine disruptions across some of the world’s largest producers. These disruptions are occurring at the same time as global demand remains resilient, supported by electrification, grid investment and early signs of recovery in traditional construction and manufacturing sectors.

Structural tightness: declining grades and constrained mine supply

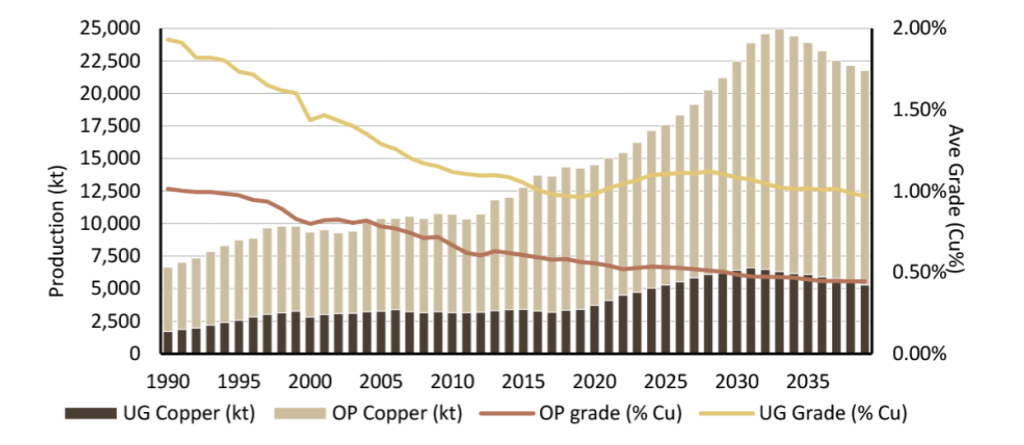

Global copper grades have been falling for decades, a trend clearly illustrated in industry data (see Figure #2). Lower grades mean more material must be moved and processed to produce each tonne of copper, raising energy intensity, cost structures and environmental footprints. At the same time, the global project pipeline remains shallow. Few large-scale greenfield developments are advancing, and most existing mines face capital-intensive expansions just to sustain output.

Figure #2: Declining average mined grades

Source: Woodmac, UBS

Recent supply disruptions have now amplified these long-run constraints. The Grasberg mud-rush incident, output issues at Kamoa-Kakula, prolonged shutdowns at Cobre Panamá, community disruptions at Las Bambas and safety-related slowdowns at Codelco have together removed hundreds of thousands of tonnes of expected supply from the 2025–27 period.

This is not a concentration of risk in marginal assets; these events involve some of the core pillars of global production. The implication is clear: even a well-signalled, cyclical soft patch in demand cannot fully offset the tightening effect of these cumulative disruptions.

Scrap supply helps—but cannot compensate for mine shortfalls.

Scrap copper availability has grown steadily, both as a smelter feedstock and through direct copper-metal reuse. This is a valuable pressure-release valve in tight markets, and scrap recycling will play a larger role over time as circularity improves. However, scrap growth is inherently constrained: it rises with historical consumption patterns and cannot accelerate quickly enough to bridge the widening gap between demand and mined supply.

Over the next 3–4 years we expect mined supply to grow below 1% p.a., while scrap may add another 2–3%—still well short of expected demand growth.

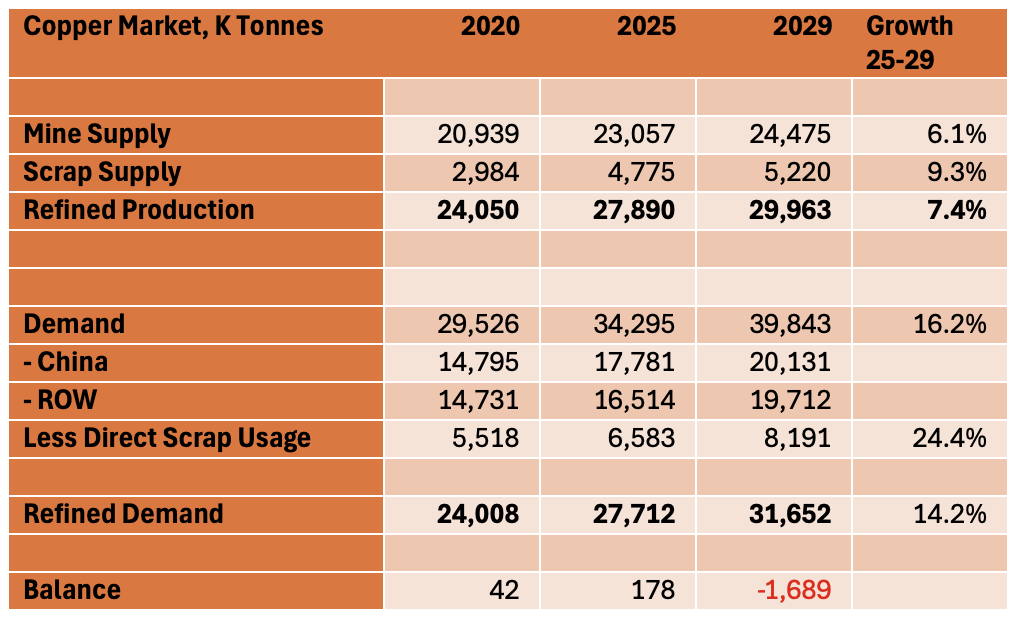

The table below provides an example of current forecasts (based on UBS current model) that we agree with. Note that despite strong growth in scrap use, the limited mining growth between 2025 and 2029 results in a significant shortfall in supply in 2029.

Source: Woodmac, UBS, First Samuel

Demand: resilience beneath the noise

Near-term demand indicators have been mixed. China has shown softness in some property-linked end-markets, and appliance demand cooled after a strong first half. But the underlying structural drivers remain intact. Global grid investment is running at multi-decade highs. Renewables installations remain robust in Europe and North America. China’s slowdown in renewables after grid-tariff changes was less severe than feared, and traditional industrial sectors in the West appear close to trough levels. We forecast global refined copper demand growth of roughly 3–3.5% in 2026–27, with upside risk if developed-market construction and autos normalise.

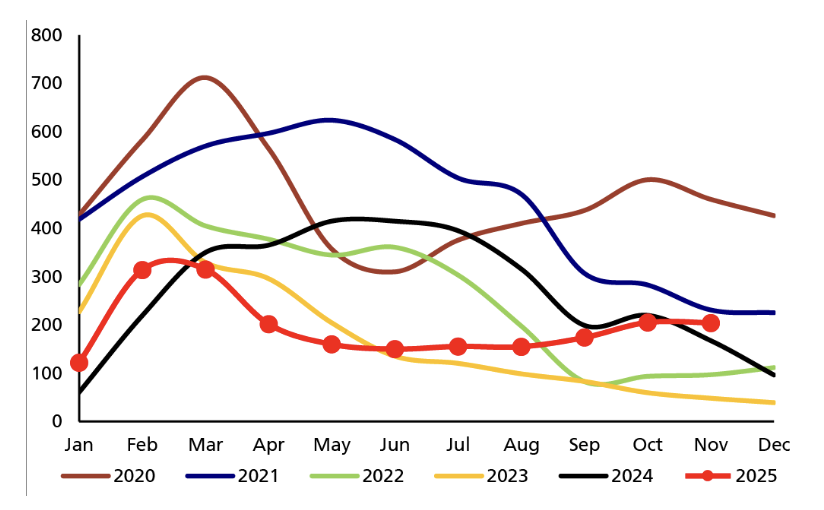

The consistency of demand is evident in inventory behaviour: despite the recent rise in visible Chinese inventories (see Figure #3), global stocks remain low by historical standards. The recent build looks more like strategic restocking—traders and consumers insulating themselves against future supply shocks—than a collapse in underlying usage.

Figure #3: China copper inventories – kt

Source: Barrenjoey Research

Short-run softness is likely temporary

Short-term price action may remain volatile. Elevated LME net-long positioning, resilient near-term refined output and the overhang of Chinese macro concerns have contributed to copper stalling below US$11,000/t. Rising inventories have also emboldened bears in recent weeks. But these dynamics look cyclical rather than structural.

Once positioning normalises and clarity emerges around the Chinese policy path, the underlying deficit trajectory is likely to reassert itself. We retain a constructive view into 2026, consistent with our belief that sustained deficits will draw inventories materially lower and support higher long-run copper prices.

Portfolio : Sandfire, Rio Tinto and Aurelia Metals

Sandfire Resources (SFR)

Sandfire remains a key copper-leveraged name in our portfolio, well-positioned through both operational delivery and emerging growth opportunities. Recent quarterly results were a modest improvement on guidance: Motheo delivered robust C1 costs (US$1.47/lb), offsetting cost pressures at MATSA (US$1.73/lb). Group revenue of US$328m and underlying EBITDA of US$157m highlight the company’s ability to generate strong free cash flow even in a mid-cycle price environment. Net debt has fallen to just US$62m, and we expect Sandfire to be in a net-cash position by year-end, paving the way for capital-management optionality.

Strategically, the most important recent development is Sandfire’s entry into a term sheet to earn up to 80% of the Kalkaroo copper-gold project in South Australia. Kalkaroo has been examined previously by OZ Minerals and BHP, with BHP’s 2023 study concluding there were no fatal flaws and confirming the deposit’s technical viability. Sandfire’s staged A$210m earn-in commits the company to a new PFS, extensive drilling and regional exploration, effectively securing a long-dated growth option in a Tier-1 jurisdiction. This complements the upcoming Black Butte PFS update, another catalyst that may reshape medium-term production visibility.

While valuation remains full, SFR continues to trade with a “scarcity premium” as the ASX’s primary copper pure-play—the combination of operational delivery, de-gearing and project optionality leaves the company well-positioned in a tightening copper market.

Rio Tinto (RIO)

Rio remains one of the world’s most important diversified copper producers, with exposure across the full project pipeline—from legacy operations like Kennecott and Escondida (JV) through to future-facing developments at Oyu Tolgoi. The scale and diversification of Rio’s copper portfolio provide both stability and embedded growth, positioning the company to benefit materially from rising long-term copper prices.

While copper is not yet the dominant earnings driver, Rio’s strategy explicitly recognises the metal as a key pillar of its future value. For investors seeking high-quality copper exposure without single-asset risk, Rio offers a balanced and lower-volatility pathway into a tightening market.

Figure #3: RIO – substantial value in Copper – NPV by division (Macquarie)

Source: RIO, Macquarie Research

Figure #5: RIO – Copper Share is a high share of EBITDA (Macquarie)

Source: RIO, Macquarie Research

Aurelia Metals (AMI)

Aurelia provides a smaller-cap, leveraged exposure to copper with meaningful optionality. While historically seen as a precious-metals-tilted business, Aurelia’s asset base includes valuable copper credits, and ongoing mine-life extensions and development opportunities provide a pathway for the company to increase copper’s contribution to the revenue mix. In a rising copper-price environment, these leverage characteristics enhance AMI’s appeal within a diversified portfolio.

Aurelia Metals’ primary copper asset is the Great Cobar Project, which is a high-grade copper development that leverages infrastructure at its operating Peak Mine. The company also produces copper as a polymetallic by-product from its other operations.

The Great Cobar Project is Aurelia’s key growth project for high-grade copper production operations officially commenced on July 1, 2025. Over an initial eight-year mine life, with first ore projected for FY28 the company’s goal is to reach 40kt copper equivalent production across all its operations by FY28.

Aurelia also has a significant exploration landholding in the Nymagee district and has reported high-grade copper intersections from recent exploration drilling, indicating future potential for resource growth.

Conclusion

Copper’s long-run fundamentals are strengthening as declining grades, rising costs and persistent mine disruptions collide with resilient global demand. Scrap supply growth helps, but cannot close the gap. Near-term price softness is possible given positioning and China noise, but the underlying deficit trajectory remains intact. Our copper exposures—anchored by Sandfire’s operational delivery and project pipeline, supplemented by Rio’s scale and Aurelia’s leverage—are well aligned with what we see as a multi-year opportunity in the copper market.

The information in this article is of a general nature and does not take into consideration your personal objectives, financial situation or needs. Before acting on any of this information, you should consider whether it is appropriate for your personal circumstances and seek personal financial advice.