Copyright 2026 First Samuel Limited

Key Takeaways

- Inflation in Australia remains high and persistent, leading to expectations of interest rate hikes from the RBA.

- Client portfolios are positioned for higher inflation and interest rates, maintaining significant cash balances amid high prices.

- Non-tradables inflation, largely driven by domestic services, continues to exert upward pressure on prices, while the RBA struggles to manage these trends.

- Develop Global continues to perform well in the mining sector, focusing on clean metals and robust cash flow generation amidst rising commodity prices.

- Emerging technologies and AI present risks to established tech stocks, but Life360’s business model appears resilient in this environment.

Read the previous edition of Investment Matters.

In this week’s Investment Matters, we are stepping back from last week’s dense analysis of the Chinese economy. A cognitive holiday, if you like, much needed after a week of high temperatures in Victoria. Whilst the cognitive load may not be as extreme, the impact on portfolios of this week’s changes remains high.

The release of ABS inflation data increased the risk of the RBA raising interest rates. The data cemented the view that inflation is persistent and needs policy intervention.

Gold nervously reached previously unimaginable highs, and the AUD is rapidly appreciating above 70c after remaining below that level since 2023. Global currencies are in a state of flux.

The pace of change reminded your author that, when it comes to structural changes in economies and markets, there is no choice but to be early in your investment positioning; the only other choice is being late.

Being early in small, measured steps can pay off in a world where the severity of change continually surprises.

The Market

Portfolio summary

Client portfolios are positioned at the margin for persistently higher inflation, higher interest rates and a strengthening AUD. We retain a significant cash balance amid relatively high prices in certain global markets.

Inflation: High and getting higher, families lament

Whilst the now monthly release of inflation data often includes excessive detail and analysis, this week’s release elicited a single, uniform response.

Inflation is simply too high and persistent.

“Too high” from the perspective of expected deliberations of Australia’s central bank, the RBA. The level of inflation is higher than it expected, and possible signs of a reversal in upward momentum simply aren’t there. Odds now favour the RBA raising interest rates at its next policy meeting in early February.

Sadly, one cohort of the population will pay the price: mortgage holders, despite limited evidence that these already-stretched households are the root cause of inflationary forces.

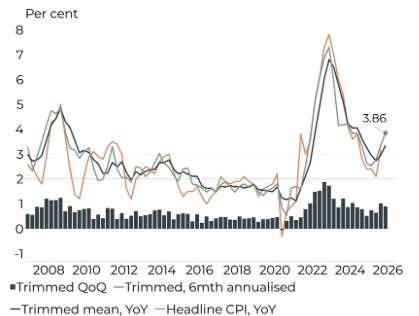

Figure #1: All measures of inflation are reaccelerating

Source: ABS, MacroBond, Barrenjoey Research

The data showed that the RBA’s preferred measure, the “six-month annualised rate of trimmed mean inflation”, is now running at 3.9%. It is shown in the figure above in green. It is clearly too high for policy settings targeting the 2-3% range through the cycle, as shown by the dotted horizontal lines. In the weeds of the detail, the data shows persistent price pressures across a broad range of goods and services.

‘Non-tradeables’ the problem

Readers may recall recent articles in Investment Matters that call out our preferred way of looking at CPI, the rate of growth of ‘non-tradable’ prices, those that are primarily domestic and not exposed to imports.

Non-tradables include most services, government services, health, education and housing costs. Note that the price of existing homes isn’t in the CPI, but the cost of new dwellings and rent is included.

Whereas Australia for decades has benefited from lower tradable price inflation, often importing from China, its domestic non-tradable inflation has remained high, and we have argued remains the source of future inflationary pressure.

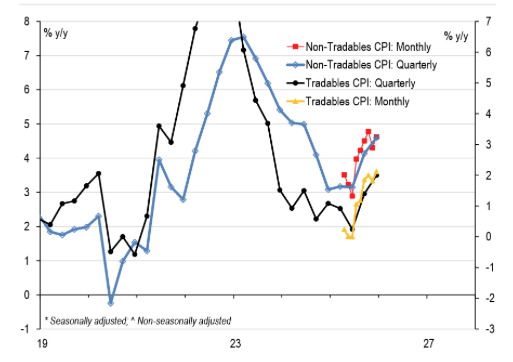

Figure #2: Tradables and non-tradables inflation are accelerating

Source: ABS, MacroBond, UBS

New data only confirms this, as shown above. Non-tradables inflation, whether the quarterly series in Blue or the monthly series in Red, is running closer to 5% (LHS of chart), much higher than its ~3% pace in late 2024/early 2025 and the ~2% y/y pace prior to the pandemic in 2019.

This is too high. It signals that households are already losing purchasing power for domestic goods and services, as wage growth simply isn’t this strong.

Excess migration

The pressures of excess migration continue to shape inflation risks. Higher housing costs, especially rents, but now also new housing prices, are still feeding through these CPI measures. But inflation is now much broader, with food and non-alcoholic beverages, as well as recreation and culture, all rising.

The concern for the economy, stuck within a paradigm of high population growth, high house prices and high government spending, is that there is no circuit breaker in our minds other than intergenerational inequities.

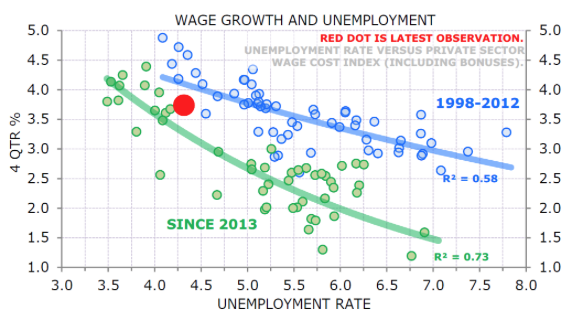

Consider the excellent chart below, produced by Minack Advisors, which shows the link between the unemployment rate and wage growth across two distinct periods since 1998.

Figure #3: Tight labour market keeps wage growth high

Source: ABS, Minack Advisors

Note the two series. Firstly, in Blue between 1998 and 2012, where population growth was more muted, and government spending was much more balanced. And secondly, in Green since 2013, where mass migration has exploded, especially after considering temporary residents not included in population metrics, government deficits exploded, and the population-led growth model was fully embraced.

The slopes of the Blue and Green lines show the tendency for higher unemployment to coincide with lower wage growth and, in turn, inflationary pressures. The steeper the line, the faster the wage/price response to higher unemployment.

Note that, in Green, average wage growth has been weaker since 2013 (lower green dots). In fact, real wages (after inflation) have barely grown since 2013. But the impact is clear: in this environment, we can control inflation and wage growth exceptionally well with higher unemployment. This is the relationship shown in the steeper Green line on the chart. Between 1998 and 2012, when the economy was stronger, more balanced, and more resilient, greater stress would have been required on demand to reduce inflation and wage growth.

How can we increase unemployment in 2026 to reduce inflation, especially in a low-productivity environment? How in an economy with (a) a huge supply of cheap workers, (b) rapid population growth driving confidence in investment, (c) high levels of government spending, much of which is income support, and (d) an entire generation of older Australians with record levels of income and spending.

Well, the answer could be to change some of those settings: government spending, investment, taxation, population dynamics, and productivity enhancement.

But the RBA only has higher interest rates in its arsenal. So next month, they will penalise a small cohort of the population with mortgage debt.

Policy solutions from the political class appear off the agenda based on the upcoming self-absorbed nonsense.

Australia now has a second-best economic policy, if I am being generous…

But the impact of this second-best policy on the portfolio is clear: avoid banks and consumer discretionary, and favour foreign income and companies that serve global markets for growth, investment, and innovation.

Around the ground – portfolio news : Life 360

A US UBS analyst summed it up well this week, Life360 “dispelled top of funnel weakness concerns”. “Top of funnel weakness” is a perception that a business is failing to generate sufficient new leads at the beginning of the customer journey. The Life360 share price fell by more than 15% in early January alone due to these concerns.

In line with global market listing rules, companies are required to update the market outside normal reporting periods if the board or management believes the market is misinformed. Life360 did this on 23 January, when it updated the market ahead of its planned 3 March release of fourth-quarter operational performance results.

The results were magnificent, and the share price rallied more than 30%.

In line with broad weakness in the high-growth technology sector, Life360’s share price had seen significant weakness, with the share price falling from $50 in mid-November to a low of $25 in mid-January.

Clients may recall that we first purchased Life360 shares in the low $20 range in late 2024 and took advantage of peak prices to realise our purchase cost in full, retaining more than half of our position.

What is Life360? What were the 4Q results?

Life360 the global-leading location tracking app used to monitor the real-time movements of family and friends. Services included safety features like crash detection, roadside assistance, and location history.

As a reminder, Life360 uses the freemium business model that combines “free” and “premium,” where it offers its basic functional services for free, while charging for advanced features. Total users are measured as Monthly Active Users (MAU), and paying users are referred to as Paying Circles. The results showed that;

- Life360’s global MAU base reached 95.8 million in Q4 2025, with full-year 2025 net additions of 16.2 million (20% growth YoY), delivering the strongest Q4 user growth in the Company’s history

- Paying Circles reached 2.8 million in Q4 2025, with full-year 2025 net additions of 576 thousand, representing the highest annual net adds on record

- Newly acquired MAUs are converting to Paying Circles at record rates

- Strong momentum across both US and International markets

Looking ahead, the company now expects 20% MAU growth in 2026, which will not only provide significant financial leverage but also further enhance its value proposition for advertisers as it expands its unique location-enabled ad-serving technology.

Massive earnings leverage

Another highlight in the early update was the earnings momentum the business is generating. Stepping back from the enormous scale of MAU of almost 100 million, it is worth noting that the number of paying customers remains relatively small at 2.8 million Paying Circles.

Nonetheless, the profitability of this small cohort is impressive, and the marginal profitability of additional revenue is fantastic. High marginal profitability is referred to as earnings leverage.

Generating almost USD500m in revenue, the company provided guidance of operating income (adjusted EBITDA) of between USD87-90m. In 2025, revenue grew USD115-120m and the company increased EBITDA by approximately USD45m. Almost 40c in every additional dollar of revenue was profit.

At these profitability levels, Life360’s core location-sharing business, regardless of advertising opportunities, justifies the current share price.

Life360, AI and risks to technology stocks

A broad range of global technology stocks has come under increasing pressure from AI. We have written about the hype around AI and data centres, but we have enormous respect for AI’s transformative potential.

One increasingly prevalent argument is that AI enables new entrants to build alternative business models that challenge existing large, highly profitable online businesses.

Part of the logic is that transforming existing corporate structures and cultures is very difficult; many Readers with corporate experience would attest to the challenges of change. Perhaps AI-native startups can deliver productivity and product benefits faster than existing businesses,despite their smaller scale.

Online classifieds, including real estate, travel, and a range of financial services businesses, appear susceptible to entirely new AI-native solutions. That is not to say existing businesses such as Realestate.com.au cannot develop AI solutions within their current offerings, but the combination of the threat of new entrants and the cost of providing additional services limits profit growth. With most large-scale technology companies trading at valuations that presume high and fast-growing profitability, the downside risks to their share prices is high.

One potential benefit Life360 retains in such an environment is that AI, at least at this stage, appears poorly suited to enhancing the relatively simple benefits of the existing Life360 offer. The product’s low cost, especially compared with the costs of search and online classifieds, also limits the profit pool available to new entrants at a lower scale.

Mining Companies: Quarterly Updates – Develop Global

An exciting addition to the portfolio in late 2024, Develop Global has proven to be both a successful investment and a company with a strong track record of delivering on its growth and investment plans.

Develop Global is an Australian resources and mining services company primarily focused on producing “clean metals” that are critical to the global energy transition. The firm operates under a dual-track strategy, serving as both a direct mine owner and a specialist in underground mining services. The Woodlawn project in New South Walews has been the first project delivered as a mine owner. The rapid development of its new Sulphur Springs Copper project in Western Australia is proving well-timed as the global copper price continues to surge.

We were attracted by the business model that leverages an internal workforce of underground mining specialists. The cash flow from these Mining Services continues to help offset the capital-intensive nature of resource development.

The net result is a lower level of value-dilution through capital raisings that early investors often face. Dilution often occurs even when higher mineral prices improve the value and viability of in-development mines. With metals prices surging across the board, Develop’s project now looksvery likely to be delivered within existing financial resources.

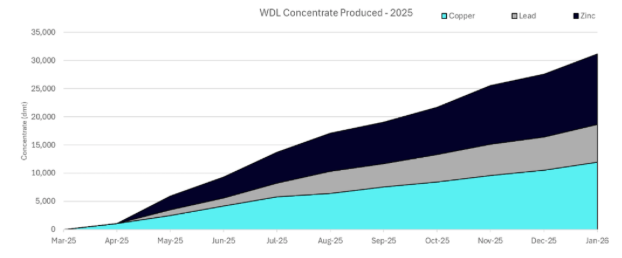

This week, we appreciated the latest update from the always-impressive CEO, Bill Beament. We particularly appreciate the ramp-up of the Woodlawn Mine, shown below. The project remains on track for steady-state production in the March quarter of 2026.

Figure #4: Woodlawn Mine – Ramp up concentrate produced through 2025

Source: Company reports January 2026

With lead prices trading at reasonable levels, zinc prices up 20% cent in a year and at levels seen rarely over the past decade, and copper at record prices, the outlook for cash generation from Woodlawn in 2026 is fantastic.

Cashflows are increasing due to the presence of gold and silver “by-product credits.” Beament highlighted this week that buyers of concentrates are increasingly rewarding poly-metallic miners, such as Woodlawn, with higher credits for these by-products. This lowers the “all-in sustaining costs” (AISC) for the primary base metals by offsetting production expenses. Whilst these credits have always existed, the surge in prices, especially for gold, is making them more relevant than ever.

Improved cash flow is enabling other options available to Develop to be exploited.

Understanding the importance of retaining optionality was another feature that attracted us to this business. A great example was demonstrated this week with Develop outlining plans for its Pioneer Dome lithium assets. Following the surge in spot lithium prices, which has benefitedportfolio companies including IGO Limited, projects that were once mothballed are now being reconsidered.

In the case of Pioneer Dome, Develop has reactivated preliminary off-take negotiations, project financing and planning of pre-development activities. The company noted that bringing Pioneer Dome into production could cost as little as A$35-40m.

Cost reductions, quicker development paths for Sulphur Springs, and upside from Pioneer Dome led to a 10% increase in our very conservative valuation of Develop. This valuation does not assume that elevated prices for Gold, Zinc, or Copper are sustainable, but nevertheless represent an attractive investment at this stage of the company’s “development”.

The information in this article is of a general nature and does not take into consideration your personal objectives, financial situation or needs. Before acting on any of this information, you should consider whether it is appropriate for your personal circumstances and seek personal financial advice.