Read the previous week’s Investment Matters.

Photo © AndreyPopov from Via Canva.com

Copyright 2025 First Samuel Limited

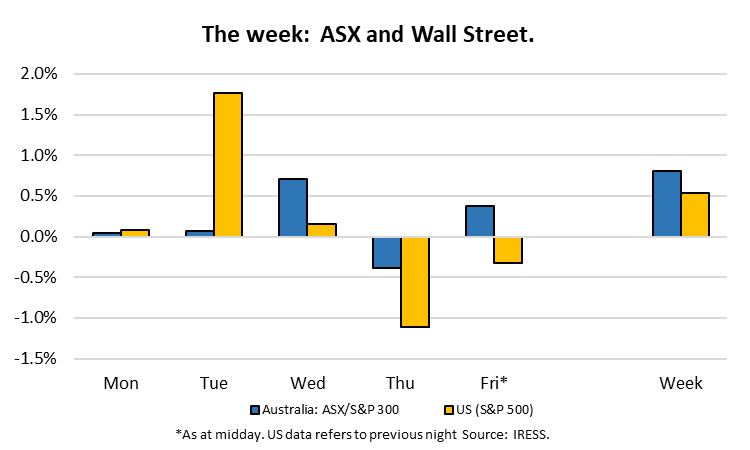

Markets remain more volatile than they were at the beginning of the year, but the volatility is continuing to decrease. Now, it is mainly dependent on the musings of Trump and his inconsistent economic policies. Underneath the noise, however, the rotation between sectors sees the market moving away from expensive momentum stocks and reflects the increased uncertainty of future growth.

We are well-positioned to continue benefiting from our existing positions. Conditions are beginning to provide opportunities amongst stocks that have been heavily sold off.

The Market

Reporting season catch-up and company news

Investment Matters will continue to focus on reporting on a select group of sub-portfolio companies that were not covered in detail in previous weeks. This week, we detail the results for Healius, which also staged a comprehensive Strategy Outlook Day for analysts and investors.

We also provide some background on the Federal budget and its impacts on our stocks and the market overall.

Federal Budget March 2025

We are aware that it is late in the week of the budget, and much time has been wasted reading commentary regarding the macro, micro, and minutiae of the pre-election pantomime that is the early Budget Process.

Let’s focus on some stock-specific, long-term economic and overall ASX market impacts.

In a nutshell, the Budget changed little, with negative underlying cash balances extending to throughout the budget forecasts. The growth elements of our economy rely on government borrowings. Figure 1 shows ongoing cash deficits.

Figure 1: Underlying cash balance showed a net improvement

Source: Federal Budget papers, Barrenjoey Research

Yet the headlines were tax cuts. How?

No surprise. According to Barrenjoey Research, in an election year, the government has handed back the ‘parameter dividend’ (positive changes to assumptions) to Australians, providing 96% of the windfall in cost-of-living relief and tax cuts across the forward estimates.

The opposition suggested only minor differences in their follow-up. Most of the Budget documents outlining the operation of 25% of the Australian economy are barely changed since last year, nor would they be different under either team’s ticket.

Chris Richardson, formerly of Access Economics and one of the better-known economists, opined on the lack of differences recently in the AFR. The lack of differentiation is crucial for ASX market participants, as the market is accustomed to and expects no change. As Richardson noted:

“Yet, with big-ticket items such as nuclear power plants and extra fighter jets sitting mostly some years away, the difference between government and opposition policies in this election will be comfortably less than 1% of the amounts we’re set to tax and to spend in the next four years.”

“And yes, that’s typical. For decades now our oppositions have promised their taxing and spending to be more than 99% matching those of the government they’re campaigning to replace.”

“In the election campaign both sides are therefore promising Australians that they’ll remain mediocre.”

Chris Richardson – AFR 16th March “We wasted a $400b windfall, and now we’ll all have to pay”

No change leads to no changes, but the tax cuts are politically savvy, and the headlines look good. Nonetheless, they are tiny and ineffectual if you aim to improve the economy and lives of future generations.

The government is reducing the lowest tax rate from 16% to 15% on 1 July 2026 and to 14% in July 2027. It will boost households’ pre-tax income by 0.14% in FY27 and 0.3% in FY28. But as all readers will be aware, the change simply reduces bracket creep. Limiting bracket creep is a notable aim, and modelling suggests success for average income earners, who will not exceed FY24 levels of tax rate until FY32.

With the economy operating near full employment, experiencing moderate inflation, and at high levels of gearing, the tax cuts will have little impact.

To provide an impulse for the economy, generate additional investment, improve the outcomes for future-oriented parts of the economy, or help middle-class households, we need tax reform, not tax tweaking.

Reform is vital because higher rates and increasing tax take from middle-income younger households are now too high. The Figure below shows the impact of rates and taxes on Household Income.

Figure 2: Policy (Government and RBA) settings remain a constraint on household spending

The chart above can appear complicated, but I ask that you take the time to understand it.

The Green line represents the tax take from the economy (as a percentage of GDP), the Orange line represents the money spent on mortgage interest, and the Black line represents the total of both.

One is driven by government policy changes, the other by the RBA. Trends can be difficult to spot, but for an aficionado of financial history and markets, some of the trends include the following:

1. Home interest payable

The level of dwelling interest payable (Orange line – note it doesn’t include the principal payments) is now much higher than any experienced readers have of high rates in the early 1990s.

2. Interest rate reductions wasted

The entire benefit to households from the reduction in interest rates since the GFC has been wasted through additional debt and higher house prices. Great for people who bought in the 1990s. A disaster for future generations. We have no more houses per person than before (in fact, we have fewer), we don’t have better houses (all the increase is in the value of land), and young people have not only the highest household indebtedness levels, higher levels of student debt but in combination also the highest burden from both interest and income tax than any generation previous.

3. China boom benefits spent

All the entire benefits from the China mineral boom from 2004 to today have been spent. The reduction in taxes (Green line) through the Costello/Swan years is gone. Leaving the nation with the same tax take needed for a 2000’s government. We did not sustainably benefit from high Terms of Trade. The mining boom is spent.

4. Costs of higher interest rates

But the costs of the lingering monetary policy (changing rates) are now so influential on the downside that higher RBA rates on mortgages can simultaneously:

- cripple households in their wealth creation, childbearing and business building time of life.

- as well as increase their cost of living through the inflation stimulated by spending made by the share of households that already have wealth and liquid savings (outside of super or mortgage offset accounts).

5. But we use the same structures

Despite this context, we are now using the same tax structures (GST, income, superannuation) that generated the wealth and income balances. Instead of balancing funding requirements towards households that have benefited from previous settings, we are sticking with the same system, which is appropriate only for an economy from two decades ago.

Direct implications for stocks

There were very few implications for portfolio stocks, apart from Healius and Origin Energy. Both measures, the expansion of support for GP bulk billing and the extension of energy concessions, were pre-announced.

For Origin, collecting outstanding energy bills is a core part of its business, and bad debts, disconnections, and complicated procedures regarding both are a significant part of the operational landscape for Australian energy retailers. Direct government support significantly enhances these processes.

For Healius, we view additional support for GPs, both in the form of Medicare funding, bulk billing, and ongoing, more substantive reform, as being vital. When implemented effectively, increased use of pathology improves health outcomes and reduces long-term health burdens. In the short-term, higher support for GPs reduces operational pressures within their businesses, which can artificially raise the cost of Healius pathology lab lease costs within GP facilities.

The chart below shows the reduction in bulk billing rates in Australia since 2019, a period (excluding COVID-19 peak) that has also coincided with lower total visits to GPs.

Figure 3: Australia: GP Bulk Billing rate, by volume (%)

In the long run, Healius and pathology rents cannot be used to subsidise the cost of primary care as such Budget steps are incrementally positive.

Broader implications for the market

There were small implications for household budgets, as discussed. The more significant long-term concerns persist regarding the weak outlook for structural reform. We have a productivity problem and a growth model that is predicated upon population growth and housing, not innovation and investment.

This may prove sufficient to sustain declining real incomes and unfavourable intergenerational outcomes. Still, if a government seeks better outcomes, it will need one that addresses the structural budget imbalance shown in the figure below.

Figure 4: Structural budget imbalance

The critical role that Government and deficits play in the economy is now clear. Without government investment, our weak investment outcomes would be even worse. Without direct government support, our households would suffer from even more significant real per capita declines in disposable income.

We could sustain such structural imbalances if we were transforming our economy towards new growth drivers and promoting higher levels of investment.

However, experiencing a higher level of reliance without a reform agenda is problematic for long-term wealth creation and the expected returns of Australian companies. It drives further investment in

– pre-existing duopolies;

– those businesses that are dependent on government support or investment; and

– towards companies that are expanding overseas.

Summary

1. The outlook for portfolios that exploit these trends, such as those constructed for our clients, is favourable;

2. However, the outlook for the broader economy that generated the savings for this investment is less optimistic.

Helius (HLS) – FY24 Result and 2th March Investor Day

Helius reported its 1H25 results on 20 February. The stock price has been turbulent both before and after the announcement of the result. Following the Investor Day held this week, the stock has experienced a positive net movement, up more than 6 percent since the result in a significantly weaker market.

However, following the initial 1HFY25 result announcement, the stock fell by more than 10 percent, as the market appreciated the improving conditions but was disappointed by the lack of detail regarding Pathology’s core operations.

As a reminder, Healius sold its Lumus imaging business (announced September 2024 and due for completion in May), plans to repay its debt, and reposition the remaining pathology business for growth.

Our investment thesis

We have identified four features of Healius that we appreciate, and we felt were not adequately reflected in the share price.

- Fantastic structural growth trends in the adoption and use of pathology tests.

- Balance sheet flexibility. The Lumus sale proceeds will free Helius from the constraints its high gearing created. Improvements in value creation can be expected with more flexibility.

- An improving outlook for the funding of pathology tests by the government. After more than a decade of reform, we recognise that much of the savings targeted by the government have now been delivered, providing an opportunity to restructure funding from now on.

- Significant capacity for self-help in the pathology operations, especially around operational improvements and the high levels of occupancy costs. In addition, we anticipate that self-help will extend to customer care, digital integration and brand development.

1H25 Results

The results showed some signs of growth in volume and commitment to improved cost control. Nonetheless, the underlying EBIT margin generated from pathology is weak compared to the levels achieved before COVID-19. The figure below shows the revenue and EBIT margin since 2018. We have included the Jefferies Research chart, which also includes their forecast for 2025 and 2026.

We observe that Jefferies is forecasting limited increases in margins; this aligns with the market, but we believe it isn’t overly optimistic, given the outlook for Healius’ self-help initiatives and changing conditions. This outlook is part of the reason why the stock is so cheap in our view.

Figure 5: Historical revenue and EBIT margin – Healius Pathology

Source: 1H25 Company reports and Jefferies Research

The 1HFY25 result demonstrated that pathology volume growth in 2HFY25E will be critical for margin improvement.

A clear roadmap (shown below) for improvement in the Pathology business complemented discussions of green shoots in the 1HFY25 results. However, management left out many financial details, including forecasts for profitability. We expected the missing information would be provided in the Investor Day.

Figure 6: Healius Pathology roadmap appeared sensible

Source: 1H25 Company reports

Investor Day

Held on March 27th, the Investor Day generated significant interest and a considerable rebound in the share price.

High levels of news flow have surrounded the stock over the past two years, including corporate activity, the sale of a significant portion of the business, and ongoing changes in the underlying Australian pathology market since the COVID-19 pandemic.

Healius management correctly determined that a detailed update to market participants was required. The market needed additional information regarding.

- The outlook for capital management and dividends following the sale of Lumus

- Information regarding the future balance sheet of the company

- More detailed background into the growth drivers available to the pathology business post the sale of the imaging business

- Updates on technology, innovation, market trends and the outlook for regulatory changes

- Forecasts regarding the levels of cost control we can expect from the smaller business and ways in which the management team was looking at medium-term margins following significant volatility in margins ever since 2018.

We felt the company delivered in spades across the board.

The highlights include targeting a Pathology EBIT margin in the “high single digits” by June 2027. We believe that such a goal is achievable, and the team provided sufficient detail on how it can be achieved, making it credible and well-received. The previous chart from Jefferies’ research expected a much lower EBIT margin.

In addition, the investor day provided the market with much-needed access to a range of senior management that can offer insight into the workings of the various aspects of the business. Healius, in its smaller guise as ex-Lumus, still employs over 9,000 staff across a myriad of locations and provides a range of services that extend from clinical trials to veterinary pathology, everyday blood work for millions of Australians, and critical response high-tech analysis at the core of hospital operations.

The investor day also provides an update on procedure volumes, with revenue up 6.2% year-to-date as of February 2025.

Highlights from the innovation and technology front included

- Robotic automation for Microbiology

- Emerging diagnostics technology

- Improvements in processes which provided multi-stage testing (high risk / low risk technology assisted triage) for straightforward procedure, change which reduce time and cost.

We were also impressed by the focus on the customer experience side of the business. We believe that, ultimately, pathology will be incorporated into a broader range of retail offerings. Preparing the company for high standards in customer experience, branding, and network optimisation is critical in unlocking such value. Management presentations included those with career experience in other health-related retailers, including OPSM.

We also appreciated the focus during the Investor Day on the cost base. The figure below shows the breakdown of costs that the Healius Pathology business faces. Despite the extreme complexity in the science and the complicated nature of the supply chain and workflow within Healius, it remains a simple business of people and property.

Improvements in staff efficiency (labour cost) and ongoing reduction in property costs (rents) are critical to expanding margins.

Figure 7: A simple complex business

Investment implications

With the sale of Lumus expected to be completed in May, the company intends to pay a special dividend of approximately A$300 million (subject to the completion of the Lumus sale), equivalent to 41.3 cents per share fully franked, with a franking credit of 17.7 cents per share, or approximately $128 million. This is a great outcome.

The embedded dividend is essential from a client portfolio. The expected $0.41 in dividends, once paid, will reduce the size of the overall position; effectively, one-third of our position is now valuable franked income.

Although Healius now holds a top 10 position in clients’ Australian shares sub-portfolios, there remains a considerable amount of work to be done for the company to achieve all of its aims. The possibility of increasing the position size back to a similar level after the payment of the dividend will be contingent upon Healius’ progress in the coming 12 months.

As noted in the previous section, a significantly broader range of self-help options is possible over the next 3-5 years. The value of any improvements will be realised in a faster time frame if coupled with corporate activity. We see several possible mergers and a range of companies that would be well placed to acquire Healius.

The combination of 1HFY25 results, the Investor Day and the upcoming dividend provides further confidence in our position in the stock.

The information in this article is of a general nature and does not take into consideration your personal objectives, financial situation or needs. Before acting on any of this information, you should consider whether it is appropriate for your personal circumstances and seek personal financial advice.