Copyright 2025 First Samuel Limited

Read last week’s Investment Matters.

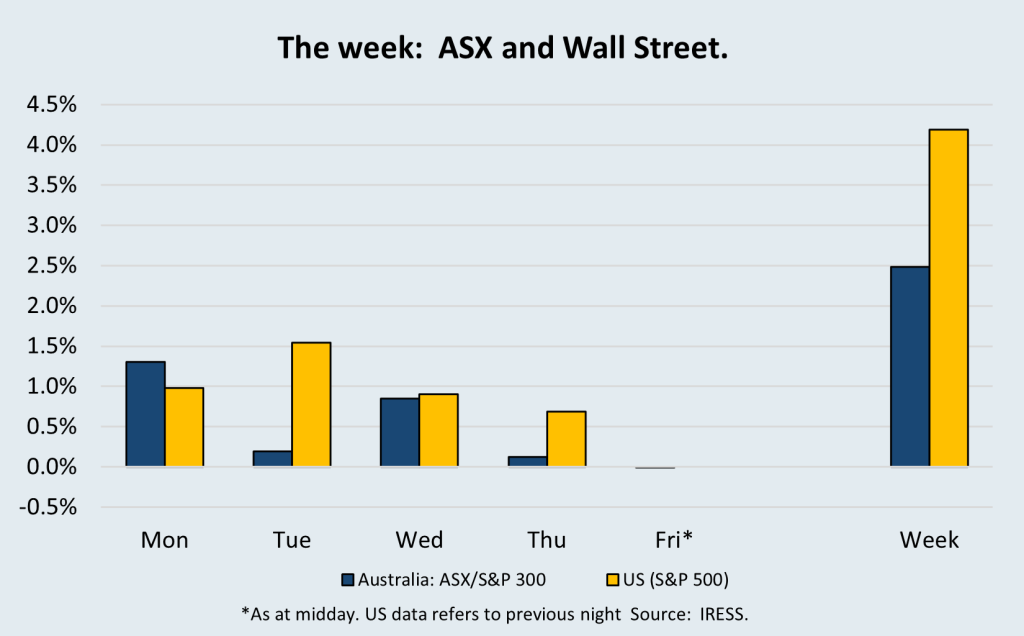

The Market

Catching up with Industrials

Following a week in Perth, the Investment team expanded its research efforts by attending the UBS Industrials Melbourne Corporate Day—an efficient forum that brings together a wide range of companies in a single sitting.

Sessions with BlueScope, Ventia, Worley, Orica, Dyno Nobel, Service Stream and Amcor provided timely operational updates and direct access to senior management, including several CEOs and CFOs. This format remains particularly valuable: it sharpens the signal-to-noise ratio, allowing strategic considerations to emerge more clearly than in the formality of financial reporting.

It also enables us to revisit former holdings such as Ventia, assess opportunities within our current positions, and evaluate new investment candidates with a depth and immediacy that is otherwise hard to replicate.

For clients’ Australian shares sub-portfolios, one standout theme was the scale of the long-term opportunity before Worley. This is based on the global energy transition investment gathers pace and the company continues to drive efficiency through its operating model. We came away from this presentation more confident in the investment, but less confident in the employment prospects for our children in technical areas due to the combination of global outsourcing and AI. Worley appears to be at the cutting edge of both.

In the case of BlueScope, there was extensive detail on the impact of US tariffs and how tariff effects are now playing out in the United States (recall BlueScope’s primary asset is a modern steel mill in Ohio, USA). The news is promising, and the ASX has recently rewarded BlueScope’s share price as steel production profitability (“hot rolled coil (HRC) spreads”) has continued to increase. In fact, the stock outperformed the market by almost 10% last month, even though the market was generally weak.

Even further in the detail, we appreciated the commentary regarding BlueScope Coated Products (BCP). Should they be successful in aggressively pursuing an external customer base, there is valuation upside not currently reflected in the BlueScope share price.

More generally, nearly every company addressed the role of AI — not in the inflated language of data-centre hype, but through the lens of practical application and productivity improvement. While certainty remains elusive, management teams are actively exploring ways to embed AI across operations. That mindset, rather than any single initiative, is what gives us confidence that incremental efficiency gains can accumulate meaningfully over time.

Minerals 260 (ASX: MI6)

In recent months, we have outlined the background of two small WA gold miners in client portfolios—this week, one, Minerals 260, has more than delivered on its promise.

Minerals260 (MI6) announced a substantial upgrade to the Mineral Resource estimate (MRE) for its Bullabulling Gold Project in Western Australia. The resource now stands at 4.5Moz at ~1.0g/t, almost doubling contained ounces and increasing ore tonnes by 124%. This upgrade meaningfully strengthens both the scale and quality of the asset and provides greater clarity around a credible, long-life development pathway.

The increase reflects successful extensional drilling—particularly at Phoenix and Bacchus—as well as optimisation work that reduced the cutoff grade from 0.5g/t to 0.4g/t under a higher A$4,500/oz pit shell assumption. The cutoff change contributed an estimated 800–900 koz to the uplift, with drilling improving geological continuity and expanding the Indicated Resource base. There remain further results due from the 110,000m of drilling scheduled for 2025, and drilling is expected to continue in 2026, depending on results, suggesting continued resource growth remains likely.

From a strategic perspective, the upgrade allows MI6 to materially expand its development case. The company’s base scenario now assumes throughput rising from 5Mtpa to 7Mtpa, increasing forecast production from ~150kozpa to ~210kozpa and extending the initial mine life from eight to 14 years. Importantly, even a 6Mtpa configuration supports the longer mine life, giving management several viable pathways, including staged expansion. Analysts have already responded: one group raised its valuation by 67% to A$1.00/share, while another lifted its price target from $0.45 to $0.55. We are a little more cautious but appreciate the upside potential.

Bullabulling continues to benefit from enviable fundamentals: it is a Tier 1 brownfields asset only 65km from Kalgoorlie, situated on granted mining leases and covered by a Native Title Land Use Agreement. Infrastructure is excellent, with sealed highway access to site, and the project remains technically straightforward, with free-milling ore and conventional CIL processing.

Figure #1: Location of Bullabulling mine

The magnitude of the upgrade versus expectations is also noteworthy. The 4.5Moz result exceeded the market’s prior upside scenarios, with MI6 achieving the uplift at a low discovery cost of $9/oz. The scale is now both larger and more concentrated, improving the project’s potential economics and reducing perceived technical risk. With a sizeable 2025 drilling program underway, the probability of further resource enhancements appears high.

While Bullabulling has been known for more than a century—its early history characterised by small, discontinuous and low-grade workings—the asset was largely dormant for the past decade under Norton Goldfields. MI6’s systematic drill-out program has repositioned Bullabulling as one of the most significant undeveloped gold assets in Australia, with a clear forward path: Project Feasibility Study (PFS) and maiden Reserve in 2026, Final Investment Decision (FID) in 2027, and first gold production in 2028.

For clients, the upgraded resource base substantially improves the project’s option value and narrows uncertainty around scale, mine life, and capital efficiency. It represents a meaningful de-risking event and strengthens the longer-term investment case for MI6.

The market appreciated the announcement with stock rising to record levels in the 40c range this week. As a reminder, we took up a position in the company when it purchased Bullabulling for 12cps and have sold down half of our original stake for 25cps. We look forward to future developments for this small portfolio position.

National Accounts (i.e. GDP data)

Your author enjoyed some esoteric elements of the news cycle surrounding the release of the quarterly ABS National Accounts. In our mind, the data regarded as the most critical snapshot of economic conditions, albeit one that looks back to the September quarter, provided further evidence of an economy losing momentum.

For a highly leveraged economy such as Australia, discussion often gravitates toward the interest-rate and political implications of these numbers. However, for long-term investors, it is the structural signals — slower to move, but ultimately more consequential — that warrant closer attention.

Hence, we weren’t surprised by the tension that continues to grow in commentary that is also trying to balance interest rates’ impacts with structural trends, all within a policy background that is devoid of genuine reform.

Recent Investment Matters have noted the problems of falling GDP per capita and productivity, and the ineffectiveness of the RBA in leading our economy with only one instrument in interest rates when all the power of policy and politics is required. We won’t repeat, but we did note the following AFR commentary.

Chanticleer 4th Dec It took just three hours for the RBA’s big problem to be exposed.

“Bullock admitted as much herself, conceding the RBA is simultaneously pleased with the state of the jobs market, surprised by last month’s hot inflation data and comforted that inflation expectations remain anchored. But the result of these cross-currents means it’s uncertain whether the economy was operating above potential.”

We respond that the “cross-currents” are complex, but rather than pointing to potential wavering of the RBA on the next 0.25% of rate movements, they should be an impetus for more structural responses.

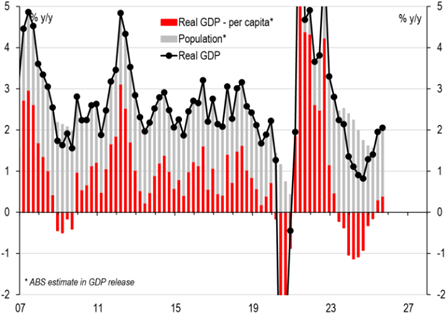

To the numbers, real GDP rose 0.4% in Q3 and 2.1% over the year, while per-capita growth was effectively flat, extending the pattern in which population gains mask underlying softness. It’s a bigger pie, but with same-size slices, which, in a lived experience of capacity constraints and higher inflation, means these numbers note once again that living standards are falling.

In the chart below, look for areas in red below the line (<0) as definitive signs of backward movement.

Figure #2: Bigger pie, same size slices – Real GDP per capita was only flat (~0.0%) q/q; & is still up only 0.4% y/y (after a long ‘recession’)

Source: ABS, UBS

Interest rate impacts

Household consumption remained subdued as higher interest rates continued to suppress discretionary demand, and the composition of growth shifted further toward public demand. But beneath that, there were signs of firmer underlying activity: when volatile components such as inventories and trade are excluded, domestic demand grew 1.2%, the strongest in more than two years.

The domestic-demand result is superficial evidence that the economy is “still too hot” for the Reserve Bank’s comfort, and the persistence of demand, driven by some positive components of investment, but mainly population growth, when combined with our view of sticky inflation, once again reduces the case for near-term rate cuts.

Structural observations critical for investors

As we continue to comment, productivity remains the key constraint on sustainable growth. On this measure, we saw some improvement in GDP per hour worked, which rose 0.8% over the year. But the trend remains weak and inconsistent with an economy that could support real wage growth without inflation risk.

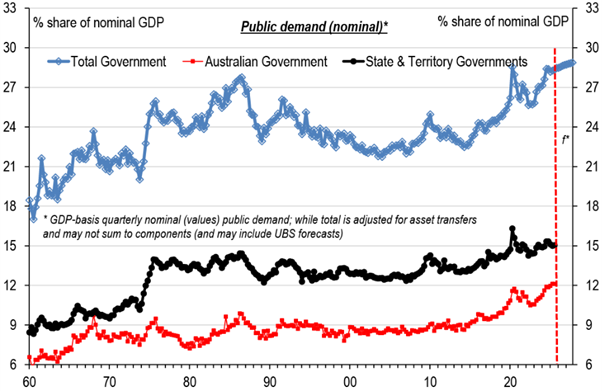

Once again, the distribution of growth — heavily reliant on government spending in recent years — continues to limit the breadth of the recovery. For the past two quarters, the pace of government spending has slowed, and we look to private investment green shoots to continue to emerge.

Figure #3: Government continues to command an increasing share of the economy. Reform required.

Source: ABS, UBS

For investors, it underscores the importance of focusing on companies with genuine productivity levers and pricing power, and companies whose options, future value, and often country of operation are spread beyond our borders.

In summary, the ABS National Accounts supported our view of the economy and its implications for the portfolio remain consistent. As citizens, we are disappointed.

The information in this article is of a general nature and does not take into consideration your personal objectives, financial situation or needs. Before acting on any of this information, you should consider whether it is appropriate for your personal circumstances and seek personal financial advice.