Copyright 2025 First Samuel Limited

Read last week’s Investment Matters.

The Market

Markets recovering

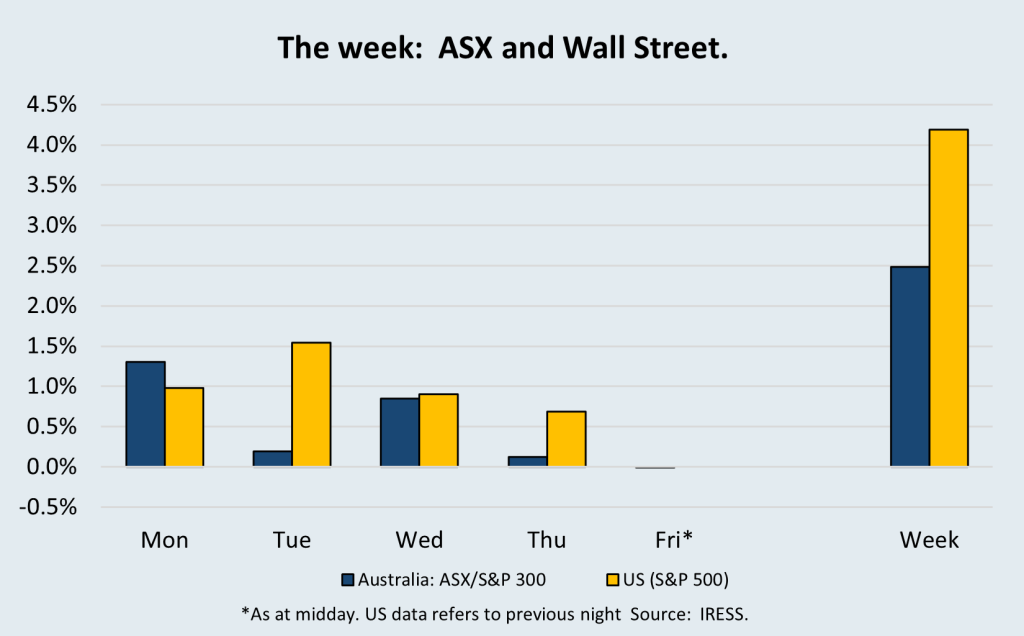

Equity markets have stabilised following four consecutive weeks of negative performance, with the ASX 200 rising approximately 2.5% over the week and above it’s most recent trough, last Friday.

Sector performance was mixed—resources gained 4.0% for the week, financials only added 0.4% while technology rallied 7% but remains 10% lower for the month. While volatility has moderated meaningfully, a deeper correction is still possible, given that valuations, liquidity conditions, and earnings expectations remain extended in our view. Having said that, many companies, including traditional large blue-chip companies, have given up considerable ground.

Despite a slight rebound, we suspect that investor positioning has not shifted back towards pure risk-taking.

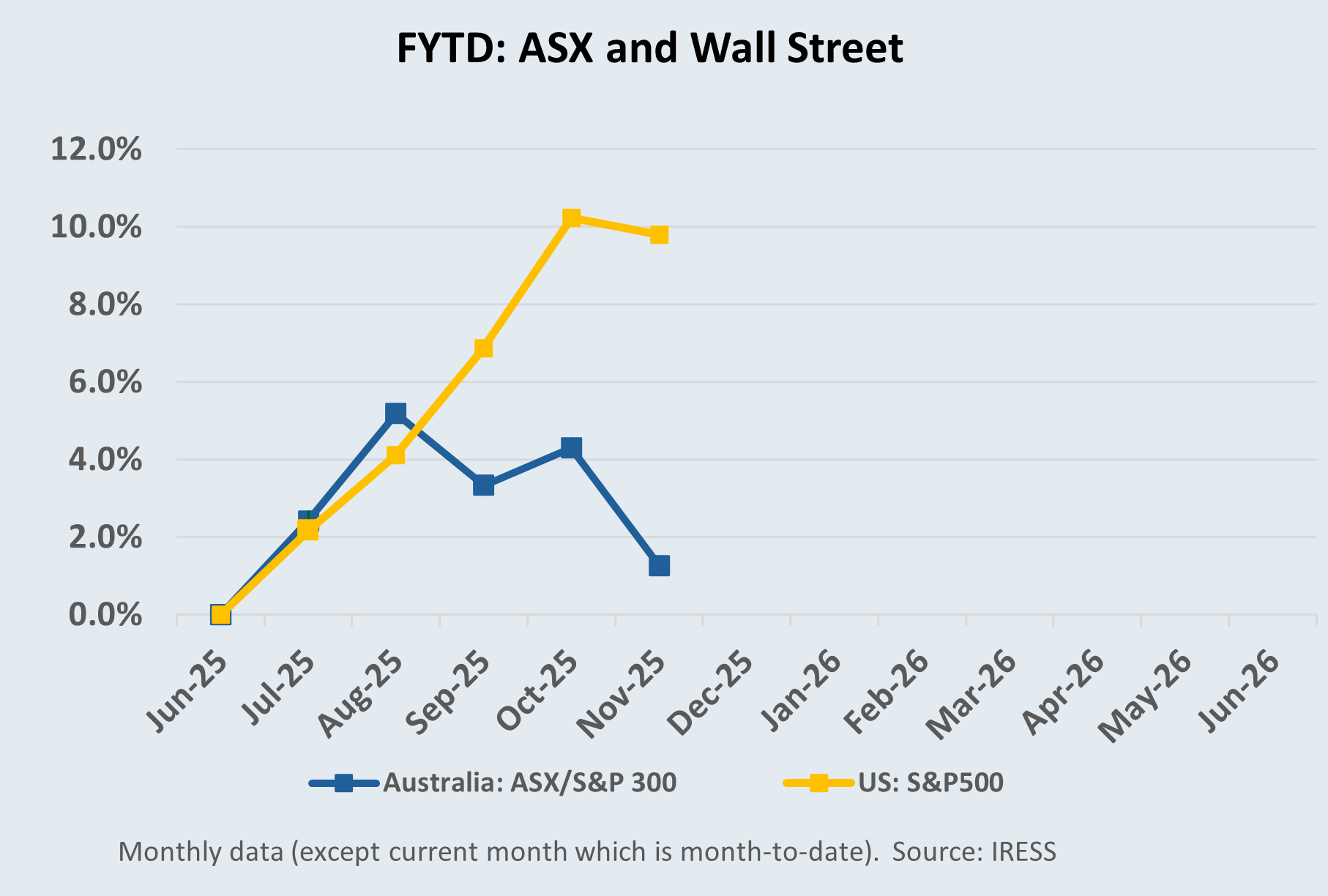

Some underlying trends warrant attention. The most notable momentum has been in Australian small caps since June 30th. The S&P/ASX Small Ordinaries (XSO) has delivered a total return of 14.8% since 30 June, materially outperforming the ASX 100 at 1.2%. Since the beginning of October, larger companies have fallen 2.5%, whilst the XSO has only fallen 0.4%.

Usually, such a divergence reflects (a) a rotation toward cyclical and domestically leveraged businesses, (b) improved capital markets activity, (c) easing funding pressures, and (d) a reassessment of growth prospects. Whilst these factors are important in this rotation, the biggest drivers have been the performance of smaller gold and materials companies, and the dramatic underperformance of banks, especially CBA.

While small caps remain below longer-term highs, their relative strength since year-end highlights renewed investor appetite and the potential for continued mean reversion as company-level fundamentals improve.

More bad news for mortgage holders and banks

The November ABS CPI release reinforced our long-held view that inflation in Australia remains more persistent than consensus expects. Headline CPI rose 3.8% year-on-year, ahead of economist forecasts and materially above the RBA’s target band, while underlying measures—particularly services, rents, insurance and food—continued to display stubborn momentum.

For several months, we have cautioned in Investment Matters that market pricing of rapid disinflation and early-2025 rate cuts was optimistic. This latest data again illustrates that inflation is proving higher and stickier than economists, financial markets and the RBA have anticipated.

Tradables and non-tradables inflation remain volatile, but the stickiness of the latter remains apparent. Core non-tradables inflation remaining high is core to our positioning in clients’ Australian equities sub-portfolios. It supports a higher level of cash on one hand, and a focus on idiosyncratic companies with pricing power as individual investments on the other.

As a result, the probability of near-term interest rate cuts has meaningfully diminished, and policy may need to remain restrictive for longer. Equity market implications are significant: banks, consumer discretionary, and other interest-rate-sensitive sectors appear overvalued relative to their earnings outlook, while companies with pricing power, stronger balance sheets, and structural growth drivers should remain favoured.

First Samuel Portfolio Positioning

First Samuel clients’ Australian equities sub-portfolios have also continued to outperform the broader index over the period, extending a consistent track record of benchmark-beating returns. This has been driven by deliberate sector positioning—greater exposure to small and mid-capitalisation companies, reduced weight in the major banks, and active participation in emerging industry trends.

Strong contributions have come from selected technology holdings, which have delivered gains on resilient earnings and expanding markets, as well as from gold producers benefiting from supportive commodity prices and improved operational performance.

News from Perth

Over the past week, your author undertook an extensive trip to Perth and regional Western Australia to meet with a wide range of portfolio companies, emerging investment prospects and industry participants. The visit provided valuable, first-hand insights into operating conditions across mining, energy, industrial services, infrastructure and agribusiness, as well as management perspectives on labour availability, cost pressures, capital allocation and demand outlooks.

These on-the-ground conversations remain a critical component of our investment process—testing assumptions, validating strategy, strengthening relationships and identifying new opportunities for clients. The following company summaries reflect the key observations and themes from that trip.

I have added small sections of information across a range of investments that may be in clients’ sub-portfolios. Note that some of the smaller opportunities are currently only in higher risk asset allocations, and others relate to sub-portfolios outside of Australian equities.

Aquirian Limited (ASX: AQN)

A small position in a limited number of clients’ sub-portfolios is a tiny company called Aquirian Limited. This position may grow and be more widely held as it continues to execute on its strategic agenda.

Figure #1: Wubin Energetic Hub

Source: Aquiran company presentation March 2025

Aquirian Limited’s medium-term growth profile is increasingly shaped by its ambition to develop Wubin into a strategic energy and mining services hub for Western Australia. Your author drove the 600km round trip to meet senior management for a solo tour of its Wubin Energetic Hub. The hub is leveraging its unique location and capacity to house explosive materials to build a diverse business.

Run by the impressive Greg Patching CEO, the team recently completed a 90-day evaluation of the site, confirming its suitability for multiple downstream activities beyond emulsion production—ranging from explosives manufacturing to integrated drill-and-blast solutions and associated logistics. That review has already produced meaningful strategic progress.

In December, Aquirian Limited executed a non-binding Framework Agreement with Hongda Civil Blasting Group Co., Ltd. to form a 50:50 joint venture to establish an electronic detonator manufacturing facility at Wubin. Hongda is one of the most advanced mining and civil explosive integrated service providers in China. It brings globally recognised capabilities in electronic blasting systems, advanced manufacturing processes and regulatory compliance.

Aquirian Limited contributes the strategically located site, established customer relationships, on-the-ground operating capability and a growing reputation as an independent supplier to WA miners. The JV structure enables shared capital and execution risk while accelerating market entry for both parties. Importantly, local production of electronic detonators would diversify a supply chain currently dominated by a small number of multinational incumbents—an outcome miners increasingly value from a cost, reliability and sovereign-security perspective. If fully implemented, the initiative would expand Aquirian Limited into higher-margin, technology-enabled consumables and would position Wubin as a genuine explosives-manufacturing precinct.

Aquirian Limited has also advanced a second strategic partnership, entering into an agreement with mine services group Topgroup to form the Drillforce WA joint venture. This follows a $2.3m strategic share placement to further align interests. The JV will combine Aquirian Limited ’s engineering IP—including its patented Collar Keeper® system used to stabilise blasthole cuttings, collars and pre-conditioned columns—with Topgroup’s substantial drilling capability, via its modern and well-maintained Topdrill fleet. Together, the parties aim to offer an end-to-end, capital-efficient drill-and-blast service to clients. For Aquirian, the structure is intentionally capital-light, monetising technology, systems expertise and customer relationships without requiring balance-sheet expansion into heavy equipment ownership. For Topgroup, it provides differentiated productivity and safety enhancements that can strengthen tender competitiveness and broaden service scope. In an environment where miners are seeking fewer contractors with broader capability and measurable performance outcomes, Drillforce WA appears strategically aligned with industry trends.

Our visit reinforced why Wubin sits at the centre of these initiatives. Located three hours north of Perth on the Great Northern Highway, it is the critical transition point where double road trains convert to triples before heading into WA’s major iron ore, gold and critical minerals regions. It has long functioned as a natural consolidation, servicing and logistics node for mining freight, and that role is being reinforced by ongoing infrastructure investment.

The Western Australian government is expanding the Main Roads changeover pad, adding 23 new bays to the existing 36, undertaking long-overdue repairs, formalising dolly parking and improving safety and traffic flow, supported by $2.5 million in state and federal funding. Linfox has also constructed a separate $3-million-plus changeover facility across the road, alleviating congestion.

For Aquirian Limited, being positioned adjacent to this infrastructure provides meaningful strategic leverage—shorter haulage distances, lower transport costs, improved delivery reliability during disruptions, and proximity to the trucking ecosystem that supports WA mining. When combined with the Hongda and Drillforce WA joint ventures, the company appears to be building not just an emulsion plant, but an emerging, multi-product hub capable of delivering explosives, drilling services and engineered blasting solutions to a wide range of mining customers. If execution continues as planned, Wubin could evolve into a differentiated supply and technology node for the state’s resources sector—one with increasing strategic value over time.

Emeco (ASX: EHL)

Our long-held position in Emeco Holdings has been a standout performer in FYTD26, with the stock up 60%. The company is proving that a combination of successful cash flow generation and improving market conditions can be rewarded

This visit to Perth we met with Emeco’s Chief Financial Officer, Theresa Mlikota, with the conversation centred on how the company is enhancing cashflow generation and using technology to strengthen its customer value proposition. Theresa outlined ongoing initiatives to improve working-capital efficiency, reduce maintenance intensity and direct capital only toward the highest-return fleet opportunities, supporting more predictable and resilient cash conversion.

At the same time, Emeco is investing in data, telemetry and fleet-performance technology to provide clients with clearer productivity insights and measurable cost outcomes, shifting the business toward a service-led offering rather than purely equipment rental. Combined with a continued focus on pricing discipline and balance-sheet improvement, these efforts aim to create a more differentiated, higher-quality earnings profile over time.

Emeco also delivered its AGM this week with limited new information provided.

Matrix Composites & Engineering (ASX: MCE)

Our visit to Matrix’s Henderson facility provided valuable insight into how the business is positioning itself for a more diversified and resilient earnings profile. We met with Chief Executive Officer Aaron Begley and Chief Financial Officer Brendan Cocks, who outlined a company benefiting from improved operational discipline, a clearer strategic focus and increasing momentum in tender activity. Demand across offshore energy—particularly LNG, deepwater and decommissioning—continues to recover after several years of global underinvestment, supporting a healthier pipeline for Matrix’s subsea buoyancy and advanced materials offerings.

The company’s IP, materials-engineering expertise and highly specialised manufacturing capability are increasingly relevant to defence, infrastructure and mining applications. Its location within the Australian Marine Complex (AMC) at Henderson is central to that strategy. The AMC is one of Australia’s most important defence and advanced manufacturing precincts, hosting major shipbuilding, sustainment and maritime technology programs and benefiting from deep-water access, heavy-lift infrastructure and co-location with primes, research organisations and specialist contractors.

This strategic significance will only increase under the AUKUS security partnership, which places Western Australia at the heart of future submarine sustainment, defence-industrial expansion and sovereign capability development. Being embedded in the AMC positions Matrix to participate in downstream opportunities—whether through direct manufacturing, component supply, systems integration or collaborative R&D—linked to AUKUS-related investment over the coming decades.

A key enabler of this long-term optionality is Matrix’s 35-year lease over a substantial, strategically located landholding within the core of the AMC. This asset provides operational security, expansion capacity and potential future value well beyond the company’s current activities. As defence and advanced manufacturing investment accelerates, the site could support a wide range of industrial uses, partnerships or co-located businesses, creating additional strategic and commercial pathways for Matrix.

With differentiated technology, increasing market breadth and a uniquely strategic footprint within a nationally significant defence-industrial precinct, Matrix is building a platform capable of generating meaningful long-term value.

Dirty Clean Food (DCFCN.UNL)

Dirty Clean Food, now operating independently following its separation from Wide Open Agriculture, continues to build momentum as a distinctive WA-based food business anchored in regenerative, provenance-driven sourcing. First Samuel clients are investors in the company through a preferred equity convertible note held within the Alternatives sub-portfolio, providing exposure to a strategically evolving, early-stage growth opportunity.

During our visit we met with Chief Executive Officer Jay Albany, who continues to impress across strategy, capital stewardship and execution capability. The business now generates more than $12 million in annual revenue, has reached profitability and is focused on scaling its multi-channel distribution network across supermarkets, specialty retail, hospitality and direct-to-consumer delivery.

While Dirty Clean Food offers a broad product suite, we were particularly impressed by the depth, traceability and operational sophistication of its meat supply chain, which remains the commercial and brand foundation of the company. Transparent relationships with farmers, tight cold-chain logistics and disciplined product standards create defensibility that is difficult for national competitors to replicate.

With rising consumer and food-service demand for sustainability, provenance and WA origin, the company is well positioned to continue expanding its footprint and brand presence over the coming years.

Summary

First Samuel portfolios have outperformed through deliberate sector positioning—more exposure to small and mid-caps, less weight in the major banks—and strong contributions from technology and gold holdings. To further test portfolio assumptions, we completed an extensive visit to Perth and regional WA, meeting with management teams across key investments.

Our discussions highlighted the strategic progress underway at Aquirian, operational and technological improvements at Emeco, growing diversification and optionality at Matrix Composites & Engineering, and the profitability and distribution expansion of Dirty Clean Food. These company-level insights continue to reinforce our long-term investment positioning.

The information in this article is of a general nature and does not take into consideration your personal objectives, financial situation or needs. Before acting on any of this information, you should consider whether it is appropriate for your personal circumstances and seek personal financial advice.