Copyright 2026 First Samuel Limited

Read the previous Investment Matters here.

In this week’s Investment Matters, we highlight ongoing market hits, short-term earnings risks from energy disruptions, risks to global growth and trade, and the RBA’s decision to lift interest rates as it continues to fight inflation amid uncertainty surrounding current economic decisions.

This week’s in-depth discussions of last month’s reporting season will focus on another three of the larger portfolio positions:

- Block (XYZ);

- Inghams; and

- Paragon Care

In the following weeks, we will finish off the remaining positions, including Nanosonics, Worley and James Hardies.

The Market

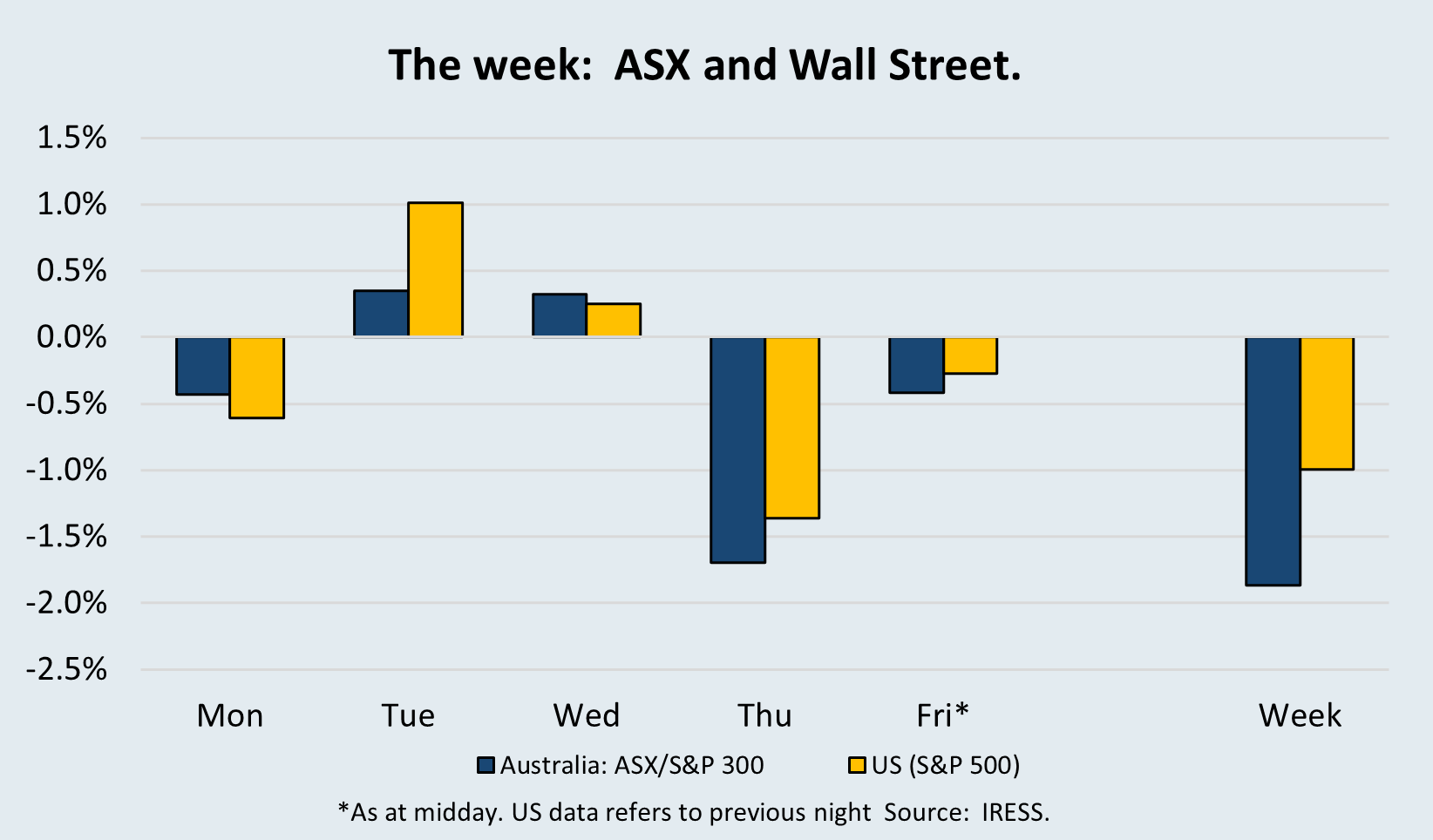

War, energy and second-round effects

This week’s market weakness was again a reminder that in geopolitical crises, the first-round shock is often less important than the chain of effects that follows. As the conflict has moved further up the escalation curve, markets have begun to price not simply war, but disruption to energy, freight and physical production. That is a much more serious problem for equities. Gold’s sell-off was part of that story. As in earlier periods of stress, it worked well while risk was building, but once risk materialised, it became a source of liquidity rather than protection. We have substantially reduced our gold exposure in recent months, but still believe it retains an important role in a balanced portfolio.

The most important development

For Australia, the most important development has been the shift from military conflict to direct pressure on energy infrastructure. The bombing of Iranian oil fields and the retaliatory strikes on Persian Gulf gas assets matter because medium-term energy disruption rarely stays confined to oil and gas. It feeds through to transport costs, industrial activity, processing margins and ultimately commodity demand. That dynamic is already appearing in metals. Zinc, relevant to Aurelia Metals, and copper, relevant to Sandfire, are each now around 8% below their levels at the start of the war. That may prove to be an early indication that the market is beginning to discount weaker industrial activity, not just geopolitical risk.

In a week when stocks fell between 1% and 2%, the best performers were our oil exposures; the worst were our metal exposures, including IGO and Aurelia Metals. Reliance Worldwide (RWC), a core holding exposed to global housing dynamics, announced a share buyback and saw its share price rise 8% for the week. A conservative company by nature, it became obvious to the RWC board that the 25% fall since the result, including 12% since the war began, was excessive.

Paths to resolution

There are paths to resolution of the conflict, and we still believe these are more likely, and more boring, than the wildly destructive scenarios the Reader and we can imagine. As such, we remain committed to real-world assets, production and supply chains. We own supermarkets, steel mills, and mines that produce more than two dozen minerals; a pathology business; a radiology business; building products; cutting-edge financial services; and insurance companies.

While the short-term impact on prices and output can be painful for short-term earnings, we continue to think the longer-run implications of heightened geopolitical conflict are supportive for Australian-sourced mineral supply chains. While domestic pressures on cash flows mean we are avoiding expensive consumer discretionary and banking names, we believe the capacity for growth in per capita income in Australia remains.

For now, however, higher portfolio cash levels (in excess of 15%) remain appropriate.

The RBA, inflation and Australia’s lack of preparation

Set against this backdrop, the Reserve Bank’s decision this week to lift the cash rate by 25 basis points to 4.10% was a reminder that Australia’s inflation problem had already become more difficult even before the latest energy shock. The Board said inflation had “picked up materially” in the second half of 2025, that recent data pointed to greater capacity pressures than previously assumed, and that the risks to inflation had become more concerning.

RBA Governor Michele Bullock was direct in the press conference. She said the economy had been growing faster than potential, the labour market had “tightened a little recently”, and underlying inflation “remains high.” She also made the important point that while higher petrol prices were relevant, they were “not the reason for today’s decision”; rather, they were an additional complication on top of an inflation pulse the Bank already considered too strong.

The RBA is not reacting only to war. It is reacting to a domestic economy where inflation has proved broader and more persistent than expected.

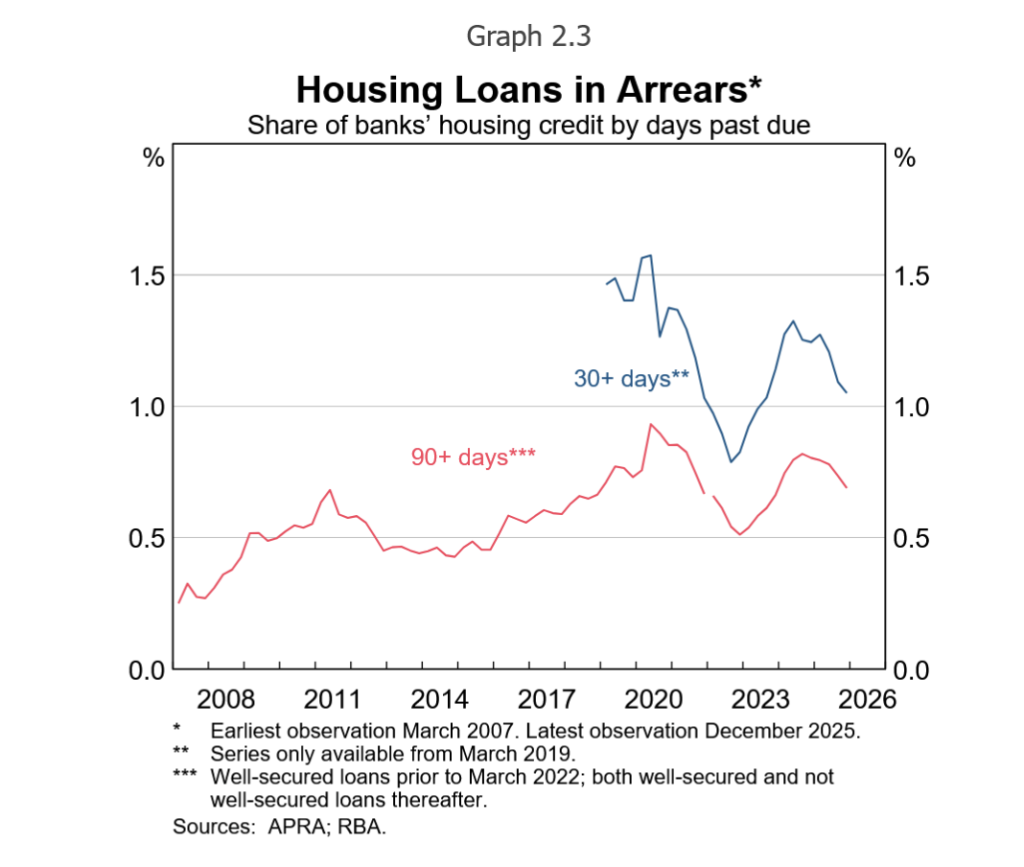

In the RBA Financial Stability Review released on Wednesday, following the Tuesday rate’s decision, the bank was comfortable with the capacity, in aggregate, for the household sector to carry the burden of higher rates. Falling levels of loans in arrears, a smaller number of households experiencing negative cash flows, and the ease with which households can simply sell up and avoid an equity loss are cited as reasons households can bear the pain.

Figure #1:Housing Loands in Arrears

Our concern is that aggregate data should never be used when assessing debt capacity in an economy. Why, because it understates the correlation between risk factors, should asset prices begin to fall, or economic confidence diminish?

Just imagine the change in cash flow for the heavily geared middle-income family with a diesel Ford Ranger this week. Or the even more important sub-category that owns an investment property/holiday house. The creditworthiness of the wealthy, or high-cash-flow, or low-loan-to-value borrower is never the relevant benchmark. Did these households need to pay more for their mortgage this week? Perhaps not.

But the RBA only has one tool, interest rates. If we need to lower aggregate demand, and we don’t agree that we do, surely all households need to bear a similar cost, and that task falls to the government through reform of spending and taxes.

The RBA’s balancing act is made harder by a weak government track record in productivity and reform. As is so often the case in life, the failure to prepare in good times is exposed when conditions deteriorate. Exogenous inflationary pressure from energy and geopolitics is arriving on top of an economy where public demand has remained strong, infrastructure programs are still absorbing labour and materials, and capacity constraints are already more binding than the Bank had assumed.

The deeper frustration is that Australia has had years to do more serious preparation. Rather than using a period of relatively favourable conditions to reform the tax base, improve regulatory efficiency and lift productivity, the country has drifted. Now the shocks have arrived first.

That leaves the Reserve Bank with less room to move than it would ideally like. If inflation is being reinforced by external energy disruptions and domestic demand pressures simultaneously, policy becomes more awkward.

Thankfully, Australia’s monetary framework still contains a circuit breaker. The dual mandate matters. The RBA is required to pursue both price stability and full employment, not inflation control in isolation. The fact that the vote was close, 5:4 in favour of raising rates, is healthy and was my favourite news story of the week, no rise at all would have been better.

The complexity of the issues and the quality of debate mean that if economic conditions weaken materially, even in a stagflationary environment, the deterioration in labour market conditions, credit and household balance sheets will eventually matter for policy. Until then, caution, cash flow and exposure to real-world assets remain sensible anchors for portfolios.

Block (XYZ): Jack Dorsey challenges the world

Block’s latest financial update landed as two stories at once: a very strong operating result, and a now-famous Jack Dorsey letter explaining why the company could remove more than 4,000 roles, 40% of its staff, even as the business was performing well.

The central tension is exactly why the update attracted so much attention. This was not a conventional “results miss followed by cost-cutting” situation. Dorsey explicitly argued the opposite: Block’s business was strong, gross profit was growing, and profitability was improving, but the company believed advances in “intelligence tools” had permanently changed what it means to build and run the business.

His core message was blunt: a much smaller team, using the tools Block (XYZ) is building internally, can do more and do it better.

That logic is what made the letter so striking. Dorsey’s argument was not really that Block had to sack people to survive, but that the organisational design of the old Block no longer made sense. He framed the layoffs as a proactive, one-step reset rather than a reactive, drawn-out series of cuts. In his view, AI and internal productivity tools reduce the need for layers, duplicated functions and oversized teams, especially in a software-heavy organisation. Investors clearly found that logic credible, or at least compelling enough in the near term: Block said headcount would fall from around 10,000 to a little over 6,000, and the market responded very positively to the announcement.

Block (XYZ) share price soared 28%, reflecting optimism that the company could materially lift margins and free cash flow if that leaner model holds. The company is the literal embodiment of the transformative opportunity AI in the workplace may create. Of course, should the development underdeliver, Dorsey will have stunted the company’s options at a time when its operating rhythm was already fantastic.

Strong underlying result from Block (XYZ)

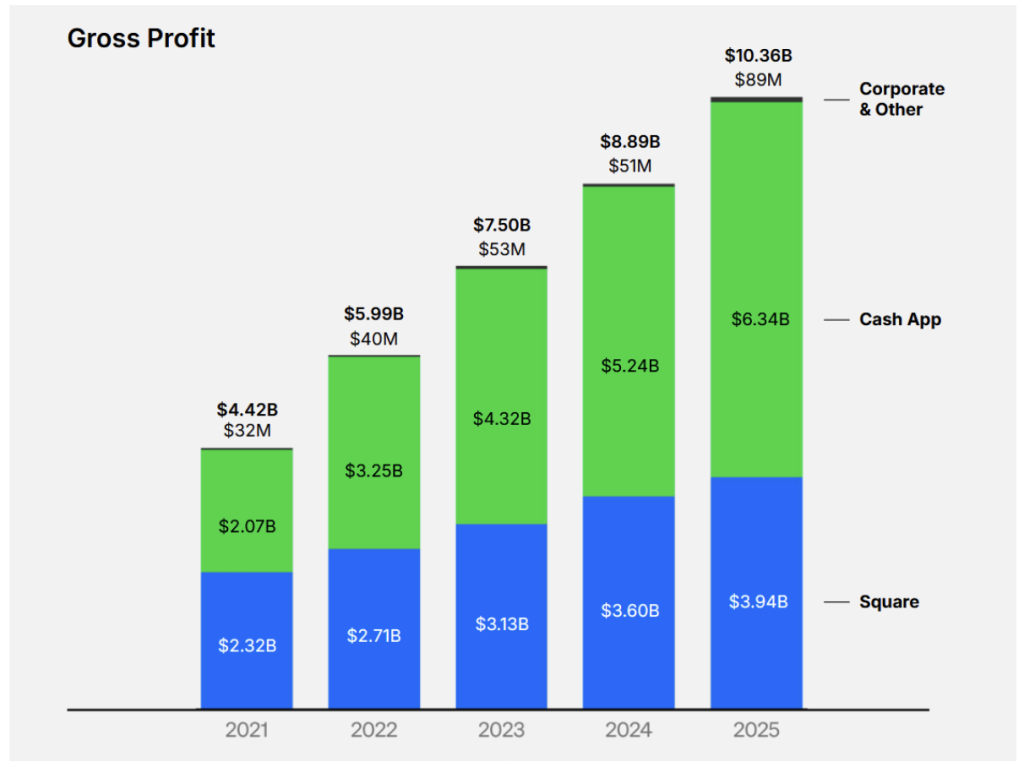

The underlying financial result was genuinely strong. In the fourth quarter of 2025, Block (XYZ) generated gross profit of $2.87 billion, up 24% year over year, while adjusted operating income rose 46% to $588 million. Adjusted EBITDA reached $930 million and adjusted diluted EPS increased 38% to $0.65. For the full year, gross profit reached $10.36 billion, up 17%.

Block raised its outlook: it now expects 2026 gross profit of $12.20 billion, implying 18% growth, and adjusted operating income of $3.20 billion, or a 26% margin. For the first quarter of 2026, it guided to gross profit of $2.80 billion, up 22% year over year, with adjusted operating income of $600 million. That upgrade was important because it showed the company was not simply cutting costs to defend a weak outlook; it was cutting while simultaneously lifting its growth and profitability expectations.

Figure #2: Consistent growth in Block (XYZ) from key business segments

Source: Block XYZ Q4 Investor Presentation

The gross margin and gross profit outlook were at the heart of the positive read-through. Block’s overall gross profit growth accelerated from 9% in the first quarter of 2025 to 24% in the fourth quarter, which management presented as evidence that product velocity and go-to-market investment were finally translating into stronger monetisation.

The company’s 2026 gross profit guidance of $12.20 billion exceeded its prior Investor Day framework, and management described sustained gross profit growth as the clearest path to long-term value creation. Operating leverage in the business model is clearer with gross profit growing 18%, leading to adjusted operating income growth of 54% – a very powerful incremental margin conversion.

We have not included the full financial value of the workplace reduction in our valuation. Should Dorsey succeed with a smaller scale workforce, the upside to our valuation is likely 20%+ and well in excess of AUD100 per share.

CashApp

Block’s CashApp product has evolved from a simple money-transfer tool into a comprehensive digital wallet. Cash App could feel “trite” or redundant to Investment Matters readers because the Australian financial ecosystem already offers core features, including instant peer-to-peer (P2P) transfers and free, simple aliases, directly within almost every standard banking app. But in the US, where cheques are still used, there is no single, centralised real-time payment system across its thousands of banks.

CashApp allows direct transfers, provides a Cash Card (Visa debit card), supports direct deposits for paychecks and tax refunds, and allows users to buy and sell fractional shares of stocks and Bitcoin. Similar dedicated savings feature, where users can set goals and earn interest.

Figure #3: Blocks CashApp features

Source: Block XYZ Q4 Investor Presentation

Cash App’s financial performance was another major reason the update was well-received. Cash App gross profit grew 33% year over year to $1.83 billion in the quarter, well ahead of the broader group. Monthly transacting actives rose to 59 million, while primary banking actives increased 22% year over year to 9.3 million. This matters because the market has long wanted evidence that Cash App could deepen engagement rather than simply add low-value users. The latest update suggested that is happening.

Block highlighted strength across Cash App Borrow, BNPL products and Cash App Card. Financial Solutions’ gross profit per active grew 57% year over year, driven by Borrow, while inflows per transacting active accelerated to 12%, helped by more customers directing their employment income into Cash App. That is a much higher-quality growth than simple user acquisition, because it points to deeper wallet share, better monetisation, and more durable customer relationships.

The other interesting element was that management tied Cash App’s improvement to a clearer strategic focus. The company said it is continuing to invest in Cash App Green as a cornerstone of its engagement strategy, aimed at “modern earners” such as hourly workers and independent earners. In terms of portfolio diversification XYZ provides upside to a range of trends in AI, employment casualisation and social dislocation, without necessarily making such trends worse for the disenfranchised.

Broader social and employment implications

There are two obvious debates running underneath the enthusiasm. Dorsey’s argument is coherent, but surely it remains an aggressive stance. Stating that you can cut roughly 40% of staff because AI tools now allow smaller teams to do better work is one thing; proving it is another.

Scepticism about Block’s capacity to absorb the loss of so many of these roles is well placed. But what does it say about the level of layoffs that are possible in all businesses? What does it say about the degree of aggressiveness all CEOs should take?

Block can sustain product speed, customer service, and gross profit momentum with a much smaller workforce. So far it has broken the mould by sacking when successful. That combination is why the letter became famous: it was not just about layoffs, but about a company claiming that AI can support a structurally more profitable model right now, not years from now.

ParagonCare: Strong operations soured by bad debt and balance sheet uncertainty

ParagonCare’s 1H26 result was easy for the market to dismiss because the statutory numbers looked ugly, but that would miss the more interesting point. Beneath the noise, the core business actually delivered a respectable half, with revenue up 2.9% to $1.90 billion and underlying EBITDA up 3.1% to $49.0 million. Underlying NPAT was $13.3 million, up modestly on the prior corresponding period, while the company reaffirmed FY26 guidance for revenue of $3.6–3.7 billion and underlying EBITDA of $97–107 million.

The statutory loss, by contrast, was driven overwhelmingly by a bad debt created 18 months ago as part of the Infinity issue rather than a collapse in day-to-day trading.

Figure #4: 1H26 Financial summary

Source: Company presentation

The Infinity exposure is genuinely regrettable but is part of the risks of a wholesaling business, and, whilst previously discussed in Investment Matters, it is the unavoidable place to start. Paragon had previously disclosed balances due from the Infinity Retail Pharmacy Group, and by 31 December 2025, the gross amount owing was still approximately $48.5 million, comprising $32.8 million in trade receivables and $15.7 million in non-trade loans and receivables. Infinity’s finance and larger operational and governance issues with the Wesfarmers Group (which operates the banner group/franchise retail) have come to a head, forcing the Paragon receivable into default. After receivers and administrators were appointed to a significant number of Infinity entities, Paragon reassessed recoverability and took a 100% lifetime expected credit loss allowance, resulting in a $47.3 million expense for the half.

Paragon had stopped supplying Infinity in March 2025, and management has continued to work with administrators as a major creditor. Writing it all off is the correct accounting decision, but it does not preclude future recoveries, which remain an upside scenario over the next 18 months.

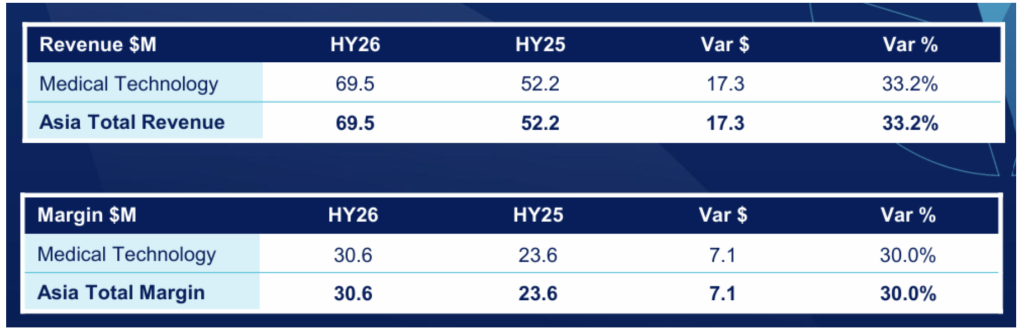

Aside from Infinity, the result is more encouraging because several operating divisions are still performing well. Asia was a clear highlight. Revenue in the Asian business rose 33.2% to $69.5 million, while margin increased 30% to $30.6 million, leaving the segment with a very healthy44.4% margin. Management said this was driven by the Aesthetics business, helped by new product sales and increased marketing investment, with organic revenue growth of $16.2 million, or 31%. That is a strong result by any standard, and it supports the broader argument that Paragon is building something more valuable than a low-growth domestic wholesaler.

Balance sheet

On the balance sheet, net debt finished the half at $287.5m (excl. AASB 16), reflecting recent acquisitions and peak seasonal working capital. Working capital is expected to trend down over coming months, with net debt guided to be circa 2x Underlying EBITDA by June 2026 (before any further acquisitions).

Ongoing acquisitions were another notable positive. Paragon acquired AHP Dental & Medical and Somnotec during the half, and continues to frame M&A as central to its ambition to become the leading healthcare distributor across ANZ and Asia. We have been so far impressed by the acquisitions the company has made, the relatively well-priced earnings they have required and the early performance of these businesses.

Figure #5: Asia Segment Growth

Source: 1H26 Company presentation

The company said acquisitions in ANZ and Asia are broadening its product reach and capabilities, and its footprint now extends across nine Asian countries. The balance sheet is more stretched in the short term, with net debt rising to $287.5 million from $216.4 million at June 2025, but management still expects pro forma net debt to underlying EBITDA of around 2.0x before any further acquisitions, suggesting leverage should improve as earnings annualise and the Infinity issue washes through.

There were also some quieter but important signs of quality in the result. Contract Logistics revenue grew 47.1% to $235.5 million, with margin up 65.0% to $11.1 million, while management cited improved cash flow from operations driven by a focus on working capital management. Net cash from operating activities remained negative at $26.7 million, materially better than the prior period’s negative $40.7 million, but was weighed down by seasonal working capital and acquisition effects. This fits with the broader impression that management is focused on growth, but not growth at any price.

That is why our meeting with CEO Carmen Riley and new CFO Brendon Pentland matters. The result itself showed a business still growing underlying earnings despite a major credit event, but the more important takeaway is that management appears committed to growth, cash-generative activities and improved market transparency.

Given Paragon’s share price has been dreadful over the past year, down roughly 55%, investors clearly want proof rather than promises. Still, stripping out Infinity, 1H26 suggested the core platform is intact, the Asian business is working, acquisitions remain additive, and the business may now be entering a cleaner, more transparent phase.

The level of debt in Paragon Care appears high to the casual observer, given that the stock has had a market cap between $275 m and $400m over the past year. However, the debt is predominantly a working capital facility backed by short-term invoicing to large clients. The company, in theory, could use alternative sources of funding, but throughout its history as a private company, Clifford Hallam (which merged with Paragon Care in 2024) has pursued growth funded by this large working capital facility. We believe that in time the market will become more comfortable with the way in which this facility is used.

Summary

At this stage, however, some reticence remains. The market, and especially the analyst community, is sceptical of the company’s ability to reduce its net debt to 2.0x EBITDA by year-end. Discussions with management outlined a credible path to their year-end goals. We were aware of numerous idiosyncratic issues with the Paragon model that accentuate the variability in these debt levels. In time, we expect the market will build a higher level of understanding of these issues and reduce the current equity discount being applied to the company.

Inghams 1H26: Disappointing result

Inghams’ 1H26 result was weak on the key operating profit line. Underlying EBITDA fell 35% to $80.6 million, from $124 million in 1H25, with group margin compressing to 5.0% from 7.7%. Revenue was broadly flat, so the issue was not top-line collapse so much as a sharp deterioration in operating efficiency and cost absorption. Australia was the main problem, while New Zealand was relatively resilient. The stock sold off 17% for the month, and we reduced our position size at higher levels.

Since the February result, the impact of the Iran War on Inghams has been significant, with the stock losing another 10%. Rising food and energy prices place additional pressure on Inghams in the short-term, and whilst the medium-term prospect of full cost recovery is high, the ASX has been harsh on companies with short-term earnings concerns, even if transient.

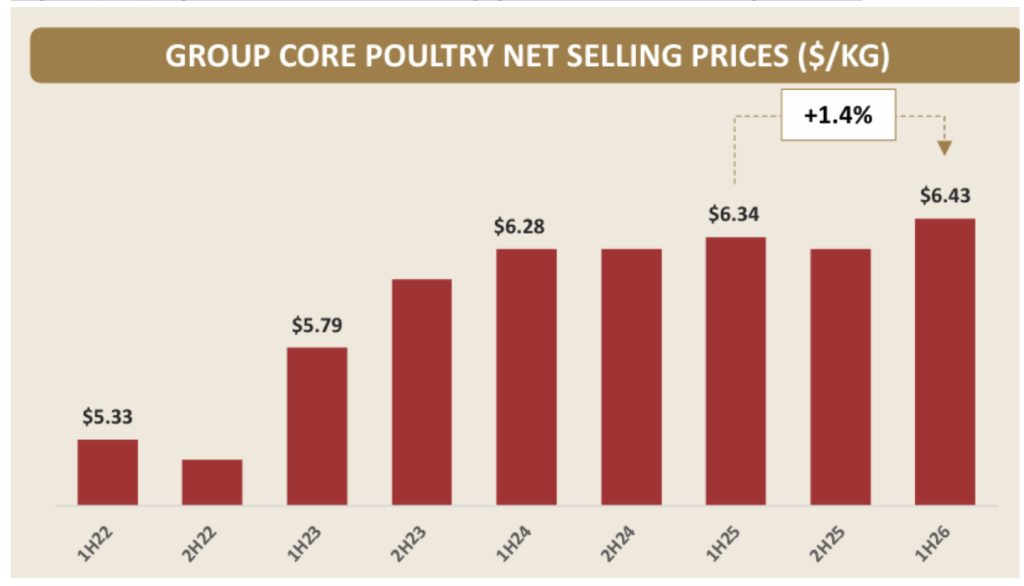

Thankfully, our disappointment on the earnings date was somewhat assuaged by our meeting with CEO Edward Alexander and CFO Gary Mallett. The drivers of cost increases are readily understood and likely to be transient, and the underlying industry conditions, including pricing, were improving leading into the war. The figure below shows the improvement in pricing following the fall we saw in 1H25, which relates to the variation in the Woolworths contract. Leading into 2H26, we expected this rebound and were pleased to see it materialise.

Figure #6: Inghams is still achieving growth in net selling prices

Source: FY25 Results Presentation

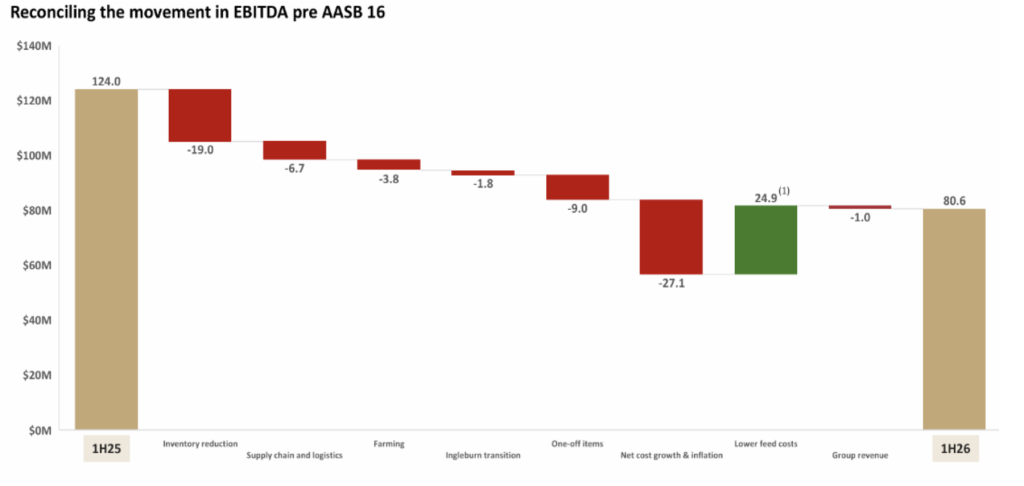

On cost control, investors were disappointed that lower feed costs were nowhere near enough to offset the other cost pressures. Inghams’ EBITDA bridge shows a $24.9 million benefit from lower feed costs, but this was overwhelmed by $19.0 million from inventory reduction actions, $6.7 million of incremental supply chain and logistics costs, $3.8 million from weaker farming performance, $1.8 million from Ingleburn transition inefficiencies, and $9.0 million of net cost growth and inflation.

In other words, lower grain and soy input prices helped, but the benefit was effectively “spent” on fixing operational issues, servicing customers, and absorbing inflation elsewhere in the system.

That explains why profit growth was so limited despite easing feed markets. Costs were elevated due to supply chain changes (Woolworths control changes), the onboarding of new customers and products, higher cost-to-serve, and measures to reduce excess inventory. Total costs rose 5.0% year on year, or $69.7 million, with inflation across labour, ingredients, cooking oil, utilities and packaging also playing a role.

The market’s concern now is the second half. Inghams cut FY26 underlying EBITDA guidance to $180–200 million from $215–230 million, as the timing of operational improvements is taking longer to materialise. Elements needed for success include supply chain and logistics performance, farming productivity, and the completion of the Ingleburn transition. With management effectively pushing more of the recovery into 4Q26, there is huge execution risk: investors are being asked to rely on a strong second-half uplift after a disappointing first half. With leverage at 2.4x and investor trust already strained by earnings volatility, the market is likely to remain cautious until unit costs improve more clearly and consistently.

Figure #7 Negative contributors a once-off? Key Drivers of 1H26 Earnings

Source: FY25 Results Presentation

Summary

Inghams have now cleared excess inventory, product pricing has been improving, and one-off costs could actually be “one-off”. Better execution in this scenario should remove some of the discount currently priced into Inghams shares.

The information in this article is of a general nature and does not take into consideration your personal objectives, financial situation or needs. Before acting on any of this information, you should consider whether it is appropriate for your personal circumstances and seek personal financial advice.