Copyright 2025 First Samuel Limited

Read the previous edition of Investment Matters.

The Market

The year has begun with a strong signal to the ASX with two significant M&A developments announced to the market.

The standout was the proposed takeover of BlueScope Steel, alongside reports of renewed merger discussions between Glencore and Rio Tinto. While very different in structure and certainty, both point to a re-emergence of strategic thinking after several years dominated by balance-sheet repair and capital discipline.

What we particularly appreciate about these potential transactions is their clear focus on the value of hard, strategic assets rather than short-term financial optimisation. These early-year developments reinforce a broader theme we are seeing globally: acquirers are prepared to act where asset quality is unquestionable and long-term strategic value is clear, even if headline market conditions remain uncertain.

In BlueScope’s case, attention has centred on the North Star mill in the United States — a high-quality, low-cost steel asset that has become increasingly valuable amid reshoring, supply-chain security and differentiated regional pricing. The joint bidders, SGH Ltd (formerly Seven Group Holdings), a holding in most clients’ Australian equities sub-portfolios, and Steel Dynamics, have management teams revered for their strategic thinking and capital allocation.

For Glencore and Rio Tinto, the strategic logic rests heavily on the quality, scale, and growth outlook of their copper portfolios, assets that are both scarce and increasingly critical to global electrification and decarbonisation. Global miners haven’t historically made great capital-allocation decisions; the commodity cycle tends to obscure underlying value in both periods of excess optimism and pessimism. Today, both parties see the strategic value of copper assets.

M&A activity entering 2026 remains well below the exuberant levels of 2021, with transactions driven by strategic fit, balance-sheet strength and clear operational synergies rather than financial engineering and cheap debt funding. This reflects a world of higher real interest rates, more demanding equity markets and boards that are far less tolerant of execution risk.

Valuation discipline is the defining feature of the current cycle. While listed market multiples remain elevated in parts of the market, private transaction multiples have adjusted downward more materially. This gap is encouraging opportunistic bids, particularly where share prices have lagged intrinsic value or where complexity has obscured underlying cash flows.

Our cash flow and valuation-based approach has been rewarded in a market where many active managers have suffered reversals in momentum and reduced appetite for pure growth stocks. A large share of client sub-portfolios continued to be invested in assets that are attractive to similar deals.

BlueScope Steel: Great assets, fabulous M&A execution

In early January 2026, BlueScope Steel confirmed it had received an unsolicited takeover proposal valued at approximately A$13.15bn (around US$8.8bn) from a consortium headed by SGH Limited, led by Ryan Stokes, in partnership with U.S. steelmaker Steel Dynamics.

The offer contemplated a scheme of arrangement at A$30.00 per share in cash, subject to extensive due diligence, regulatory approvals and other conditions, with SGH proposing to take control of BlueScope’s shares and then on-sell certain North American assets to Steel Dynamics. SGH would on-sell BSL’s North American operations, including the US North Star Flat Rolled Steel Mill and Building and Coated Products North America business.

Seven Group Holdings would retain the remaining “Australia & Rest of World” operations, including Australian Steel Products, Asia Coated Products and New Zealand & Pacific Islands business.

At the time of the bid, BlueScope was the largest position in clients’ Australian equities sub- portfolios.

BlueScope’s board unanimously rejected the proposal, stating it “significantly undervalued” the company’s global asset base, ongoing growth initiatives, and long-term prospects, noting that the bid’s value could be undercooked once future dividends and changing conditions are factored in. Sure enough, BlueScope’s board subsequently announced a $438m special dividend, and we expect further actions from BlueScope to defend against the merger.

With a 29% increase in the share price in January, and when combined with the stock now trading above the $30 bid price, we have reduced the size of our position in BlueScope- we have taken some profits – consistent with our portfolio management approach.

Background

To better understand the proposed deal, the prospects of a higher bid, our logic in building the BlueScope position and any broader implications, some background is required.

Australians tend to view BlueScope Steel through the lens of the original BHP Steel business, spun out of BHP in the early 2000s. The BHP spin-off pursued a specialised strategy to focus on high-value flat and coated steel products, including the ubiquitous Colourbond products.

But one asset emerged as the key asset from within the original business, the North Star steel mill, which started life as a 50-50 joint venture with Cargill and began operating in 1997. Major expansions and the buyout of the Cargill stake over the past 25+ years have increased the plant’s value to BlueScope.

Figure #1: One of the best global steel assets: BlueScope’s North Star Mill in Ohio

Source: macrotrends.net

As the US deindustrialised and the Electric Arc Furnace (EAF) technology replaced traditional mills, the US steel industry became more sustainable but remained sensitive to steel price volatility and potential “dumping” from Asian markets if trade protections weakened. Despite the North Star milled location and customer base, its value fluctuated.

However, the emergence of tariffs and Trump’s political stance from 2016 onwards in protecting the US steel industry has become very important to assets such as North Star. The political support extended throughout the Biden era, with “national security and unfair competition cited as reasons for moving away from traditional economic views on tariff protection.

In 2025, the mill’s future value was clear but remained out of focus for the Australian market.

In addition to the North Star mill, we valued the US Building and Coated Products business highly. Readers may recall our disappointment in the write-down of this business in August 2025. Together, we valued these businesses at more than the prevailing share in 2024.

Three previous bids

As part of the information release from the parties associated with the bid, the market learnt that indeed there was sustained interest in the BlueScope assets. This was the fourth such approach from Steel Dynamics (SDI) in about two years, with the previous three undisclosed to the market. Previous bids ranging from A$27.50 to A$33.00 per share were also dismissed by the board.

Steel Dynamics is a premier North American steel producer and metals recycler. Headquartered in Indiana, the company utilises Electric Arc Furnace (EAF) technology to manufacture high-quality steel from recycled scrap, maintaining a circular, lower-carbon manufacturing model. Beyond steel, the company is diversifying into aluminium production, with new flat-rolled aluminium products launched since 2025. Backed by strong financial health and consistent dividends, SDI remains a leader in sustainable, value-added industrial manufacturing

We rate Steel Dynamics as one of the best businesses in the world, and they will generate enormous synergies from one of the best industrial assets in the US

What sets this deal proposal apart from previous ones is its engagement with SGH, another position in clients’ sub-portfolios. Combining Steel Dynamics with the local SGH team not only strengthens the deal financially but it also creates a clear solution for Australian shareholders and governments alike.

At the same time, the political circumstances facing the US steel industry have been improving; similar developments are unfolding in Australia. Politicians and policymakers alike are increasingly recognising the need for some steel production capacity. When combined with industry changes, the positive outlook for Colourbond, and opportunities to develop excess land holdings, the value in the residual non-US holdings has been increasing.

To maximise the value of Australian assets, there is an urgent need for strong execution capacity, investment-grade cash flow, extensive political connections, and diligent management. This is where SGH has both a demonstrable record, a great management team and a strong balance sheet. We agree with SGH’s statement regarding the bid

SGH and SDI believe that BSL’s independent enterprises in Australia + Rest of the World, and North America are not strategically compatible and would benefit as stand-alone businesses under new ownership.”

“.. we have a proven track record of driving performance improvement in domestic industrial businesses. We intend to leverage our disciplined operating model and capital allocation approach to deliver better outcomes for stakeholders”

What bid gets the deal across the line?

Institutional investors, including major shareholders, have publicly backed the board’s valuation stance, leaving the deal’s progression uncertain absent a materially higher offer.

As noted, BlueScope announced a special dividend and is committed to defending the company against being purchased for less than its long-term value. However, in our view, a bid above $33 per share (including dividends) would represent adequate value for Australian shareholders, especially as an SGH shareholder in our case.

Mega-mergers are back: RIO and Glencore

Early this month, Rio Tinto and Glencore confirmed they had entered preliminary discussions regarding a potential $300 billion mega-merger. The deal, which was outed by the Financial Times and subsequently confirmed by both companies on January 9, 2026, would create the world’s largest mining company by market value, surpassing BHP.

Details of the deal structure are thin on the ground due to the strange rules governing takeovers on the London Stock Exchange. Rio has until February 5 to put a real proposal on the table. And Rio may not be the only player looking to acquire the Glencore assets.

Glencore is a major producer and marketer of more than 60 commodities, founded in the 1970s as a trading company, now employs more than 150,000 employees and contractors, and has a strong footprint in over 30 countries across both established and emerging natural resources regions.

We suspect that the final structure of the deal will involve trading a range of assets among several companies (including BHP) and the new RIO may ultimately include spin-off assets, including coal. It is even possible that the Australian iron ore asset could be listed separately.

Does a deal make sense? Unequivocally yes in principle, but the details, the implied prices paid and the final structure of the deal will define how much value is created or destroyed.

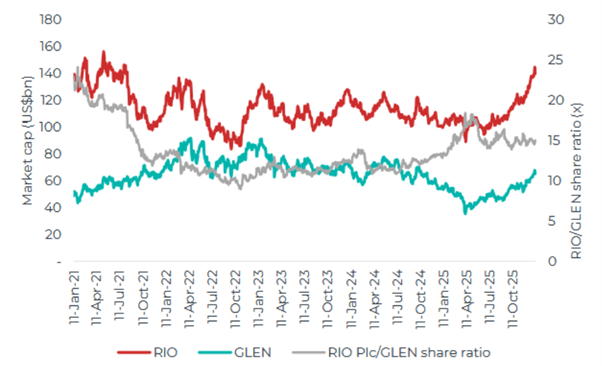

The chart below shows the share prices for both companies since 2021, along with the ratio of the two prices. The ratio has been relatively stable.

Figure #2: #1: RIO, GLEN market cap (US$bn, LHS) and share price ratio (x, RHS)

Source: Bloomberg, Barrenjoey Research

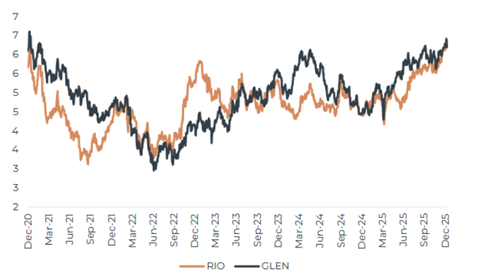

In addition, when we look at prices over the same period based on the price-to-future-earnings ratio (EV/EBITDA), the close relationship between how both companies trade is even clearer. Apart from a small periods, the factors that drive prices in global commodities are the dominant drivers of market value.

Figure #3: RIO and Glencore tend to trade on similar 12-mth forward EV/EBITDA

Source: Bloomberg, Barrenjoey Research

When both companies trade at similar relative values and move in step with similar drivers, a merger is more likely to create value. Should the deal complete without significant premiums being paid to either party, the value of synergies (estimated at more than $8bn) could be shared by both parties.

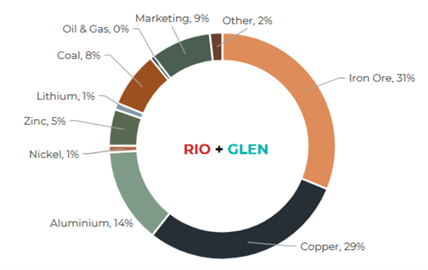

The significant benefit we see from the merged entity is the diversification of value across commodities. From the perspective of current RIO shareholders, the mix of value-add (below) is now less skewed toward iron ore, the future growth in copper assets is broader, and RIO benefits from Glencore’s significant marketing resources.

The split of commodity value is shown in the chart below.

Figure #4: RIO plus Glencore breakdown by value-added, consensus (2026)

Source: Visible Alpha, Barrenjoey Research

Our view

The market reaction to the deal has been relatively straightforward. Glencore’s share price in London has risen 15 per cent, suggesting the market anticipates that RIO will need to pay a premium to secure the Glencore assets.

In Australia RIO has traded down 2-4 per cent for similar reasons. We expect that RIO would trade higher if the merger proceeds in a format that balances price expectation and includes rationalisation of assets, especially coal.

We have recently been trimming our position in RIO due to the strong run-up in the share price prior to the announcement. Current price levels of around $150 per share imply long-run commodity prices: US$80/t Iron ore, US$5.00/lb Copper, and US$1.25/lb Aluminium. These prices are 10-15 per cent higher than our assumptions.

The RIO-Glencore merger is likely a drawn out story that extends through 2026.

The information in this article is of a general nature and does not take into consideration your personal objectives, financial situation or needs. Before acting on any of this information, you should consider whether it is appropriate for your personal circumstances and seek personal financial advice.