Copyright 2025 First Samuel Limited

Read the previous week’s Investment Matters.

The Market

What a manhole cover in Collins St says about Australia; current markets and AI

Overinvestment

This week’s Investment Matters examines the topic of AI investment within a historical framework of overinvestment and the misallocation of resources.

A rash of new investment in artificial intelligence in the US, especially by Nvidia, the chip-maker, and OpenAI, the owner of ChatGPT, has been announced in recent months. Investment in data centres and IT helps explain a significant portion of overall US growth in recent years. But markets have begun to concentrate on the financial engineering and cross-company relationships that funded this investment.

Data centres and chips

At the core of these trends are data centres and the semiconductor chips that they house.

The AFR Chanticleer article summarised it nicely.

“The circular nature of these deals has been much discussed, and rightly so. But let’s just consider the financial scope of what OpenAI has been able to do. According to the Financial Times’ estimate, the tech start-up has managed to sign deals worth approximately $US1.5 trillion, securing access to 26 gigawatts of computing power…

That’s a remarkable achievement at any level. But it’s even more remarkable given no one seems to have any idea as to how OpenAI will pay for the purchases it has signed up to.”

There is clearly a desire to invest; every AI query made today around the world requires vast computing resources. Each model is continually refined, and many companies are also developing new versions of AI tools to address new problems and capture market share.

No money to pay

However, even those that are best placed and seemingly most confident in the future profitability of the AI, currently have no money. Hence, we’re seeing quite contrived financial dealings to deliver actually growth rather than profitability. This reminds your author of similar periods of excess in the late 1990s and in the early 2000s.

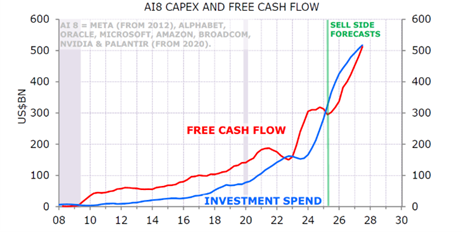

The following chart highlights that AI-related companies in the US are using all of their operating income (cash flow) to fund reinvestment in the opportunity of AI. The AI investment boom continues to accelerate.

Figure #1: AI Capex by Listed AI Companies expected to strengthen

Source: Minack Advisors, Bloomberg, NBER

Actual and forecast investment spending by the AI8 (Alphabet, Oracle, Microsoft, Amazon, Meta, Broadcom, Nvidia & Palantir).

While the chart above shows how currently profitable firms in search and advertising are using these profits to invest, this does not include the unlisted sector and the spending by OpenAI, which has received so much attention. Much of the unlisted investment is unfunded debt and appears to the author as little more than IOUs and empty promises. It is worthwhile noting that OpenAI is not a public company. Its financials are not publicly available.

OpenAI announced it would buy 10 gigawatts’ worth of chips from Nvidia, in return for which Nvidia would invest as much as $US100 billion in OpenAI. Instead of paying cash for the chips, Nvidia will give them to OpenAI in return for the promise of future profits. Not surprisingly, the details of the contracts that underpin such deals are rarely released!!

And to prove that OpenAI will take money and support from wherever it can be found. It announced it would buy six gigawatts worth of chips from AMD (a rival chipmaker), in return for which AMD would again receive OpenAI equity instead of cash.

To clarify, we are optimistic about the future wave of productivity that AI will ultimately unlock, and we also foresee AI tools being at least as essential as previous rounds of general-purpose technologies. Revenue from products such as Office 365 and document applications, like Adobe, provides some context for the potential revenue. But even the revenue generated by these success stories would struggle to justify the planned investment is currently being promised.

If everyone is buying, which companies are selling?

The answer appears to include a client sub-portfolio investment with the Macquarie Group. Based on the investment made over the last decade, they appear to be well-positioned in a period when players are desperate for capacity. Only time will tell if selling today is premature.

Still, we were thrilled by the announcement that it had sold a network of 50 data centres across North and South America to Global Infrastructure Partners and the Artificial Intelligence Infrastructure Partnership, a consortium including BlackRock, Nvidia, and Microsoft.

Aligned Data Centres was the Macquarie-owned and Texas-based firm it sold for $US40 billion ($A61 billion) in the asset class’s largest-ever deal. The markets expect that shareholders in Macquarie will benefit from significant fees and performance bonuses from the sale over the next 2 years.

The manhole cover?

Your author occasionally notices a manhole cover in Collins St that reminds one of another era in which overinvestment never caught up with demand, and companies were left with little.

Ironically, in a city that was also spectacularly expanded in the 1880s on a misconceived dream, and funded by overseas capital, the manhole cover with WorldCom still imprinted reminds us of another company that invested globally to build out infrastructure that was not utilised for decades.

Figure #2: Examples of WorldCom manhole covers still litter global cities

Source: Facebook

WorldCom was a major U.S. telecommunications company that became infamous for one of the largest corporate accounting scandals in history. The fraud led to its spectacular bankruptcy in 2002. The company grew rapidly through aggressive acquisitions of other telecom firms. By the late 1990s and early 2000s, WorldCom had become a giant in the industry, expanding beyond just voice calls to become the world’s largest carrier of internet traffic.

Ultimately, the issue was that many companies overinvested simultaneously, creating a glut of fibre with little real demand. One analyst estimated in 2004 that only about one-tenth of the installed fibre was actually being used.

This lack of demand and lack of renewal is the reason why the manhole cover in Collins St still says WorldCom!!!

In 2025, so early in the AI investment cycle, it is almost impossible to determine if the rosy projections of future requirements also prove to be overstated. What is clear today is that there isn’t yet the revenue from AI services to support the AI infrastructure.

In the early 2000s, expensive voice calls ultimately funded overinvestment. Today, is it expensive search and doom-scrolling on Facebook and Twitter the source of the future AI machines? Perhaps.

Clients’ international securities sub-portfolio positioning is tilted away from the largest AI-related companies. Instead, we are more concentrated in global indices that will benefit from the real-world applications of these technologies over the next two decades.

Impressive capacity to mobilise capital

Regardless of the financing and the questionable economics, we are still hugely impressed by the United States’ capacity to mobilise capital.

The “Stargate” facility in Abilene, Texas is a huge investment built on the promise of artificial intelligence (AI) and its projected infrastructure needs. A joint venture between OpenAI, Oracle, SoftBank, and investment firm MGX, it is aiming to build massive data centre campuses across the U.S. The Abilene campus is being built on a footprint of approximately 900 acres (or more) and is intended to deliver 1.2 gigawatts (GW) of power upon completion.

Figure #3: Stargate: It is always bigger in Texas

Source: OpenAI

Why is so much power required today, and why is the amount planned so large? The simple graphic below illustrates that, at a minimum, current ChatGPT queries alone require power equivalent to that of approximately 30,000 homes. Many alternatives to ChatGPT also need powering, and the applications of this technology are just beginning to be developed.

Figure #4: ChatGPT Queries all users per year & Electricity Required

Source: ABS, UBS

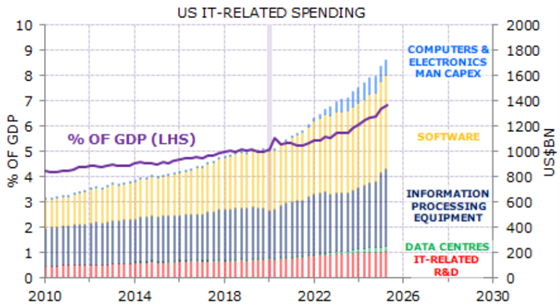

The scale of US investment is clear across the economy in the following chart, with acceleration since COVID across manufacturing (Man Capex), equipment, data centres along with Software.

Figure #5: US IT-related Spending

Source: Minack Advisors

Lessons from history

More than a century ago, the railroad was the most transformative technology of its era, promising to shrink distances and open up vast new territories to commerce. This stimulated heavy industries, such as steel, created a national market, and became a powerful symbol of progress.

The construction of rail lines became an obsession for investors and entrepreneurs. During the “Gilded Age,” in the US, railroad companies were funded by a mix of private investment, government land grants, and subsidies. Investors poured money into new lines, often based on speculation rather than proven demand.

In Victoria, the Railway Construction Act 1884, also known as the Octopus Act, was promoted by the legendary Thomas Bent (“Bent by name and bent by nature”) of Bentleigh and Brighton fame. The Act authorised the construction of 59 new railway lines in the colony.

The results in Victoria and the US alike were characterised by political interference, dubious financial dealings, and ultimately, significant overcapacity.

The reason over-capacity often results is that success frequently comes from the relentless logic of economies of scale. Driving out competition, controlling the supply and distribution chains, and keeping wages as low as possible have often underpinned the emergence of new general-purpose technologies in the past.

As an investor, finding a balance in new investment opportunities in this environment is possible if we avoid the hype.

As a nation, balancing demands is much more difficult. We contend that in the Australian case, being the recipient of others’ overinvestment can be enormously profitable for a small-open economy such as Australia. In a similar way to the 1880’s being funded by Scottish Pension Funds, our fibre was funded by global telco companies twenty years ago. In 2025, AI tools that we all access in a globally connected world are now funded by US companies and the global debt market.

Whilst we may not need to fund these evolutions, we do need to maintain a vital reform agenda to make the most of the change. In our view, this is the most significant risk. To date, Australia has chosen labour over additional capital investment.

Will our companies soon invest?

Australia: Doing less also has implications

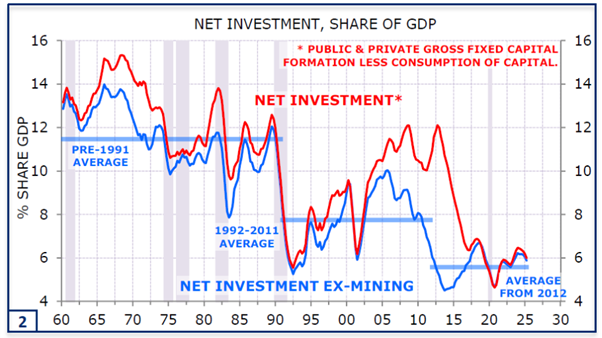

The chart below shows that we continue to struggle with underinvestment by businesses in the face of excess concentration.

Figure #6: Australia stopped investing

Source: Minack Advisors

Since the period of underinvestment began in 2012, we have chosen to maintain moderate economic growth by offsetting lower levels of investment with higher population growth. But it may not have added significantly to the depth of skills, and it almost certainly generated higher growth than anticipated.

The August 2025 “International Students Pathways and Outcomes Study” by the Australian Government and Jobs and Skills Australia assessed how education-driven migration is shaping the economy. It identified three key concerns:

- Higher-than-expected retention – Twice as many international students remain in Australia as policymakers anticipated, driving stronger population growth and, indirectly, suppressing wage growth while adding to inflationary pressure.

- Unclear national objectives – The pursuit of tuition revenue has blurred the sector’s broader purpose. The report’s first recommendation urges a shared national framework linking international education to both total economic output and long-term skills development goals.

- Weak employment outcomes – More than half of graduates work below their qualification level, with many earning substantially less than domestic peers. Business graduates, for instance, earn a median $56,900 versus $115,000 for Australians, suggesting the system functions more as a low-wage migration channel than as a skilled-workforce strategy.

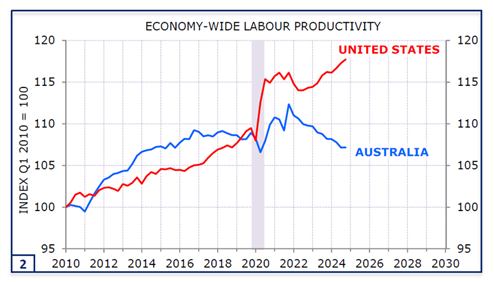

This low-wage, labour-dependent, and capital-depleting process has accelerated since the Covid pandemic. Although the outcomes are unlikely to be the direct result of the stated policies of government and business, the chart below illustrates how far we have diverged from the US in terms of both investment and productivity outcomes.

Figure #7: Significant divergence in productivity outcomes between US and Australia

Source: Minack Advisors

The AI revolution provides an opportunity for policy to re-engage in driving investment and productivity as a necessary part of building an economy for future generations, which in turn, for investors, creates an economy with a range of opportunities to deploy savings.

When capital misallocation is nationwide

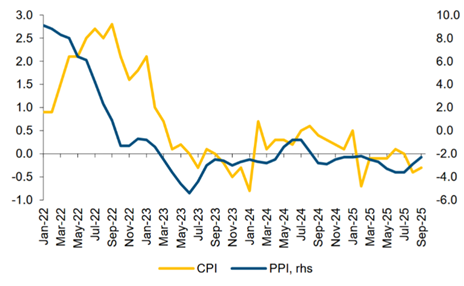

And finally, we note that this week provided further proof that capital misallocation is the risk markets now face. China is struggling with legacy of capital misallocation. Much of this misallocation benefits Australia through high commodity prices, and imported deflation in consumer goods which together provided an entire generation with low inflation, low interest rates, higher asset prices and enhanced public spending and lower taxes.

Figure #8: China Consumer Price Index (CPI) and Producer Price Index (PPI)

Source: ABS, UBS

For more than three years, an oversupply of domestic production, especially in the face of weak population growth, has led to falling prices (deflation) in China. China is actively working to mitigate this deflationary force through additional controls. Ultimately, we believe this provides risks to global inflation.

The information in this article is of a general nature and does not take into consideration your personal objectives, financial situation or needs. Before acting on any of this information, you should consider whether it is appropriate for your personal circumstances and seek personal financial advice.