Copyright 2025 First Samuel Limited

Read last week’s Investment Matters.

The Market

Are you sure that was only one year?

At Investment Matters, we spend a great deal of time on company updates and outlining our expectations for the future. At year’s end, we step back and review a fascinating year.

Our overall take – “Are you sure that was only one year!”

It is still less than twelve months since President Trump was sworn in, and barely a year since his election. Global tariffs were reintroduced in 2025, gold started the year in the mid $ 2,000 USD range, and the RBA was widely expected to reduce interest rates for several years.

Along with the heightened political uncertainty, abrupt policy shifts and market behaviour that at times appeared disconnected from fundamentals, only to recover in the following months.

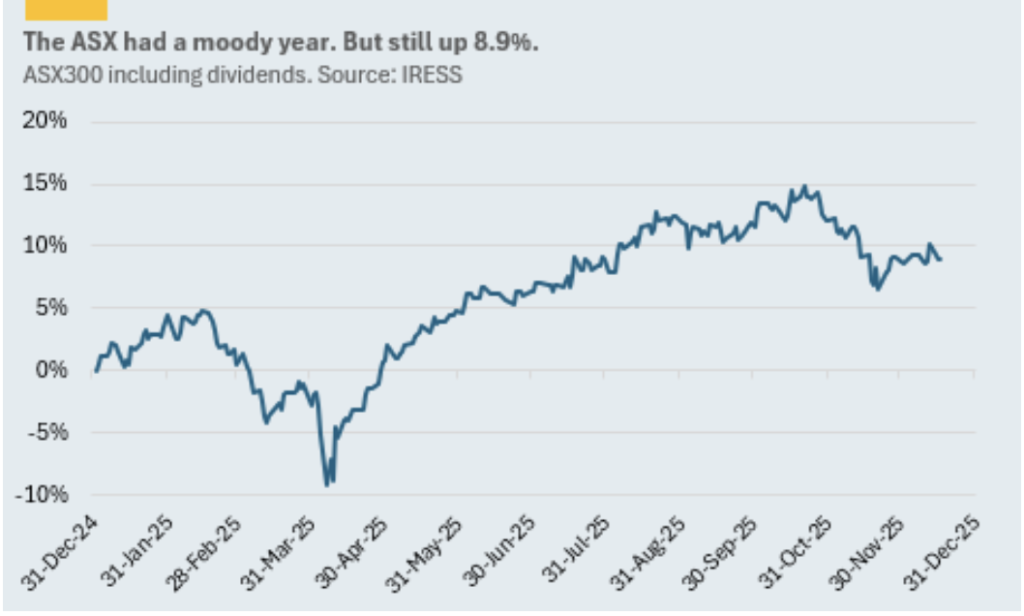

Despite it all, 2025 has been a positive year for Australian equities, with the ASX S&P 300 delivering a total return of 8.9 per cent, comprising 5.6 per cent capital growth and 3.3 per cent in dividends.

#1: Australian market, ASX300 including dividends in 2025

Source: IRESS

While this outcome is in line with long-term expectations in absolute terms, it understates both the volatility experienced during the year and the huge dispersion beneath the surface. One third of ASX300 stocks returned more than 25%, whilst another third had negative returns, highlighting the importance of stock selection and portfolio construction.

Against this backdrop, First Samuel client portfolios have performed materially better than the index, reflecting disciplined portfolio construction, selective risk-taking and an ongoing emphasis on valuation. The dispersion in our portfolios below the surface was lower than the market’s, with a higher share of strong performers and fewer detractors.

In this week’s Investment Matters, we highlight our five favourite themes to review 2025.

Theme 1: The Liberation Day Sell-Off – Sharp, Global and Short-Lived

The Liberation Day (i.e. Trump’s tariff announcement) sell-off was notable, not just for its speed but for its global reach. Equity markets across regions moved lower in unison, risk premia widened, and defensive assets outperformed. Bond markets also repriced as investors reassessed inflation risks, growth expectations and policy credibility.

In Australia, the market drawdown was swift. Figure #1 above shows the sharp sell-off and reversal in April 2025. Export-oriented companies, global industrials and parts of the resources sector were particularly affected, while domestic defensives and income-oriented stocks proved relatively resilient. That said, few areas of the market were untouched.

Crucially, as the initial shock faded, investors began to differentiate between headline risk and economic reality. While tariffs represent a tax on trade and efficiency, their direct impact on Australian corporate earnings is uneven and, in many cases, second-order. As this distinction became clearer, markets stabilised and subsequently recovered much of the lost ground.

For First Samuel portfolios, this period was characterised by specific reallocations. We felt the sell-off provided an excellent opportunity to increase our technology exposure to names including Block and Life360. We also selectively increased exposure to businesses with strong balance sheets and durable earnings, while avoiding those with short-term earnings at risk due to global uncertainty. These included Seek, Reliance Worldwide and BlueScope Steel.

We noted at the time that Liberation Day was more about geopolitics than economics, and this has played out over the year. Markets are now coming to terms with how long these measures will remain in place. In the meantime, global companies are learning to diversify supply chains, increasing reshoring, and investing in AI to reshape operations. In our view, these measures are making global business more resilient.

We suspect history will note 2025 and the tariff disruptions as the building blocks of future returns and productivity.

Theme 2: Gold – Insurance That Paid Out

One of the defining asset-class stories of 2025 was gold. The gold price rose from approximately US$2,600 per ounce to around US$4,300 per ounce, reflecting a combination of geopolitical uncertainty, concerns around fiscal sustainability and a desire by investors and central banks to diversify away from traditional fiat currencies.

Figure #2: Gold price 2025

Source: macrotrends.net

For First Samuel clients, this outcome was consistent with our long-held view of gold as portfolio insurance rather than a speculative asset. Gold’s value lies not only in its return potential, but in its tendency to perform when confidence in policy frameworks, currencies or financial stability is undermined.

The events of 2025 provided a clear illustration of this role. As equity markets sold off following Liberation Day, gold moved higher, providing both protection and optionality. Significantly, its benefit was magnified by its low correlation to risk assets during periods of stress.

Seeing the gold price rise does not guarantee profits; we still need exposure to quality gold miners. Highlights in 2025 in the portfolio included Newmont Mining, the world’s largest gold miner and emerging players such as Catalyst Metals. This company took an existing operation that had suffered from underinvestment and built a regional success story. The portfolio also included Minerals260, a gold miner that is currently not producing any gold but has projected significant future profits from the resources it is successfully developing through drilling and feasibility studies.

Theme 3: CBA and June 30th Big Caps Euphoria

One of the more unusual features of the Australian equity market in 2025 was the behaviour of large capitalisation stocks in the lead-up to 30 June. Rather than fundamentals driving relative performance, index mechanics, capital flows and investor behaviour appeared to play an outsized role. Nowhere was this more evident than in Commonwealth Bank of Australia.

Figure #3: Various returns including CBA – First 6 months, since June 30th and overall returns (including dividends)

Data has been rounded. Source: Emeco Investor Day Presentation, Dec 2025

CBA became the most discussed equity story of the year as its share price rose above $190 per share in late May 2025, briefly making it the most expensive major bank in the world on conventional valuation metrics. This outcome was extraordinary, not because of a sudden improvement in earnings or returns, but because it appeared increasingly disconnected from underlying fundamentals.

A range of explanations was offered. Some pointed to mechanical index buying, as CBA’s growing index weight attracted passive inflows. Others highlighted the behaviour of large superannuation funds, where scale, liquidity constraints and benchmark sensitivity can concentrate capital into the largest names regardless of valuation. Momentum and investor euphoria also played a role, reinforced by the perception of CBA as a safe, defensive asset in an uncertain global environment.

Whatever the mix of drivers, the episode highlighted how price-insensitive capital can distort outcomes, particularly in heavily owned large-cap stocks. These distortions are often most visible near reporting and financial year-end periods, when portfolio positioning and relative performance pressures intensify.

What made the episode particularly striking was how it resolved. Despite its extraordinary rise into June, CBA finished the year as an underperformer, delivering returns below the broader market. One of the most talked-about stocks of 2025 ultimately served as a reminder that valuation still matters.

Theme 4: Resources Reassert Themselves – Geopolitics, Scarcity and Supply Discipline

If 2025 will be remembered for one sector in particular, it is the mining and resources sector. After a 14% decline in 2024, the ASX S&P 300 Mining Index (including dividends) rose 34% in 2025, marking a decisive reversal in sentiment. This recovery reflected a reassessment of the strategic importance of resources in a world facing increasing geopolitical tensions, constrained supply, and higher marginal production costs.

Gold stocks are included in the Mining Index and are essential to overall performance. Still, we saw above-index returns from Rio Tinto and BHP, the sector’s largest companies.

‘Rare earths’ emerged as a clear geopolitical flashpoint. As governments increasingly framed supply chains through a national security lens, access to critical minerals shifted from a commercial issue to a strategic priority. In this environment, Lynas Rare Earths stood out as one of the few large-scale, non-Chinese producers, with its share price rising 93% over the year.

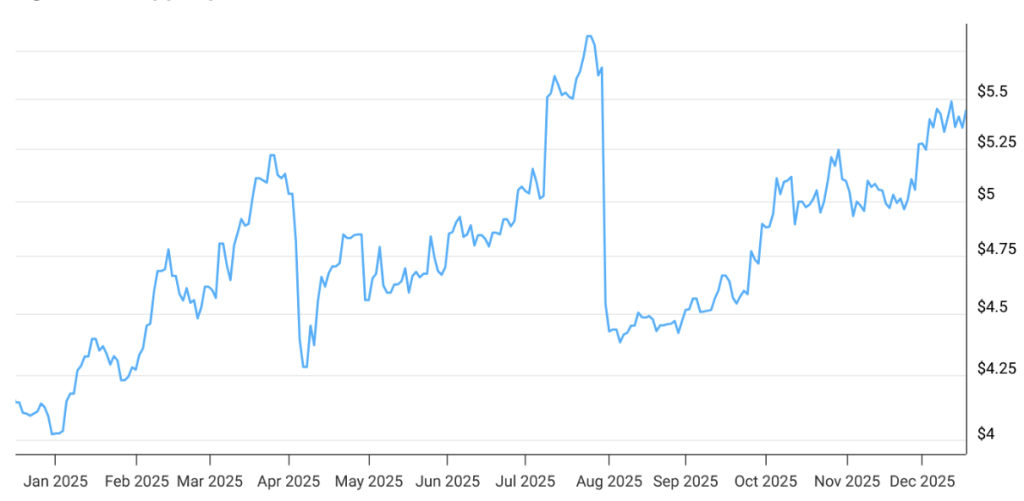

Copper was another standout; see Figure #4 below. The copper price rose from around US$4.00 per pound at the start of 2025 to approximately US$5.30 per pound by year end. This move reflected the collision of long-term trends—declining ore grades, rising capital intensity and higher operating costs—with near-term supply disruptions across key producing regions. Note the spike in copper prices in July related to Trump copper tariff measures.

Figure #4: Copper price 2025

Source: macrotrends.net

For copper producers, the earnings leverage was significant. Portfolio companies such as Sandfire Resources benefited materially, with Sandfire’s share price rising approximately 80% during the year. This performance reflected not only higher prices, but also improved operational execution and balance-sheet strength following several years of investment.

Other battery-related minerals also contributed positively. Lithium, which had been under pressure earlier in the cycle, staged a late-2025 recovery as supply growth slowed and demand expectations stabilised. While volatility remains a feature of these markets, 2025 reinforced the importance of well-positioned resource assets in diversified portfolios.

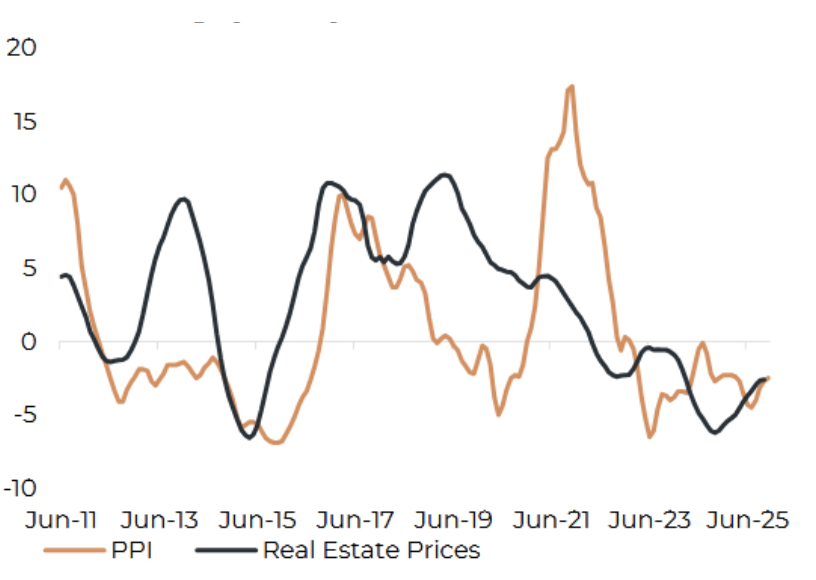

Heading into 2026, the big question for the Miners relates to China’s uncertain economic outlook. China’s economy thrived on excess investment, excess capacity, and apparently unlimited money printing. This strategy has proven to be fabulous for companies such as BHP and Rio, which have supplied materials for the past three decades. But investment in China is now slowing, producer prices (PPI) are falling, and so are Real Estate prices (see figure below). Ore prices in 2026 are at risk.

Figure #5: China’s economy is still struggling with excess capacity, per cent change year on year

Source: NBS, Macrotrends, Barrenjoey Research

Theme 5: Artificial Intelligence (AI) – Exuberance Today, Productivity Tomorrow

Artificial intelligence was one of the most powerful forces shaping global equity markets in 2025. Capital flowed rapidly into AI-related infrastructure, computers, data centres and semiconductor supply chains, with valuations often reflecting optimistic assumptions about future demand and profitability. Yet at this early stage of the investment cycle, it remains challenging to distinguish enduring value creation from speculative excess.

In recent weeks, Investment Matters has noted similarities to the telecommunications fibre-optic cabling build-out in 1999 and to Japanese financial engineering in the late 1980s. Another parallel is the US Railways in the late 19th century.

Former RBA central banker turned investment adviser Guy Debelle has offered a useful historical analogy, likening today’s AI build-out to the construction of railways in the United States during the 1800s. While the railways were transformational, Debelle notes, “the companies building the railways did not make all the money – it was the people using the railways who made the money.” This distinction is critical when assessing where long-term returns from AI are most likely to accrue.

In 2025, the scale of planned AI infrastructure investment will far exceed the revenue currently generated by AI services. Even companies that appear best positioned and most confident about future profitability are, in many cases, not yet generating meaningful cash flows from AI. As a result, we are seeing increasingly contrived financial structures, circular financing arrangements, and growth narratives prioritised over profitability.

None of this diminishes the long-term potential of AI. We are optimistic about the productivity gains AI will ultimately unlock and view it as a general-purpose technology on par with earlier waves such as electrification or computing. Existing revenue models—such as Office 365 or Adobe’s document applications—provide some context for what successful monetisation might look like. However, even these examples would struggle to justify the scale of investment currently being promised across the AI ecosystem.

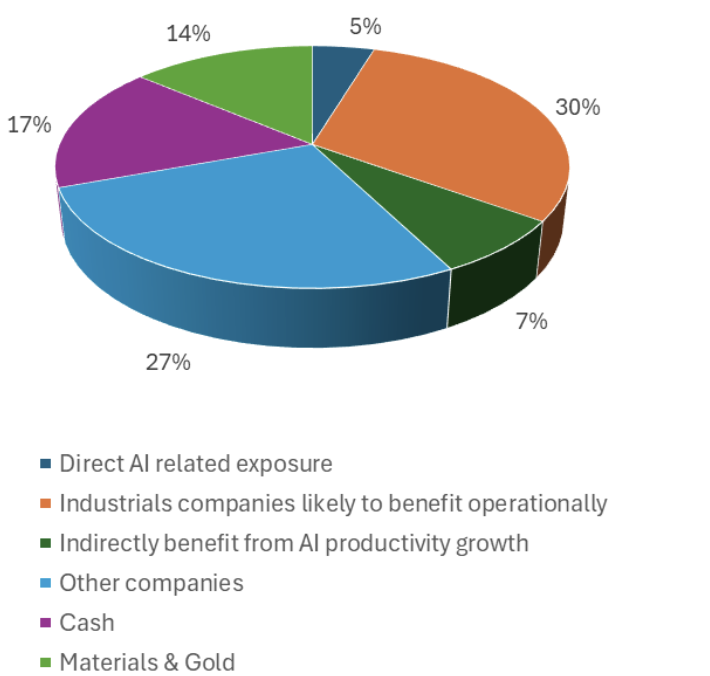

The Australian equity market remains relatively under-exposed to AI infrastructure, with direct exposure primarily limited to NextDC and other data centres, as well as a small number of technology companies, including TZ Limited.

Broader exposure exists through businesses such as Life360 and Block (ASX Code: XYZ), where AI is expected to sit at the core of product development and customer interaction. In aggregate, we estimate that approximately 5% of Australian equity portfolios are directly AI-related.

At First Samuel, the AI theme is deliberately twofold. Firstly, we favour companies we believe can become materially more efficient and competitive through AI adoption, including Worley, Cleanaway, Seek, and healthcare providers IDX and Healius. Secondly, we invest in businesses that can indirectly benefit from their customers’ adoption of AI, including EarlyPay, Challenger, Woolworths and Paragon, where we see particularly durable gains in areas such as supply chain optimisation.

The figure below shows an approximate breakdown of our portfolio exposure. We are of the view that we need to concentrate on those companies that will benefit operationally, and those that will benefit indirectly from medium-term AI productivity. Similar to the market overall

Figure #6: First Samuel Australian Equity approximate exposure to AI

Source: First Samuel

In short, while AI is likely to reshape the global economy, history suggests that patience, selectivity and a focus on users—not just builders—will be critical in translating technological promise into sustainable investment returns.

In International markets, especially in the US, exposure to AI is much higher. The five most prominent tech companies heavily invested in AI (Apple, Nvidia, Microsoft, Alphabet, and Amazon) collectively account for nearly 30% of the entire S&P500 value, and this in turn is 70%+ of the MSCI Global index by market capitalisation. Hype in this narrow range of companies is part of the reason why we have increased our non-US large-cap exposure.

Summary

2025 has been a successful, challenging, and volatile year. The massive trends of 2025, Gold, and Artificial Intelligence and the politicisation of materials have driven value for clients.

It would be comforting to presume that 2026 will be more straightforward, that markets and companies will face less change. We could assume that geopolitics and government will play a lesser role. But that strategy will disrespect the creative destruction processes that generate value. As noted by the successful investor and academic Robert Arnott, “In investing, what is comfortable is rarely profitable.”

Have a fabulous festive season and best wishes for a productive 2026.

The information in this article is of a general nature and does not take into consideration your personal objectives, financial situation or needs. Before acting on any of this information, you should consider whether it is appropriate for your personal circumstances and seek personal financial advice.