Key Takeaways

- Australia is experiencing the largest wealth transition from baby boomers to younger generations.

- Many individuals are unprepared for this transition due to a narrow focus in wealth management advice.

- Optimal Intergenerational Wealth Management involves planning today, rather than waiting until after death.

- Key objectives include tax optimisation, asset distribution certainty, and protection for beneficiaries.

- It is essential to engage with experts to navigate complexities and secure financial futures.

Massive wealth transition underway

We now sit at the beginning of the largest-ever transition of wealth in Australia’s history. That transition is not from taxpayers to the government. But, instead, from the baby-boomer generation (born 1946 to 1964) to their children and/or grandchildren.

Who is prepared for the great transition of wealth?

My experience is that too few people are fully prepared to optimise tax, provide certainty and give protection in planning their wealth transition.

The reason is that the focus of many in the wealth management/financial planning industry is on limiting advice to deal solely with the testator’s benefits and on the sale and distribution of that firm’s financial products. This compares to advice on their client’s broader situation and wider family matters (e.g. family tax).

Hence, for most people, a recommended estate planning package includes a will, a letter of wishes and a superannuation ‘binding death benefit nomination’ (BDBN) form and advice about investing the current asset pool.

However, this standard approach is insufficient for families with reasonable wealth or complex circumstances as it lacks the customisation necessary to optimise tax, provide certainty and give asset protection.

After death, it’s too late

Intergeneration wealth planning certainly starts today. But also, the actual transition of wealth often starts today, not on your passing.

Instruments such as a will or an BDBN are constrained and procedural. They are designed to take effect after death, in a prescribed manner and primarily direct the distribution of assets.

In so doing, they miss the opportunity of cross-generational transfers of income and/or capital for family tax-management or asset protection reasons (see below for an example).

Furthermore, many of these instruments can hardly provide for timely outcomes (note the recent ASIC action against a large industry superannuation fund over its delayed payment of benefits).

Optimal intergenerational wealth management should have the structures and processes in place today to meet three major objectives:

1. Optimal overall tax on Intergenerational Wealth Management

Too many people (a) see ‘tax’ as only their individual tax and (b) intergeneration wealth transition as happening after their death. This accepts tax as a fait accompli and ignores the opportunity to act before death.

It makes sense the less of your wealth that goes to the ATO, the better. Today or tomorrow, from you or from your beneficiaries.

For example, inter vivos (between living persons) cross-generational transfers of income and/or capital can significantly reduce the family tax obligations. They can also provide assistance for needy recipients (e.g. home loan deposits for children).

And note that testamentary charitable bequests seem nice, but are not tax-effective to your estate. Better to give today.

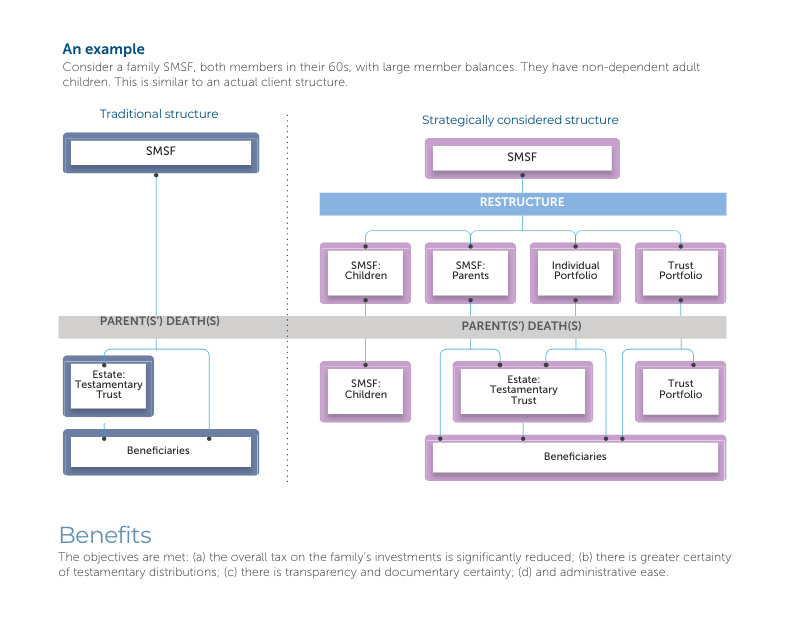

Consider the below example of restructuring before death.

2. Certainty of asset distribution

Simply having a current will, even one that clearly states who gets what, doesn’t guarantee a smooth and effective distribution of your estate. True certainty comes from more than just naming beneficiaries. It involves strategically planning for things like minimising taxes for those receiving your assets and giving your executors, trustees, or directors (and their successors) the flexibility to adapt to unforeseen changes, such as shifts in family dynamics or tax laws.

This extends to consideration of the potential addition of a corporate beneficiary, and possibly with limitations on which beneficiaries can or should receive income compared to capital.

Ultimately, the goal is to create an estate plan that’s both robust and adaptable, while also maintaining a level of simplicity that avoids unnecessary complications.

3. Protection of testamentary distributions

So-called ‘predator protection’ is vital. This is more than consideration of vulnerable beneficiaries, for example bequests where the recipient may be unable to manage the asset.

For example, too often a bequest to a child is put at risk at a future date by a claim from a divorced or separated partner.

Other objectives

Of lesser significance, but nonetheless, important objectives are:

4. Transparency to and understanding by stakeholders

Make your testamentary intentions clear to beneficiaries

5. Documentary certainty

Opaqueness is costly

6. Administrative ease

Asset identification, asset access (note the problems of large superannuation funds in releasing superannuation benefits), and asset distribution should be considered

7. Investment efficiency

Multiple managers, illiquid assets, and multiple accounts are examples of costly structures that often evolve over time.

Summary

The operation of intergeneration wealth management starts today, not on your passing.

It is more than a will, a BDBN and a letter of wishes.

You will need advice to optimise tax, provide certainty and manage family relationships.

First Samuel has the experience and experts to guide you. If you want to secure the financial future for your family, get in touch with us.

The information in this article is of a general nature and does not take into consideration your personal objectives, financial situation or needs. Before acting on any of this information, you should consider whether it is appropriate for your personal circumstances and seek personal financial advice.