Read the previous week’s Investment matters.

Photo © alexlmx from Via Canva.com

Copyright 2025 First Samuel Limited

The Market

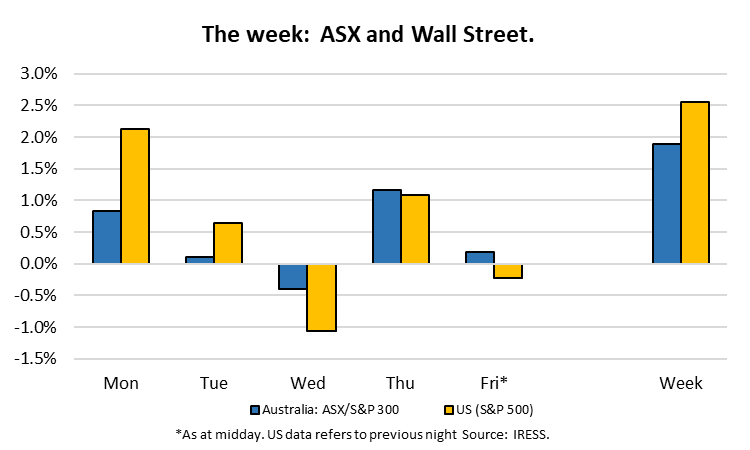

Some stability returns to the markets

The highlight of the week was the return of stability in equity markets. The US market was up 2.6% since the previous Thursday. In Australia, we saw a 1.9% move over the same period.

We spoke last week of the importance of the relative changes within the declining market. And continue to observe them:

- Globally: unwinding of momentum in large-cap companies;

- In Australia: a relative switch away from the expensive Big 4 banks and other financials and towards mining companies; and

- Increased appreciation of ‘value’ companies with favourable cash flow yield and asset backing characteristics.

We also noted that any reduction in uncertainty would lead to market improvements, regardless of the underlying economic conditions and company performance. We still expect this to be the case. In addition, our view is that the market is beginning to accept the premise that inflation will remain slightly higher and that long-term interest rates will remain near current levels.

Reporting season catch-up and company news

Investment Matters will continue to concentrate on reporting on sub-portfolio companies that were not covered in detail in previous weeks. This week, we detail the results for Woolworths and Nanosonics.

We also provide some background on an exciting transaction in a long-held position in TZ Limited. Following almost 12 months of discussions, the company has successfully navigated a transformational merger. The implications for the company and clients are later provided.

Woolworths

Woolworths reported its 1H25 results on 25 February. On the eve of publication, the ACCC’s final report on supermarkets was released. The 441-page report devoted a significant amount of time to discussing margins, with limited new information.

The media suggested that the retailers got off lightly, and the 5 percent increase in Woolworth’s share price indicates that the market agrees. Some recommendations could limit the pace of store openings for Coles and Woolworths, while also providing farmers and fresh suppliers with better information. We see limited risk to margins beyond the issues discussed in the remainder of this update.

Woolworths remains a core position in clients’ Australian equities sub-portfolios for three key reasons:

- Its duopoly position with structurally high operating margins;

- Its capacity to navigate the switch between in-store and a variety of online and alternative delivery models;

- The Australian economy is principally driven by population growth, nominal income support from the government and general support for consumption from monetary policy. This is the perfect backdrop for consumer staples companies.

The combination supports Woolworths stock’s role as a long-term hold in client sub-portfolios, generating compounding returns in a tax-efficient manner. In the short term, the size of the position in portfolios remains driven by operating conditions and the share price.

February’s result demonstrated an incongruous mix of structural strength but weak operational performance. After covering Woolworths for more than 20 years as an analyst, I note that ebbs and flows in operational success are a constant. While Australia-wide system sales growth has always remained substantial, variations in growth have tended to move with:

- the hit-or-miss nature of marketing programs

- the cadence of new product development

- the rate of store refreshes

- changes in customer behaviour

- pricing architecture success, including specials and promotions

Management teams with deep supermarket experience tend to be able to respond to changes within 12-18 months, thereby limiting the costs of short-term operational shortcomings. We share that markets are concerned that Woolworth’s responsiveness over the next 12 months could be limited by:

- a new management team’s limited experience

- declining inflation

- increasing online competition

- change in shopping behaviours

- political interference, especially arising from the ACCC investigation

- the task of managing the migration of sales to online and alternative delivery options

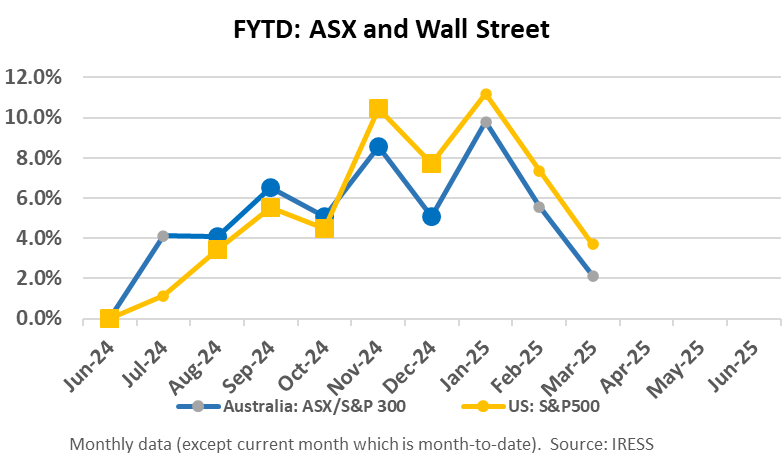

In FY25, Woolworths has been a weak performer, falling by more than 11% (including dividends) compared to market growth [is that share market or retail market?] of 4%. We reduced our position by more than 50% in 2024, at price levels more than 15% higher than today.

The result

The 1H result was affected by the supply disruptions we saw in Victoria arising from a 17-day industrial dispute in early December 2024. The total cost of the dispute was $95 million at the EBIT (Earnings Before Interest and Tax), representing a 2-3% impact on FY25 total profit.

Operational weaknesses and limited cost control magnified the overall affect. Profits in Australian Food fell 5% in 1HFY25, excluding the affect of the dispute and incremental supply chain costs. We remain concerned that Woolworths is not achieving the level of cost control that we would expect in current conditions.

In response, the new management team announced set of cost-saving measures. We are concerned managing unfavourable operating challenges and at the same time as experiencing cost inflation may require more significant attention than has been currently proposed. Whether the team is culturally and politically capable of more substantial changes remains unclear.

Investment implications

With Woolworth’s share price now at levels that provide moderate upside based on long-run valuation, we would look to add to client portfolios over the next six months. To have confidence in such a move, we will need to see more evidence from the Woolworths management team and the broader supermarket supply chain that it can adapt to the challenges of cost growth and customer behaviour.

We currently see no evidence in store that Woolworths has appropriately adapted its pricing architecture. The combination of scattered promotions, the complicated nature of Everyday Rewards, and an inconsistent overall value proposition remain visible in a range of locations and formats.

Woolworths’ results’ presentation slide deck highlighted that current consumer behaviour provides a terrible backdrop upon which to exhibit operational inconsistency. The figure below highlights that customers are much more focused on “Lower prices” than they were in 2021.

When price becomes more important, customers naturally increase the amount of time and effort they are willing to commit to searching for better prices. This results in an increase in the percentage of customers who are willing to shop at multiple supermarkets, referred to as “cross-shopping” in industry parlance.

Families, despite obvious time constraints, are cross-shopping at a rate seven percentage points higher than they were only two years ago. Despite smaller increases, even older couples are increasing cross-shopping despite being the recipients of most of the real income growth in the economy over the period.

Customer behaviour change – more price sensitivity and increases in cross-shopping

Source: Company reports

Structural strength

Despite the concerns above expressed, the ongoing structural strengths in the Woolworths business remain clear. These strengths include:

- ongoing successful investment in the supply chain

- significant leverage in generating revenue from advertising and data-rich customer information

- migration to online solutions remains exceptionally rapid:

- Everyday Rewards membership has surpassed 10 million customers and has grown by 8% in the past twelve months

- There are more than 30m visits per week to the Woolworths Group’s digital assets, up 12.8% in 2025

- Customer adoption of Direct-to-Boot is superb. Sales are up more than 20% year on year, and customers are exploiting the ability to utilise this service on a same-day basis (88% of orders), increasing the stickiness of customers to the local store network. Local stores are Woolworths’ great strategic asset, with 83% of the Australian population within a 10-minute drive time to a Woolworths store).

Each of the structural strengths points to assets that are well-positioned to deliver future performance, but the assets themselves do not guarantee that they are well-managed.

The core message of this note is that great assets still require exceptional execution, especially in terms of price and value proposition. The importance of this value proposition was highlighted in recent weeks by the release of Calendar 2024 data regarding Amazon sales. Readers who are Amazon Prime members and customers would attest to the value proposition and convenience of the free, often same-day delivery proposition.

The data suggest that Amazon is proving to be exceptionally successful in Australia, and it is our perception that Australians, in general, are still learning to utilise the best features of this business model. Amazon’s financial results indicated its gross transaction value (number of sales on the platform) rose by 33%, or $1.7 billion, in the 2024 calendar year. According to MST Marquee, “as a share of all non-food retail, including bricks & mortar, Amazon captured one-third of the growth in the market last year”.

Australian online sales growth – Calendar 2024

Source: MST Marquee

When one company, Amazon captures one-third of all system growth, it has a significant effect on market structure. As we have anticipated in Investment Matters over the past five years, the effect is to consolidate activity in a small number of players and accentuate the value of existing duopoly structures. This enables Woolworths (including Big W), Wesfarmers (Bunnings and Officeworks), and Coles to capture the remaining share. Amazon’s growth is more so at the expense of other pure-play retailers, including eBay. Eventually, it will impact majors, including ASX-listed companies that aren’t well-prepared.

Conclusions

We retain a cautiously optimistic “watching brief” on Woolworths. We love great assets and good prices.

Nanosonics (NAN) – Great results and better announcement

Nanosonics reported its 1H25 results on 25 February. For those unfamiliar, Nanosonics is an Australian medical device manufacturer, predominantly making endoscope probe cleaning machines.

The stock price reaction was exceptionally positive with a +23% move on the result day and an overall reaction of positive 26% since the result, despite the falls in the overall market.

In additional news this week, the company received the critical US FDA (Federal Drug Administration) clearance for CORIS, its new product. Investors have been waiting for this new product for many years. CORIS is a device for the automated cleaning of flexible endoscopes. This will now allow the much-anticipated controlled launch activities that are planned for 1Q26, encompassing US, EU, UK and Australia, to proceed. The positive stock reaction of 10% is a testament to the degree to which the market has been waiting for such an announcement. and medium-sized businesses across Australia.

1H25 Results

The result demonstrated a rebound in growth that had been questioned over the previous 12 months. The first half revenue result of $93.6 million represented a strong start to the year – up 18% compared to previous corresponding period. The stronger first half allowed the company to upgrade its full year forecast of sales growth. Nanosonics noted “a solid foundation to build on for the remainder of the financial year. Consequently, the range for revenue outlook for the full year has been increased from 8%-12% to 11%-14%.”

The market loves a result which placates concerns and upgrades revenue forecasts.

In terms of long-term value, we were impressed by the global installed base of Trophon units reaching 35,480, up 7% on the previous year. The growth generated a high level of new capital sales income. But the real value in the business, as regular readers would recall, is the consumables and service revenue that is generated from the installed base.

Nanosonics reported consumables and service revenue generated from this installed base grew by a fabulous 20%. Consumables and services revenue have extremely high margins and now represented more than 70 per cent of all revenue. Margins in this area had weakened in the 2H24 period and was anticipated to rebound. The figure below shows the rebound in margins at this result.

Nanosonics Consumables margins – rebound in 1H25

Source: 1H25 Company reports

Higher sales and an increasing mix of consumables revenue drove an across-the-board improvement in financial metrics. The graph included below from the company result shows the positive performance extended from sales all the way through to dramatically increased overall profit.

1H25 Result: Improvements across all financial performance metrics

The cost of investment

Regular readers of Investment Matters will note that we often bemoan the level of investment in the Australian economy. This directly leads to weak wages growth and lower productivity. Listed companies are particularly poor at sustaining high levels of growth and productivity-enhancing capital expenditure, instead preferring to distribute franked dividends.

This will ultimately reduce national wealth and have adverse outcomes for future generations.

Therefore, when a company we own is engaged in high levels of investment, including prospective projects, we are aware that we need to consider the returns to the existing core business separately from the returns achieved on new R&D.

Nanosonics has assisted the market with this task in recent years by publishing the profitability of its core business, distinct from that of the entire industry.

In 1H25, the core business generated a profit before tax of approximately $25.6 million, representing a 41% increase compared to the previous period. Other financial metrics were just as impressive.

Based on these financial deliverables, we suspect that the market was assuming almost no additional value creation in the business when the share price was trading in the mid-$3 range. There was no value attributable to the new CORIS business.

At today’s share price in the mid $4 level, Nanosonics needs to deliver strong growth in its core and moderate outcomes in CORIS.

Expenses

One of our concerns in previous periods has been the rate of growth in operating expenses. Part of the expense’s growth relates to new CORIS product development, and part relates to expansion into new markets, including Japan. Those expenses make sense, but we have been concerned that the general level of costs outside of these areas is too high, especially when compared to other businesses with similar margins and customer profiles.

This was the principal theme we explored with the long-time CEO Michael Kavanagh after the 1H25 result. We were pleased with this discussion in which Michael highlights that the road map for margin expansion that we first discussed more than a decade ago remains in place. Based on the success the business has had in achieving its plans to date, it was reassuring that the aims for operating margins remain as high as we expected.

Investment implications

The recent rise in the share price has seen us mildly reduce the size of our position in Nanosonics.

We view the investment as a small standalone opportunity in the high-growth global healthcare sector. We would look to add should the stock disappoint over the coming 12 months, but equally appreciate the upside is not limitless and the stock is already priced for a considerable level of future growth.

TZ Limited (TZL)

The long-held position in TZ Limited has reached a positive inflection point, marked by a series of announcements this week. Those announcements followed a previous market announcement in November 2024 regarding the potential purchase or merger of TZ Limited with a previously privately held business called KeyVision.

As a reminder, TZ Limited is a global provider of smart locking, access control, and “smart locker solutions”. Its customers are a mix of blue-chip clients (Microsoft, adidas, Samsung, etc) engaged across a variety of industries. It is fair to say, however, that despite this client list, the profitability and growth profile of the existing TZ business has been problematic for many years.

Improvements in its operating systems, the migration to cloud solutions, and its recent return to profitability have all been improvements witnessed the past 3 years. Until this week’s transaction was secured, First Samuel owned more than 20% of the outstanding TZ Limited shares.

What’s changed?

TZ Limited has entered into a binding agreement to acquire KeyVision Holdings Pty Ltd, a leading provider of tenant engagement platforms. The completion of the acquisition will be subject to approval by the shareholders.

Negotiated over the previous 12 months, the transformation will leverage the best assets and sales capabilities of the existing TZ Limited business, combining them with a highly relevant application-based business that exploits one of TZ’s key long-term residential market density developments.

KeyVision’s core product is a software program designed for residential building management that is generating strong recurring revenue.

KeyVisions core product: What is a Tenant app?

The deal between TZ Limited and KeyVision sees TZ Limited acquiring the KeyVision assets using a mixture of upfront payments and ongoing success-based milestone payments. Ultimately the success of the business in its new form will depend on the ongoing rapid growth of the KeyVision offer and the ability of TZ Limited to exploit the synergies available.

To fund the upfront costs of the new business acquisition, TZ Limited needed to reorganise its debt position. The initial announcement of the KeyVision deal in October 2024 was contingent upon such a reorganisation. The proposed transaction received some support in the share price, albeit at small traded volumes. The TZL stock price had been languishing at historically low levels at the end of FY24.

Support from existing shareholders and the higher share price ultimately enabled TZ Limited to secure new debt funding. Critically for First Samuel clients, we secured the repayment of 50% of our outstanding debt and increased the interest rate payable on the remainder.

With the change in direction of the company, and especially to achieve closer alignment between KeyVision principals and the existing shareholder base, First Samuel facilitated the sale of part of its existing shareholding in TZ Limited to KeyVision associates.

The transaction proceeded this week and was announced to the market on Monday. Clients will have seen reductions in their TZL positions commensurate with tax benefits received from the sale and risk-based position sizing.

The new, significantly smaller position (less than 1% of equity portfolios), reduced debt exposure, tax benefits, and repositioning of the TZ Limited offer represent significant progress for the overall portfolio, particularly in terms of risk assessment.

The total returns generated from the TZ Limited position in FY25 has been +125% (before any tax benefits), a great result in a year in which the ASX is up less than 5%. Additionally, we appreciate the release of capital created by the part sale at a time when the recent ASX sell-off is providing many new investment opportunities.

The TZ Limited ASX announcement included the following quote which we include for completeness.

“Recognising the strong synergies of the acquisition and the strategic value it brings, we were encouraged by the commitment of the KeyVision team to invest in TZ Limited. Facilitating the sale of 9.5% of TZ Limited to KeyVision’s leadership was in the best interest of the company and its shareholders, ensuring alignment and a shared vision for growth. First Samuel remains a significant shareholder with over 13% and is fully supportive of TZ’s expansion and integration of KeyVision. We look forward to continuing our support through various means as the company executes its global rollout strategy.” (Craig Shepherd, Chief Investment Officer of First Samuel)

The information in this article is of a general nature and does not take into consideration your personal objectives, financial situation or needs. Before acting on any of this information, you should consider whether it is appropriate for your personal circumstances and seek personal financial advice.