Copyright 2026 First Samuel Limited

Read the previous Investment Matters here.

In this week’s Investment Matters, we focus on:

- Iran War, importance of a path to resolution

- deploying cash: what are the opportunities?

- Merits of Income Securities in changing economic conditions

- results review for Nanosonics

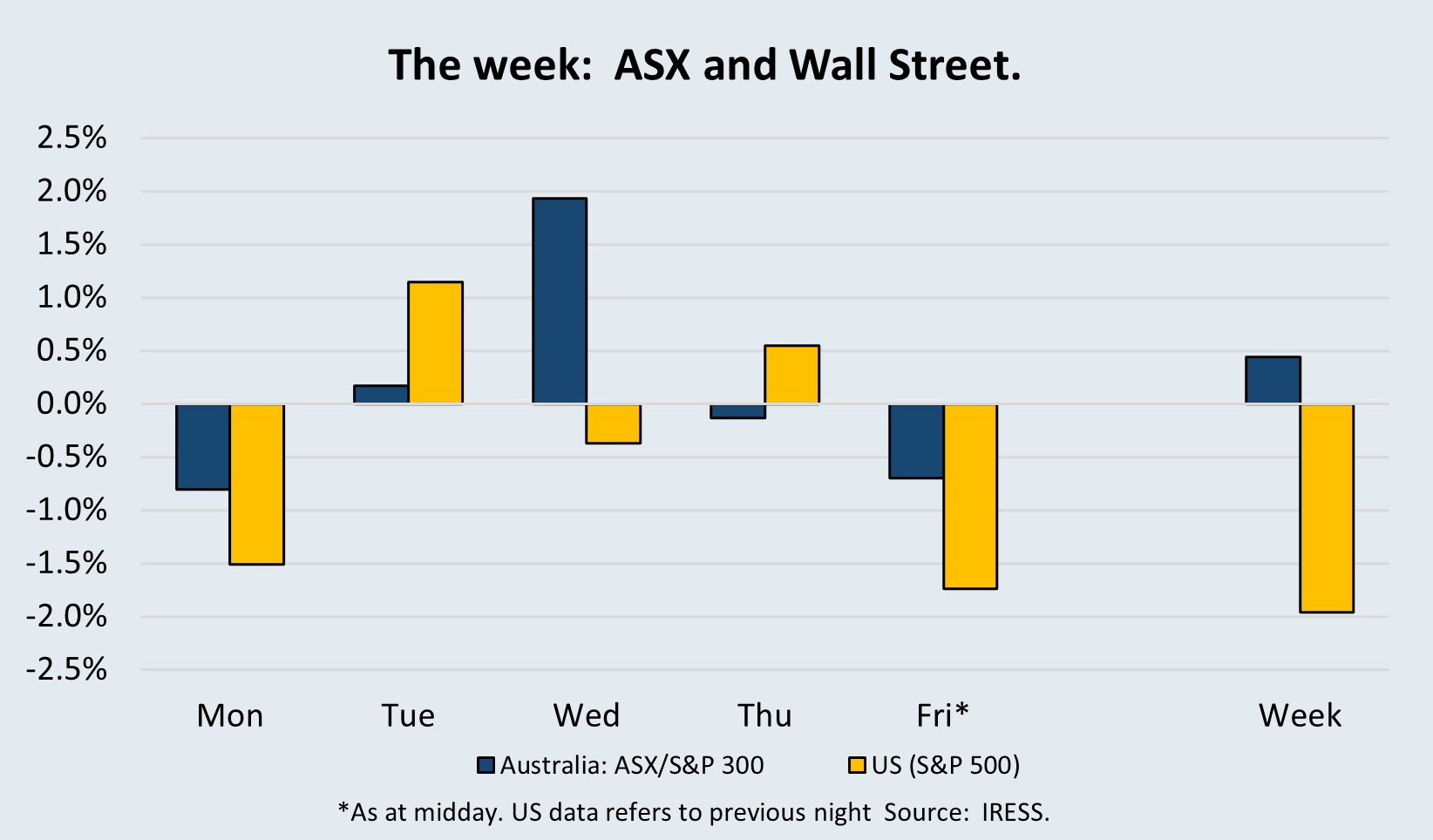

The Market

The importance of a path to the resolution of the Iran War second-round effects

Markets do not need a perfect outcome

Last week in Investment Matters, we noted that even amid a war-driven sell-off, there were still paths to resolution. That remains the key point. Markets do not need a perfect outcome. They need a credible path away from escalation, a return of oil supply in a reasonable time, and some confidence that the conflict does not produce a much larger shift in the long-run geopolitical balance.

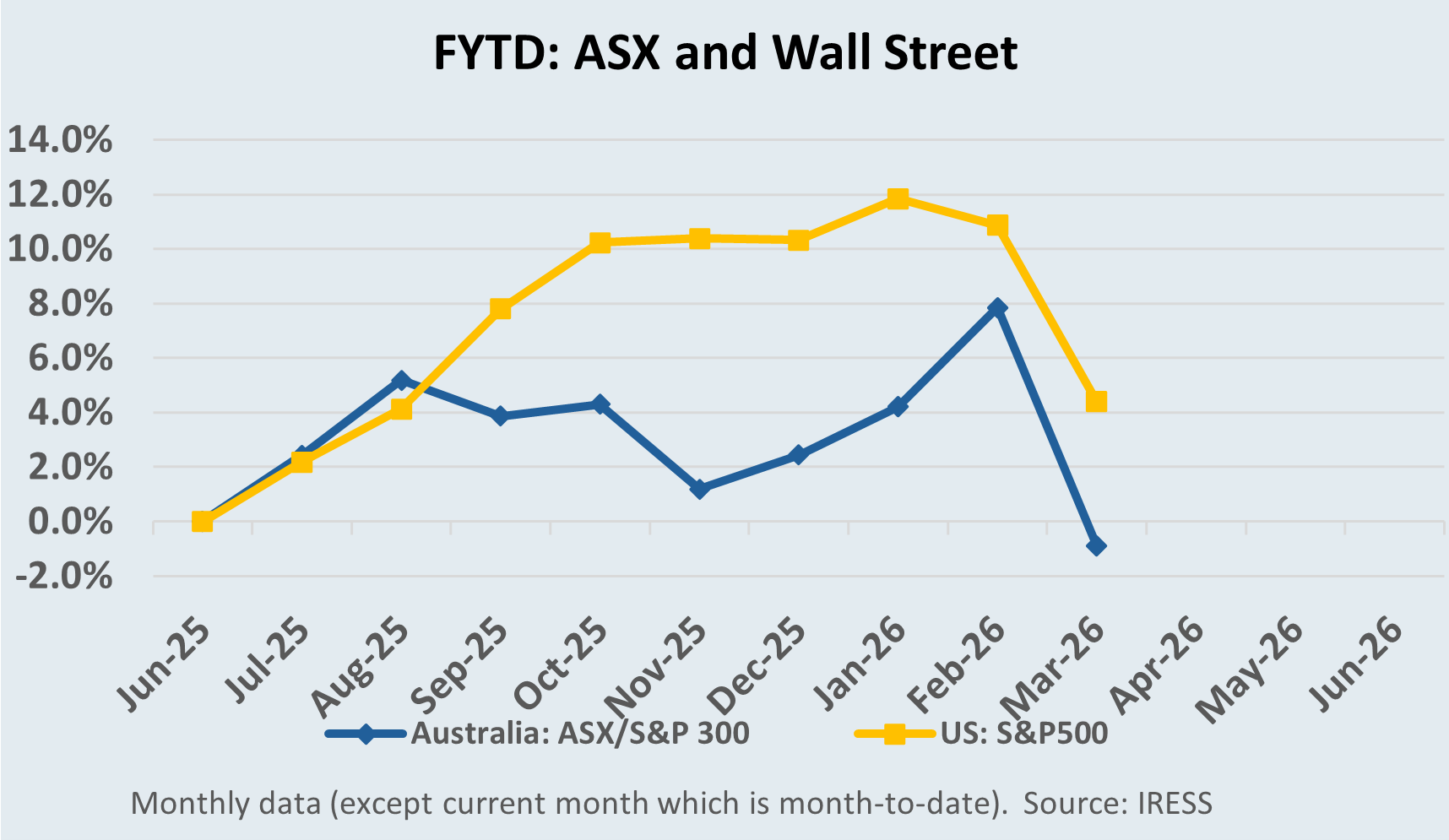

By the close on Monday, 23 March, ASX-listed stock prices, especially outside the top 20, had fallen by more than 10 per cent. This followed a highly irregular February that had already seen signs of weakening outside the largest stocks.

In response to the changing landscape and the magnitude of the discounts, we began to pivot from defence to offence for the first time in more than a year.

| Decline from February 28th to Monday, 23rd March | Movements from January 31stto Monday, 23rd March | |

| AS20 | -6.1% | +1.4% |

| ASX20 to ASX50 | -11.6% | -13.0% |

| ASX Mid-Cap ETF | -12.8% | -12.9% |

| ASX Small Caps | -13.6% | -15.8% |

| Overall Market | -8.6% | -5.1% |

We have begun deploying our cash holdings into the Australian equity portfolio. For the first time in FY26, we have reduced our cash holdings this week by circa 4% of the portfolio. A back-channel to begin negotiations emerged, with Pakistan acting as an intermediary, matters because it points to a route for de-escalation that sits within the existing regional framework. It suggests the conflict may yet be contained, negotiated, and ultimately normalised without immediately redrawing the strategic map.

We have been increasingly concerned with two aspects of the conflict. Firstly, the elongation of conflict leads to vast global shortages of energy and its impact on economic activity. Secondly, the degree to which the geopolitical map is redrawn both in the Middle East and more broadly.

China’s role and the impact on Russia, Turkey, and other Gulf states vary greatly across possible scenarios. Among those scenarios are which country brokers the resolution and the timing and context of the resolution.

What if China steps into the vacuum?

If the conflict were to end with China expanding its standing in the Middle East simply by waiting and stepping into the vacuum, the implications would reach far beyond oil. That would represent a more material change in the geopolitical landscape and justify a higher long-run risk premium across global equity markets. In other words, resolution is not enough by itself. The shape of the resolution matters.

That is why, in our view, the current setup for resolution is manageable but not yet comfortable. A framework in which conflict eases, supply returns and oil settles at a somewhat higher long-term level is something equity markets can absorb.

What would be harder to absorb is a settlement that leaves the West weakened, regional power dynamics altered, and capital markets forced to consider a structurally less stable world. For now, using Pakistan as the channel is one of the more constructive aspects of the situation.

Impact on the petrodollar remains a consequential risk

The long-term legacy of the Iran conflict for the dollar (USD) could lie in how it tests the foundations of the petrodollar regime. If fault lines are further exposed, there could be significant downstream effects on the dollar’s use in global trade and savings, as well as on its role as the world’s reserve currency.

In an excellent Deutsche Bank Research Institute report this week, they summarised it best. “The world saves in dollars largely because it pays in dollars. The dollar’s dominance in cross-border trade is arguably built on the petrodollar: globally traded oil is priced and invoiced in dollars. This arrangement can be traced to a deal struck in 1974, in which Saudi Arabia agreed to price oil in dollars and invest its surpluses in dollar-denominated assets, in exchange for US security guarantees.”

Because oil is essential for making and moving goods, global trade naturally relies on the dollar. This has given the U.S. the unique ability to spend more than it earns for 50 years, knowing that other countries will always need dollars to buy the energy and minerals they require.

The foundations of the petrodollar regime have been under pressure even before this conflict. The current conflict may expose further fault lines by challenging the US security umbrella over Gulf infrastructure and maritime security for global oil trade.

Petroyuan?

Damage to Gulf economies could encourage an unwind of their foreign-asset savings, held largely in dollars. In this context, reports that the passage for ships through the Strait of Hormuz may be granted in exchange for oil payments in yuan should be closely followed. The conflict could be remembered as a key catalyst for erosion in petrodollar dominance and the beginnings of the petroyuan.

A world that becomes more self-sufficient in defence and energy would also hold fewer dollar reserves. The Middle East’s huge strategic importance to the dollar’s role as the world’s reserve currency should not be underestimated. The current conflict may be the perfect storm for the petrodollar.

Weakened demand for dollars for energy will tend to increase US and, in turn, global interest rates.

Sell-off is creating opportunities in this market, however

Against that backdrop, the breadth of the sell-off has created opportunities. Much of the damage in Australia has occurred away from the very largest names. Some of the most expensive stocks in the market, including the Big 4 Banks, have held up relatively well, while a wide range of industrials and cyclical businesses have been sold down heavily.

That has left parts of the market looking plainly too cheap. We identified in recent Investment Matters that the sell-off in industrials had been particularly severe. That remains our view. Names such as SGH and James Hardie have fallen hard, even though the medium-term value of those businesses has not moved anywhere near as much as their share prices.

We have therefore chosen to add across a range of names and broaden the portfolio rather than make one large call. Our research agenda sits behind this. On any given day, there are stocks we like, but not at every price. In many cases, we are happy to own more only when the market gives us the opportunity. That applies both to core holdings such as QBE or Woolworths, where position size should respond to valuation, and to stocks from the research bench that can become new positions when prices move to the right level.

New investments

From that bench, we have used the current conflict to broaden our minerals exposure through WA1 Resources Limited (WA1). For some time, we have been looking for niobium exposure to sit alongside our existing positions in copper, zinc, lithium and rare earths. WA1 gives us that. Niobium is not a large market, but it matters because it is strategically useful and supply is concentrated. These positions are not always large on their own, but in aggregate, they reflect a deliberate research view about where future value may emerge.

Another new portfolio entrant is Artrya, a very exciting biotech company, which suffered share price falls in recent weeks. Artrya is an Australian medtech company that uses AI to read coronary CT scans, identifying plaque and narrowing in the arteries that supply the heart. In plain English, it is trying to help clinicians work out more quickly and more accurately which patients are low risk, which need further attention and which may be heading toward a cardiac event. That is appealing because it is not a science experiment in search of a market. It is a product aimed at improving diagnosis in one of the world’s largest areas of healthcare demand.

It is the sort of stock that belongs on a research agenda because it offers genuine medium-term upside if execution continues. It also broadens the portfolio in a different way: not through macro exposure or resources, but through company-specific innovation and product adoption. In addition, in combination with Nanosonics, discussed in the next section provides additional exposure to health care product demand without necessarily doubling the risk with simply one particular product.

The broader point is simple: our high cash levels did their job during the sell-off. This week, we began the process of redeploying part of that defence.

The war is not resolved, but the market has already priced in too much damage across a range of businesses we are happy to own. At the same time, it is sensible to take some profits in stocks that have benefited from the conflict, particularly oil names. That is the balance now: begin adding where prices have become attractive, keep building portfolio breadth, and stay focused on the nature of the resolution rather than the noise around it.

Nanosonics 1H26: Coris on its way

Nanosonics’ half-year results were better than the market reaction suggested. Indeed, since just prior to the result on the 23rd of February, the stock price is flat, versus a broader market fall of 12% amongst smaller ASX companies over the same period.

Revenue for H1 FY26 rose 9% to $102.2 million, recurring revenue increased 9% to $75.7 million, capital revenue also rose 9% to $26.5 million, and operating margin expanded 27% to $8.5 million. Reported EBIT was up 15% on a constant-currency basis, although the rising AUD impacted it. The statutory print looked softer than the underlying operating performance, so the quality of the result was partly obscured by currency.

The operational story was also stronger than the top line alone implied. Gross margin moderated to 76.3%, reflecting tariffs, product mix and higher airfreight costs, but Nanosonics kept a tight grip on costs. Total operating expenses rose only 4% to $69.5 million, allowing earnings to hold up much better than many investors likely expected based on the revenue line alone.

A regular Investment Matters Reader would know how important that operating discipline is to us. Management is finally scaling the business sensibly and balancing cash needs to fund Nanosonics’ new growth platforms. On the negative side, we wanted a cleaner beat on revenue and consumables.

Core franchise is worth more than the current market cap

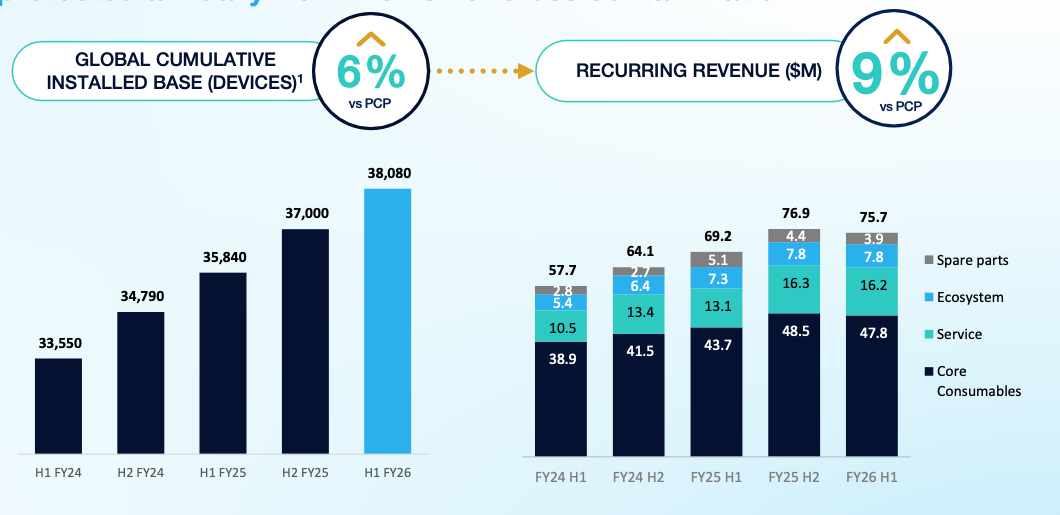

The core reason we remain constructive on Nanosonics is that the Trophon-only franchise continues to look like an excellent business. The installed base increased to 38,080 devices, supported by 2,070 total unit installations in the half and a record 980 upgrades in North America. That installed base is the engine of the model. It supports recurring consumables, service revenue and, increasingly, software-led monetisation. The Trophon-only business delivered an operating profit of $25.6 million for the 1st half, up 20%, with margin as a share of sales rising to 22.9%.

Those are very strong numbers. They show the legacy franchise is not simply mature and defensive; it is still growing, still highly profitable and still producing operating leverage. A yearly full costed run-rate profitability of circa $50m growing this quickly would be worth $1bn standalone.

Figure #1: Nanosonics – Trophon (LHS) and Coris (RHS)

Source: Company presentation

The innovation progress in the half also deserves more attention than it received on the day. Nanosonics launched Trophon3 and the Trophon2 Plus software package, cleared Coris regulatory hurdles in Australia, the EU and the UK, secured a new headquarters and manufacturing facility for an April 2027 move, implemented a new ERP system, and went live with cloud-based traceability offerings. Management is simultaneously strengthening the operating backbone, building digital capabilities, and extending the product portfolio.

We were pleased to see this progress at a time when it has become clear that the core focus of the business is to launch Coris and extend Nanosonics into a broader infection-prevention platform.

Other concerns genuine.

That said, we do think the market’s concerns were real, even if they were overdone. Our two main reservations about the result were the rising Australian dollar, which does reduce the AUD value, and softer growth in consumables.

Figure #2: Nanosonics performance by half – rising installed base (LHS) but disappointing recurring revenue (RHS)

Source: 1H26 Results Presentation

Understanding what was really happening inside recurring revenue in the US was key. CEO Michael Kavanagh note that service revenue in the US grew 24% on 1H25, core consumables grew about 9%, the broader ecosystem grew about 6%, but spare parts fell about 23% as older machines were upgraded. That mix helps explain why the market may have marked the shares down. Consumables growth is central to the investment case because it is the cleanest indicator of procedure-linked activity across the installed base.

Coris arrives

Regulatory progress across Australia, Europe and the UK, plus the first controlled market release in the UK after period end, means the market is now dealing with an execution timetable. The strategic upside remains significant. After what feels like a decade since they began in earnest Coris is no longer just an abstract R&D story.

Coris is now moving from concept to commercial reality, even if revenue is still largely an FY27 story. During the half, Nanosonics achieved regulatory progress across Australia, Europe and the UK, submitted its first FDA 510(k) for expanded indications. An FDA 510 (k) is a premarket submission to the FDA demonstrating that the device to be marketed is as safe and effective, that is, substantially equivalent, to an already legally marketed device. Nanosonics then moved into the first controlled market release in the UK after the period ended. Management continues to point to broader commercialisation from FY27, following real-world learning during the controlled-release phase. There is still execution risk here, of course, but value in Coris is clearly becoming more tangible. Within 18 months, the business will have a second platform in the market while the first platform continues to generate high returns and strong cash generation.

Our view remains that there is tremendous value in Nanosonics. The market, in our opinion, is more than discounting the near-term issues around currency and softer growth in consumables. The core Trophon business is already a highly profitable, cash-generative franchise, and on our reading, it is worth more than the current share price on its own. If that is right, the market is attributing little value to Coris, which could plausibly add another 50% of value over time if commercialisation is executed well, and even less to the broader innovation pipeline. That strikes us as too pessimistic. Investors are being offered a proven, high-quality core business today, while paying very little for a potentially meaningful second act.

The information in this article is of a general nature and does not take into consideration your personal objectives, financial situation or needs. Before acting on any of this information, you should consider whether it is appropriate for your personal circumstances and seek personal financial advice.