Copyright 2026 First Samuel Limited

Read the previous Investment Matters here:

In this week’s Investment Matters, we focus on:

- How a plan for peace has driven a rebound in markets.

- Around the grounds – catch up on company news

The Market

A plan for a plan is sometimes enough for markets

In the most recent Investment Matters in mid-March, we noted that even amid a war-driven sell-off, there were still paths to resolution. In market terms, that was sufficient to qualify as encouragement. We took the opportunity to deploy additional funds. Not because the outlook had become perfectly clear, but because several of the companies we already owned had been sold down rather more aggressively than the market. Stock prices were assuming permanent impacts when a temporary disruption was more likely.

By mid-April markets are assuming that sanity prevails. This is not the same conclusion as assuming the Iran War has no permanent cost, or that all players are sane.

The following figure shows the evolution of market sentiment through daily moves since the 28th of February.

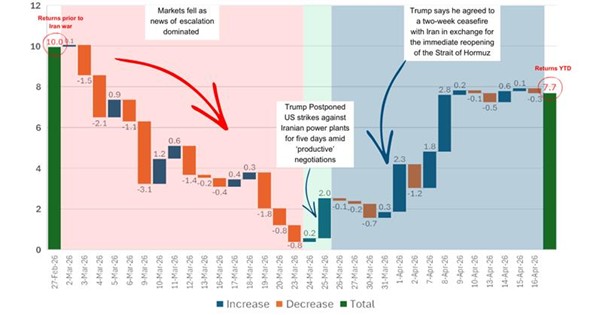

Figure #1: Movements in the ASX300 – from beginning of Iran War

Source: IRESS, First Samuel

The first three weeks of the war were essentially an exercise in moving up the escalation curve, and the market behaved accordingly. Each fresh step higher in the conflict was met with another leg down in risk appetite. At the lows in March, nearly all the returns in the market for the financial year were erased.

The rebound, by contrast, was not driven by any sudden outbreak of peace and goodwill. It was associated with something much more modest: the possibility of de-escalation through ceasefire, talks and the avoidance of further bombing. Markets, after all, do not require harmony. They merely require a chance that things may become less bad at a slower rate. A chart showing the market stepping lower with each escalation, then rebounding as the news flow shifted toward a ceasefire and negotiations, would make that progression visually obvious. The war began on February 28; by April 15, the S&P 500 had recovered to record highs as investors responded to signs of possible de-escalation, even though the conflict itself remained unresolved.

That is usually how these episodes unfold. Investors begin by selling what looks dangerous, continue by selling what looks exposed, and finish by selling almost anything that requires thought. Our relatively high cash holdings had provided a useful buffer through that process. More importantly, they gave us the flexibility to respond when prices in parts of the portfolio began to diverge from business reality.

Portfolio diversification provided some oil exposures, including Santos, which has risen 13 per cent since the beginning of the war. However, we don’t have a portfolio that is disconnected to the real world. We have meaningful exposure to smaller companies, to asset-heavy businesses, and to companies operating through energy-dense supply chains or with cost bases vulnerable to higher input prices.

The figure below shows six companies that have sold off sharply. Six companies, one awkward thing in common: a sensitivity to diesel prices, which the market had wasted no time in noticing. Markets are highly efficient at finding anything that burns diesel and marking it down accordingly.

Figure #2: Movements in the ASX300 – from beginning of Iran War

Cleanaway faces rising costs of rubbish collection, and Paragon Care faces higher prices for distributing health care products, operating at razor-thin margins. Metcash faces the same squeeze in delivering food to the nation’s IGA, liquor stores and Mitre10 networks. For industrial companies such as Orara and Amcor, there is not only a high cost of doing business, but they faced rising input costs of resin.

Plastics are deeply embedded across industries, from packaging and construction to auto manufacturing and healthcare. Switching to alternatives made from paper or glass is often expensive and time-consuming, requiring changes across entire manufacturing processes.

Additional downside leverage was visible in parts of the US housing and construction markets. Holdings such as James Hardie and Reliance Worldwide were dealing with the unhappy combination of global growth anxiety, higher interest rates and weakening industry sentiment. Markets can be severe, facing such combinations; sell first and leave the finer distinctions, such as valuation metrics and long-term value creation potential, to come later.

By mid-March, we thought that in several cases, fear was dominating and short-term impacts were being priced as long-term value destruction. But more likely, Cleanaway raise prices to collect rubbish, supermarkets and chemists raise prices to cover the cost of deliveries, and paper packing prices rise to cover the cost of inputs.

On these occasions, cash in the portfolio moves from defence to capacity for new investment.

Around the grounds – Company Updates

In this week’s Around the Ground, we note some developments in a range of companies held in client portfolios.

In some cases, such as Aquirian Limited (AQN), the position may only be held in portfolios with a higher concentration of smaller companies or a higher risk appetite. We tend to invest in these companies based on a long-run view of structural tailwinds, acquisition opportunities, or unique options that the market doesn’t appear to value correctly. This group of stocks has performed well this financial year.

CWY — Cleanaway Waste Management | 14 April 2026

Cleanaway issued a price-sensitive trading update, revising its FY26 EBIT guidance downward by approximately $20 million, citing the financial and operational impact of the ongoing Middle East conflict.

While downgrades related to the Middle East conflict are becoming daily events, this was the first significant holding in First Samuel portfolios to be downgraded. Interestingly, and somewhat surprisingly, the market took a mature approach to this announcement and barely moved the stock price. Cleanaway marginally underperformed in March, in line with expectations of a fuel cost impact, so the reality came as no real surprise. Cleanaway has been in a frustrating position recently, but the strategic value of its asset base may be beginning to be recognised.

Source: Cleanaway website

The company now expects full-year EBIT of between $460 million and $480 million, down from the previously guided range of $480 million to $500 million. The primary drivers are higher fuel and diesel costs.

Cleanaway operates a large vehicle fleet with significant fuel exposure, elevated third-party logistics and supplier costs, and reduced activity within its Contract Resources business in the affected region. The company noted its contractual cost pass-through mechanisms are recovering a substantial portion of the higher fuel costs, and that most contracts reprice on 1 July 2026, which should provide meaningful earnings relief in the second half. No fuel supply disruption has been reported. Despite the downgrade, Cleanaway’s underlying performance remains solid, with first-half FY26 revenue and EBIT growing 13% and approximately 17% respectively.

NUF – Nufarm Limited Trading Update | 15th April

Our position in Nufarm (NUF) has been amongst the worst performing over the past couple of years. Our average entry price was circa $4.75, and we lightened our position in the lower $3.00 range. Depending on portfolio risk and tax preferences, many clients will no longer own a position in the company.

A combination of poor execution, global pricing pressure, and a range of corporate decisions we view as questionable has weighed on the stock. The Iran War and its impact on global chemicals and agricultural demand further depressed the price towards $1.80 per share at the market lows on March 23rd.

It is fair to say that despite a reasonable financial update in February, the trading update on 15th April was the first good news in the stock for a number of years. Why?

Nufarm’s latest trading update points to the early stages of an earnings recovery, with first-half FY26 EBITDA guided to A$239–244 million, broadly in line with consensus but still representing roughly 17% growth on the prior corresponding period. More importantly, the update suggests that operating momentum is improving even as balance sheet pressure begins to ease.

The NUF stock price finished the week around $2.40 per share.

Net debt was reported at A$1.23 billion, down A$130 million on the prior year, with last-twelve-month leverage at 3.6x. UBS argues this is not yet comfortable, but it does support the view that de-gearing is underway. For the full year, EBITDA is forecast at A$381 million, up 26% on FY25, with leverage expected to fall to about 2.1x by year-end. The drivers of the recovery appear to be fairly practical rather than heroic: cost-out benefits, particularly in Europe, and some improvement in gross profit per tonne as agricultural chemical pricing stabilises.

The more interesting part of the note is the discussion around chemical pricing.

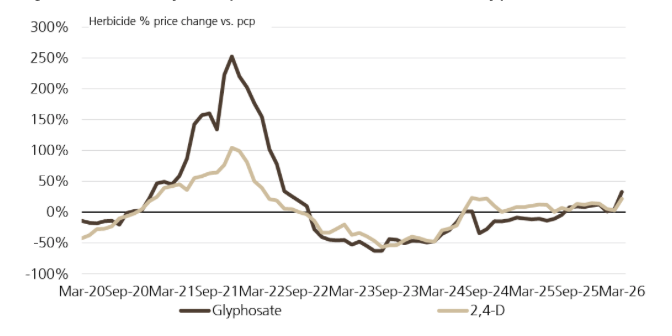

Figure #3: Price recovery in core products: Herbicide and Pesticide monthly prices

Source: UBS Research

After two to three years of decline, UBS’s China price tracking showed a sharp move higher in March. Glyphosate rose 26%, 2,4-D rose 15%, insecticides increased 31%, and fungicides were up 20% relative to pre-disruption January levels. UBS links this move to higher oil and petrochemical derivative costs, as well as tighter raw material availability associated with the current Middle East conflict. The key point is not that one month does not make a cycle, but that this is the first genuine sign of positive price inflection after a long period of pressure. That matters for Nufarm because it has historically benefited when chemical prices rise, although farmers’ profitability remains a constraint on how much of that increase can ultimately be realised.

AIH — Advanced Innergy Holdings | 30 March 2026

Advanced Innergy is a global leader in the engineering, manufacture and application of insulation and passive fire protection systems, as well as buoyancy and other marine products, notably sub-sea in the energy industry. It is relatively new to First Samuel portfolios, having listed late in 2025. We are attracted to the company’s leading market position, the strong revenue growth it generates, and the opportunities to grow through acquisition.

Figure #4: AIH marine product examples: Hose flotation system and Sub Sea Buoyancy

Source: Advanced Innergy

Significant news this month was the company’s submission of a non-binding indicative proposal to acquire all shares in Matrix Composites & Engineering (MCE) at AUD$0.40 per share via a scheme of arrangement. The offer represents a 66.7% premium to MCE’s last closing price. AIH has also secured call option deeds over 19.9% of MCE’s issued shares, providing meaningful deal protection against a competing proposal. FIRB approval has been applied for.

Strategically, the acquisition is central to AIH’s ambition to build a leading platform for technical buoyancy and subsea ancillaries in the Asia-Pacific region, with MCE’s Henderson facility offering an immediately deployable regional manufacturing base. The proposal remains subject to due diligence, regulatory approvals and final AIH board sign-off. The offer price is stated as best and final.

Matrix (MCE) is also owned in some of First Samuel’s higher-risk portfolios.

AMI — Aurelia Metals | 1 April 2026

Aurelia Metals is both a long-held position and one that receives regular attention in Investment Matters. The copper-rich, polymetallic mining company based in Cobar, NSW, provides a unique combination of future value, strong cash flows, and a range of options to pursue over the next decade.

As the company has now completed development of the Federation Mine, it is well placed to refinance its existing financing facilities. This month, Aurelia Metals announced it had secured an A$150 million senior secured financing package arranged with a syndicate of tier-one international institutions.

The facility does not require amortisation (payment of principal), cash backing, or mandatory hedging. The package replaces existing arrangements with Trafigura, which remains as a concentrate offtake partner, and is expected to unlock approximately A$38 million in restricted cash. The successful refinancing reflects market confidence in the company’s strategy

AQN – Aquirian Critical Contract Announcement | 15 April 202

Aquirian announced its wholly owned subsidiary Drillforce WA has been awarded an initial three-year supply agreement with ASX-listed Brightstar Resources for drilling and blasting services at Brightstar’s Lord Byron open pit mine in Laverton, Western Australia.

Investment Matters readers may recall the company has been developing critical infrastructure based in Wubin, WA, with an emphasis on explosives and drilling products. Aquirian manufactures explosive materials and provides dangerous goods storage solutions in Wubin. The Wubin facility is a major independent source of emulsion manufacturing. Your author visited the site in November with the company CFO and was impressed with the capacity for future growth.

This deal cements Aquarian’s growth outlook with the revenue from the new contract of approximately $48 million. Services provided span the range of Aquarian’s offerings, including drilling and blasting using Aquarian’s patented technology Collar Keeper® System, and energetics supply and logistics, including storage and reload facilities. The deal falls under a broader Strategic Framework Agreement between the two companies that covers Brightstar’s entire Goldfields Hub.

Aquirian already owns approximately 75% of the required assets, including two T45 drill rigs, with the balance to be funded through cash and existing facilities. This is Aquirian’s second long-term technology-led agreement, following the Mt Ida Gold contract announced in January 2025.

CGF — Challenger Financial | 7 April 2026

Challenger Financial has been a strong performer in client portfolios over the last year, rising more than 50% as assets under management and annuity sales grew rapidly, outpacing market expectations. We have progressively reduced the position into this strength as the share price reached our target valuation, and we are a little underwhelmed by Challenger’s recent acquisitive moves. Firstly, the failed attempt to acquire Pepper Money to broaden its non-bank lending strategy and then secondly, this deal with Bank Of Queensland. We fail to see the valuation uplift from this strategy and will continue to reduce.

On April 7 Challenger announced a capital partnership with Bank of Queensland involving the acquisition of BOQ’s $3.7 billion equipment finance loan book via a whole-of-loan sale, alongside a 12-month forward flow arrangement enabling Challenger to acquire newly originated BOQ loans on an ongoing basis, extendable by mutual agreement. The portfolio provides diversified exposure across SME and commercial customers in capital-intensive industries.

The deal expands Challengers’ whole loan investment strategy and aligns with its stated ambition to diversify beyond traditional annuities and funds management. CIO Graham described the portfolio as high-quality, seasoned and highly diversified, delivering attractive risk-adjusted returns for Challenger and institutional investors.

We are less impressed.

DVP — Develop Global | 9 April 2026

Develop Global announced that its Woodlawn zinc-copper mine in New South Wales has achieved steady-state production, exceeding its nameplate processing capacity of 850,000 tonnes per annum during the March 2026 quarter.

At the centre of our investment thesis, backed by fundamental research and site visit, was a view that DVP could achieve nameplate capacity at Woodland.

In March alone, mined ore reached 80,510 tonnes — equivalent to 966,000 tonnes per annum — while processed ore reached 77,741 tonnes, equating to 933,000 tonnes per annum. Across the full quarter, mined tonnes grew 46% on the prior quarter, processed tonnes rose 25%, and metal concentrate tonnage increased 50% to 14,219 tonnes, with metal concentrate value up 66% quarter-on-quarter. The company credited extensive infill drilling, early development work and disciplined use of low-grade ore during ramp-up with de-risking the operation and establishing the foundation for flexible, consistent production.

Given Woodlawn’s cash flow generation, the fantastic mining services business on which the company was built, and the prospects for its copper-rich Sulphur Springs mine in development, we have not been surprised that the market is increasingly appreciating the value of the DVP portfolio.

The share price has risen 32 per cent in April, fully recovering from the Iran War sell-off.

MI6 — Minerals 260 | April 2026

Amongst the stars of the portfolio in FY26 Minerals 2060, the upstart WA gold development company continues to produce fantastic results. Almost immediately following our participation in the recapitalisation and Bullabulling acquisition in April 2024 positive developments have followed.

From an initial 12c purchase price, MI6 is now trading closer to 80c. Whilst we have sold much of the position, it remains an important part of the portfolio’s gold basket.

In recent weeks, Minerals 260 reported additional strong drilling results from its 100%-owned Bullabulling Gold Project in Western Australia’s Eastern Goldfields, with new assays continuing to support resource confidence and growth. The latest batch covered 22 holes for 5,425 metres across the Bacchus and Phoenix deposits, both of which are contained within the December 2025 resource base of 130 million tonnes at 1.0 g/t gold for 4.5 million ounces. Standout intercepts at Bacchus included 7 metres at 7.2 g/t from 86 metres, 11 metres at 3.3 g/t from 185 metres, and 28 metres at 1.7 g/t from 159 metres with internal high-grade zones reaching 22.6 g/t. Drilling is confirming mineralisation continuity along the 8.5-kilometre strike extent of the resource while also testing lenses outside the current estimate. Seven rigs remain on site. A pre-feasibility study incorporating a maiden ore reserve remains on track for mid-CY2026, with an updated Mineral Resource Estimate also planned for that time to feed into a definitive feasibility study scheduled for early CY2027.

OBM — Ora Banda Mining Quarterly Production | 16 April 2026

Ora Banda Mining has been an outstanding performer for portfolios since its first appearance in 2025. We recognised the potential in this business if it could successfully transition from an open-pit operation to underground mining and advance its next project, the Sand King mine. These milestones have been achieved, and we’ve also had the strong gold price during the process, further accelerating returns. We visited the site in late 2025 and came away impressed by the scope for future drilling and the team’s competence in delivering investment.

Pictured below are the “before and after” shots from 2025 of the Sand King Decline after 12 months of development. This team is great at getting things done!

Figure #5: Before and After: Sand King decline

Source: Ora Banda Mining

Ora Banda Mining delivered its March 2026 quarterly activities report, recording an all-time high quarter of 38,766 ounces of gold produced — up 21% on the prior quarter — and bringing FY26 total gold sales to 101,200 ounces.

We loved the cash flow with free cash flow for the quarter, a record $76.3 million, lifting the closing cash balance to $231.7 million, up 49% from December. Ora Banda is a company that is turning high gold prices into cold, hard cash.

The quarter also delivered an updated 1.3-million-ounce Mineral Resource for the Round Dam project, as well as high-grade intercepts from the Golden Pole and Little Gem discoveries. A notable headwind was the all-in sustaining cost (AISC) of $3,612 per ounce, elevated largely by third-party processing costs. This was a necessary burden of success, as the available ore exceeded the capacity of the company-owned plant. Management confirmed that studies for a new standalone 3 million tonne per annum processing plant are advancing, with a construction decision expected in the June quarter. Over the quarter, $52.5 million was invested in capital projects, resource development and exploration, consistent with the company’s $73 million FY26 exploration and development budget.

ORA — Orora Trading Update | 9 April 2026

Orora is a more recent addition to client portfolios, along with it’s larger competitor Amcor. The two complementary positions give clients exposure to defensive consumer businesses that generate strong, stable cash flows. They have diversity in geographical and product mix, with Orora focused on glass, cans and fibre-based packaging, while Amcor is more rigid plastics and flexible packaging.

Source: Orora website

However, as noted in the introduction to this week’s Investment Matters, neither Amcor (AMC) nor Orora (ORA) is well placed for global conflict. Both stocks have sold off despite reporting positive financial updates in February.

The sharp deterioration caused by the war led to this month Orora released a trading update revealing the material financial impact of the Middle East conflict on its premium glass division, Saverglass.

The company’s Ras al Khaimah facility in the UAE — which accounts for approximately 15% of Saverglass’s total production capacity, primarily supplying high-end bottles for North American markets — has been transitioned to a closed-loop hot idle state, with furnaces maintained but all bottle production halted due to disruption of shipping and overland routes. Production is being redirected to Orora’s Mexican facilities to meet customer commitments.

The combined impact is estimated at €20 million to €27 million on second-half FY26 earnings, comprising €9–11 million in direct shutdown costs and €11–16 million from weaker demand and negative sales mix in the premium wine and spirits segment. Saverglass FY26 underlying EBIT guidance has been cut to €63–68 million, from a prior expectation broadly in line with FY25’s €79.2 million. Orora also paused its on-market share buyback program. Guidance for the Cans and Gawler Glass segments was unchanged.

Orora is a small position in portfolios that we are monitoring for potential increases during this weakness. The current global situation, however, is impacting all of the obvious businesses leveraged to fuel prices.

The information in this article is of a general nature and does not take into consideration your personal objectives, financial situation or needs. Before acting on any of this information, you should consider whether it is appropriate for your personal circumstances and seek personal financial advice.